A Finance Leader's Guide to AR Collection Agencies

A clear guide for CFOs on when to hire an AR collection agency vs. using automation. Learn the triggers, costs, and benefits to protect your cash flow.

An AR collection agency is a tool for asset recovery. It’s a third-party specialist engaged to recover severely overdue payments—typically those 90 to 120 days past due where client communication has ceased.

Engaging one is a tactical decision, not a sign of process failure. For CFOs and controllers at professional services firms, the key is knowing precisely when to escalate.

The Escalation Decision: When to Engage an Agency

Managing accounts receivable is a constant balancing act. The objective is to protect cash flow without damaging client relationships built over years.

This leads to a critical decision point: when does it make sense to transfer an account to a third-party collection agency?

A Strategic Decision, Not a Sign of Failure

Escalating a delinquent account to an agency is a calculated, data-driven action for a specific risk profile. It is not an admission of internal failure.

The alternative—indefinite internal pursuit—carries tangible costs that impact firm performance and profitability. These are measurable drags on the P&L.

- Resource Misallocation: Every hour a finance team chases a 120-day-old invoice is an hour not spent on forecasting, strategic analysis, or higher-value financial operations. A firm with $10M in revenue and a 5% delinquency rate can lose over 500 hours annually to this low-yield activity.

- Operational Drag: Unsuccessful collection efforts are demoralizing. They create process friction and reduce the effectiveness of your finance team.

- DSO Inflation: Aged, delinquent accounts directly inflate Days Sales Outstanding (DSO). A 5-day increase in DSO for a $20M firm can tie up over $270,000 in working capital.

The objective is not just collection, but system integrity. A modern approach uses accounts receivable automation to minimize the number of accounts that ever reach the escalation threshold.

How an AR Collection Agency Operates

From a finance operator’s perspective, an AR collection agency is the final step in the collections process. They are specialists engaged when an account has gone silent, typically 90+ days past due, and internal efforts have been exhausted.

Once an account is transferred, the agency initiates a systematic and assertive communication process. This typically involves a series of demand letters, persistent phone calls, and skip tracing to locate unresponsive clients. A professional agency documents every interaction with precision.

The global debt collection market is valued at approximately USD 30.19 billion, reflecting the prevalence of payment delinquency. You can discover more insights about the collection agencies market on ResearchAndMarkets.com.

The Financial Models of Collection Agencies

Agency compensation is almost always performance-based, aligning their incentives with your recovery goals. Understanding the fee structure is critical before engagement.

Here are the standard models:

- Contingency Fees: This is the industry standard. The agency retains a percentage of the amount recovered, typically between 20% to 50%. The rate increases with the age and difficulty of the debt. Recovering a $10,000 invoice at a 25% rate nets your firm $7,500.

- Flat-Fee Services: Less common for full collection efforts, some agencies charge a fixed price for specific actions, such as sending a series of formal demand letters. This is more appropriate for pre-collection activities.

- Hybrid Models: A combination of a smaller upfront fee and a lower contingency percentage. This model is less common but can mitigate risk for both parties.

The contingency model means you only pay for results. It also means that for every dollar recovered from a severely aged account, you will only realize between $0.50 and $0.80. This highlights the value of effective, early-stage receivable management services.

The Legal Landscape and Compliance

A professional agency’s core value includes navigating the complex legal environment of debt collection. Partnering with a non-compliant agency creates significant reputational and legal risk.

In the United States, the Fair Debt Collection Practices Act (FDCPA) sets federal guidelines for collector conduct. It prohibits:

- Calling before 8 a.m. or after 9 p.m. local time.

- Using harassing or threatening language.

- Misrepresenting the debt amount.

- Contacting third parties for purposes other than location verification.

A reputable agency operates strictly within FDCPA guidelines and stays current on varying state-level regulations. Their legal expertise shields your firm from liability while they execute the necessary actions to improve cash flow from non-performing accounts.

Of course, this is the final step. Implementing accounts receivable automation, such as a platform offering QuickBooks AR automation, can systematically reduce the number of accounts that reach the 90-day threshold.

Data-Driven Triggers for Engaging an Agency

The decision to send an account to collections should not be based on intuition. It must be a calculated business decision based on clear, data-driven triggers.

This removes emotional bias and establishes a consistent, defensible process for escalating a receivable from an internal matter to a task for an external specialist.

Time is the primary variable working against you. The probability of collecting an overdue invoice declines sharply with age. After 90 days, the likelihood of collection is approximately 74%. At 180 days, it drops to 50%. Delay is a direct financial loss.

Key Escalation Thresholds

A clear set of rules, tied to observable data points, dictates precisely when the finance team escalates an account.

These are the primary triggers:

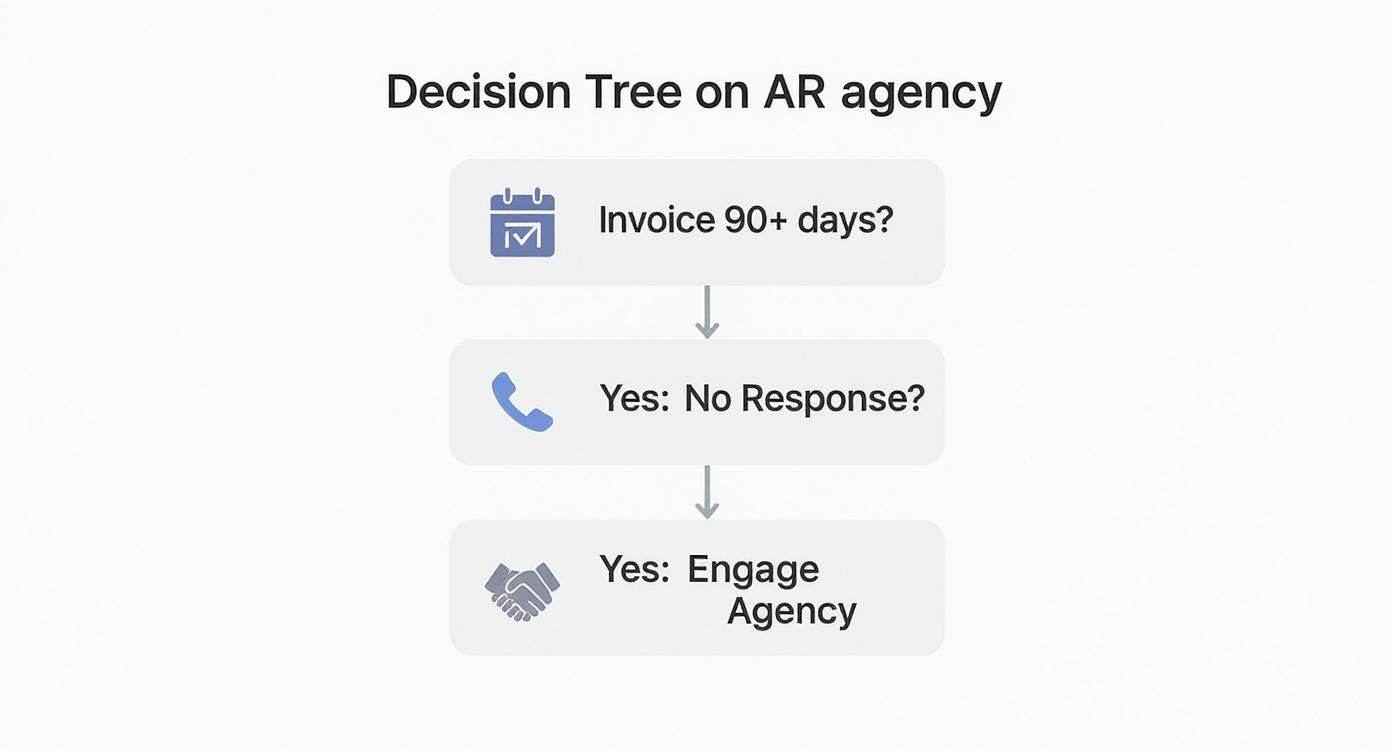

- Invoice Age: Any invoice exceeding 90 days past due without an active, documented payment plan is a candidate for escalation. At 120 days, the transfer should be automatic.

- No Communication: If a client ignores three or more contact attempts (phone and email) over a 30-day period, they have gone dark. Further internal efforts will yield diminishing returns.

- Broken Promises: A client who repeatedly promises payment and misses the date without proactive communication demonstrates a high risk of default. This pattern warrants escalation.

- Disputes as Delay Tactics: A legitimate dispute is one thing. Raising a dispute and then refusing to engage in resolution for more than 30 days is a delay tactic.

An account that is 120+ days past due with no communication is no longer a collections challenge—it's a balance sheet risk. The objective shifts from relationship management to asset recovery.

This decision process can be mapped to a simple flowchart.

When an account meets a critical age and communication stops, escalation to an agency maximizes the probability of recovery.

Decision Matrix: When to Escalate to a Collection Agency

This matrix codifies the triggers into an actionable framework for the finance team, removing ambiguity.

Indicator | Threshold | Internal Action | Escalation Trigger |

|---|---|---|---|

Invoice Age | 90+ days past due | Issue final internal demand letter. | No payment or plan after final demand. |

Communication | 3+ unanswered contacts in 30 days | Vary contact method (phone/email). | No response after final varied attempt. |

Payment Promises | 2+ broken promises without notice | Document broken promises, request immediate payment. | Third promise is broken or ignored. |

Disputes | Dispute resolution stalled for 30+ days | Send formal request to resolve dispute by a deadline. | Client fails to engage by the deadline. |

Financial Distress | News of bankruptcy, insolvency, layoffs | Cease internal collection efforts immediately. | Immediate escalation to agency or legal counsel. |

This matrix ensures every team member follows the same logic, acting decisively at the appropriate moment.

How a Proactive System Reduces Escalation

The strategic goal is to minimize the number of accounts that meet these triggers. This is the core function of accounts receivable automation.

An intelligent AR system prevents delinquencies. It manages client communications at scale with professional, consistent, and correctly timed follow-ups. This is how you systematically reduce DSO.

For firms using standard accounting packages, tools providing QuickBooks AR automation integrate directly to close the gap between invoicing and payment. By implementing AI AR automation, you reallocate your team from collections to strategic work.

Comparing Alternatives: In-House vs. Automation

Transferring an account to a collection agency is a final measure. Before reaching that point, finance leaders should evaluate two other options: managing collections entirely in-house or implementing accounts receivable automation.

Each approach presents a different mix of control, cost, and operational efficiency.

The In-House Collections Model

An in-house team provides maximum control over client communication. They understand the firm’s culture and can navigate sensitive conversations with long-term clients.

This control has a direct cost. The overhead for a dedicated collections function—salaries, benefits, training—is a significant fixed expense. For firms in the $3M–$50M revenue range, this cost can be difficult to justify against fluctuating delinquency rates.

Furthermore, an in-house team often lacks the specialized legal training and psychological tactics of agency professionals, reducing their effectiveness on deeply delinquent accounts.

The Rise of Accounts Receivable Automation

A more modern, strategic alternative is accounts receivable automation. Unlike an agency that acts reactively, an automation platform is a proactive system designed to prevent accounts from becoming severely delinquent.

This shifts the AR function from recovery to prevention.

For any business, understanding how automation can streamline business processes is a critical first step. AI AR automation platforms can send personalized reminders triggered by invoice status and client payment history, ensuring systematic follow-up.

This systematically reduces DSO by ensuring no account is overlooked.

Automation is not a replacement for a collection agency. It is a system that dramatically reduces the need for one by optimizing the entire AR lifecycle and improving cash flow from the outset.

Automation vs. Agencies: A Head-to-Head Comparison

Comparing these options clarifies their distinct roles. An agency is a tool for asset recovery. Automation is a system for cash flow management.

Feature | AR Collection Agency | AR Automation Platform |

|---|---|---|

Primary Function | Reactive Debt Recovery | Proactive Payment Optimization |

Timing | Post-escalation (90+ days past due) | Full lifecycle (pre-due date to 90 days) |

Client Relationship | Potentially adversarial, high risk of damage | Collaborative, focused on preservation |

Cost Structure | High contingency fees (20-50% of recovery) | Predictable SaaS subscription fee |

Financial Impact | Recovers a fraction of aged debt | Improves overall cash flow and reduces DSO |

The financial impact is stark. Agency recovery nets a fraction of the invoice value. In contrast, AR software for professional services works upstream to collect the full invoice value before it ages.

For firms on standard platforms, integrating QuickBooks AR automation can create a seamless system that prevents revenue leakage.

A Hybrid Strategy for Total Control

The optimal approach for most professional services firms is a hybrid model.

First, implement a robust automation platform. This system handles 99% of accounts receivable with precision, shrinking the pool of invoices that reach 90 days past due and freeing up the finance team for high-value work.

Then, for the rare cases—the client who disappears or refuses to cooperate—the AR collection agency remains the final tool.

This layered strategy provides systematic, relationship-focused collections for the majority of clients and a powerful escalation path for the exceptions.

To learn more about how this technology works, see our complete guide to accounts receivable automation software.

How to Select the Right Agency Partner

When the data indicates it's time to escalate, selecting the right agency is a critical decision. You are entrusting a partner with your firm's reputation.

A poor choice can create legal exposure and damage client relationships.

There are approximately 5,467 debt collection agencies in the U.S. The variance in quality and professionalism is significant, making a systematic vetting process essential.

Non-Negotiable Vetting Criteria

Before discussing fees, a potential partner must meet these baseline requirements.

- Industry Specialization: The agency must have a proven, verifiable track record in B2B collections for professional services firms. Collecting from a corporate client is fundamentally different from consumer debt.

- Verifiable Compliance: Request documentation of FDCPA compliance training and licenses for all states where your clients operate. Any hesitation is a disqualifier.

- Transparent Reporting Protocols: Vague promises are insufficient. Demand access to a client portal or, at minimum, regular, detailed reports on all actions taken.

Assessing Their Approach and Brand Preservation

Once the basics are confirmed, evaluate their methodology. An agency's process reveals its level of professionalism.

The objective is to find a partner who is firm and persistent, but never unprofessional. Their methods must align with your firm's standards. This is key when evaluating the best call center for debt collection.

Use direct, scenario-based questions to gauge their approach:

- "Describe your standard communication cadence for a new account at 120 days past due." This question reveals their process, intensity, and organization. A structured, multi-channel approach is expected.

- "Walk me through your escalation process for a disputed invoice from a high-value client." This tests their ability to handle nuance and sensitive situations without destroying a valuable relationship.

- "How do your collectors document client interactions, and how can we access those records?" This confirms their commitment to transparency and legal protection.

Calm, clear, systematic answers indicate control and professionalism.

The Role of Technology in Agency Selection

Finally, assess their technology stack. A modern agency uses sophisticated tools for data analysis, secure communication, and reporting.

A client portal and robust data security protocols are signs of an efficient, transparent, and secure partner.

This reinforces the larger point: the most effective way to improve cash flow is to invest in your own accounts receivable automation platform. An AI AR automation system prevents accounts from aging out, dramatically reducing the number of files ever sent to a third party.

Resolut automates AR for professional services—consistent, accurate, and human.

Building a Proactive AR Management System

For finance leaders, the focus shouldn't be on how to use an AR collection agency, but how to engineer a system that makes them largely unnecessary.

Agencies are a tool for recovering assets from non-performing accounts. True financial control, however, is achieved through a proactive AR system that prevents invoices from aging in the first place.

The goal is to architect a financial operation where severe delinquencies are systematically eliminated.

Shifting from Recovery to Prevention

The most direct path to this control is accounts receivable automation. An intelligent platform manages the AR lifecycle with a consistency that manual processes cannot achieve.

True financial control is not measured by recovery effectiveness. It is measured by how few invoices ever reach a critical age. Proactive management protects cash flow; reactive collection salvages a fraction of it.

By optimizing the early and middle stages of collections, professional services firms can protect client relationships, reduce costs, and build predictable cash flow.

The Strategic Value of AR Automation

Implementing an AI AR automation system transforms the AR function from a cost center into a strategic asset for managing working capital.

- Reduces DSO: Consistent, automated follow-ups shrink the payment cycle. A 10% reduction in DSO can free up significant cash for a mid-market firm.

- Preserves Client Relationships: Professional, timely communications avoid the adversarial tone that damages long-term partnerships.

- Optimizes Team Focus: Your finance team is reallocated from chasing payments to high-value analysis and forecasting.

This is not about replacing your team. It is about equipping them with a system that executes flawlessly, providing them the capacity for strategic work.

Resolut automates AR for professional services—consistent, accurate, and human.

A Few Final Questions

Engaging a collection agency is a significant step where financial data meets client reality. Here are common questions from finance leaders at this juncture.

What is the Real Cost of an AR Collection Agency?

Most agencies operate on a contingency model, taking a percentage of funds recovered. This fee typically ranges from 20% to 50%.

The exact rate is based on risk. Older, smaller debts are more difficult to collect and thus command a higher fee.

For a $20,000 invoice at 120 days past due, a fee of 25% to 30% ($5,000 to $6,000) is standard. While some firms offer flat-fee demand letters, the contingency model is used for active collection efforts.

What is the Impact on the Client Relationship?

Be direct: sending an account to collections is a terminal event for the relationship. It is a final measure for accounts where future business is already written off.

An agency's function is asset recovery, not goodwill preservation. This is precisely why proactive AR management—which protects relationships and cash flow—is strategically superior.

The true cost of using an agency is not just their fee; it is the permanent loss of that client's lifetime value.

When Is a Debt Considered Uncollectible?

The probability of collection drops precipitously over time.

- At 90 days past due, the recovery probability is 74%.

- At 180 days, the probability falls to 50%.

- After one year, the probability of collection is less than 10%.

Firms typically write off a debt after an agency has exhausted its efforts (usually 6-12 months) or if the client declares bankruptcy. Each day of inaction is a decision to accept a lower recovery probability.

Can We Pursue Legal Action After Using an Agency?

Yes. If an agency is unsuccessful, your right to file a lawsuit remains. Legal action is the next step in the escalation process.

Many agencies have in-house legal teams or partnerships with law firms to manage litigation. This service will involve additional costs, either a higher contingency fee or a separate legal retainer. Clarify the legal escalation process and associated costs before signing an agreement.

--- A proactive system is the best defense against bad debt. Resolut automates AR for professional services—consistent, accurate, and human. Learn more about our approach.