A CFO's Guide to the Letter of Demand for Money Owing

A definitive guide for CFOs on crafting a letter of demand for money owing. Learn to improve cash flow, reduce DSO, and manage AR with expert precision.

A letter of demand for money owing isn't an act of aggression. It's a control function.

For a finance operator, it marks the shift from routine follow-ups to a structured recovery process. It’s about enforcing commercial terms, creating an official record, and protecting the firm’s working capital.

It’s a standard operational procedure, not a personal dispute.

The Strategic Role of the Demand Letter in AR Management

For a professional services firm, a letter of demand is a critical tool for financial control. It converts a delinquent account from an operational issue into a formal commercial dispute requiring resolution. Its function is to protect cash flow and reduce DSO.

The letter serves two operational purposes. First, it establishes an unambiguous, official record of the debt and the firm's intent to collect.

Second, it signals to the client that standard payment terms have been breached, and the recovery process is now entering a more formal phase.

Differentiating From Standard Follow-Ups

Routine reminders are part of a standard accounts receivable workflow. They are often automated and assume a simple oversight by the client.

A letter of demand marks a deliberate shift in tone and intent. It assumes polite reminders have been ineffective and the firm must now formally assert its position to protect its financial interests.

This distinction is critical. A standard follow-up preserves the client relationship. A demand letter signals that the financial component of that relationship is now at risk. It is a calculated action designed to elicit a response.

A Data-Driven Financial Instrument

Operationally, the demand letter is a trigger within a defined workflow, not an emotional reaction to non-payment.

A firm might establish a rule: an account hitting 60 days past due automatically initiates the demand process. This removes subjectivity and ensures consistent application of the credit policy.

For professional services firms, a disciplined escalation process is a hallmark of strong financial governance. A well-timed letter of demand can reduce the collection period by 10-15 days for accounts in the 60–90 day aging bucket, directly impacting liquidity.

Systematizing this step builds a predictable collections timeline. This procedural rigor is essential if legal action or third-party collections become necessary. Reviewing strategies on how to collect unpaid invoices effectively can add valuable context to internal protocols.

Protecting Cash Flow and Controlling DSO

The value of a demand letter is measured by its impact on key financial metrics. Every dollar in aged receivables is working capital unavailable for payroll, growth, or investment.

A formal demand process directly accelerates collections on the most stubborn accounts. This is a key differentiator for sophisticated finance operations. Many firms find that receivable management services provide the necessary structure for consistent execution.

The objective is not to sever client relationships, but to enforce the agreed-upon commercial terms. A firm, professionally executed demand letter reinforces that the firm's services hold value and payment is a non-negotiable part of the agreement.

Crafting a Demand Letter That Works

A letter of demand for money owing is an instrument of precision. Its purpose is to state the facts of the debt and the consequences of non-payment, creating a formal record for potential escalation.

The document must be fact-based, unambiguous, and free of accusatory language. The tone should be firm and professional—an execution of standard business process, not a confrontation. Accuracy is paramount.

Define the Debt with Unshakable Clarity

The core of an effective demand letter is a statement of debt that leaves no room for misinterpretation. Vague references to an "outstanding balance" invite delays.

List the exact services rendered. Reference each invoice by its unique number and date. This provides the client’s finance team an immediate reference point and demonstrates meticulous record-keeping.

For example: "Invoice #4812, dated March 15, for Q1 strategic consulting services." This level of detail confirms the claim’s legitimacy.

Calculate Fees and Set a Firm Deadline

If the contract allows for late fees or interest, show the calculation. State the contractual basis for the charges and present the simple math.

Next, set a clear, non-negotiable payment deadline. A window of 7 to 30 days from the letter's date is standard. This creates urgency while remaining reasonable. An ambiguous deadline like "as soon as possible" signals a lack of resolve.

A well-drafted letter including principal, calculated fees, a hard deadline, and clear consequences converts 20–40% of delinquent accounts without further action.

State Consequences, Not Threats

The consequences for non-payment must be framed as a procedural next step, not a threat. Remove emotional or aggressive language.

Instead of, "If you don't pay, we will be forced to take legal action," use:

"Should the full balance not be settled by the specified deadline, this matter will be escalated to our external collections partner for recovery."

This phrasing frames the action as a standard, predetermined step in the firm’s credit policy. It removes personal sentiment and reinforces a controlled, systematic process.

Starting with a solid legal demand letter template can provide a strong foundation for this process.

Assembling the Essential Components

A professional letter of demand is a formal document built from specific, non-negotiable components. Each element serves a purpose, from establishing facts to outlining required actions. Omitting any piece weakens its legal standing.

This checklist ensures all bases are covered.

Essential Components of a Professional Letter of Demand

A checklist of critical elements every demand letter must include to meet legal and professional standards.

Component | Purpose and Key Details |

|---|---|

Clear Identification | Your firm’s name, address, and contact info on official letterhead. The recipient's full legal name and address. |

Precise Debt Details | Every relevant invoice number, its original due date, and a brief, factual description of the services provided. |

Total Amount Owed | The exact principal amount. Separately itemize any accrued interest or late fees as defined in the service agreement. |

Unambiguous Deadline | A specific date for payment. "Within 14 days of the date of this letter" is standard and effective. |

Payment Instructions | Clearly outline payment methods (e.g., wire transfer, online portal) and provide all necessary details. |

Consequences of Non-Payment | State the specific, predetermined next step (e.g., referral to collections) in a neutral, procedural tone. |

Official Record Clause | A formal statement indicating this is an attempt to collect a debt and information obtained will be used for that purpose. |

Structuring the letter this way transforms it from a request into an instrument of financial control. It demonstrates that your firm manages its accounts receivable with discipline.

When and How to Send Your Demand Letter

In accounts receivable, timing is a strategic lever. Sending a letter of demand for money owing too early appears aggressive. Sending it too late suggests payment terms are flexible, damaging cash flow and financial discipline.

The effectiveness of this letter depends entirely on its timing and delivery method. It is an operational decision with direct financial consequences.

The Optimal Window for Escalation

For professional services, the optimal window to send a formal demand letter is between 15 and 30 days past the due date.

This period is a strategic sweet spot. It allows standard, automated reminders sufficient time to work, justifying escalation. It is also early enough to convey urgency before the debt becomes a heavily aged receivable.

Acting within this timeframe demonstrates process control. It shows the firm operates on a predictable schedule, applying the same procedural rigor to all overdue accounts.

B2B receivables data supports this. A formal demand sent within this 15–30 day window can reduce the need for external recovery services by 15–25% compared to waiting until 60 or 90 days. More on economic trends can be found by reviewing global financial outlooks and stability on IMF.org.

The objective is to shorten the entire collection cycle. The probability of collection drops significantly with each passing month. A demand at 30 days past due is far more effective than one sent at 90.

Choosing the Right Delivery Method

The delivery method must align with the letter's purpose: creating an undeniable, auditable record of the demand.

Delivery Options and Their Strategic Use

- Certified Mail with Return Receipt: The standard for legal weight. It provides indisputable proof of sending and receipt, creating a paper trail essential for potential litigation.

- Secure Email with Read Receipts: For speed and efficiency. Modern AR software for professional services can automate this, providing digital confirmation of both delivery and open rates.

A hybrid approach is common: send via tracked email for immediate impact, followed by a physical copy via certified mail for legal documentation. This dual-channel strategy makes it impossible for a client to claim non-receipt.

Automating Timing for Consistency

Manually tracking invoices for escalation is inefficient and prone to error. Inconsistency in timing creates an unpredictable client experience and volatile cash flow.

This is where accounts receivable automation provides a distinct advantage. An AR platform can be configured to automatically generate a demand letter when an invoice hits a specific trigger—for example, 25 days past due. The system enforces credit policy without manual intervention.

Systems offering QuickBooks AR automation can trigger these workflows, ensuring every overdue account is handled with the same discipline. This helps reduce DSO and frees up the finance team for higher-value analysis.

A systematic approach transforms the demand letter from a reactive chore into a proactive component of your strategy to improve cash flow.

Shifting from Manual Drafting to AR Automation

Manually drafting and sending a letter of demand for money owing is an operational drag. The process is inefficient, prone to inconsistency, and difficult to track. It is a reactive measure, typically initiated only after an account becomes a significant problem.

For firms focused on disciplined financial management, this legacy approach is inadequate. The logical step is toward strategic accounts receivable automation. This is about converting the entire escalation workflow from a manual burden into a proactive, data-driven component of your cash flow strategy.

Systematizing the Escalation Workflow

The primary benefit of automation is consistency. An AR platform can be configured to automatically flag invoices meeting specific triggers—for example, any account 30 days past due with a balance over $5,000.

When a trigger is met, the system executes the pre-designed playbook. This is not about removing human judgment; it is about applying that judgment systematically to every account, every time. It eliminates the risk of inconsistent treatment of clients.

Automation removes the operational friction and emotional hesitation from the collections process. It ensures the firm's credit policy is enforced consistently, which is the foundation of effective working capital management.

This systematic approach builds a complete, auditable trail. Every communication is logged, timestamped, and tracked centrally.

Ensuring Data Accuracy and Professional Tone

A manually drafted demand letter is susceptible to errors—an incorrect invoice number, a miscalculation of interest, or an unprofessional tone. Such mistakes can undermine the letter's authority and create unnecessary disputes.

AI AR automation mitigates this risk by integrating directly with your ERP or accounting software, such as with QuickBooks AR automation. It uses real-time data to populate approved templates.

- Invoice Details: The system pulls correct invoice numbers, service dates, and principal amounts automatically.

- Accrued Fees: It calculates late fees or interest based on contract terms, eliminating manual calculation.

- Client Information: It uses the correct contact information and legal entity name, ensuring proper addressing.

This precision ensures every letter of demand is professional, accurate, and defensible. The tone remains procedural, reinforcing that this is a standard business process. Our guide on accounts receivable automation software provides further detail on these systems.

From Reactive Burden to Proactive Control

Without automation, the finance team is constantly chasing the most overdue accounts—a poor use of their expertise. AR software for professional services reverses this dynamic.

Instead of waiting for an account to become a problem, the system flags at-risk invoices early. It can analyze payment histories and other data to predict which clients may become delinquent, enabling proactive intervention.

* **Visual Idea: A clean, data visualization chart showing "Probability of Collection vs. Invoice Age." A steep curve drops sharply after the 30-day, 60-day, and 90-day marks, visually reinforcing the need for timely escalation. ***

This proactive approach directly impacts financial performance. By systematizing the demand process, firms can reliably reduce DSO and improve cash flow. This aligns with best practices that emphasize fast, documented communication, as noted in research from institutions like the Federal Reserve Bank of San Francisco.

The goal is to build a predictable collections engine. Automation makes the letter of demand a standard, measured, and effective step in protecting your firm’s financial health.

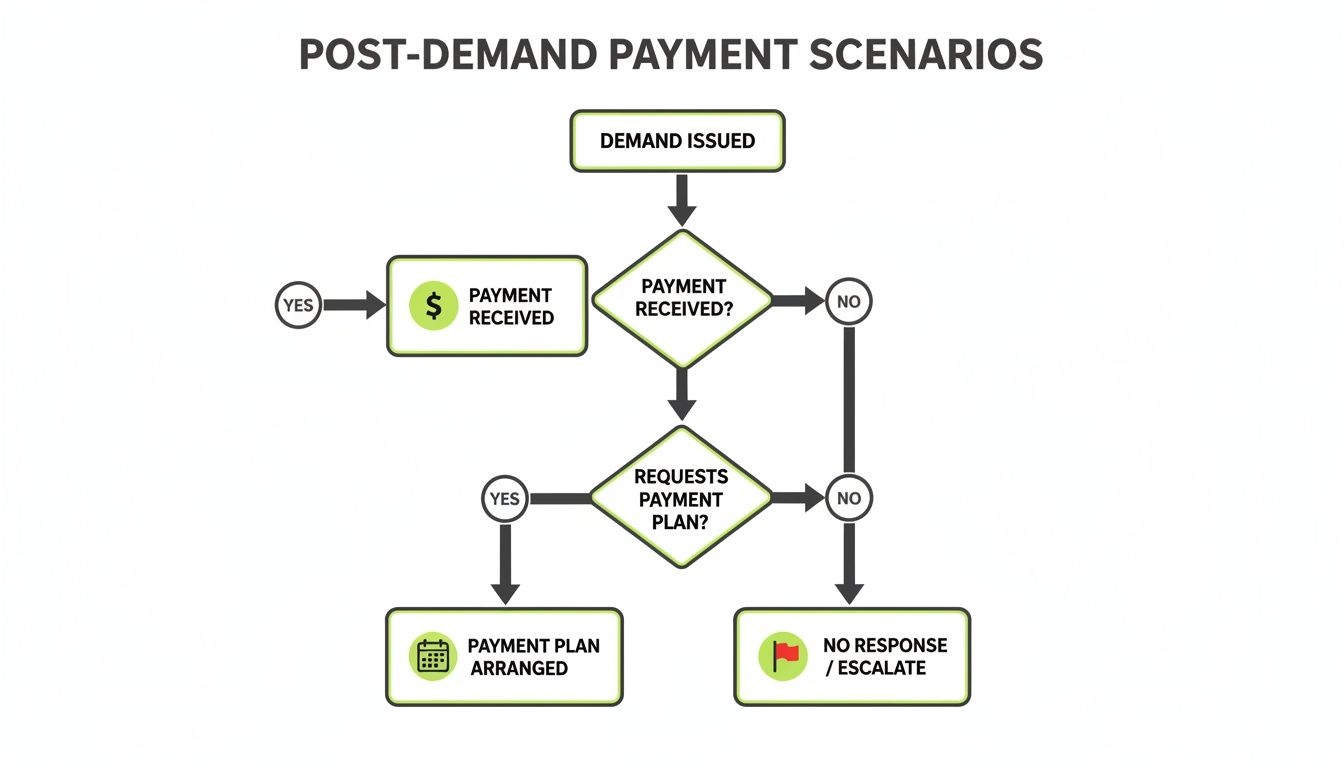

Post-Demand Scenarios and Responses

Sending the letter of demand is not the final step; it is the start of a formal escalation process. The client's response—or lack thereof—determines the next action.

From this point, your response must be as disciplined as the letter itself. After the payment deadline passes, one of three outcomes will occur. Each requires a planned, systematic response to maintain control.

Scenario 1: The Client Pays in Full

This is the desired outcome. A firm, professional demand has functioned as intended.

Once payment is received, send a brief, professional confirmation acknowledging receipt. A simple note confirming the matter is resolved provides official closure and reinforces the firm's organized approach.

Scenario 2: The Client Proposes a Payment Plan

A request to pay in installments is the beginning of a negotiation, not a solution. The objective is to secure the debt without surrendering legal leverage.

If a payment plan is accepted, it must be formalized in a written agreement. This is non-negotiable. The agreement must clearly define:

- The total amount owed.

- The exact amount and due date of each payment.

- The consequences of a single missed payment (e.g., the full balance becomes immediately due).

This converts a verbal promise into an enforceable instrument. It prevents trading one large overdue invoice for a series of smaller ones.

The flowchart below maps these three paths, providing a clear operational guide for your team.

As shown, every outcome requires a specific, disciplined response. Maintaining control of the process is paramount, regardless of the client's action.

Scenario 3: The Client Does Not Respond

Silence is a definitive response. The probability of voluntary payment plummets after a formal demand is ignored. Hesitation at this stage signals that stated deadlines are not firm.

This is the trigger to escalate according to your credit policy. For most firms, this means a handoff to a third party.

A non-response to a formal demand letter is a definitive trigger. The account should be immediately escalated according to the firm’s credit policy—whether to an external collections partner or legal counsel—to maintain process integrity and maximize recovery potential.

Using AR software for professional services can automate this handoff. The system can compile all necessary documents—invoices, communications, the demand letter—and transmit them directly to your collections partner. For firms managing this internally, understanding accounts receivable outsourcing can help determine when to engage specialists.

This is not a punitive action. It is the execution of a predictable financial process designed to protect firm assets and improve cash flow.

Questions from the Finance Department

CFOs and Controllers must balance financial controls with client relationships. Implementing a formal demand letter process often raises key operational questions.

Will a Demand Letter Damage a Client Relationship?

An aggressive, emotional, or unexpected letter can damage a relationship.

However, a professional, fact-based letter sent as part of a standard, documented credit policy is different. Most businesses understand that procedural steps are part of commerce.

When framed as a systematic action, a demand letter is perceived as operational discipline. Consistency is key; applying the policy uniformly removes subjectivity.

A well-structured AR process signals financial stability. It communicates that your firm takes its commercial agreements seriously. This is a sign of a well-run business.

* **Visual Idea: Cinematic imagery of a steady hand signing a formal, well-structured document in a modern, organized office. The lighting is clean and focused, conveying control, precision, and calm authority. ***

Is This Worth the Effort for Smaller Balances?

Chasing a $500 invoice with the same resources as a $50,000 one is an inefficient allocation of capital.

A materiality threshold is essential. Your credit policy should define a clear cutoff. For balances below that line, a less intensive, fully automated follow-up sequence is more efficient. This allows the finance team to focus on high-value receivables that materially impact cash flow and DSO.

AR software for professional services is designed to manage these parallel workflows—high-touch for strategic accounts and low-touch for smaller balances—simultaneously.

How Does Automation Integrate with Legal Escalation?

Accounts receivable automation and legal action are sequential steps in a single, cohesive workflow.

The automation platform serves as the system of record. It builds a detailed, time-stamped audit trail of every communication, from initial invoice to final demand.

When an account requires escalation to a collections partner or legal counsel, this documented history is invaluable. A platform with AI AR automation can package this entire record, providing the legal team with a clean, complete, and defensible file. This accelerates the recovery process and strengthens your legal position.

--- Resolut automates AR for professional services—consistent, accurate, and human. Learn more at https://www.resolutai.com.