CFOs Guide: How to Improve Cash Flow

Learn practical steps on how to improve cash flow, from forecasting to optimization, that CFOs can apply now to strengthen liquidity and drive growth.

The gap between profit on the books and cash in the bank is a familiar problem for professional services firms. A strong P&L is good, but it doesn't fund payroll. This disconnect is almost always rooted in the operational drag of an inefficient accounts receivable cycle.

The Real Reason Your Profits Aren't Showing Up as Cash

This isn't an issue of a few late-paying clients. It’s about systemic friction: manual invoicing, inconsistent follow-ups, and a lack of real-time visibility into your receivables.

The symptoms are predictable: strained vendor relationships, delayed strategic investments, and the constant, low-grade stress of meeting payroll obligations.

Shifting from Theory to Operational Reality

Forget abstract financial models. The challenge is tangible and operational. The problem isn’t a lack of effort from your finance team; it's the absence of a scalable, systematic process.

When your team manually tracks invoices, sends reminders, and reconciles payments, it creates bottlenecks. Those bottlenecks directly constrain your cash conversion cycle. This guide offers a clear, operator-focused playbook for regaining control.

The core issue lies in the gap between service delivery and cash collection. Every manual touchpoint widens that gap, creating delays that compound. The solution isn't to chase harder—it's to fix the process.

This focus on operational health is critical. According to Aon's global risk analysis, cash flow and liquidity risk has re-entered the top 10 global business risks, a position it hasn't held since before 2019, driven by economic volatility and inflation.

While 81% of companies claim to have a plan for this risk, nearly a third still suffered related losses. That signifies a major disconnect between planning and execution. The full findings are available in Aon's global risk analysis.

The True Cost of Inefficient AR

Inefficient accounts receivable is a direct brake on growth. The costs are measurable:

- High Days Sales Outstanding (DSO): Every day an invoice sits unpaid, your firm finances your clients' operations. A high DSO is a direct measure of this financial drag. For a $10M firm with a 75-day DSO, a 10-day reduction frees up over $270,000 in cash.

- Wasted Team Capacity: Manual AR burns valuable hours that should be spent on strategic financial analysis, not repetitive email reminders.

- Inaccurate Cash Forecasting: Without a systematic collections process, predicting cash inflows is guesswork, making strategic planning nearly impossible.

This guide provides a structured approach to diagnosing these issues and implementing targeted fixes, from quick wins to foundational shifts like accounts receivable automation, that will permanently improve your firm’s liquidity.

How to Find Your Hidden Cash Flow Gaps

Relying solely on Days Sales Outstanding (DSO) provides an incomplete picture. It confirms cash is slow but doesn't explain why. A proper diagnosis requires digging deeper to find the actual friction points, swapping assumptions for data.

Go Beyond the Standard DSO Metric

To get an actionable view of your accounts receivable health, supplement DSO with more precise KPIs.

- Collection Effectiveness Index (CEI): This measures what you actually collected versus what was available to collect in a given period. A CEI consistently below 80% indicates a systemic collections problem that DSO might obscure.

- Average Days Delinquent (ADD): This metric isolates how many days your invoices are past due, on average. It separates collections performance from your contractual payment terms, providing a pure measure of follow-up effectiveness.

A firm tracking both CEI and ADD can quickly determine if it has a collections problem (low CEI) or a payment terms problem (high DSO but low ADD). This clarity ensures you fix the right issue. These KPIs shift the conversation from "how long does it take?" to "how effective are we?"

Segment Your Receivables for Deeper Insights

Analyzing total AR in aggregate masks the real story. Segment your receivables to identify where delays originate. Slice the data by:

- Client Tier: Are your largest clients your slowest payers? It’s a common scenario where preferential treatment inadvertently trains them to pay late.

- Service Line: Do invoices for consulting projects age out faster than recurring retainers? This may signal issues with project sign-offs or billing clarity for that service.

- Invoice Size: Small, unmanaged invoices can create significant cash drag. Conversely, large invoices may require a different follow-up approach to navigate complex client approval chains.

This segmentation turns a vague problem like "Our DSO is 60 days" into a specific, solvable one: "Invoices over $25k for our strategy engagements are averaging 85 days to pay." Now you have a clear target for intervention.

Key Cash Flow Diagnostic Metrics

Metric | Calculation | What It Tells You |

|---|---|---|

Days Sales Outstanding (DSO) | | The average number of days it takes to collect payment after a sale. |

Collection Effectiveness Index (CEI) | | How effective you are at collecting receivables during a period. A score below 80% is a red flag. |

Average Days Delinquent (ADD) | | The average number of days invoices are past due, isolating collections performance from payment terms. |

Accounts Receivable Turnover Ratio | | How many times per year you convert your receivables into cash. Higher is better. |

Tracking these metrics provides a multi-dimensional view of AR performance, moving you beyond a single, often misleading, number.

Audit Your Upstream Processes

Slow payments are often a symptom of upstream problems. Friction in your process—from the initial statement of work to final invoicing—is a common culprit. Review the entire client financial journey.

Are your invoices confusing? Is your project sign-off process clunky? Consider seeking strategic guidance from an outsourced CFO to spot operational blind spots.

These small inefficiencies are often the root cause of a lagging cash cycle. Digging into the true cost of AR inefficiency in professional services can reveal how these minor drags compound.

Prioritizing Fixes for Immediate and Long-Term Impact

Once you’ve diagnosed the why, the focus shifts to execution. A sequenced plan that delivers quick wins first, then builds momentum toward sustainable change, is the most effective approach. Resist the temptation to fix everything at once.

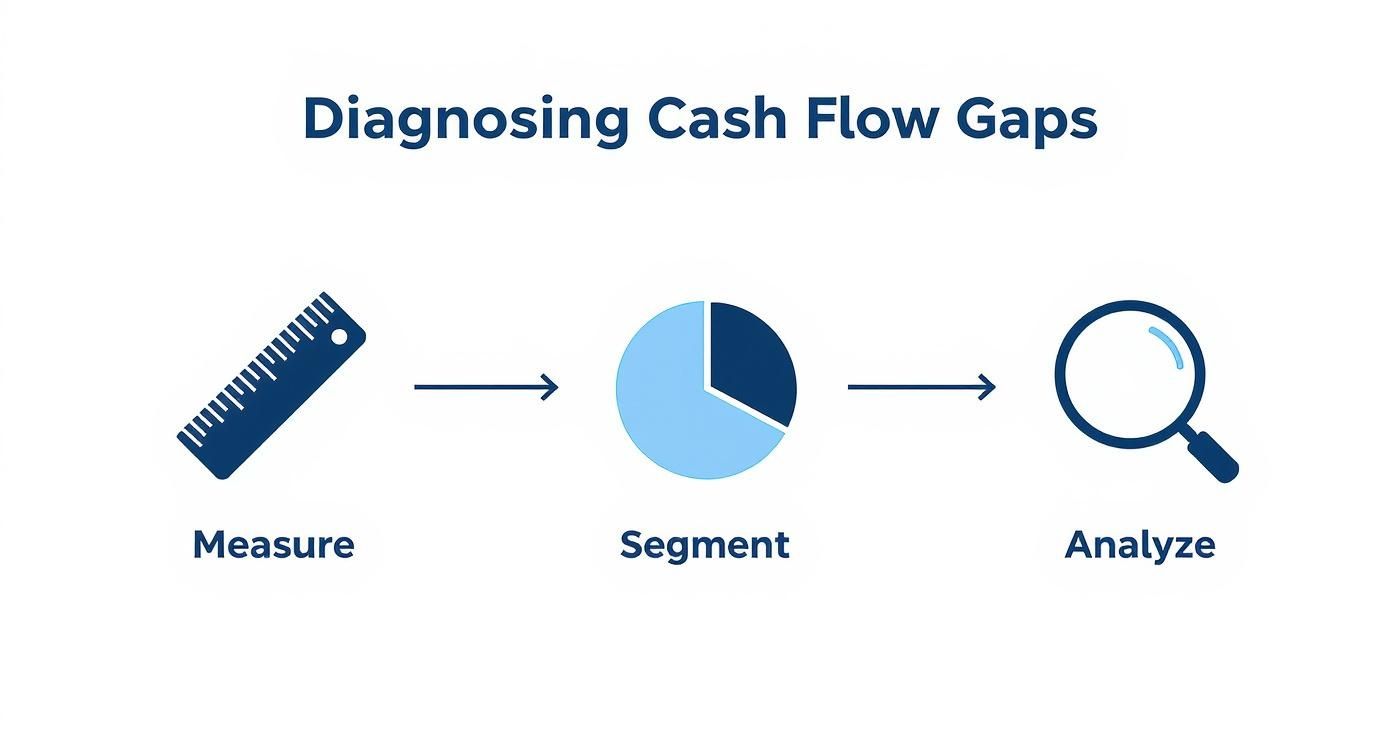

This simple flow—measure, segment, analyze—prevents reactive problem-solving and targets the actual behaviors or process flaws causing delays.

Phase 1: Quick Wins to Unlock Cash Now

Prioritize simple, low-effort changes to free up cash in the next 30 to 60 days. These tweaks require minimal resources but have a disproportionate impact on payment speed.

Start with the invoice itself. Is the due date clearly visible? Are payment instructions concise? A simple redesign for clarity can often shave 3-5 days off your payment cycle.

Next, standardize communications. Create professional, concise email templates for each stage of delinquency (7, 15, and 30 days past due). Consistency removes guesswork for your team and sets clear expectations for clients. For more ideas, see these eight real-world ways to clean up your accounts receivable.

Phase 2: Medium-Term Projects for Process Control

With quick wins secured, focus on structural improvements that create lasting efficiency. These projects, typically rolled out over one or two quarters, formalize your collections strategy and remove systemic friction.

The highest-impact initiative in this phase is expanding payment options. If you only accept checks or wire transfers, you are making it harder for clients to pay you. Adding ACH and credit card payment links directly to your invoices can reduce DSO by 10-15% on its own. It removes the most common excuse for late payment.

This is also the time to establish a formal collections escalation path. Define clear triggers for action:

- 30 Days Past Due: Automated reminder sequence continues.

- 45 Days Past Due: Account is flagged for a personal phone call from the finance team.

- 60 Days Past Due: Project manager or partner is alerted to contact their client counterpart.

- 90 Days Past Due: A final demand letter is sent, and the account is reviewed for third-party collections.

A structured process ensures no account is overlooked and removes emotion from the collections workflow.

Phase 3: Foundational Fixes for Long-Term Resilience

The final phase builds a resilient financial operation by addressing root causes with technology and policy.

First, tighten your client credit policies. Conduct proper credit assessments before signing new clients. Set clear credit limits and review them annually. A disciplined onboarding process is your best defense against future payment issues.

This is the logical point to implement accounts receivable automation. Manual follow-up is prone to human error and doesn't scale. Modern AI AR automation platforms manage the entire collections workflow, from sending personalized reminders to escalating at-risk accounts.

For firms on QuickBooks, dedicated QuickBooks AR automation tools add a layer of operational intelligence the core software lacks. This is not about replacing your team; it’s about equipping them with tools to handle repetitive work so they can focus on high-value client relationships and financial strategy. Implementing AR software for professional services is the final step in shifting from reactive collecting to a predictive, controlled cash flow system.

Implementing AR Automation Without Disrupting Your Firm

Implementing accounts receivable automation is not about replacing finance staff. It is about providing leverage. The objective is to shift their focus from repetitive, low-impact tasks to high-value analysis and client relationship management.

How Automation Augments Your Team

Modern AI AR automation platforms handle the critical but relentless work that consumes your team's day: sending timed payment reminders, flagging at-risk accounts, and projecting cash inflows with greater accuracy than a spreadsheet model.

This frees up your personnel for work that requires human judgment. Instead of chasing invoices, they can analyze payment trends, resolve complex client disputes, and strengthen relationships with key accounts. The system handles the repetitive tasks; your team executes strategy.

A Roadmap for Selecting the Right AR Software

Choosing the right platform is critical. Focus your evaluation on a few key criteria to ensure the software aligns with your firm's operational needs.

Seamless integration with your accounting ledger is non-negotiable. For many firms, this means native QuickBooks AR automation. The system must sync flawlessly to avoid creating new manual reconciliation tasks.

Next, evaluate customization. Professional services firms require tailored AR processes. The platform must allow you to define different dunning cadences and messaging for different client segments. The communication for a strategic partner should differ from that for a smaller, transactional client.

Finally, insist on an intuitive user interface. A platform that is difficult to navigate will not be fully adopted by your team. Look for clear dashboards and actionable insights. For a deeper analysis, consult this guide to accounts receivable automation software.

Moving from Reactive Collections to Predictive Control

A well-implemented AR software for professional services enables a shift from a reactive to a predictive cash flow model. Automation provides the data and tools to identify problems before they escalate.

The system can analyze payment histories to identify clients who consistently pay late, flagging their invoices for earlier, proactive attention. This is how you systematically reduce DSO. Cash flow forecasting becomes far more reliable, providing a clearer view of expected payments—a crucial advantage in an uncertain economy.

Measuring the Real-World Impact

A successful implementation delivers measurable results. One of our clients, a $15M consulting firm, had a DSO of 68 days, with their finance team spending nearly 50% of their time on manual collections.

After implementing a tailored AI AR automation solution, the results within six months were:

- DSO Reduction: DSO dropped from 68 to 52 days, a 23% improvement that unlocked significant working capital.

- Team Efficiency: Time spent on manual collections fell to 15%, allowing the controller to focus on strategic financial planning.

- Improved Client Experience: Consistent, professional reminders and an easy-to-use payment portal led to fewer disputes and faster payments.

Technology is one piece of the puzzle. Understanding collections frameworks is also vital. You can explore effective debt collection strategies to enhance your processes. This combination of technology and process is how you improve cash flow permanently.

How to Measure Success and Sustain Cash Flow Health

Optimizing cash flow is a continuous discipline, not a one-time project. Sustained control comes from a system that monitors performance, adapts to new data, and maintains financial health over the long term.

The objective is to transition your financial operations from a reactive team that chases cash to a predictive one that manages it. This requires a commitment to data-driven improvement.

Revisit Your Core KPIs to Track Progress

The metrics used for diagnosis—DSO, CEI, ADD—now serve as your performance scorecards. They should be live KPIs on your financial dashboard.

Set clear, quantitative targets. For a professional services firm, a DSO under 45 days and a CEI consistently above 90% are strong indicators of a healthy collections process.

Tracking these KPIs is about spotting negative trends early. A three-day increase in DSO this quarter is an immediate signal to investigate whether it's an isolated issue with one client or a systemic problem. Your AR software for professional services allows you to drill down past headline numbers to identify the root cause.

Cultivate a Cash-Aware Culture

Sustaining healthy cash flow requires a culture where project managers and partners understand how their decisions impact the firm's cash conversion cycle. This does not mean turning your entire staff into collections agents.

It means providing them with the necessary information. A project manager should be aware of a client's payment history before scoping a new project. A partner must understand that offering extended payment terms has a direct, measurable cost to working capital.

This mindset is reflected in broader market trends. Global money market fund balances—a key indicator of corporate cash hoarding—jumped 15% in one year, from $5.87 trillion to $6.75 trillion, signaling a major shift toward liquidity. More on these cash management trends and their implications.

From Reactive to Predictive Financial Operations

The ultimate goal is to move from historical reporting to forward-looking analysis. Your accounts receivable automation platform is the tool that enables this shift, turning payment data into predictive insights.

An AI AR automation system learns from payment behavior to flag at-risk accounts for early intervention. It can project cash inflows with high accuracy, providing the confidence needed to manage payroll, invest in growth, and operate from a position of financial control. This is what separates a well-run firm from a resilient one.

The Questions We Hear Most Often

As finance leaders begin to modernize their AR processes, several practical questions consistently arise. Here are the most common issues from CFOs and controllers at professional services firms.

When Does Manual AR Become a Real Problem?

The tipping point for manual AR usually arrives when a firm processes over 100 invoices a month or when DSO remains stubbornly above 45-50 days.

The warning signs are clear: the finance team spends more time chasing payments than on analysis, invoice disputes rise due to human error, and client follow-up becomes inconsistent. If you cannot produce a real-time, consolidated view of all receivables, you have outgrown your process.

How Do We Automate Without Sounding Like a Robot?

Effective accounts receivable automation reinforces client relationships, not replaces them. A good system allows for customized communication based on client tier, payment history, and invoice status.

For strategic accounts, automation can send gentle, professional reminders, reserving personal calls for substantive issues, not routine follow-ups. Position this to clients as an operational improvement that enhances billing accuracy and provides convenient payment options.

Automation should handle predictable, repetitive work with perfect consistency. This frees up your team to manage exceptions and strengthen the relationships that drive your business. The goal is consistency at scale, not robotic communication.

What Kind of DSO Drop Can We Actually Expect?

For a professional services firm with a DSO between 60 and 75 days, a 15-25% reduction within the first six months is an achievable target. This translates to shaving 9 to 19 days off your cash conversion cycle.

The fastest gains come from eliminating human delays in follow-ups. AR software for professional services ensures every invoice is managed on a consistent, predetermined schedule. Over time, an AI AR automation platform can deliver further improvements by proactively identifying and managing at-risk accounts.

We Already Use QuickBooks. Isn't That Enough?

QuickBooks is an excellent accounting ledger—a system of record. However, it is not an AR operations platform. It records what happened but lacks the workflows and analytics to proactively manage future cash flow.

A dedicated QuickBooks AR automation platform sits on top of your ledger, adding a critical operational layer. It provides:

- Customizable Reminder Workflows: Set different dunning cadences for different client segments.

- Dispute Resolution Tracking: A structured system to manage and resolve invoice issues.

- AI-Powered Cash Forecasting: Move from static reports to predictive insights based on actual client payment behavior.

Think of it this way: QuickBooks is the database. An automation tool like Resolut is the engine that uses that data to accelerate cash flow and reduce DSO.

--- Resolut automates AR for professional services—consistent, accurate, and human. Learn more at https://www.resolutai.com.