Is Invoice Factoring a Strategic Tool or a Costly Crutch?

Explore invoice factoring services to boost cash flow and reduce risk. Learn costs, terms, and smarter alternatives for professional services in 2026.

For a growing professional services firm, long payment cycles create a persistent cash flow gap. You've delivered the work and issued the invoice, but the cash remains locked in accounts receivable for 30, 60, or even 90 days.

Invoice factoring offers a direct solution. You sell unpaid invoices to a third-party "factor" and receive 80–90% of the value upfront, typically within 48 hours. This converts receivables into immediate working capital.

However, this speed comes at a significant cost and introduces operational risks. For finance leaders, the key is to determine if factoring is a necessary tactical tool or a crutch for an inefficient AR process.

The CFO's Dilemma: Balancing Growth and Cash Flow

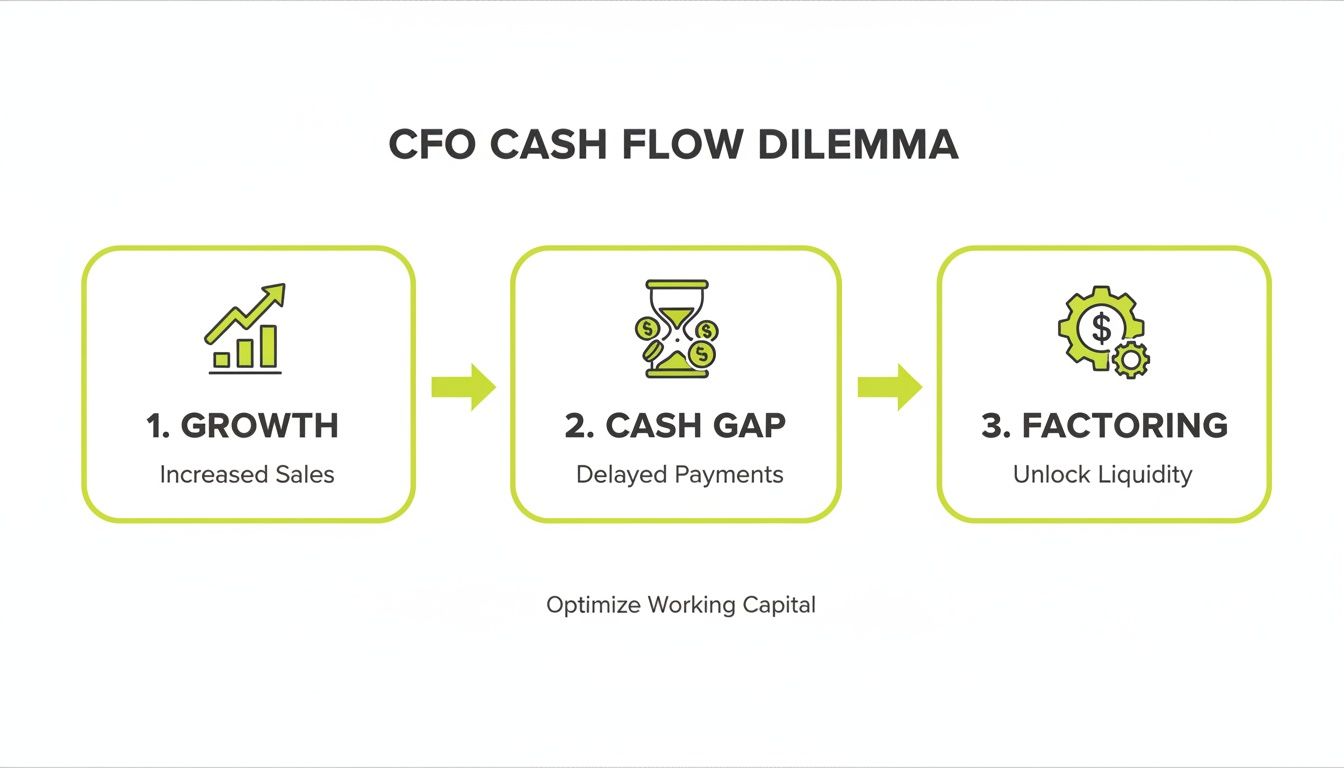

As a finance leader, a major new client is a strategic win. But their Net 60 or Net 90 payment terms immediately create a financial challenge: funding growth with delayed cash receipts.

This is a structural problem in the professional services industry. Profitability on paper does not equal cash in the bank, making predictable financial planning exceptionally difficult.

Revenue sits on the balance sheet as accounts receivable—an asset you can't use for payroll, operational expenses, or new investments. The pressure to bridge this gap is constant.

The Strain on Operational Stability

This constant juggle to maintain liquidity can strain any finance team. If you're consistently worried about your business finances, it's time to evaluate your capital strategy.

Consider the numbers: a $10M firm with an average Days Sales Outstanding (DSO) of 60 days has over $1.6M perpetually tied up in receivables. This locked capital is the direct cause of the operational strain that invoice factoring aims to resolve.

The primary goal is to make cash flow predictable. You need to convert receivables to cash faster, but without damaging client relationships or taking on excessive risk. Our complete guide shows you how to improve cash flow with sustainable strategies.

The Rise of Alternative Financing

The demand for liquidity has driven significant growth in the factoring market. Valued at USD 5.68 billion in 2024, it's projected to reach USD 13.82 billion by 2035.

This growth is fueled by firms grappling with the cash crunch caused by extended payment cycles. Factoring is a straightforward lever for unlocking cash tied up in receivables.

However, it treats the symptom—delayed cash—not the cause. A more robust, long-term strategy involves optimizing internal collections, often with tools like accounts receivable automation.

How Invoice Factoring Works in Practice

Factoring is a transaction that converts static invoices into usable cash. It is a mechanism to accelerate your cash conversion cycle for work already completed.

Here's the operational sequence.

The Transaction Sequence

The process is standardized across most factoring providers.

- Submit & Verify: You submit a copy of an approved invoice to the factor. They contact your client to verify the invoice's legitimacy and satisfactory completion of work.

- Get the Advance: Upon verification, the factor advances 80–90% of the invoice value. This capital is typically wired to your account within 24 to 48 hours.

- The Factor Takes Over Collections: The factoring company now manages collection for that specific invoice. They follow up with your client to secure payment on its due date.

- Settle Up: Once your client pays the factor, the factor deducts its fee from the remaining balance (the "reserve"). The rest, known as the "rebate," is sent to you.

This flow is designed to solve the cash gap created by the lag between revenue recognition and cash collection.

As the diagram shows, factoring acts as a bridge, providing liquidity to maintain operations while you wait for customer payments to align with your growth trajectory.

Recourse vs. Non-Recourse Factoring

A critical detail is who bears the risk of non-payment. This is determined by the recourse structure of your agreement.

Recourse Factoring: This is the most common model. If your client fails to pay for any reason, you are obligated to buy back the bad debt from the factor. The fees are lower because you retain the credit risk.

Non-Recourse Factoring: The factor assumes the credit risk if your client becomes insolvent. This protection results in higher fees and does not cover commercial disputes (e.g., your client is unhappy with the work).

For a professional services firm, this choice directly impacts your contingent liabilities and the total cost of financing. Since most agreements are recourse-based, your own client credit diligence remains paramount.

While a tool like QuickBooks AR automation helps track receivables, it doesn't mitigate the credit risk of a client default. Understanding liability is fundamental to using invoice factoring services effectively.

Calculating the True Cost of Unlocking Your Cash

The advertised discount rate is only the starting point. To accurately assess the impact on your P&L, you must calculate the true, all-in cost of this financing.

The effective cost is a function of two variables: the factoring fee (discount rate) and the advance rate. Modeling how these interact is the only way to compare it to other sources of capital.

Deconstructing Factoring Fees

The factoring fee is often structured to increase over time. A common model is a base rate for the first 30 days with incremental fees for each subsequent period.

For example, a factor might charge 1.5% for the first 30 days, plus 0.5% for every 10 days thereafter. For clients on Net 60 or Net 90 terms, this escalating structure can significantly increase the final cost.

The advance rate is the percentage of the invoice you get upfront. A lower advance rate means more of your capital is held in the factor's reserve, effectively increasing your cost of capital.

A Practical Cost Calculation

Let's model this with a $100,000 invoice on Net 60 terms.

The factor's terms are:

- Invoice Value: $100,000

- Advance Rate: 85%

- Factoring Fee: 2.0% for 60 days

This table breaks down the cash flow.

Sample Factoring Cost Calculation for a $100,000 Invoice

Metric | Calculation | Amount |

|---|---|---|

Upfront Cash Advance | $100,000 x 85% | $85,000 |

Amount Held in Reserve | $100,000 x (1 - 85%) | $15,000 |

Total Factoring Fee | $100,000 x 2.0% | $2,000 |

Final Rebate (Reserve minus Fee) | $15,000 - $2,000 | $13,000 |

Total Cash Received by You | $85,000 (Advance) + $13,000 (Rebate) | $98,000 |

Total Cost to Factor | $100,000 - $98,000 | $2,000 |

You paid $2,000 to access $85,000 of your own capital 60 days early.

To compare financing options, calculate the Annual Percentage Rate (APR). Paying $2,000 for a 60-day use of $85,000 translates to an effective APR of approximately 14.3%. This provides a true "apples-to-apples" figure to weigh against a bank line of credit.

The convenience of factoring often comes at a price significantly higher than traditional business credit. That speed has a direct, measurable impact on profit margins.

The Hidden Costs in Your AR Process

A consistent need for factoring often signals a more expensive underlying problem: an inefficient accounts receivable process. The search for external financing is frequently a symptom of slow collections and high Days Sales Outstanding (DSO).

Addressing this root cause is more valuable than treating the symptom. Implementing accounts receivable automation can fix the operational drag that creates the cash crunch.

By systemically using AR software for professional services to reduce DSO, you make cash flow more predictable. This internal optimization avoids the high cost of factoring and returns control over client relationships and financial health.

An AI AR automation system provides the visibility and efficiency needed to manage receivables without selling them to a third party.

Weighing the Pros and Cons of Invoice Factoring

Deciding to factor invoices is a strategic move, not just a financial transaction. It can be a powerful lever in the right situation, but it can also become a costly dependency.

Factoring is most prevalent in industries with inherently long payment cycles. The transportation and trucking industry, for instance, makes up 20% of all factoring demand due to payment terms stretching to 90 days.

We also saw factoring in construction jump by 12% in 2023 alone, a direct result of project-based billing and rising material costs, as highlighted in recent industry statistics about invoice factoring.

While less common in professional services, the core problem is identical. For a fast-growing firm, factoring offers a predictable cash infusion to fund growth without waiting on Net 60 or Net 90 payments.

The Clear Advantages of Factoring

The primary benefit is immediate liquidity. An outstanding receivable is converted into cash in your bank account, often within 24-48 hours. This provides a direct improvement to cash flow, smoothing out operational bumps.

Another benefit is outsourcing collections. The factoring company takes over the administrative task of chasing the invoices it has purchased, freeing up your finance team for higher-value work.

Significant Drawbacks to Consider

The most obvious drawback is cost. As the calculation shows, the effective APR on factored invoices is often substantially higher than traditional credit, eating directly into profit margins.

There is also a critical, non-financial risk: potential damage to client relationships. When you outsource collections, you lose control over that communication. An aggressive or impersonal collector can sour a relationship built over years.

Reliance on factoring can also mask deeper operational issues. A constant need to sell receivables may indicate a broken accounts receivable process. Factoring becomes a band-aid for systemic inefficiency, not a strategic solution.

Factoring: A Tactical Tool vs. a Strategic Crutch

The utility of invoice factoring services depends on context.

- As a Tactical Tool: Factoring is a valid solution for a defined, short-term need, such as funding a large one-off project or bridging a seasonal cash low. Used sparingly, it allows you to seize a growth opportunity.

- As a Strategic Crutch: If factoring becomes a routine part of your monthly cash flow management, it's a warning sign. It indicates your cash conversion cycle is too slow, and you are paying a steep price for internal inefficiencies.

The goal is to build a resilient operation that does not depend on high-cost external funding. A superior long-term strategy is to optimize collections with tools like AR software for professional services.

By embracing accounts receivable automation and AI AR automation, you can systematically reduce DSO. This approach protects client relationships and, most importantly, safeguards margins.

How to Vet an Invoice Factoring Provider

If you determine factoring is the right tactical move, choosing the right partner is critical. This company will interact with your clients and manage a vital component of your cash flow.

Look beyond the advertised rates. The real value is in the provider's transparency, contractual terms, and collections professionalism.

Assess Fee Structures and Contractual Obligations

A reputable factor will provide a clear, unambiguous breakdown of all costs. Vague pricing or an intentionally confusing fee structure is a major red flag.

Pay close attention to details that increase your total cost:

- Hidden Fees: Watch for "application fees," "credit check fees," or other ancillary service charges not disclosed upfront.

- Restrictive Minimums: Some contracts require a minimum monthly invoice volume, with penalties for falling short.

- Termination Penalties: Understand the exact process and costs for ending the agreement. Steep termination fees can trap you in an unfavorable partnership.

Scrutinize the legal agreement before signing. Familiarity with standard business contract templates provides a baseline for what is normal. Our guide on what to look for in a factoring contract agreement offers a deeper analysis.

Evaluate Their Collections Professionalism

For a professional services firm, client relationships are a primary asset. Since the factor's collectors will be calling your clients, their professionalism is non-negotiable.

Before committing, speak directly with the collections managers who will handle your account. Ask about their communication style, dispute resolution process, and approach to sensitive conversations. If they sound like aggressive collectors, walk away.

A factor's experience in the professional services sector is crucial. They must understand the nuance and long-term value of your client relationships, which differs from a purely transactional collections mindset.

Understand the Evolving Market Landscape

The factoring industry is consolidating. While the global market for invoice factoring services is growing, the number of US-based factoring firms has declined from over 600 in 2019 to just 261 in 2024.

This trend, representing a 16.1% annual decline, favors larger, integrated financial institutions. Your due diligence is more important than ever. Verify that a provider has specific, relevant experience with firms like yours.

A rushed decision can lead to damaged client relationships and hidden costs that negate the cash flow benefits you sought.

A Smarter Alternative to High-Cost Factoring

Invoice factoring is a reactive solution. It solves an immediate cash flow problem but fails to address its root cause. Constantly turning to expensive financing is a tactical retreat, not a strategic advance.

A more sustainable approach is to build a robust accounts receivable process internally. This creates a system you own and control, delivering predictable cash flow without the high cost of external financing. It is about owning your cash conversion cycle, not renting it.

From Reactive Financing to Proactive Control

A recurring need for invoice factoring services is a clear indicator of AR process inefficiencies. Manual follow-ups, inconsistent communication, and poor visibility stretch collection times. This operational drag is where your capital is truly lost.

Instead of selling invoices at a discount, the superior long-term strategy is to systematically reduce DSO (Days Sales Outstanding) by optimizing your internal processes.

The Power of AR Automation

Modern accounts receivable automation platforms are designed to solve the underlying causes of slow payments. They replace manual, inconsistent chasing with a data-driven collections strategy that accelerates payment without damaging client relationships.

For firms in the $3M–$50M range, AR automation has a measurable impact. A firm with $10M in annual revenue and a 60-day DSO can unlock an additional $137,000 in cash flow for every 5-day reduction in its collection cycle. This is capital you earn, not borrow.

This approach has distinct advantages over factoring:

- Cost Efficiency: The ROI from automation software, which helps firms reduce DSO by 10-25%, far exceeds the recurring cost of factoring.

- Client Relationship Control: You retain full control over all client communications, ensuring every interaction reflects your firm's standards.

- Data-Driven Insights: AR software for professional services provides clear visibility into payment trends, at-risk accounts, and team performance for proactive management.

Platforms that integrate with tools like QuickBooks AR automation or use advanced AI AR automation amplify these results. They can learn client payment behaviors, predict delays, and tailor follow-up strategies for optimal outcomes. You can compare this to other financing options by reading our guide on what is receivables financing.

By improving the mechanics of how you invoice, follow up, and collect, you fundamentally improve cash flow at its source. This builds a resilient financial operation that can fund its own growth—a far more powerful position than perpetual dependence on outside capital.

Frequently Asked Questions About Invoice Factoring

As a finance leader, you must weigh the immediate cash benefit of factoring against its real-world operational impact. Here are the most common questions from CFOs and controllers.

How Does Invoice Factoring Affect My Client Relationships?

This is the most critical question. When you factor an invoice, you typically outsource collections to the factoring company, inserting a third party into a trusted client relationship.

Your client's payment experience will now be shaped by the factor's collections team. An abrasive or inefficient process can damage a relationship you spent years building. Vetting a provider's collection style is as important as analyzing their fees.

Some factors offer "non-notification" or "confidential" factoring where your client is unaware of their involvement, but this service is typically more expensive and has stricter qualification criteria.

Is Invoice Factoring a Sustainable Long-Term Solution?

No. Factoring is best viewed as a tactical, short-term tool, not a permanent finance strategy. It is effective for bridging a specific cash gap, such as funding a large project or managing a seasonal trough.

Relying on it consistently, however, erodes margins due to its high effective cost. A chronic need for factoring signals an inefficient accounts receivable process. The sustainable solution is to fix your internal AR engine to reduce DSO on your own terms.

What Is the Difference Between Factoring and a Line of Credit?

The distinction is whether you are selling an asset or taking on debt.

- Invoice Factoring: This is the sale of an asset (your accounts receivable) to a third party for immediate cash. It is not debt and does not appear as a liability on your balance sheet.

- Business Line of Credit: This is a loan. A bank provides a revolving credit limit. You pay interest on the amount drawn, and it is recorded as debt on your balance sheet.

Both provide cash, but they have different financial implications. A line of credit is almost always cheaper but has a slower, more rigorous underwriting process. Factoring is faster but commands a premium for that speed and convenience.

--- Resolut automates AR for professional services—consistent, accurate, and human.