A CFO's Guide to Net 30 Payment Terms

A strategic guide for CFOs on using net 30 payment terms to optimize cash flow, reduce DSO, and strengthen financial control with AR automation.

Net 30 payment terms stipulate that a client has 30 calendar days from the invoice date to remit payment in full.

For a professional services firm, this is not just a billing cycle. It is the interest-free line of credit extended to every client, forming the foundation of your working capital.

How Net 30 Terms Define Financial Operations

Net 30 is the operating cadence for your firm's cash. It sets the rhythm for collections and directly impacts your ability to forecast, invest, and maintain liquidity.

It's a strategic lever for managing credit risk.

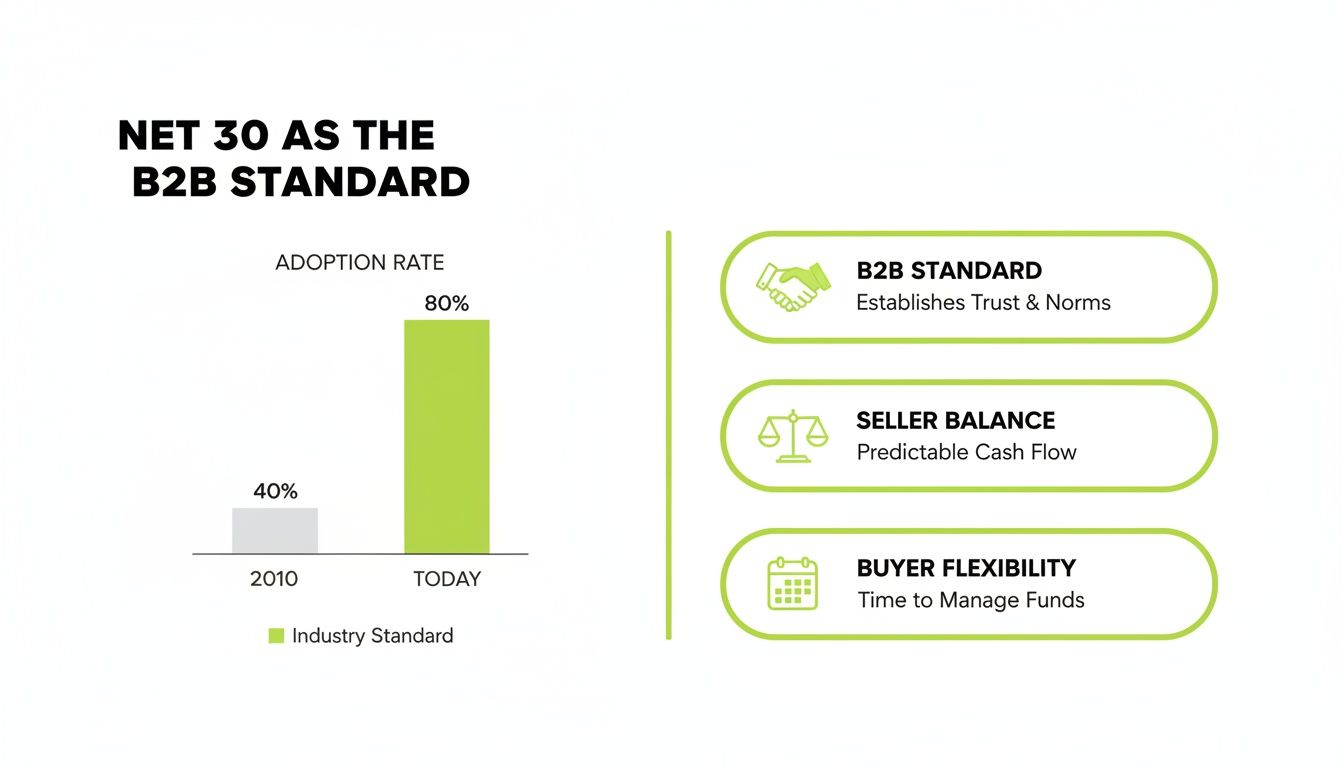

The 30-day window is the B2B standard because it balances competing needs. Clients receive a buffer to manage their payables, and you have a reasonable timeline to convert receivables to cash.

Mastering this is key to controlling Days Sales Outstanding (DSO) and achieving predictable revenue.

The Strategic Balance of B2B Credit

Net 30 is the most common payment term in B2B transactions. The model works because it is perceived as equitable.

It is less risky for the seller than longer-term financing but flexible enough to be attractive to clients.

Every invoice represents a controlled extension of trust. You deliver value upfront; Net 30 formalizes the expectation of timely payment.

This system underpins professional relationships but introduces inherent financial risk.

An unmanaged accounts receivable process is a hidden liability. When Net 30 drifts to Net 45 or Net 60 due to inconsistent collections, the drag on working capital is significant. It quietly erodes your capacity to meet payroll and fund growth.

From Policy to Performance

A Net 30 policy is meaningless without systematic enforcement. Without a system, it becomes a loose suggestion.

Inconsistent follow-up signals that due dates are negotiable, a message that erodes your cash position over time.

This is where financial operations must execute. The firm's performance is determined by its ability to consistently invoice, remind, and collect within the 30-day window.

This requires a structured system, not ad-hoc reminders. For a deeper analysis, review these proven strategies for improving cash flow.

Analyzing the Financial Impact of Payment Term Variations

Selecting payment terms is a critical financial decision, not an administrative task. Applying a blanket Net 30 policy to all invoices is a missed opportunity.

This approach ignores the nuances of client risk, relationship value, and your firm’s specific cash flow requirements.

A more effective approach is to manage client credit like a portfolio. You align payment terms with a client's credit profile and strategic importance.

For example, Net 15 can accelerate cash intake and mitigate risk for new clients or smaller projects. Extending Net 60 may be a calculated decision to secure a high-value, long-term partner. That decision must be modeled to quantify its impact on working capital.

The Financial Leverage of Early Payment Discounts

The early payment discount, often expressed as 2/10 Net 30, is a powerful financial tool that many firms misinterpret.

Offering a 2% discount for payment within 10 days is not a margin loss. It is a calculated fee to accelerate access to your capital by 20 days.

A 2% return for 20 days of acceleration translates to an effective annualized return of over 36%. From a cost-of-capital perspective, this is a highly efficient way to improve liquidity and predictability.

Offering this discount is a sound strategic move when your own cost of capital is high or when predictable cash flow is a top priority. Despite the clear financial logic, few companies systematically leverage these discounts—a point highlighted in J.P. Morgan research on payment term benefits.

How Different Terms Shape Your Cash Flow

The choice between Net 15, Net 30, and Net 60 directly impacts your Days Sales Outstanding (DSO)—the core metric for collection efficiency.

Shorter terms reduce DSO. Longer terms increase it, trapping more working capital in accounts receivable.

This trade-off is why Net 30 became the default for professional services firms. It offers a reasonable buffer for clients while keeping the credit window manageable for sellers.

Consider a professional services firm with $5 million in annual revenue. Shifting the average collection period from 45 days (a poorly enforced Net 30) to a disciplined 30 days frees up approximately $104,000 in working capital. That is cash available for growth, hiring, or debt reduction.

The goal is not merely to offer terms, but to manage them. An unenforced Net 30 policy is effectively a Net 45 or Net 60 policy in disguise, bearing the associated capital costs without the strategic intent.

Payment Term Comparison Cash Flow and Risk Analysis

From a CFO's perspective, every payment term is a trade-off between cash flow velocity, client relationships, and credit risk. This table breaks down the operational impact of common terms.

Payment Term | Typical Timeframe | Impact on DSO | Cash Flow Velocity | Associated Risk/Benefit |

|---|---|---|---|---|

COD/PIA | 0 days | Lowest possible | Immediate | Benefit: Zero credit risk. Ideal for new or high-risk clients. Risk: Can signal distrust and may not be competitive. |

Net 15 | 15 days | Low | Very Fast | Benefit: Accelerates cash flow significantly. Risk: May feel too aggressive for larger, established clients. |

2/10 Net 30 | 10-30 days | Variable | Fast to Moderate | Benefit: Incentivizes fast payment, improving predictability. Risk: Small margin reduction (the 2% discount). |

Net 30 | 30 days | Moderate | Standard | Benefit: B2B standard, balances buyer/seller needs. Risk: Requires diligent collections to prevent DSO creep. |

Net 30 EOM | 30-60 days | Moderate to High | Slow | Benefit: Aligns with corporate AP cycles. Risk: Can extend payment out by an extra 30 days. |

Net 60 | 60 days | High | Very Slow | Benefit: Can be a powerful negotiating tool for key accounts. Risk: Significantly strains working capital. |

A blended portfolio approach is optimal. Use shorter terms for new clients, strategic terms for key partners, and discounts to accelerate cash when needed.

End of Month (EOM) Terms

Another common variation is Net 30 EOM. This means payment is due 30 days after the end of the month in which the invoice was issued.

An invoice dated March 5th under these terms is not due until April 30th. This structure is common for clients whose AP teams process payments in monthly batches.

For the seller, EOM terms can extend the collection cycle by several weeks.

This is where technology provides control. Modern accounts receivable automation allows you to manage this complexity without manual tracking. A system can apply different terms to client segments automatically, triggering customized follow-up sequences based on the precise due date.

Whether you need QuickBooks AR automation or a solution for another ERP, the objective is the same: convert payment policies into predictable financial outcomes. Effective AR software for professional services provides the control to reduce DSO and improve cash flow without manual overhead.

Weaving Your Payment Terms into Contracts and Invoices

Ambiguity is the primary cause of delayed payments. When contracts or invoices leave room for interpretation, you invite friction into your cash flow.

Financial documents should be viewed as precise operational instruments.

Enforcing net 30 payment terms requires absolute consistency. The terms defined in the Master Service Agreement (MSA) must appear verbatim on every proposal, statement of work, and invoice.

Any discrepancy creates a loophole that a client's AP department can use to justify a delay.

Crafting Contract Language That Holds Up

Your service agreements are the foundation of your accounts receivable process. The language must be specific and actionable, leaving no doubt about payment expectations.

Vague phrases like "payment is due upon completion" invite disputes and collection challenges.

Instead, your contracts should contain precise clauses that define the entire payment lifecycle. This is not adversarial; it is about establishing clear, professional boundaries from the outset.

A contract with clear payment terms is the mark of a well-run business. It communicates that you manage your finances with the same discipline you apply to client work, which builds confidence.

Effective contract language should include these key components:

- Due Dates: "All invoices are due and payable within thirty (30) calendar days of the invoice date (Net 30)."

- Late Fee Triggers: "A late payment charge of 1.5% per month will be applied to any outstanding balance not paid within the Net 30 term."

- Dispute Resolution: "Client must notify Firm in writing of any disputed charges within ten (10) business days of the invoice date. Undisputed portions of the invoice shall be paid on time."

- Collections Costs: "Client agrees to pay all reasonable costs of collection, including attorney's fees, incurred by the Firm in the event of default."

This language transforms an agreement into a tool for financial control, providing the legal standing to enforce your terms.

Designing Invoices That Get Paid Faster

An invoice is a critical communication tool that can either accelerate or decelerate payment. A poorly designed invoice forces the client’s AP team to search for information, creating avoidable delays.

Your invoice design must prioritize clarity and immediate comprehension.

- Invoice Date and Number: Position these at the top for easy reference.

- Due Date: Display this prominently. Do not just state "Net 30"—specify the exact date: "Due Date: [Date]."

- Payment Instructions: Provide simple, clear instructions for payment via ACH, wire, or an online portal. Remove all friction from the payment process.

The objective is to eliminate cognitive load for the person processing the payment. Making their job easier directly accelerates your cash flow. This is a core principle of successful accounts receivable automation.

Building a Disciplined Credit and Collections System

A contract specifying net 30 payment terms is inert. The real value—predictable cash flow—is derived from the system built to enforce it.

Most firms operate reactively, chasing invoices only after they become overdue. This approach slows payments and signals that your process is negotiable.

The goal is to shift from chasing payments to guiding them. This begins with a structured approach to credit that sets clear expectations before an engagement starts.

Pre-Engagement Credit Assessments

Offering Net 30 terms without a credit assessment is a gamble. You must understand a client's payment history before committing resources.

This is not about rejecting clients. It is about matching appropriate credit terms to the client's risk profile.

A standardized process for new clients is essential:

- Credit Application: A brief, mandatory form provides basic financial data and trade references.

- Reference Checks: A call to two or three of their current vendors reveals their actual payment habits more effectively than a credit report.

- Risk Thresholds: Establish clear internal rules. A new client with no history may start on Net 15 or require a deposit. They can graduate to Net 30 after demonstrating reliability.

This removes emotion from the decision, protecting your firm before work begins.

From Invoice to Collection: A Proactive Workflow

Once an invoice is sent, a disciplined collections system operates on a predefined schedule. It uses automation to deliver a consistent, professional experience.

The objective is to make on-time payment the path of least resistance for your client.

A collections process should not be confrontational. It should be a series of professional, predictable communications that guide the client toward timely payment. Automation enables this at scale, preserving client relationships while enforcing financial discipline.

An automated workflow cadence could look like this:

- Invoice Delivery: Invoice sent instantly with a direct link to a payment portal.

- Payment Reminder (7 Days Before Due): A polite, automated notification of the upcoming due date.

- Due Date Notification: A simple confirmation on the day payment is due.

- Past Due Notice (1 Day After Due): The tone shifts to be more direct but remains professional.

- Escalation Path (7 Days Past Due): The system flags the account for a personal call from an AR specialist.

To ensure these calls are productive, equip your team with effective, compliant debt recovery call scripts.

Strategic Use of Late Fees and Escalation

Late fees are not a revenue stream; they are a tool to compel action. Your contract must define the terms clearly, such as a 1.5% monthly charge on overdue balances.

These fees should be applied automatically and consistently. Waiving them should be a deliberate, strategic decision, not a default action.

Finally, a disciplined system requires a clear escalation point. When an invoice becomes 30 days past due, it should automatically trigger a review by a controller or CFO. This ensures senior leadership focuses only on accounts that require their attention, preventing minor issues from escalating into significant write-offs. This is how accounts receivable automation ensures your net 30 payment terms are consistently met.

How AR Automation Creates Predictable Cash Flow

Your firm’s financial policies, including net 30 payment terms, are only as effective as your ability to enforce them consistently.

Manual accounts receivable processes are susceptible to human error, inconsistency, and oversight, which quietly undermine your strategy.

Accounts receivable automation bridges the gap between credit policy and cash flow. It transforms rules into a disciplined, systematic workflow that operates with perfect consistency.

The goal is to stop chasing payments reactively and start proactively guiding clients to pay on time.

From Manual Workflows to Intelligent Systems

For many firms, the invoice-to-cash cycle is a series of manual steps. An invoice is generated, emailed, and tracked with calendar reminders, followed by manual reconciliation. Each step is a potential point of failure.

An AI AR automation platform orchestrates this entire process. It enforces your payment terms without emotion or fatigue, ensuring every client receives the right communication at the right time.

Automation enforces financial discipline at scale. It transforms your finance team from manual collectors into strategic analysts, providing the time and data to focus on high-value work like cash flow forecasting and client credit analysis.

By systemizing collections, you establish a predictable rhythm. This consistency conditions clients to pay on time, converting accounts receivable from a liability into a reliable source of working capital. To further streamline this, many firms explore the benefits of recurring billing automation.

The Core Components of AR Automation

Effective automation is more than an email scheduler. It is a complete system designed to remove friction and compel action. For professional services firms, these components deliver the greatest impact:

- Intelligent Workflows: The system initiates a predefined sequence of communications based on an invoice's due date and status.

- Omnichannel Outreach: Communication can escalate from automated emails to SMS reminders or trigger a task for a personal phone call.

- Self-Service Payment Portals: A client portal with flexible payment options (ACH, credit card) removes logistical hurdles that cause delays. Providing an easy way to pay results in faster payments.

A CFO can define the exact escalation path, ensuring the firm's tone and actions align with the client relationship and the severity of the delay.

The Measurable Impact on DSO and Cash Flow

The primary outcome of implementing AR software is a direct, measurable reduction in Days Sales Outstanding (DSO). By ensuring invoices are delivered and followed up on systematically, automation closes the gap between billing and payment.

A firm with $10 million in annual revenue and a DSO of 45 days has $1.23 million in working capital tied up in receivables. Reducing DSO by just 10 days—a typical result of automation—unlocks over $270,000 in cash.

This is a permanent improvement in the firm's working capital position. It turns unpredictable payment habits into a stable, forecastable cash flow engine. You can explore these accounts receivable automation benefits in more detail.

For firms using platforms like QuickBooks, QuickBooks AR automation integrates directly, pulling invoice data to drive the entire collections process without manual data entry. This guarantees accuracy and frees your finance team to manage capital, not chase it.

The KPIs That Truly Measure AR Performance

Implementing net 30 payment terms and automation is the start, not the end.

The objective is a measurable, predictable improvement in the firm's financial health. You cannot manage what you do not measure.

These KPIs elevate AR from a back-office function to a strategic one. They provide the data to identify friction, prove ROI, and focus the finance team on optimizing working capital.

Days Sales Outstanding (DSO)

DSO is the fundamental AR metric. It measures the average number of days required to collect payment after work is completed. A low DSO signifies an efficient cash conversion cycle.

For professional services firms, a rising DSO is a leading indicator that collections processes are not keeping pace with stated net 30 payment terms.

DSO is a direct reflection of your firm's operational discipline. Every day removed from DSO represents tangible working capital returned to your balance sheet.

It is calculated with a standard formula:

(Total Accounts Receivable / Total Credit Sales) x Number of Days in Period

Tracking DSO over time provides direct evidence of the impact of process improvements, such as implementing accounts receivable automation.

Collection Effectiveness Index (CEI)

While DSO measures speed, CEI measures quality. It calculates the percentage of collectible receivables that were actually collected during a specific period. A CEI near 100% indicates a highly effective collections process.

The formula provides a clearer picture of performance than DSO alone:

(Beginning Receivables + Monthly Credit Sales - Ending Total Receivables) / (Beginning Receivables + Monthly Credit Sales - Ending Current Receivables) x 100

A low CEI points to systemic issues, such as client disputes or a flawed credit policy, providing a specific area for investigation.

Average Days Delinquent (ADD)

ADD offers an unfiltered view of how late overdue invoices are. It isolates past-due accounts to calculate the average number of days clients pay after the due date.

DSO - Best Possible DSO = ADD

This metric diagnoses the health of your collections process. If your DSO is 45 days against Net 30 terms, your ADD is 15 days. This indicates the high DSO is caused by poor enforcement, not the terms themselves.

Key Accounts Receivable Performance Indicators

Tracking these KPIs is the foundation of a data-driven AR strategy.

KPI | Formula | What It Measures |

|---|---|---|

Days Sales Outstanding (DSO) | | The average number of days it takes to collect payment after a sale. |

Collection Effectiveness Index (CEI) | | The percentage of collectible receivables that were actually collected. |

Average Days Delinquent (ADD) | | How many days, on average, payments are past their due date. |

When you have control over these metrics, you shift from reacting to payment delays to proactively managing the systems that determine your cash flow.

Resolut automates AR for professional services—consistent, accurate, and human.

A Few Common Questions

When Should We Offer Terms Other Than Net 30?

This is a risk-reward analysis. Shorter terms like Net 15 are appropriate for new clients with no payment history, minimizing your cash exposure on initial projects.

Conversely, a strategic enterprise client may require Net 60 as a condition of engagement. Before agreeing, you must model the impact on your working capital. This is a data-driven decision, weighing the client's creditworthiness against your firm’s ability to finance the receivable.

What Do We Do About a Great Client Who Always Pays Late?

This requires a combination of financial discipline and relationship management. First, use your AR data to quantify the impact of their payment habits on your DSO.

Next, a senior member of your team—not a junior collector—should initiate a direct, professional conversation. Frame it as a partnership issue to identify the root cause. Is it a cash flow problem on their end or an inefficient AP process?

Often, suggesting automated payments or a structured payment plan can resolve the issue for both parties while preserving the relationship.

What's the First Step to Implement AR Automation?

Before evaluating software, audit your current AR process. Map every step from invoice creation to cash application, documenting every communication and delay. This exercise will identify the specific bottlenecks that accounts receivable automation must solve.

With that data, define your primary objective. Are you trying to reduce DSO, reallocate team resources, or improve the client payment experience?

This clarity allows you to evaluate AR software for professional services based on its ability to solve your firm’s specific problems and integrate with existing systems like QuickBooks.

--- Resolut automates AR for professional services—consistent, accurate, and human.