How to Handle Delinquent Accounts: A CFO's Framework for Control

Discover how to handle delinquent accounts with a proven playbook for CFOs. Use data-driven strategies and AR automation to improve cash flow and reduce DSO.

The work is done, the invoice is sent, and then… silence. The old playbook advises patience, suggesting a 90-day wait before making awkward phone calls.

This reactive approach is a direct threat to cash flow.

Effective delinquency management means identifying at-risk invoices within 15-30 days. It requires a structured, data-driven outreach process that secures payment without damaging client relationships.

The Economic Reality of Delinquent Accounts

Economic headwinds are increasing payment delays, even from historically reliable clients. A reactive collections process is no longer just inefficient; it's a significant operational risk.

This is a systemic issue. Federal Reserve data on the broad rise in delinquent debt shows that in Q1 2025, U.S. credit card delinquency rates rose across all income levels.

Most notably, the highest-income ZIP codes saw a 73% relative increase. This is a clear indicator that even prime clients are facing payment pressures.

Why Your Aging Report Is a Lagging Indicator

The traditional aging report is a historical document. By the time an invoice appears in the 90-day column, the probability of collecting the full amount has fallen dramatically.

After 120 days, recovery rates drop below 50%. This delay directly impacts the firm's financial health.

- It Constrains Cash Flow: Late payments create operational bottlenecks, tying up capital needed for payroll, operations, and strategic investments.

- It Inflates DSO: A high Days Sales Outstanding (DSO) signifies an inefficient cash conversion cycle. It means your working capital is funding your clients' operations, not your own.

- It Diverts Strategic Resources: Your finance team's time is better spent on financial planning and analysis than on manual payment reminders.

A proactive, data-driven system for managing receivables is a prerequisite for financial control. The objective is to orchestrate AR with intention, not chase overdue payments.

The Modern Framework for Delinquency Management

A modern approach protects both cash flow and client relationships. It is built on accounts receivable automation that identifies risk as early as 15-30 days past due.

Effective AR automation analyzes payment histories and communication patterns to predict late payments. This foresight enables early, low-intensity intervention before an account becomes a significant problem.

Integrating systems like QuickBooks AR automation transforms a reactive cost center into a strategic asset that improves cash flow and reduces credit risk.

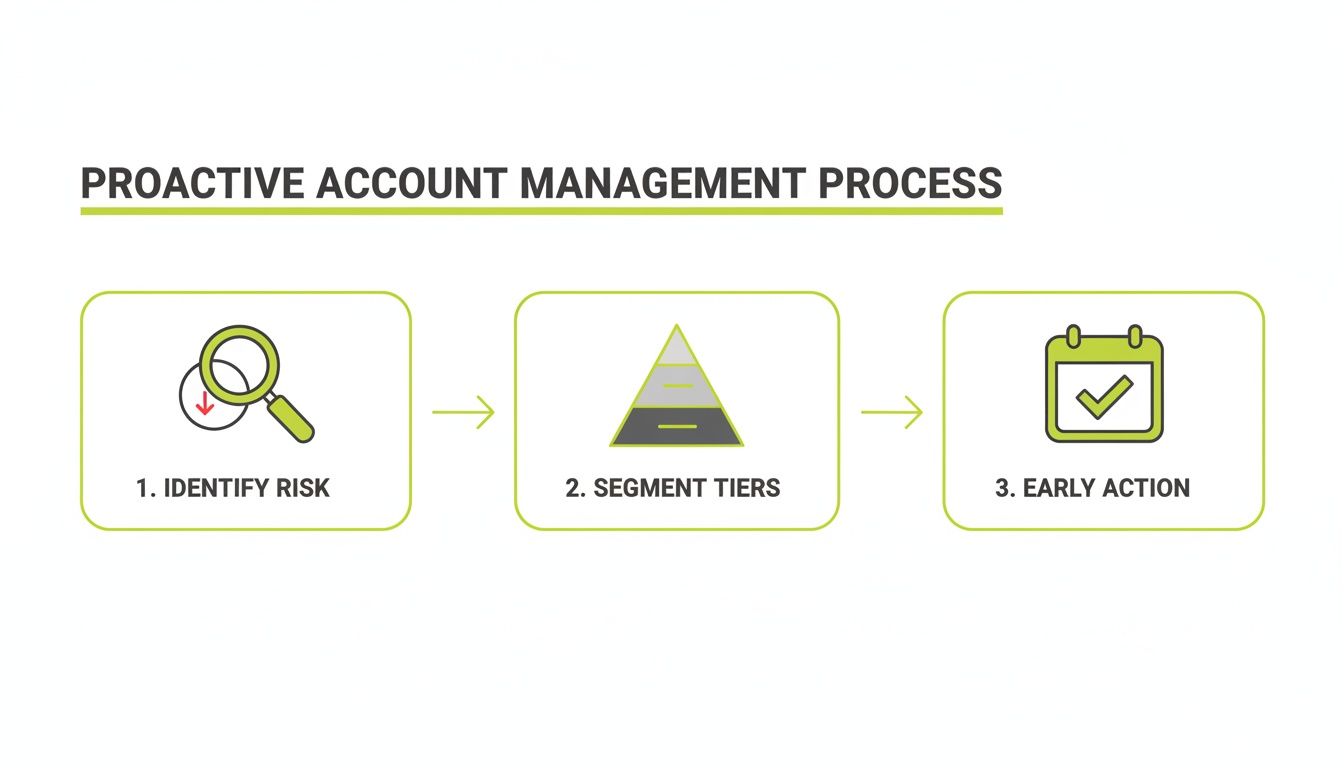

Building a Proactive Account Management Framework

Most firms don't have a collections problem; they have a timing and process problem. They react to aging reports instead of acting on predictive signals.

Effective delinquency management begins before an invoice is due. It involves shifting from lagging indicators to predictive models that identify which accounts are likely to become delinquent.

This framework allows for intervention at 15-30 days past due, when the probability of collection is highest.

From Aging Reports to Predictive Risk Scoring

An aging report shows what has already occurred. A predictive risk score forecasts what is likely to happen next.

A robust risk model synthesizes multiple data points to score each client, providing an early warning system.

Key inputs include:

- Payment History Deviation: A client who consistently pays in 20 days but suddenly takes 45 presents a clear red flag. The deviation from their baseline is the critical signal.

- Communication Patterns: A sudden drop in responsiveness often precedes a payment delay. Modern AR software for professional services can track these engagement metrics.

- Invoice Inquiries: An increase in invoice disputes can indicate client cash flow issues or growing dissatisfaction.

This data-driven approach allows your team to focus its efforts on accounts that pose a genuine risk to your cash flow.

Segmenting Clients for Targeted Action

A one-size-fits-all collections strategy is ineffective. You must tailor your outreach based on client risk profiles.

Grouping clients into tiers—such as prime, standard, and at-risk—enables customized communication cadences. As delinquency rates rise, this segmentation becomes critical. TransUnion data on rising consumer delinquency rates shows the percentage of consumers 60+ days past due reached 1.31% in Q2 2025, a post-recession high.

Our data indicates prime customers respond best to gentle nudges within 30 days, resulting in an 85% collection rate. At-risk accounts often require firmer communication by day 60 to achieve a 65% recovery rate—a figure that drops to 20% if you wait until 90+ days.

The core principle is to match the intensity of your follow-up to the risk profile and value of the account. A strategic client with a temporary issue requires a different approach than a chronically late, low-margin account.

Risk-Based Segmentation and Action Triggers

This framework connects client segments to specific, time-based actions, ensuring a consistent and appropriate application of pressure.

Client Segment | Risk Score | 15-30 Days Overdue Action | 31-60 Days Overdue Action | 61-90 Days Overdue Action |

|---|---|---|---|---|

Prime / Strategic | 0-30 | Automated, gentle email reminder. | Personal email from account manager. | Phone call from senior team member. |

Standard | 31-60 | Automated multi-touch (email + SMS). | Automated call from finance team. | Formal demand communication. |

Subprime / At-Risk | 61-100 | Immediate call from finance specialist. | Formal demand communication. | Escalate to collections/legal review. |

The key is to establish a clear protocol and execute it consistently.

Leveraging Automation for Early Intervention

Manual tracking of these early warning signs is not scalable. This is where accounts receivable automation provides a distinct operational advantage.

Systems powered by AI AR automation monitor payment behaviors and flag deviations in real time.

For example, a platform with QuickBooks AR automation can sync with your accounting data, identify when a client's average days-to-pay increases, and automatically initiate a pre-defined outreach sequence tailored to that client's risk profile. This mirrors the logic of using proactive customer outreach to reduce churn. You can learn more in our guide to structured receivable management services.

This framework systematizes the collections process, smooths cash flow, and enables your finance team to focus on high-value strategic initiatives.

Designing an Omnichannel Outreach Cadence

A generic email reminder is insufficient. The communication sent to a strategic partner at 15 days past due must differ from the one sent to a chronically delinquent account at 60 days.

An effective outreach cadence methodically increases urgency while maintaining professionalism. It leverages different communication channels based on their specific strengths.

The objective is a clear, consistent, multi-channel sequence that protects the client relationship while compelling action.

Why an Omnichannel Approach Is Essential

A modern outreach strategy uses the right channel at the right time. Applying principles from what omnichannel customer service is to AR is key.

Each channel serves a specific function:

- Email for Documentation: Creates a formal record of communication, which is invaluable in the event of a dispute.

- SMS for Immediacy: With an open rate over 98%, text messages cut through inbox clutter for direct calls-to-action, such as a payment link.

- Phone Calls for High-Stakes Issues: A direct call adds a necessary human touch for high-value invoices, complex disputes, or unresponsive accounts.

AI AR automation platforms can orchestrate these channels into a cohesive workflow, personalizing messages based on client data and risk profile without manual intervention.

Effective outreach begins with a structured approach to risk and segmentation—before the first reminder is ever sent.

Building The Cadence by Stage

A well-designed cadence applies methodical pressure. This is a sample for a "Standard" risk client.

Days 15-30 Past Due: Professional Reminders

The tone is helpful, assuming an oversight.

- Day 15 (Email 1): Automated reminder. Subject: "Reminder: Invoice [Invoice #] Past Due." The body includes the amount and a direct payment link.

- Day 25 (Email 2): Second automated email. The tone is slightly firmer. Subject: "Follow-Up: Action Required on Invoice [Invoice #]."

Days 31-60 Past Due: Direct Prompts

Outreach becomes more direct and expands to new channels. The assumption shifts from oversight to requiring attention.

- Day 35 (SMS Notification): "Notice from [Your Firm]: Invoice [Invoice #] for [Amount] is now overdue. Pay securely: [Link]."

- Day 45 (Automated Call): A pre-recorded, professional message from the finance team reiterates the overdue status.

- Day 55 (Email 3): A more formal email notes previous contact attempts and requests an immediate payment update.

Firms using flexible payment portals can increase self-service payments by 40%, while a well-tuned automated cadence can manage up to 90% of routine collections activity.

An automated, multi-channel cadence does not replace human judgment. It frees your team to apply that judgment to complex, high-value accounts.

The Human-in-the-Loop Model

Automation should augment, not replace, your team. The best accounts receivable automation platforms operate on a human-in-the-loop model.

The system manages repetitive follow-ups but flags exceptions for human intervention.

If a strategic client becomes 45 days past due or disputes an invoice, the automated sequence pauses, and the case is assigned to a finance specialist. This model blends the efficiency of automation with the critical thinking of your team, which is exactly how modern AR automation protects client relationships.

This system ensures timely, persistent follow-up, reducing the payment cycle and creating predictable cash flow.

Negotiating Payments and Structuring Plans

When automated reminders fail and a client remains unresponsive, the process shifts from collection to recovery negotiation.

This requires a pivot from an automated sequence to a direct, human conversation. The objective is not leniency but pragmatism—to secure cash when the standard process fails.

Opening the Negotiation

The initial direct contact must be firm yet empathetic. The goal is to diagnose the root cause of non-payment.

Use open-ended questions. Instead of "Why haven't you paid?" use "We've noted invoice [#] is significantly overdue. Can you share what's causing the delay on your end?" This opens a dialogue rather than putting the client on the defensive.

A successful negotiation establishes a new, viable payment agreement. Securing cash is the primary objective, even on a revised timeline.

A smart accounts receivable automation system facilitates this by flagging the account and providing a complete communication history, enabling your team to enter the conversation fully informed.

A Framework for Payment Solutions

Two primary tools are available: settlement discounts and structured installment plans. The choice depends on the client's situation and the amount owed.

- Settlement Discount (Lump Sum): Offer a 5-10% discount for payment in full within a few business days. This accelerates cash receipt and resolves the issue.

- Structured Installment Plan: For clients with genuine cash flow constraints, break the total into smaller, manageable payments. This often maximizes the total amount recovered over time.

For a $20,000 overdue invoice, an offer might be a settlement for $18,500 paid within five days, or four weekly payments of $5,000.

Automating and Documenting the Plan

Immediately document any new agreement. Send a confirmation email outlining the new terms to serve as a written record.

Modern AR software for professional services allows you to input this new payment plan directly into the system.

Platforms with QuickBooks AR automation can then manage the revised schedule by:

- Sending automated reminders before each installment is due.

- Processing scheduled payments via the client portal.

- Flagging any missed payments on the new plan for immediate follow-up.

This process removes manual tracking burdens and holds the client accountable. For more on this, review our real-world ways to clean up your accounts receivable.

Blending human negotiation with automated execution creates a system capable of recovering funds from difficult accounts without overburdening your team.

Knowing When to Escalate the Process

Not every delinquent account is resolved through negotiation. For clients who become unresponsive or refuse to pay, a pre-defined escalation path is a critical financial control.

A clear, data-driven protocol removes emotion from the decision-making process. It ensures consistency and protects the firm from allocating resources to unrecoverable debts.

Defining Data-Driven Escalation Triggers

An effective escalation policy is based on objective criteria. When an account hits a specific threshold, a pre-determined action is taken.

Your triggers should combine financial and behavioral data:

- Days Past Due: For professional services firms, an invoice reaching 90-120 days overdue without a payment plan is a critical trigger.

- Total Amount Owed: Establish specific dollar thresholds that automatically trigger a review by a senior finance leader, bypassing the standard cadence.

- Communication Silence: If a client ignores all contact attempts for 15-30 consecutive days, it signals a significant problem beyond simple oversight.

An escalation protocol creates an unavoidable decision point. It forces a clear choice on whether to invest more resources, based on data, not emotion.

The Escalation Ladder: Internal and External Steps

Once a trigger is hit, the account moves up an escalation ladder, starting with internal resources.

Stage 1: Internal Executive Involvement

The first step is involving a senior team member—a Controller, CFO, or firm partner. A communication from an executive signals that the issue is now a firm-level priority and often elicits a response.

This represents a final, good-faith effort to resolve the matter directly.

Stage 2: 'Voice of a Lawyer' Communication

Modern AI AR automation platforms can send a formal notice with the authoritative tone of a legal letter.

This communication is not a lawsuit but serves as a precursor. It formally states the debt, references prior collection attempts, and outlines the consequences of non-payment. This tactic often spurs payment without the expense of engaging legal counsel.

Stage 3: Third-Party Collections or Legal Action

This is the final step. The decision to engage a collections agency or take legal action must be purely economic.

Agencies typically charge 25-50% of the amount collected. Legal action is more costly. This step is reserved for high-value accounts where the ROI is clear. For smaller debts, a write-off is often more prudent.

AR software for professional services is invaluable here. It packages the complete communication history for the agency or lawyer, enabling them to proceed efficiently.

Measuring AR Performance: From Activity to Outcome

Managing delinquent accounts is an ongoing operational function. To confirm your strategies are effective, you must track key performance indicators (KPIs).

The goal is to build a predictable system that produces measurable improvements in the firm's financial health by reducing the time, cost, and risk associated with the AR portfolio.

The KPIs That Matter

While many metrics are available, only a few are critical for assessing collections effectiveness.

- Days Sales Outstanding (DSO): The primary measure of how efficiently you convert revenue into cash. A declining DSO is a direct indicator of improved AR management.

- Collection Effectiveness Index (CEI): Measures the percentage of receivables collected during a specific period. CEI provides a clear benchmark of team performance.

- Aged AR Percentages: Track the percentage of receivables in each aging bucket (e.g., 31-60, 61-90, 90+ days). An effective strategy will shift balances from older to more current buckets.

The objective is to transform accounts receivable from a reactive cost center into a strategic asset that helps improve cash flow and strengthen the balance sheet.

From Chaos to Controlled Orchestration

This framework provides a clear path from manual, reactive collections to a state of controlled AR orchestration. It is not about replacing your team but augmenting their judgment with powerful tools.

AI AR automation enables you to manage the entire invoice lifecycle with precision. For firms on QuickBooks, integrating QuickBooks AR automation creates a seamless flow from invoice creation to cash collection.

*Visual Idea 1: A dashboard chart showing a clear, downward trendline for Days Sales Outstanding (DSO) over six months, labeled "DSO Reduction After AR Automation Implementation."*

A systematic approach removes inconsistency from a critical business function, ensuring every account is handled with a data-driven process that protects revenue and client relationships.

*Visual Idea 2: A CFO calmly reviews AR analytics on a tablet. In the blurred background, their finance team is engaged in collaborative, strategic work, not making collection calls.*

This is the new standard for professional services firms committed to financial control and sustainable growth.

--- Resolut automates AR for professional services—consistent, accurate, and human. Find out more at https://www.resolutai.com.