Mastering the Allowance for Uncollectible Accounts

A CFO's guide to the allowance for uncollectible accounts. Learn proven methods, journal entries, and how AR automation reduces bad debt for service firms.

Not every dollar you bill will reach your bank account. That’s a fundamental reality of business.

The allowance for uncollectible accounts isn’t an admission of failure; it's a mark of financial control. It is a contra-asset account on your balance sheet that anticipates the slice of your accounts receivable (AR) you won't realistically collect. It’s a financial buffer ensuring your books reflect reality, not just optimism.

Why the Allowance for Uncollectible Accounts Is a Strategic Tool

For a CFO or Controller, this allowance isn't about tracking losses. It's about exercising financial discipline.

Acknowledging that some revenue is uncollectible is the first step toward building a balance sheet that can withstand operational friction. This reserve ensures you report the true net realizable value of your receivables.

Without it, you’re overstating your assets. This misleads stakeholders and skews key metrics like DSO and cash flow forecasts, which is particularly dangerous in professional services where project billing cycles are complex and unpredictable.

Gaining Control Over Financial Reporting

Managing this allowance with precision gives you a direct handle on the accuracy of your financial reporting. It’s a quiet declaration that you understand your clients, their payment habits, and the risks baked into your credit policies.

A well-managed allowance transforms reactive, painful write-offs into a predictable operational expense. It’s the difference between being blindsided by bad debt and actively managing its impact on your bottom line.

When you forecast accurately, you build confidence with investors and lenders. It signals that your firm has a firm grasp on the levers that drive profitability.

The Real Cost of Uncollected Revenue

Globally, businesses write off roughly 1 in 10 B2B invoices. For a $10M firm, that’s a potential $1M drag on cash flow and enterprise value.

Proactively accounting for these potential losses isn't just good practice—it's essential for operational stability. It allows for:

- Reliable cash flow forecasting. When you already expect a certain amount to be uncollectible, your cash projections become far more dependable for managing payroll and other operational expenses.

- Smarter credit policy decisions. Spotting trends in your allowance can illuminate weaknesses in client vetting or credit terms, giving you the data to make corrective adjustments.

- Improved strategic planning. A realistic picture of collectible revenue leads to better decisions on hiring, investment, and expansion. For a deeper dive, this A Guide to Allowance for Credit Losses for Bank Executives offers valuable insights.

Ultimately, a precise allowance for uncollectible accounts is a cornerstone of a tough-minded financial strategy. It directly supports the one goal every finance leader shares: to improve cash flow.

Choosing the Right Estimation Method for Your Firm

Selecting the right method to estimate your allowance for uncollectible accounts is a strategic decision. Your choice directly impacts the accuracy of your income statement and balance sheet.

The two primary methods are percent-of-sales and AR aging. For a professional services firm, where client payment behavior varies significantly, precision is non-negotiable.

The Percent-of-Sales Method

The percent-of-sales method is a broad-strokes approach. It is income-statement-focused, calculating bad debt expense by applying a flat percentage to total credit sales for a given period, based on historical data.

For example, if your firm historically fails to collect 1% of revenue and you billed $2M on credit this quarter, you would book a $20,000 bad debt expense.

This method aligns the expense with the revenue that generated it, satisfying the matching principle. But its simplicity is its biggest flaw. It completely ignores the current status of your outstanding receivables, making it a poor fit for firms with varied project timelines and high-value invoices.

The AR Aging Method

The AR aging method is a balance-sheet-focused approach that provides a much sharper picture. It works by bucketing outstanding receivables by age—current, 31-60 days past due, 61-90 days, and so on.

You then apply a different, increasing uncollectibility percentage to each bucket. The logic is simple: the longer an invoice goes unpaid, the less likely you are to collect it.

This isn't just an estimate; it's a calculated risk assessment. This is why the AR aging method is the standard for professional services. It provides a specific, defensible number for your allowance.

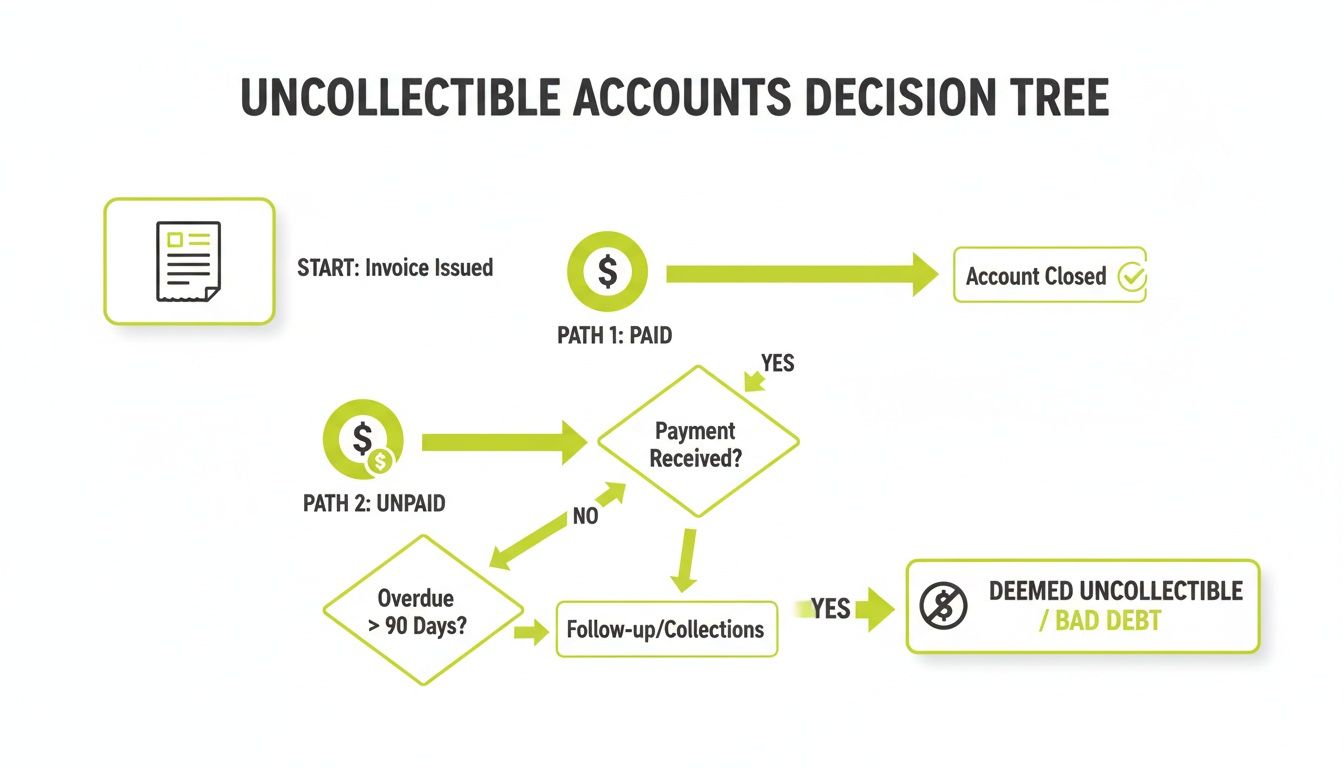

This flowchart shows how an invoice moves through its lifecycle, from issuance to the point where it's either paid or written off as a loss.

The aging process is the critical juncture. Once an invoice ages past 60 days, the risk of it becoming a write-off climbs exponentially.

Comparing Allowance Estimation Methods

Choosing between these two isn't a technical exercise; it's about deciding how much clarity you require.

Factor | Percent-of-Sales Method | AR Aging Method |

|---|---|---|

Focus | Income Statement (Matching expenses to revenue) | Balance Sheet (Valuing current receivables) |

Simplicity | High. Easy to calculate and apply. | Moderate. Requires an aging report and analysis. |

Accuracy | Low. Ignores the actual status of receivables. | High. Based on real-time collection risk. |

Insight | Limited. Provides a single, period-based expense. | Granular. Pinpoints risk in specific aging buckets. |

Best For | High-volume, low-value transactional businesses. | Professional services & B2B with varied payment cycles. |

Ultimately, the aging method forces a level of discipline—a regular review of who owes you what—that the percent-of-sales method simply can't. These financial guidelines apply to both retail and services sectors.

A Practical Comparison

Let’s apply this to a firm with $500,000 in total accounts receivable.

Using the AR aging method, they might find that after applying different risk percentages to each bucket, they require a $20,000 allowance (4% of total AR). This calculation is specific—assigning a 95% reserve to invoices over a year old but only 2% to those under 60 days.

If that same firm used a percent-of-sales method with a 1% historical loss rate on $1,000,000 in credit sales, their allowance would be just $10,000. That number has no direct connection to the actual risk sitting in that $500,000 of outstanding AR.

The aging method provides a more accurate net realizable value of your receivables. It forces a disciplined, regular review of who owes you what and for how long—essential for proactive cash flow management.

This detail does more than satisfy auditors; it drives better operational decisions. If your 90+ day bucket is swelling, that’s a direct indicator that the collections process is broken. You’d never get that signal from a simple percent-of-sales calculation.

Putting It All on the Books: A Worked Example

Theory is one thing, but accurate journal entries are where an estimate becomes a hard number on your financial statements.

Let's walk through the mechanics using a professional services firm and the AR aging method—the standard for businesses with complex client payment cycles.

Step 1: Calculating the Required Allowance

A consulting firm, "Innovate Solutions," closes the year with $750,000 in total accounts receivable. Their controller generates an AR aging report and applies the firm’s historical loss rates to each bucket.

Aging Bucket | AR Balance | Uncollectibility Rate | Required Allowance |

|---|---|---|---|

Current (0-30 Days) | $400,000 | 1% | $4,000 |

31-60 Days | $200,000 | 5% | $10,000 |

61-90 Days | $100,000 | 20% | $20,000 |

91+ Days | $50,000 | 50% | $25,000 |

Total | $750,000 | $59,000 |

The analysis shows the firm needs a total allowance of $59,000 to accurately reflect its net realizable value. This is a data-driven figure, not a guess.

Step 2: Recording the Adjusting Journal Entry

Innovate Solutions already has a $25,000 credit balance in its Allowance for Uncollectible Accounts from the prior period. The new target is $59,000.

The firm needs to book an additional $34,000 in bad debt expense for the period ($59,000 target minus the $25,000 existing balance).

Here’s the journal entry:

- Debit: Bad Debt Expense $34,000

- Credit: Allowance for Uncollectible Accounts $34,000

This single entry hits the income statement (increasing expenses) and the balance sheet (increasing the contra-asset allowance). If these calculations become a burden, you might consider how to outsource bookkeeping for your small business.

Step 3: Writing Off a Specific Bad Debt

Months later, a specific client invoice for $10,000 is deemed uncollectible after 180 days and multiple failed collection attempts. It’s time to remove it from the books.

A write-off is purely a balance sheet event. It does not create a new expense because you already recognized the expected loss when you funded the allowance. This entry just cleans up the books by removing a known bad asset.

The journal entry to write off the invoice is:

- Debit: Allowance for Uncollectible Accounts $10,000

- Credit: Accounts Receivable $10,000

This entry shrinks both the total AR and the allowance balance, but the net realizable value of your receivables remains unchanged. Before the write-off, Net AR was $691,000 ($750,000 AR - $59,000 Allowance). After, it’s still $691,000 ($740,000 AR - $49,000 Allowance).

How It Looks in T-Accounts

T-accounts visualize the movement of these numbers.

Accounts Receivable (AR)

Debit | Credit |

|---|---|

Beg. Bal. $750,000 | Write-off $10,000 |

End. Bal. $740,000 |

Allowance for Uncollectible Accounts

Debit | Credit |

|---|---|

Write-off $10,000 | Beg. Bal. $25,000 |

Adjustment $34,000 | |

End. Bal. $49,000 |

This methodical process keeps you compliant and creates a clear audit trail. It transforms the allowance for uncollectible accounts from an abstract concept into a practical tool for sharp financial management.

How to Refine Your Allowance Over Time

Calculating your allowance for uncollectible accounts is not a one-time task. It is a living forecast that must become sharper over time. Your goal is to move from a reasonable guess to a data-backed prediction.

The process starts with your own history. The percentages applied to your AR aging buckets must reflect how your clients actually pay and how effective your collections are.

Conduct a Look-Back Analysis Annually

The most effective way to improve future accuracy is to analyze past performance. An annual look-back analysis compares the bad debt you estimated against the invoices you actually wrote off.

The goal is to find the gaps. If your actual write-offs were consistently higher than your allowance, your aging percentages are too optimistic. If they were lower, you may be tying up excess cash in reserves.

This review provides the evidence needed to adjust your rates. For example, you may find that invoices in the 61-90 day bucket have a true historical loss rate of 18%, not the 15% you’ve been using. That single tweak improves your entire model for the next year.

Use Key Metrics as Leading Indicators

Beyond looking backward, you must look forward. Certain KPIs act as an early warning system, enabling proactive adjustments to your allowance.

For a professional services firm, two metrics are critical:

- Days Sales Outstanding (DSO): A rising DSO means it’s taking longer to collect cash. This is a direct signal of increasing credit risk and a strong indicator that you may need to increase your allowance percentages.

- Accounts Receivable Turnover Ratio: This ratio measures collection efficiency. A declining turnover suggests collections are slowing—a trend that often precedes a spike in bad debt.

These metrics are not just for a dashboard; they are operational controls. A steady increase in your DSO should trigger a review of your allowance and your entire collections process.

Benchmarking against industry averages provides crucial context. For instance, a firm with $3M in net credit sales and $300,000 in average net AR has a turnover ratio of 10. If that number slows year-over-year and dips below industry norms, it is a red flag. A proactive CFO uses this trend to adjust the allowance for uncollectible accounts before it becomes a material problem.

The Role of Technology in Refining Estimates

Performing this level of analysis manually is inefficient. Modern accounts receivable automation platforms provide the data infrastructure to do it correctly. Instead of spreadsheets, you get a real-time view of aging trends, DSO, and client payment patterns. For firms on QuickBooks, AR automation adds an analytical depth the core software lacks.

This data-driven approach elevates the finance leader from a bookkeeper to a strategic operator. You are no longer just booking an entry; you're actively managing one of the biggest risks to your firm's financial health. For more on optimizing your collections framework, see our guide on accounts receivable best practices for professional services firms.

Proactively Reducing Bad Debt with AR Automation

Perfecting your allowance for uncollectible accounts is a smart, defensive move. The real win, however, is not just predicting bad debt—it's actively shrinking it.

This requires a shift from a reactive accounting mindset to that of a proactive financial operator.

Modern accounts receivable automation platforms make this shift possible. They are not just tools for efficiency; they are strategic systems designed to address the root causes of payment delays and defaults. The goal is to intervene early, long before an invoice becomes a material risk.

Driving Measurable Outcomes with Automation

The line between effective technology and a healthy balance sheet is direct. When you automate client communication and risk analysis, you can systematically reduce invoice aging, lower your Days Sales Outstanding (DSO), and cut the percentage of revenue written off. A 10% reduction in DSO for a $20M firm can unlock nearly $550,000 in cash flow annually.

Key features drive these outcomes:

- Automated, Personalized Reminders: Consistent, well-timed follow-ups are the antidote to delayed payments. AI AR automation ensures no client falls through the cracks, sending the right message at the right time.

- Intelligent Risk Scoring: Platforms can analyze payment histories to flag at-risk accounts, allowing your team to focus its energy where it matters most.

- Integrated Payment Portals: The easier you make it to pay, the faster you get paid. For firms using systems like QuickBooks, AR automation adds a layer of payment convenience that the core software is missing.

An effective AR platform does more than send reminders; it executes a collections strategy. It keeps outreach consistent, data-driven, and maintains a professional tone that preserves client relationships.

From Accounting Theory to Operational Control

This is where an abstract accounting concept—the allowance—is tied to a tangible business outcome: improved cash flow. Instead of accepting a certain level of bad debt, you are actively driving that number down.

By automating the first 60 days of the collections process, a firm can shrink its 61-90 day AR bucket by 20% or more. This immediately improves your allowance calculation. Your bad debt expense drops, and the net realizable value on your balance sheet increases. The entire ecosystem of receivable management services becomes healthier.

This is what an AR software for professional services like Resolut is built to do. It moves past the symptoms of late payments to fix the cause with persistent, intelligent, and scalable communication.

Your Questions, Answered

Managing the allowance for uncollectible accounts brings up common operational questions. Here are straightforward answers for finance leaders.

How Often Should We Adjust Our Allowance?

You should review and adjust your allowance at the end of every reporting period—monthly or quarterly. This ensures your financial statements reflect the current value of your receivables.

Annually, step back and review your entire estimation model. Use the last 12 months of collection data to validate your aging percentages. If your 90-day bucket proved to be riskier than forecast, adjust the rate. This annual tune-up is what maintains forecast accuracy.

What’s the Difference Between Bad Debt Expense and a Write-Off?

The difference is simple: one is a forecast, the other is a specific action.

Bad Debt Expense is the proactive estimate. It’s an expense recorded on the income statement to account for invoices you expect will go bad, matching the potential loss to the period the revenue was earned.

An account write-off is the reactive step when a specific invoice is confirmed as uncollectible. A write-off is a balance sheet event: it debits your Allowance account and credits Accounts Receivable. The expense was already accounted for, so this action does not impact the income statement.

Think of it like this: Bad Debt Expense is the forecast predicting a 20% chance of rain. A write-off is the confirmation that a specific storm has passed and is being recorded as such. The forecast prepared you for the loss; the write-off cleans up the books.

Can We Recover a Receivable After It’s Been Written Off?

Yes. If a client pays an invoice you had previously written off, you simply reverse the write-off to maintain accurate records.

It is a two-step process:

- Reinstate the Invoice: Reverse the write-off by debiting Accounts Receivable and crediting the Allowance for Uncollectible Accounts.

- Record the Cash: Record the payment as usual by debiting Cash and crediting Accounts Receivable.

This two-step entry creates a clean audit trail. Of course, the primary goal is to minimize write-offs. Strengthening your collections process with accounts receivable automation is the most direct way to reduce DSO and improve your cash position.

--- Resolut automates AR for professional services—consistent, accurate, and human.