What Is Invoice Factoring and How Does It Work?

What is invoice factoring? Learn how selling unpaid invoices impacts cash flow, costs, and strategic financial planning for professional services firms.

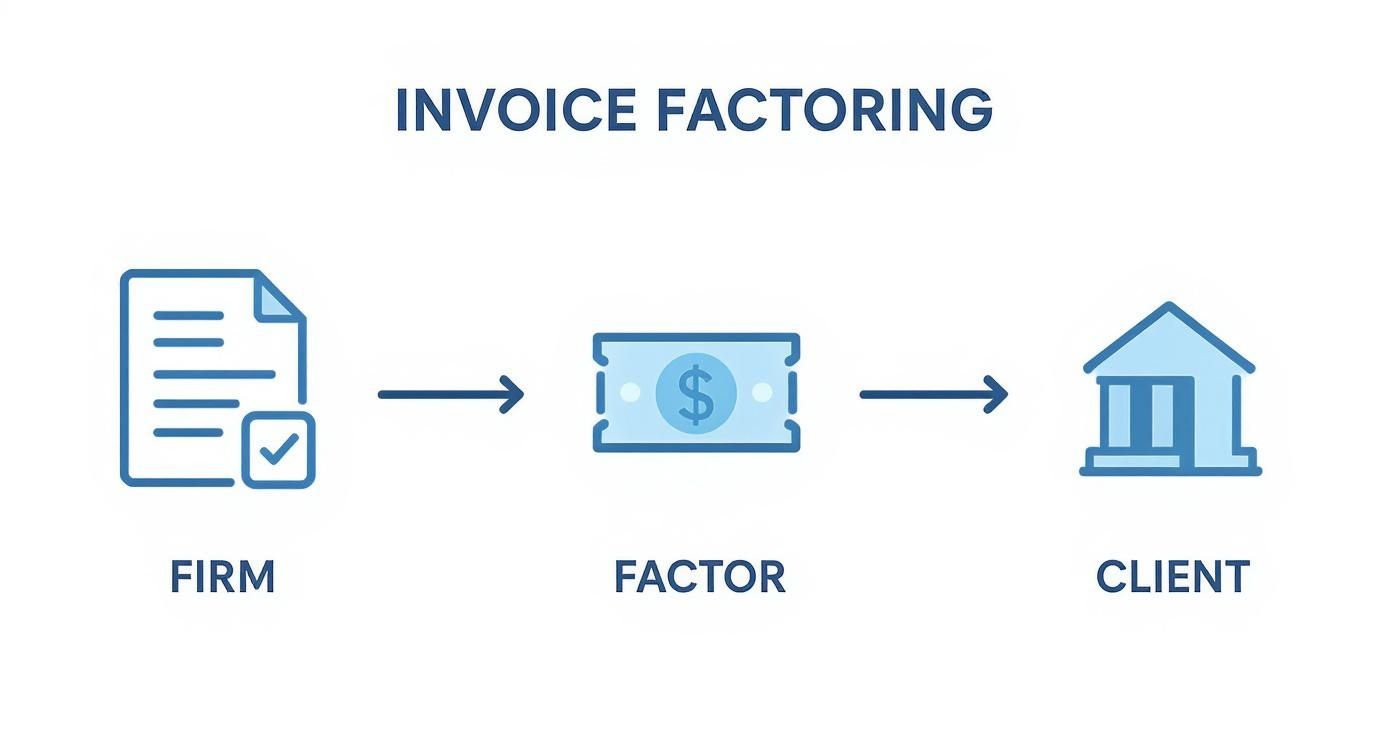

Invoice factoring is a financial transaction where a business sells its accounts receivable to a third party, known as a factor, at a discount.

This process converts outstanding invoices into immediate cash. It is not a loan; it is the sale of a balance sheet asset. This distinction is critical for financial operators managing debt covenants and liquidity.

Understanding Invoice Factoring as a Cash Flow Tool

Unpredictable cash flow is a significant operational drag for professional services firms. When client payment cycles extend to 60 or 90 days, liquidity is constrained, impacting payroll, operational expenses, and growth investments.

Invoice factoring directly addresses this by monetizing the cash tied up in receivables. Instead of waiting on client payments, the firm sells the invoice to receive an immediate advance, typically 80-95% of the invoice value. This liquidates a current asset, improving the cash position without adding a liability to the balance sheet.

>This strategy provides a predictable injection of working capital, transforming your AR from a source of uncertainty into a reliable cash source. By stabilizing cash flow, you gain the financial control needed to run operations smoothly.

Factoring is one of several small business funding options available. However, before considering external financing, firms should first optimize internal processes. An efficient collections engine is the most cost-effective first step. Many cash flow issues can be resolved if you clean up your accounts receivable.

The Modern Factoring Landscape

The global factoring market is projected to exceed $4.0 trillion. Digital platforms have accelerated this growth, enabling firms to convert approved invoices into cash within 24 to 48 hours. This speed is driven by automation and AI, which streamline underwriting and funding.

While factoring provides a rapid liquidity solution, it does not fix systemic collections inefficiencies. For sustainable financial health, the superior long-term alternative is optimizing internal AR processes.

How the Invoice Factoring Process Works Step by Step

The factoring transaction involves three parties: your firm (the seller), your client (the debtor), and the factoring company (the factor).

The process begins after work is completed and an invoice is issued. At this point, you hold an accounts receivable asset but have no corresponding cash.

The Transactional Flow

The factor purchases the outstanding invoice. Their due diligence focuses primarily on your client's creditworthiness and payment history, not your firm's credit profile.

Upon approval, the factor advances a significant portion of the invoice value, typically 80% to 95%. This cash is usually deposited within a few business days. The factor then assumes ownership of the invoice and manages the collection process directly with your client. This introduction of a third party into the client relationship is a critical operational consideration. To understand how this fits into your broader financial operations, see our guide on the order-to-cash process.

You are exchanging a fee and direct control over collections for immediate liquidity. It is a straightforward, if significant, trade-off.

Settlement and Key Distinctions

Once your client pays the invoice in full to the factor, the transaction is settled. The factor remits the remaining balance (the 5% to 20% reserve) to you, minus their fees.

Factoring agreements vary based on who assumes the risk of non-payment.

- Recourse Factoring: This is the most common arrangement. If your client fails to pay, your firm is liable for repurchasing the unpaid invoice. It is less expensive because you retain the credit risk.

- Non-Recourse Factoring: The factor assumes the risk of client default due to insolvency. This acts as a form of credit insurance but comes at a higher cost due to the increased risk for the factor.

Understanding these contractual terms is essential for any CFO or controller, as it directly impacts cash flow forecasting, risk exposure, and client relations.

Calculating the True Cost of Invoice Factoring

A precise analysis of the cost is mandatory before entering a factoring agreement. Fees are variable, contingent on invoice volume, client credit quality, and the average days to pay.

The cost structure typically includes a factoring fee (an administrative charge) and a discount rate. The discount rate is time-sensitive; the longer an invoice remains outstanding, the higher the total cost.

Breaking Down the Fee Structure

The flat factoring fee typically ranges from 1% to 5% of the invoice face value. This rate is influenced by your industry's risk profile and your clients' payment histories. According to industry data, the US invoice factoring market was valued around $3.0 billion, facing competition from other credit facilities. More detail is available on the state of the factoring market on IBISWorld.

This variability requires precise modeling to make an informed decision.

The only metric that truly matters for comparison is the effective Annual Percentage Rate (APR). Calculating this lets you put the cost of factoring right next to a business line of credit for a true, apples-to-apples evaluation.

A Practical Cost Example

Consider a $100,000 invoice from a professional services firm under a typical factoring agreement.

Invoice Factoring Cost Calculation Example

Metric | Example Value |

|---|---|

Invoice Amount | $100,000 |

Advance Rate | 90% |

Initial Cash Advance | $90,000 |

Factoring Fee (2%) | $2,000 |

Discount Rate (1.5% per 30 days) | Tiered based on payment speed |

If the client pays in 45 days, the discount fee would be $2,250 (1.5% for the first 30 days + 0.75% for the next 15).

Adding the $2,000 flat factoring fee, the total cost is $4,250.

This equates to an effective interest rate of 4.72% on the $90,000 advance over 45 days. Annualized, this single transaction could carry an APR exceeding 35%—significantly higher than most traditional financing.

Understanding the true cost of AR inefficiency is the only way to determine if such an expense is justified.

The Strategic Trade-Offs You're Really Making

The decision to use invoice factoring is a strategic choice with consequences beyond the P&L. It requires weighing the immediate need for liquidity against the associated costs and operational impacts.

The primary benefit is accelerated cash conversion. This liquidity enables agility—funding growth initiatives, making strategic hires, or capitalizing on time-sensitive opportunities without the delays of traditional bank financing.

The Upside: Outsourced Collections

A secondary benefit is outsourcing the administrative burden of collections. For lean finance teams, this can free up resources for higher-value activities like financial planning and analysis. This operational lift can improve overall team efficiency.

The Downside: Cost and Control

The primary drawback is cost. As demonstrated, the effective APR on factoring is almost always higher than a conventional business line of credit. For firms with strong credit, factoring is a more expensive source of capital.

The second, and arguably greater, cost is the loss of control over client communication. The factor’s collection practices—their tone, persistence, and frequency—become a direct reflection of your firm.

For professional services firms, where relationships are the core asset, this presents a substantial risk. An aggressive or impersonal collections process can erode goodwill built over years. The potential damage to client relationships must be carefully weighed against the need for cash.

For firms aiming to reduce DSO and improve cash flow without ceding client control, the sustainable solution is operational improvement through accounts receivable automation. Systems leveraging AI AR automation, including those with QuickBooks AR automation capabilities, provide a path to financial stability.

Factoring vs. Financing vs. AR Automation

A financial operator's objective is to build a predictable, healthy cash flow engine, not merely to apply temporary fixes. When facing slow receivables, three distinct options emerge: invoice factoring, invoice financing, and accounts receivable automation.

Each addresses a cash flow problem but with different impacts on the balance sheet, client relationships, and operational control.

Invoice factoring is the sale of receivables. It provides immediate cash and outsources collections but at a high cost and with a loss of client control.

Differentiating Financing and Automation

Invoice financing is a loan collateralized by your accounts receivable. You receive cash but retain ownership of the invoices and manage collections yourself. This maintains client relationship control but adds debt to the balance sheet.

The third path is accounts receivable automation. This is not a financing product; it is an operational solution that addresses the root cause of slow payments. Instead of selling or borrowing against invoices, AR software for professional services accelerates collections by improving the efficiency of your internal processes.

AR automation is about process ownership, not asset sale. It focuses on systematically reducing DSO by improving the efficiency and effectiveness of your collections engine, turning your AR team into a high-performance function.

Platforms using AI AR automation streamline communications, forecast payment timing, and provide clear visibility into the entire receivables portfolio. For firms using QuickBooks, dedicated QuickBooks AR automation tools offer seamless integration.

A Strategic Comparison for Finance Leaders

The choice depends on your firm's immediate needs versus its long-term objectives. Factoring is a short-term solution that sacrifices margin and control for speed. Financing provides capital but adds debt. AR automation builds a foundation for sustainable cash flow through operational excellence.

Comparison of Cash Flow Solutions

Criteria | Invoice Factoring | Invoice Financing | AR Automation (e.g., Resolut) |

|---|---|---|---|

Primary Goal | Immediate cash by selling invoices | Loan secured by invoices | Accelerate collections, improve process |

Cost | High (fees + discount rate) | Moderate (interest + fees) | Low (SaaS subscription) |

Client Relationship Control | Lost (Factor handles collections) | Retained by firm | Retained and enhanced by firm |

Balance Sheet Impact | Removes receivable (off-balance sheet) | Adds debt (loan liability) | No direct impact; improves asset performance |

Best For | Urgent cash needs, weak credit | Established firms with strong receivables | Firms seeking operational efficiency and control |

For firms focused on long-term financial health, the objective is to improve cash flow and reduce DSO permanently. A disciplined financial operator prioritizes optimizing internal systems before seeking external financing.

So, Is Factoring the Right Move?

Invoice factoring is a significant financial lever, but its application requires careful consideration. It should be a strategic choice, not a reaction to a crisis.

First, determine if your cash flow problem is a temporary gap or a systemic issue. Factoring can bridge a short-term liquidity crisis, but it is an expensive and unsustainable solution for chronic slow payments.

The Real Cost—Financially and Relationally

Have you calculated the all-in, effective APR? The true cost of capital can be substantially higher than traditional financing or the cost of optimizing internal collections.

Consider the impact on client relationships. How will your clients perceive communication from a third-party collections entity? In professional services, the client relationship is a primary asset. Ceding control over this touchpoint is a major brand risk.

The decision to factor should only ever come after you’ve exhausted options to optimize your own house. Fixing the root cause of payment delays is almost always the more strategic and cost-effective path to long-term financial health.

For objective analysis of complex financial strategies, engaging fractional finance director services can provide valuable expert perspective.

Globally, factoring is a substantial market, indicating its utility for companies with limited access to traditional credit. European factoring volume grew from EUR 1.84 trillion in 2020 to over EUR 2.55 trillion in 2023. You can review factoring statistics and their global impact for further context.

However, if sustainable financial control is the goal, optimizing your own collections engine is the most direct route. Solutions like accounts receivable automation provide the tools to reduce DSO and stabilize cash flow without sacrificing margin or client relationships.

Common Questions About Invoice Factoring

Here are answers to practical questions that financial leaders have when evaluating invoice factoring, focusing on its operational and relational impacts.

Will My Clients Know I'm Using a Factoring Service?

Yes, in most cases. The standard process is notification factoring, where the factor informs your client they have purchased the invoice and instructs them to remit payment to a new account.

This disclosure is a significant consideration. Non-notification services exist but are less common and more expensive.

What’s the Difference Between Recourse and Non-Recourse Factoring?

The key distinction is liability for non-payment.

With recourse factoring, the most common and less expensive option, your firm retains the risk. If your client defaults, you must repurchase the invoice from the factor.

With non-recourse factoring, the factor assumes the credit risk of client insolvency. This protects you from bad debt but comes with higher fees.

Your choice between recourse and non-recourse directly shapes your firm's risk exposure and the total cost of capital. A lower fee in a recourse arrangement means you retain the liability for client default.

How Is Factoring Different From a Business Line of Credit?

These are fundamentally different financial instruments.

Invoice factoring is the sale of an asset (your AR). It is not a loan, so it does not add debt to your balance sheet. Approval is based primarily on your client’s creditworthiness.

A business line of credit is debt. You borrow against a pre-approved limit, and eligibility is determined by your company's credit profile. You repay the principal plus interest and maintain full control over your client relationships.

--- Resolut automates AR for professional services—consistent, accurate, and human. Learn more.