The CFO's Guide to the Factoring Contract Agreement

A definitive playbook for CFOs on the factoring contract agreement. Learn to analyze key clauses, negotiate better terms, and improve your firm's cash flow.

A factoring contract agreement is a tool for converting unpaid invoices into immediate working capital. For a professional services firm, this mechanism can reduce Days Sales Outstanding (DSO) and inject predictability into cash flow.

This is a significant financial decision. It requires a detailed, operational analysis before any commitment is made.

Understanding The Core Mechanics of Factoring

Factoring is a cash flow accelerator. It turns a non-liquid asset—your accounts receivable—into immediate cash. This directly addresses the lag between service delivery and payment receipt, a persistent challenge in professional services.

The agreement's financial impact is governed by three primary terms. A clear understanding of these levers is essential for any financial leader assessing the viability of factoring for their firm.

Key Financial Levers in an Agreement

- Advance Rate: The percentage of an invoice’s face value paid upfront. Professional services firms with strong client payment histories can expect advance rates between 70% to 90%. For a $100,000 invoice at an 85% advance, this translates to $85,000 in immediate liquidity.

- Discount Fee: The factor's cost for the service and risk assumption. This percentage is influenced by invoice volume, client creditworthiness, and average payment cycles.

- Reserve Amount: The portion of the invoice held by the factor until your client pays in full. It is the total invoice value less the advance. Upon client payment, the factor releases the reserve, minus their discount fee.

This process effectively outsources a component of your collections. Firms often explore accounts receivable outsourcing to model the costs and benefits of such a move. The objective remains constant: improve cash flow without degrading client relationships.

A factoring agreement re-engineers your revenue cycle. It compresses payment timelines from months to days. This shift directly impacts your firm's liquidity and its capacity to fund growth.

Modeling these components allows you to accurately forecast the cost of capital and the net cash benefit. This isn't a short-term patch; it's a systematic approach to maintaining low DSO and insulating the balance sheet from payment delays.

***

Core Components of a Factoring Agreement

For any CFO evaluating a factoring contract, these are the primary financial terms to dissect. The table below outlines these core components and gives a sense of typical ranges for a professional services firm.

Term | Description | Typical Range for Professional Services |

|---|---|---|

Advance Rate | The percentage of the invoice value paid to you upfront. | 70% - 90% |

Discount Fee | The factor's fee, often a percentage of the invoice value. | 1% - 4% of invoice face value |

Recourse Period | The time you have to buy back an unpaid invoice. | 60 - 120 days past due date |

Monthly Minimums | A minimum amount of fees you must generate each month. | Varies; sometimes waived for high volume |

Termination Fees | Penalties for ending the contract before its term expires. | Often a percentage of your credit line |

Understanding these numbers in the context of your firm's specific cash flow is critical. It is the only way to determine if the cost of accelerated cash is a worthwhile investment.

***

Recourse vs. Non-Recourse Factoring

The choice between recourse and non-recourse terms is the single most critical risk decision in a factoring agreement. It determines who assumes the liability for client non-payment.

This is not merely a contract clause; it is the core of your risk management strategy. This decision dictates cost, balance sheet resilience, and the ultimate utility of factoring as either a safety net or a potential liability.

Understanding Recourse Factoring

A recourse factoring agreement is the industry standard. You receive a cash advance, but the ultimate risk of client default remains with your firm.

If your client fails to pay, you are obligated to repurchase the invoice or repay the advance. The credit risk never fully transfers from your books.

Because the factor assumes less risk, the fees are lower—typically in the 1% to 2.5% range. For firms with a portfolio of creditworthy, long-standing clients, recourse factoring is a cost-effective method to manage cash flow. However, if a key client defaults, the liquidity benefit inverts into an immediate liability.

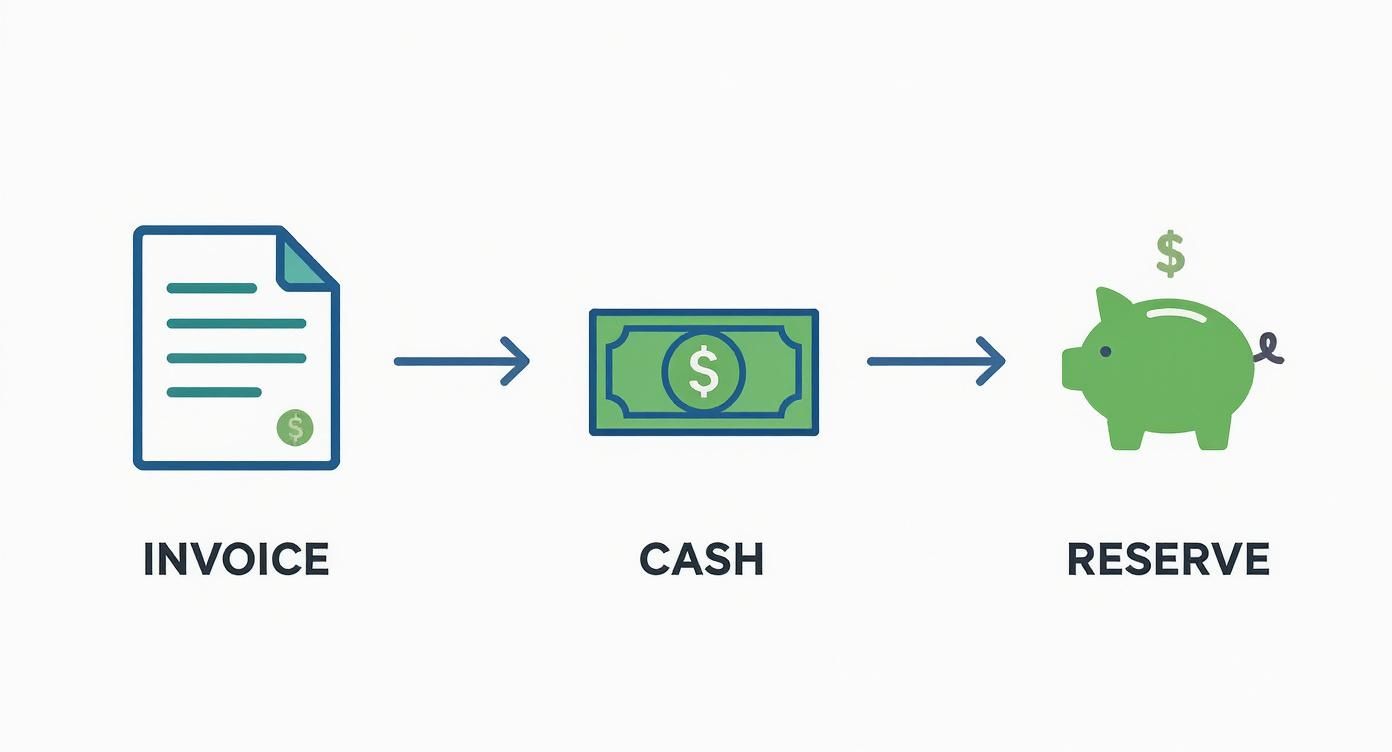

This diagram illustrates the flow from invoice to cash.

What the diagram doesn't depict is the risk allocation. Who absorbs the loss if the client never pays? This is where non-recourse fundamentally alters the equation.

The Dynamics of Non-Recourse Factoring

A non-recourse factoring agreement shifts the credit risk for approved invoices to the factoring company. If your client becomes insolvent or fails to pay for a documented financial reason, the factor absorbs the loss. You retain the advance.

This structure functions as a form of credit insurance for your receivables. You are paying a premium to mitigate the risk of a client's financial failure. For firms serving new clients or operating in volatile markets, this certainty is a significant benefit.

With non-recourse factoring, you are essentially purchasing certainty. The higher fee removes bad debt risk from your balance sheet, enabling more predictable financial forecasting and a cleaner AR ledger.

This protection comes at a higher cost. Factors charge higher fees, often 2% to 4% of the invoice value, to underwrite this risk. They also perform more stringent credit analysis on your clients before approving invoices.

Comparing Recourse and Non-Recourse Factoring

The decision between these options hinges on your firm’s risk tolerance versus cost sensitivity. This table provides a direct comparison of the key differences.

Feature | Recourse Factoring | Non-Recourse Factoring |

|---|---|---|

Risk of Non-Payment | Stays with your business. You must buy back unpaid invoices. | Transfers to the factoring company for approved credit reasons (e.g., bankruptcy). |

Cost (Discount Rate) | Lower, typically 1% to 2.5%. | Higher, often 2% to 4% or more. |

Qualification | Easier to qualify for. Focus is on your firm's stability. | Harder to qualify for. The factor heavily scrutinizes your clients' creditworthiness. |

Best For | Businesses with a strong, reliable client base and low risk of default. | Businesses operating in volatile industries or with new, unproven clients. |

The optimal choice requires a clear-eyed assessment of your client portfolio and their payment reliability.

A Practical Scenario

Consider a factored $150,000 invoice. Your client unexpectedly files for bankruptcy 60 days post-invoice.

- With a Recourse Agreement: The factor requires repayment of the advance—$127,500 (at an 85% advance rate). The initial liquidity injection becomes a sudden liability.

- With a Non-Recourse Agreement: You retain the $127,500. The factor absorbs the loss. Your firm is insulated from the client's failure.

While offloading risk is appealing, the higher fees of non-recourse agreements can erode margins, particularly if your receivables are generally healthy.

A superior long-term strategy involves strengthening internal credit and collections. Using accounts receivable automation, you can reduce the underlying need for factoring. AR software for professional services helps accelerate payments, organically improve cash flow, and maintain full control over client relationships.

Dissecting Critical Contract Clauses

A factoring contract is a legal instrument that dictates your firm's financial agility. Beyond headline rates, the true operational and financial impact resides in the fine print. For a CFO or controller, mastering these clauses is a fiduciary responsibility.

The details define the true cost, flexibility, and risk of the partnership. A single provision can have significant consequences for cash flow and balance sheet health. A line-by-line review before execution is essential.

This level of scrutiny is critical. The global factoring market was valued at $3.65 trillion in 2022 and is projected to reach $5.68 trillion by 2031, signaling widespread adoption as a cash flow management tool.

The Discount Rate Structure

The discount rate is the primary cost, but its structure dictates the actual expense. A tiered structure, where the fee increases every 10 or 15 days an invoice remains unpaid, can significantly erode margins on slow-paying accounts.

For example, a 2% flat fee on a $50,000 invoice is a $1,000 cost. A variable rate starting at 1.5% for the first 30 days and adding 0.5% every 15 days thereafter can increase that cost to $2,500 if the client pays at 75 days. This detail fundamentally changes the cost of funds calculation.

Notification Requirements and Client Interaction

The contract will specify if clients must be notified to remit payments to the factor. This "notification" clause is standard but introduces a third party into your client financial relationship.

Examine the language governing client communication. Who manages invoice disputes or payment inquiries? A factor with an impersonal or aggressive collections approach can damage client relationships cultivated over years. You must retain control or ensure the factor’s process aligns with your firm's professional standards.

Contract Length and Termination Penalties

Many factoring agreements include 12- to 24-month terms with automatic renewal clauses. Early termination often triggers significant penalties, sometimes calculated as a percentage of your credit line or projected fees.

A substantial penalty reduces your financial agility. It limits your ability to transition to more favorable financing or to bring AR management back in-house. This clause poses a direct threat to strategic financial freedom.

Red Flag Clause Example: "This agreement shall automatically renew for successive one-year terms unless either party provides written notice of non-renewal no less than 90 days prior to the expiration of the then-current term. Early termination by the Client will incur a fee equal to 3% of the Client's maximum facility limit."

Such clauses require proactive calendar management to avoid unintended renewals. When analyzing complex agreements, understanding contract management systems can be invaluable for tracking critical dates and obligations.

Uncovering Hidden Costs and Fees

Beyond the discount rate, factoring contracts often include a schedule of ancillary fees that increase the total cost. Vigilance is required to identify and quantify these charges.

Key fees to identify include:

- Application or Setup Fees: A one-time charge to establish the account.

- Service or Maintenance Fees: A recurring monthly charge, irrespective of factoring volume.

- Penalties for Slow-Paying Clients: Additional fees for invoices aged beyond a certain threshold, e.g., 90 days.

- Misdirected Payment Fees: A penalty if a client incorrectly remits payment to you instead of the factor.

These costs are cumulative. A $250 monthly service fee, plus transaction fees, can add thousands to the annual cost and alter the ROI of the arrangement. A complete analysis must extend beyond the headline rate to capture the true financial impact and ensure predictable cash flow improvement.

Evaluating Alternatives To Invoice Factoring

A factoring contract is a specific solution for immediate liquidity from receivables. It is one of several tools available. The optimal choice depends on the firm’s specific needs and its tolerance for trade-offs in cost, control, and client relationships.

Selecting a financing tool is a strategic decision. Each option presents a different balance between speed, cost, and operational control.

Traditional Business Lines of Credit

A business line of credit provides a revolving credit limit for maximum flexibility. You draw funds as needed and pay simple interest only on the amount borrowed, which is typically lower than factoring discount fees.

Approval is based on your firm’s credit history, profitability, and balance sheet strength, not your clients' creditworthiness. For financially sound firms requiring a temporary working capital bridge, this option preserves the integrity of the AR process and client communications.

Invoice Financing: A Key Distinction

Invoice financing uses accounts receivable as collateral for a loan or advance. It is often confused with factoring but is fundamentally different.

The critical distinction is control. You retain ownership of the invoices and manage the entire collections process. Client relationships remain undisturbed, as they are typically unaware of the financing arrangement. This is a significant advantage for professional services firms built on trust.

The Strategic Value of AR Automation

A third alternative is operational, not financial. Rather than treating the symptom of poor cash flow, accounts receivable automation addresses the root cause.

Modern AR platforms like those with QuickBooks AR automation can systematically reduce DSO by optimizing invoicing, reminders, and collections. This strategy enhances internal capabilities, providing complete control over cash flow. For more detail, review modern receivable management services.

The long-term ROI from accelerated payments, reduced administrative overhead, and improved client relationships is substantial. This approach shifts the firm from reactive financing to proactive financial control.

Breaking the Cycle with AR Automation

Factoring is a tactical solution for a cash flow gap. A superior strategy is to build a business that minimizes the need for such financing. This requires shifting focus from external funding to optimizing the internal engine: your accounts receivable process.

Taking Aim at DSO

Firms turn to factoring because Days Sales Outstanding (DSO) is too high, tying up critical working capital. AI AR automation directly targets this metric.

An automated system ensures timely invoice delivery and persistent, professional follow-up. For example, it can send a reminder three days before the due date, a notification on the due date, and flag the account for personal follow-up at 15 days past due. This consistency can reduce DSO by 10-25% within the first few quarters. The benefits of AR automation manifest as cash in the bank, faster.

AR automation transforms collections from a reactive, manual task into a proactive, data-driven system. It doesn't replace finance teams; it equips them to manage exceptions rather than routine follow-ups.

From Reactive Financing to Proactive Control

Automation fundamentally alters a firm's financial posture. Instead of reacting to cash shortages by selling assets, you proactively address the cause of collection delays.

The measurable outcomes are clear:

- Improved Cash Flow: Lowering DSO unlocks cash that is already on your balance sheet, reducing or eliminating the need for external financing.

- Reduced Overhead: Automating routine follow-ups can cut the administrative burden of manual collections by up to 80%, freeing up finance staff for higher-value analysis.

- Stronger Client Relationships: Automated reminders are consistent and professional, removing emotional friction from payment discussions.

The need for liquidity is undeniable. Europe's factoring market grew from EUR 1.84 trillion in 2020 to EUR 2.55 trillion in 2023. But automation provides a path to solving the problem at its source. Pairing AR software for professional services with an AI contract management system delivers comprehensive oversight of both financing agreements and internal AR performance.

AR automation is a strategic move toward financial self-sufficiency. It reduces the cost of capital and strengthens operational control.

Resolut automates AR for professional services—consistent, accurate, and human.

Frequently Asked Questions

A factoring agreement is a significant commitment. These are direct answers to common questions from financial leaders.

How does a factoring company evaluate my invoices?

Factors are primarily concerned with your clients' creditworthiness, not yours. They are purchasing an asset—the invoice—and their risk is tied to your client's ability and willingness to pay.

They will analyze your clients' payment histories and credit profiles. For professional services, they also scrutinize service contracts to ensure deliverables are clear and not subject to dispute. A portfolio of high-quality, reliable clients will secure more favorable terms.

Will my clients know I am using a factoring service?

In most cases, yes. The standard model is "notification factoring," where clients are instructed to remit payment to the factor's lockbox.

While some leaders express concern over client perception, it is a standard B2B financial practice. Framing it as an update to your firm’s accounts receivable automation and payment processing maintains a professional tone. "Confidential factoring," where clients are not notified, is rare and typically reserved for very large corporations.

What are the most common hidden costs?

The discount fee is only the baseline cost. A thorough review of the contract is necessary to identify all potential fees. Look for initial setup fees, monthly maintenance charges, wire transfer fees for each advance, and fees for credit checks on new clients.

Also, quantify penalties. What are the charges for invoices that age past 90 days? What is the cost of early contract termination? A complete understanding of the fee schedule is mandatory to accurately calculate the all-in cost of funds and its true impact on cash flow.

A factoring agreement should deliver financial clarity. If the fee structure lacks transparency, it is a significant red flag.

Can I select which invoices to factor?

This depends on the agreement. "Spot factoring" allows you to submit single invoices on an as-needed basis. This provides flexibility but comes at a higher cost.

More commonly, factors require "whole ledger" factoring, where you must submit all invoices from a specific client or your entire AR portfolio. This provides the factor with a diversified risk pool and typically results in better rates for your firm. Clarify this during negotiations to ensure the structure aligns with your operational needs.

--- Resolut automates AR for professional services—consistent, accurate, and human. Learn more about our approach.