How to Compute Average Collection period to Improve Cash Flow

A guide for CFOs on how to compute average collection period. Learn the formula, interpret the results, and use automation to improve your firm's cash flow.

The formula is straightforward: (Average Accounts Receivable / Net Credit Sales) × 365 days. This calculation yields your Average Collection Period (ACP), a direct measure of your firm's cash flow velocity.

It reveals how long revenue remains locked in unpaid invoices before converting to operational cash.

The Critical Metric Hiding in Your Financials

For a professional services firm, the Average Collection Period (ACP) is a primary indicator of financial health. It is not an abstract accounting metric; it is a vital sign.

A high ACP strains operations, limits growth, and can signal underlying issues with client stability or internal processes. It is the clearest measure of collections efficiency.

Mastering this metric begins with a precise calculation.

Why This Metric Demands Your Attention

An elevated ACP represents a direct, measurable cost to the firm. Every dollar tied up in accounts receivable is capital that cannot be invested in talent, technology, or strategic growth.

Consider a firm operating on Net 30 terms with an ACP of 75 days. The 45-day gap must be funded, typically by drawing on lines of credit or depleting retained earnings.

This metric also serves as an early warning system. A rising ACP often indicates:

- Financial instability within a key client account.

- Inefficiencies in your invoicing or follow-up procedures.

- Client confusion regarding payment terms.

From Diagnosis to Action

Diagnosing the health of your collections process begins with this calculation. Consistent tracking—annually, quarterly, or on a rolling basis—establishes a clear baseline.

This baseline allows you to measure the impact of strategic changes, from refining credit policies to implementing accounts receivable automation.

A practical example: a firm with $10M in annual revenue and a 60-day ACP has over $1.6M tied up in receivables. Reducing that period by 10 days frees up over $270,000 in cash flow.

The objective is to build a system that predictably converts invoices into cash. Your ACP is the primary tool for measuring that system's performance.

This clarity provides the control needed for strategic financial decisions. It elevates accounts receivable from a reactive administrative task to a function that directly fuels growth.

Resolut automates AR for professional services—consistent, accurate, and human.

A Practical Guide to Calculating Your ACP

Calculating the Average Collection Period is the first step toward controlling cash flow. The formula is simple, but its correct application is what provides actionable intelligence.

An imprecise calculation can create a false sense of security, masking operational issues until they directly impact liquidity.

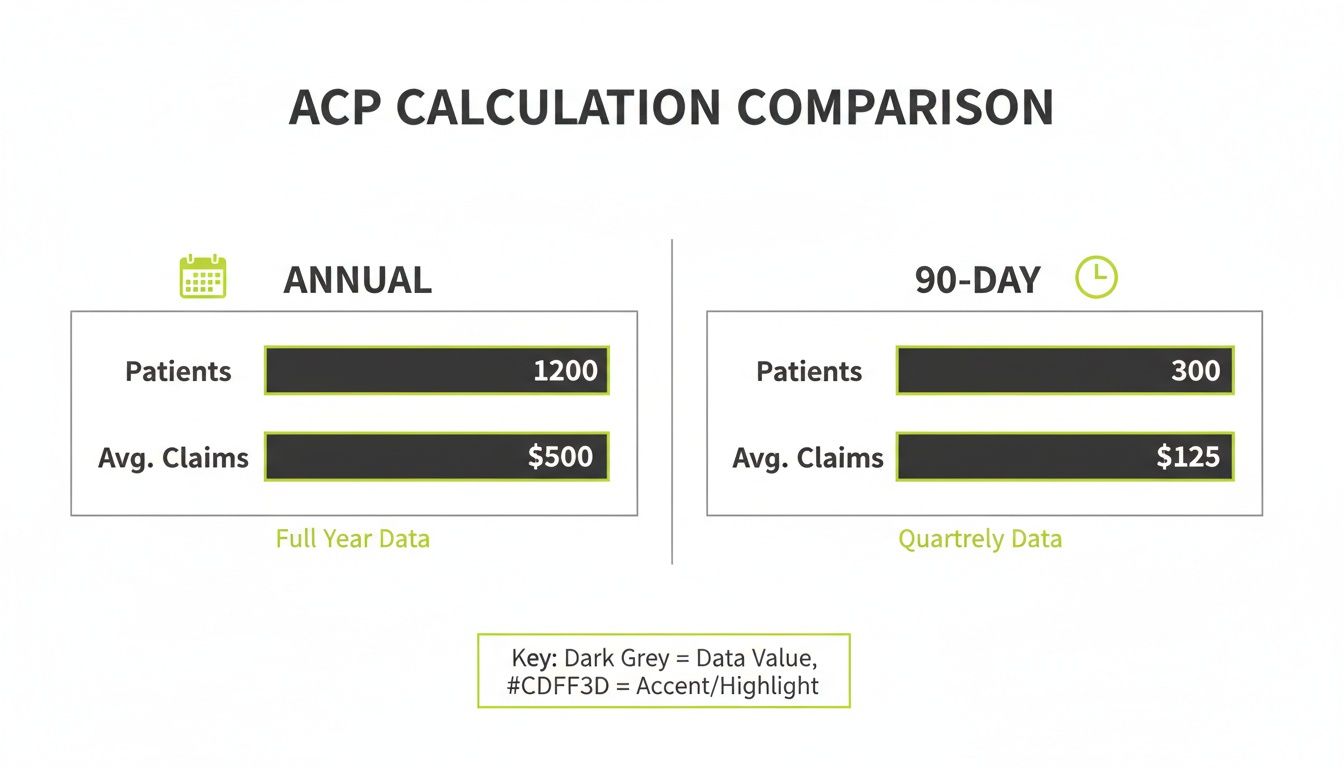

Let's review two applications for a professional services firm: an annual calculation for strategic planning and a rolling 90-day calculation for tactical management.

The Annual Calculation for a Strategic Overview

An annual ACP calculation provides a stable, high-level view, ideal for year-end reporting and setting forward-looking benchmarks. It smooths out monthly volatility.

Consider a hypothetical firm, "Apex Engineering."

- Net Credit Sales (Annual): $8,000,000

- Beginning Accounts Receivable (Jan 1): $1,200,000

- Ending Accounts Receivable (Dec 31): $1,400,000

First, calculate the average accounts receivable for the period.

- Average AR = ($1,200,000 + $1,400,000) / 2 = $1,300,000

Now, apply the ACP formula.

- ACP = ($1,300,000 / $8,000,000) × 365 = 59.3 days

Apex Engineering takes nearly 60 days to collect payment. If its standard terms are Net 45, the 15-day gap is a clear signal of working capital inefficiency.

A common error is to include cash sales in the Net Credit Sales figure. This artificially lowers the ACP, creating a misleading picture of collection speed. Isolate credit sales for an accurate calculation.

The Rolling 90-Day Calculation for Tactical Management

While the annual view informs strategy, a rolling 90-day calculation is essential for active, week-to-week financial management. It identifies emerging issues quickly.

Let's examine Apex Engineering's first quarter.

- Net Credit Sales (Q1): $2,000,000

- Beginning AR (Jan 1): $1,400,000

- Ending AR (Mar 31): $1,600,000

- Number of Days in Period: 90

Calculate the average AR for the quarter.

- Average AR = ($1,400,000 + $1,600,000) / 2 = $1,500,000

Apply the formula using the specific number of days in the measured period.

- ACP = ($1,500,000 / $2,000,000) × 90 = 67.5 days

This is where tactical insight emerges. The ACP jumped from an annual average of 59.3 to 67.5 days. This change prompts the controller to investigate immediately, rather than waiting for quarter-end reports.

Consistent measurement provides the data required for sound operational decisions. It is the foundation to improve cash flow. Tools like QuickBooks AR automation can streamline the data aggregation for this process.

Resolut automates AR for professional services—consistent, accurate, and human.

What Your Collection Period Is Actually Telling You

The ACP is more than a number; it is a narrative about your firm’s financial operations and market position. Understanding this narrative is what drives improvement.

The analysis starts with benchmarking against industry norms. Comparing an architecture firm to a software company is useless. The comparison must be against direct competitors.

Visual Idea: A simple line chart comparing a firm's rolling 90-day ACP against its industry benchmark over 12 months. This visually flags deviations and trends.

Finding Your Industry Baseline

Each professional services sector operates on a different payment cycle. A marketing agency on monthly retainers has a different cash flow profile than an engineering firm on long-term project milestones.

For example, the construction industry average collection period is approximately 70 days. Financial leaders in that sector manage their operations against that known figure. More data on industry collection timelines on sage.com can provide context.

An ACP significantly higher than your industry average is a competitive disadvantage. It indicates your peers are converting revenue to cash faster, enabling them to reinvest while you are funding your clients.

While an annual ACP provides a stable benchmark, a rolling 90-day calculation acts as an early warning system for shifts in client payment behavior or internal process failures.

Translating Trends into Actionable Intelligence

Tracking your firm’s ACP over time reveals trends that are predictive of operational health.

A rising ACP is a red flag for:

- Deteriorating Client Health: A key account may be facing its own liquidity issues.

- Process Breakdown: Your internal follow-up cadence has become inconsistent or ineffective.

- Scope Creep or Disputes: Unresolved project issues are creating valid reasons for payment delays.

A falling ACP is a positive indicator of:

- Process Improvement: Efforts to streamline invoicing or adopt AR software for professional services are delivering results.

- Healthier Client Portfolio: You are successfully onboarding clients with strong payment histories.

- Clear Communication: Your team is setting firm payment expectations from project inception.

Reading these signals transforms a simple metric into a powerful management tool. It moves your finance function from calculation to control.

Tying ACP and DSO to Your Firm's Cash Flow

While Average Collection Period (ACP) and Days Sales Outstanding (DSO) are often used interchangeably, both measure the efficiency of cash collection.

These are not merely accounting terms. They quantify the lag between revenue earned and cash available to operate the business. This lag has a direct, material impact on liquidity.

Visual Idea: Cinematic imagery of a digital dashboard showing a large DSO number in red. A hand reaches out and adjusts a slider, causing the DSO number to decrease and turn green, while a cash reserve balance simultaneously increases.

Reducing this metric is not about aggressive collections; it is about systematic process improvements that strengthen the firm's financial foundation.

The Real-World Impact on Working Capital

Let's quantify the cost of slow payments for a $10M professional services firm with an ACP of 60 days.

The capital tied up in receivables is calculated as: (Annual Revenue / 365 Days) x ACP

For this firm, the calculation is:

- ($10,000,000 / 365) x 60 = $1,643,835

Over $1.6M of earned revenue is unavailable for payroll, investments, or operational expenses.

Now, assume the firm implements process improvements to reduce its ACP from 60 to 45 days.

The new calculation becomes:

- ($10,000,000 / 365) x 45 = $1,232,876

By shortening the collection cycle by 15 days, the firm has unlocked an additional $410,959 in cash. This capital moves from its clients' balance sheets to its own.

From Metric to Strategic Advantage

This freed-up capital is a strategic asset. That $410,000 could fund two senior-level positions, a major technology upgrade, or a strategic marketing campaign without incurring debt.

Such improvements are typically the result of addressing systemic friction—unclear invoices, a lack of payment options, or inconsistent follow-up.

This is where accounts receivable automation delivers a clear ROI. It establishes a consistent system designed to reduce DSO. You can learn more about how to improve cash flow with these strategies.

The goal is to engineer a financial operation where a low ACP is the natural outcome of an efficient, client-centric process.

Resolut automates AR for professional services—consistent, accurate, and human.

Using Automation to Systematically Reduce Your ACP

Knowing your ACP is the diagnosis. Reducing it is the cure. A high ACP in professional services is rarely a surprise; it is the predictable result of manual processes.

Manual follow-up, inconsistent communication, and limited payment options create friction for clients and an operational drag for your team.

Modern accounts receivable automation shifts collections from a reactive, manual burden to a proactive, data-driven system that provides control over cash flow.

Orchestrating Personalized Outreach at Scale

Manual collections are constrained by human capacity. An AI AR automation platform orchestrates personalized, timely outreach for every invoice, without exception.

This is not about generic, automated reminders. It is about intelligent sequences that maintain a human touch and professional tone, aligned with your client relationships.

- Pre-Due Date Nudges: A professional reminder sent days before payment is due.

- Day-Of Notifications: A clear confirmation that payment is expected.

- Post-Due Follow-Ups: A structured cadence of communications with escalating urgency, maintaining a professional tone.

This automated discipline ensures no invoice is overlooked. Understanding workflow automation is key to grasping the power of this structured approach.

Removing Payment Friction

Every obstacle to payment adds days to your ACP. A modern payment portal is one of the fastest ways to improve cash flow by removing this friction.

Instead of waiting for a check to be mailed and cleared, clients can pay instantly via their preferred method, whether credit card or ACH. This alone can reduce collection periods by days or weeks.

The scale of these collection challenges is massive. The U.S. debt collection industry, valued at $20.2 billion, highlights the systemic difficulty businesses face in converting receivables to cash. This environment directly impacts average collection periods and the ability to recover funds effectively.

Proactively Identifying Risk

The most effective way to handle a delinquent account is to prevent it. Intelligent AR software for professional services can analyze payment patterns to flag at-risk invoices early.

This allows your team to intervene with a personal touch where it matters most, long before an account becomes a serious problem.

This proactive approach transforms collections from chasing late payments to actively managing the firm's financial risk. This fits within a broader strategy of receivable management services.

By combining these elements, you build a system that predictably drives down your average collection period.

Resolut automates AR for professional services—consistent, accurate, and human.

From Calculation to Control Over Your Cash Flow

Calculating your average collection period is simple. Using that metric to gain control over your firm’s cash flow is what separates effective financial operators from administrators.

Knowing the number is the starting point. The real work is interpreting the data and methodically fixing the operational friction that inflates it.

This is how a simple metric becomes a powerful lever for financial stability and growth.

The goal is not to chase every late dollar. It is to build a predictable and efficient financial operation where prompt payment is the default outcome.

Bridging Insight and Action

A common mistake is stopping at the calculation. Knowing your ACP is 65 days is an observation. Building a system to reduce it to 45 is a strategy.

With accounts receivable automation, you can ensure consistent, professional follow-up on every invoice. The system maintains a constant, disciplined presence that conditions clients to pay on time. You can find more practical ideas to clean up your accounts receivable.

Combine that consistency with a payment portal that removes friction, and you have addressed the two primary drivers of a high ACP: inconsistent follow-up and difficult payment processes.

This is how you convert a number on a report into tangible, unlocked working capital. The result is a more resilient firm, stronger client relationships, and true control over your financial position.

--- Resolut automates AR for professional services—consistent, accurate, and human.