A CFO's Guide to Mastering Net 30 Days and Cash Flow

A definitive guide for CFOs on mastering net 30 days. Learn how to optimize payment terms, slash DSO, and boost cash flow with AR automation.

For professional services firms, net 30 days is the default payment term: a client has 30 calendar days from the invoice date to remit payment. It's a straightforward, accepted standard.

In theory. In practice, it's often the source of significant cash flow friction.

The Hidden Costs of Standard Net 30 Terms

Net 30 provides a baseline for forecasting, but the forecast rarely reflects reality. The 30-day promise routinely extends to 45, 60, or even 90 days.

This isn't a minor administrative issue. It's a strategic liability that inflates Days Sales Outstanding (DSO) and constrains working capital. The root cause is operational, not contractual.

The Disconnect Between Policy and Reality

The problem with net 30 isn't the term itself, but its inconsistent enforcement. Finance teams are caught in a repetitive cycle of manual follow-ups, chasing revenue that is already earned.

These hours represent a significant opportunity cost, diverting skilled personnel from high-value financial analysis to clerical collection tasks.

The challenge isn't a client problem; it's an operational one. It demands a systematic solution to master—not just manage—your accounts receivable.

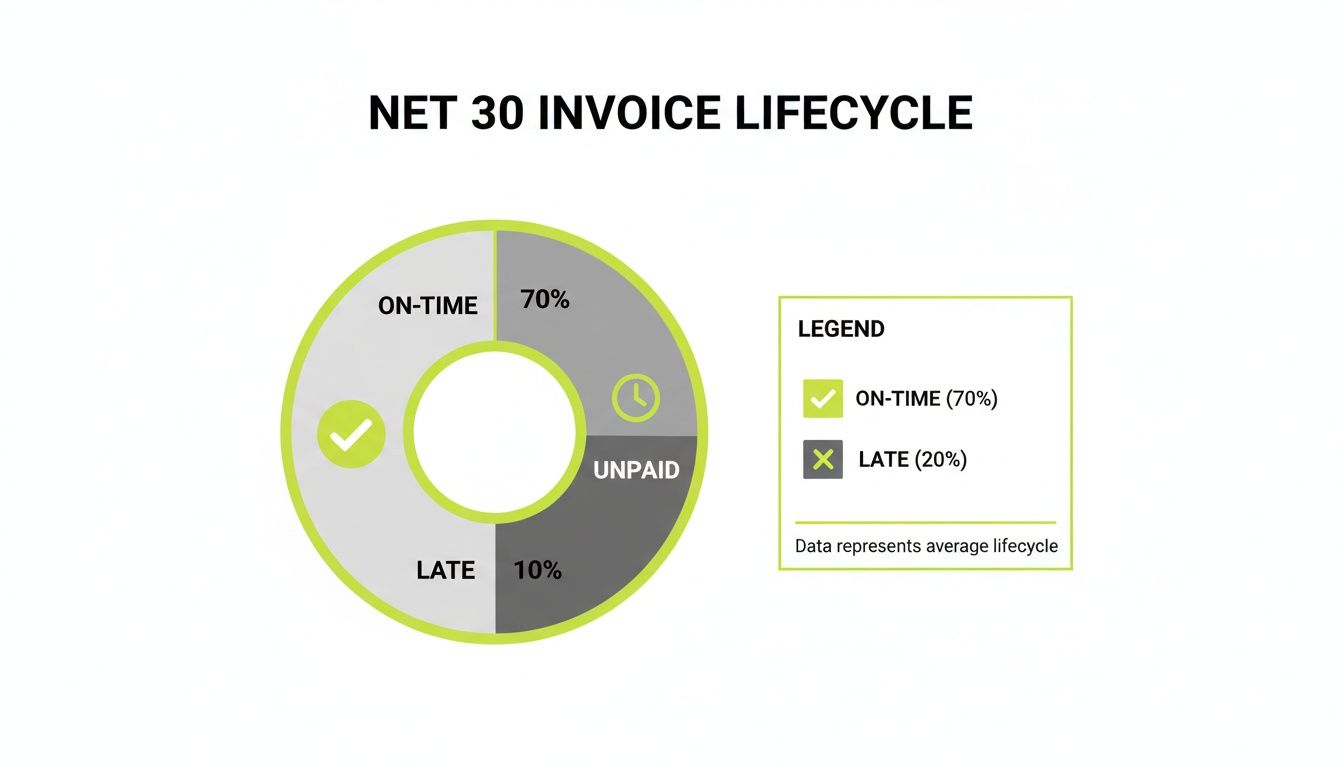

This disconnect has measurable consequences. Globally, only 52-58% of net 30 invoices are paid on time. A significant portion—10-15%—drift more than 30 days past due. You can dive deeper into the statistics on B2B payments at Clearly Payments.

(The Real Lifecycle of a Net 30 Invoice)

Moving from Reactive to Proactive AR Control

Accepting late payments as a cost of doing business is a flawed premise. Financial control requires shifting from a reactive collections model to a proactive system built on consistency and clarity.

This is where technology like accounts receivable automation becomes a critical lever. An effective AR system operates with precision, using intelligent workflows to ensure timely communication without manual intervention.

This approach doesn't just reduce DSO; it delivers predictable cash flow, providing the visibility required for accurate strategic planning. The objective is to enforce payment terms methodically while preserving client relationships.

Calculating the True Financial Drag of Delayed Payments

Delayed payments are not just an entry on an aging report. They represent a tangible drag on your firm's profitability and capacity for growth.

The first step is to quantify the dollar-for-dollar impact of every late invoice. This begins with a disciplined analysis of your Days Sales Outstanding (DSO).

Mastering the Days Sales Outstanding (DSO) calculation is essential. DSO is a direct measure of how long it takes for invoiced revenue to become usable cash.

Translating DSO into Working Capital Impact

Consider a professional services firm with $10 million in annual revenue.

A 30-day DSO corresponds to an accounts receivable balance of approximately $822,000. If DSO slips to 45 days—a common scenario with lax net 30 enforcement—the AR balance increases to over $1.23 million.

That $411,000 difference is capital that should be funding strategic initiatives, key hires, or technology investments. Instead, it is trapped in the receivables ledger. This is the direct cash flow impact of delayed payments.

The financial drain intensifies as DSO expands.

Financial Impact of DSO on a $10M Services Firm

DSO | Accounts Receivable Balance | Working Capital Impact (vs. 30-Day DSO) |

|---|---|---|

30 Days | $821,918 | $0 |

45 Days | $1,232,877 | -$410,959 |

60 Days | $1,643,836 | -$821,918 |

75 Days | $2,054,795 | -$1,232,877 |

At a 60-day DSO, over $821,000 of the firm's own capital is unavailable. It is a silent tax on operational capacity and growth potential.

This chart illustrates how many invoices in a typical net 30 cycle fail to meet their payment deadline.

This is not an anomaly; it is the standard operating reality for most firms. A significant portion of invoices will miss their due dates, directly inflating DSO and straining cash reserves.

The Hidden Operational Costs of Chasing Payments

Beyond the direct cash flow impact, a high DSO introduces hidden operational costs that erode profitability.

- Labor Costs: Finance and administrative teams spend valuable hours manually tracking overdue invoices, drafting reminder emails, and making collection calls. These are salaried hours that could be reallocated to strategic financial analysis.

- Relationship Strain: A clumsy collections process introduces friction into client relationships, potentially jeopardizing future engagements. Professionalism in collections is paramount.

- Opportunity Cost: Every dollar tied up in overdue AR is a dollar not working for the firm. This represents the cost of a missed opportunity—a service line not launched, a key hire passed over, or a technology investment deferred.

These factors compound, turning what appears to be a simple administrative function into a significant financial liability. You can explore the true cost of AR inefficiency in professional services in more detail.

Beyond Net 30: Strategic Payment Terms to Improve Cash Flow

Adhering to a standard Net 30 policy for all engagements surrenders control over a critical asset: cash. A one-size-fits-all model is operationally inefficient.

The objective is to move from a reactive collections posture to a proactive billing strategy, where payment terms are aligned with project scope, client profile, and the firm's capital requirements.

The Early Payment Discount: A Financing Decision

A common alternative is the early payment discount, often structured as “2/10 Net 30.” This offers the client a 2% discount for payment within 10 days, with the full amount otherwise due in 30 days.

This is not a simple incentive; it is a financing decision. You are paying the client for early access to your own capital. The critical question for a finance operator is whether the cost is justified.

A 2% discount for payment 20 days early is equivalent to an annual percentage rate (APR) of over 36%. This "small" discount carries a significant cost of capital.

This high rate is not inherently negative. If the firm's cost of capital is higher, or if immediate liquidity is required for a specific, high-return opportunity, it can be a sound strategic choice. However, it should be deployed selectively, not as a blanket policy. When you're ready to dial in your financial operations, review our guide to effective receivable management services.

*Visual Idea 1: *A clean, minimalist chart titled "The True Cost of a 2/10 Net 30 Discount." A bar chart visually compares the 2% discount to a ~36% APR, highlighting the significant financial implication.

Shorter Terms and Upfront Deposits

A sophisticated firm tailors its terms to mitigate risk and optimize cash flow.

- Net 15 Terms: For short-duration projects or new clients without an established payment history, Net 15 terms are a prudent choice. They reduce financial exposure and set a clear expectation for prompt payment from the outset.

- Upfront Deposits or Retainers: For large, multi-month engagements, requiring a deposit (25-50%) is standard practice. It de-risks the project by securing client commitment and provides the initial capital to commence work.

This approach is about strategic risk management, not rigidity. It protects the firm while maintaining the flexibility required for complex partnerships. This is where AR software for professional services excels, allowing for the automated application of specific terms based on client or project parameters.

*Visual Idea 2: *A cinematic image of a controller calmly reviewing a project plan and a client contract side-by-side, conveying a sense of strategic decision-making and control over financial terms.

Building a System for Enforcing Payment Terms

Effective accounts receivable management depends on two core principles: clear communication and consistent execution. Without a system, payment terms are merely suggestions.

An enforcement policy is not about aggression. It's about creating a professional, predictable process that protects cash flow. This process begins long before an invoice is issued.

Every contract and statement of work must contain unambiguous language specifying the net 30 days policy, invoice delivery methods, and the protocol for late payments. This preempts future misunderstandings.

Setting Clear Expectations From Day One

The invoice itself must be clear, concise, and professional. Vague or confusing invoices invite payment delays.

Every invoice should include these non-negotiable elements:

- A Clear Due Date: Display the exact date payment is due, not just "Net 30."

- Itemized Services: A clear breakdown of services rendered prevents questions that stall the payment process.

- Multiple Payment Options: Facilitate prompt payment by offering ACH, credit card, and bank transfer options through a secure online portal.

- Contact Information: Provide a direct point of contact for billing inquiries to enable rapid resolution.

While net 30 terms are a B2B standard, market realities are shifting. Average supplier payment terms have stretched to 46 days as buyers optimize their own cash positions, a trend detailed in KPMG's 2025 supplier payment index.

The Escalating Follow-Up Cadence

Once an invoice is issued, enforcement relies on a structured, escalating follow-up system. The goal is persistence without unprofessionalism. This is where accounts receivable automation provides a distinct advantage, ensuring no invoice is overlooked.

A disciplined cadence transforms a reactive process into a proactive one, helping to reduce DSO and establish control over the financial timeline.

An automated, systematic follow-up process removes emotion and inconsistency from collections. It ensures every client receives the same professional treatment, protecting both your cash flow and your client relationships.

An ideal workflow uses a multi-channel approach with a progressively firmer tone. This signals commitment to payment terms while providing ample opportunity for the client to remit payment.

The following schedule outlines a practical, proactive workflow.

A Proactive Payment Term Enforcement Schedule

Timing (Relative to Due Date) | Action | Communication Channel | Tone |

|---|---|---|---|

7 Days Before | Proactive Payment Reminder | Automated Email | Helpful & Courteous |

1 Day After | Gentle Nudge | Automated Email & SMS | Professional & Direct |

7 Days After | Direct Follow-Up | Personal Email from AR Specialist | Firm & Inquiring |

15 Days After | Scheduled Phone Call | Direct Phone Call | Solution-Oriented |

30 Days After | Final Notice & Escalation | Certified Letter / Legal | Formal & Authoritative |

This systemized approach builds the consistency that is foundational to effective AR management. It professionalizes the collections function, making it predictable and less reliant on manual, ad-hoc efforts.

How AR Automation Creates Predictable Cash Flow

Reliance on manual processes—spreadsheets and calendar reminders—to enforce net 30 days terms is a primary driver of unpredictable cash flow. The inefficiency is not due to a lack of effort, but to the inherent limitations of the system itself.

Intelligent accounts receivable automation fundamentally changes this dynamic. It does not replace finance professionals; it equips them with a system that enforces payment terms with perfect consistency.

This transforms a reactive, manual function into a proactive, strategic advantage that directly contributes to financial stability.

From Reactive Chasing to Proactive Engagement

The core weakness of manual AR is its reactive nature. An invoice becomes delinquent before any action is taken. This approach creates gaps where invoices are missed and follow-ups lack urgency.

AI AR automation closes these gaps. It operates on a predefined workflow, engaging clients at precise intervals.

- Automated, Personalized Reminders: The system sends a reminder before an invoice is due, a notification on the due date, and a series of escalating follow-ups if it becomes overdue. Communications can be tailored by client or invoice value to maintain a human touch.

- Omnichannel Outreach: An effective platform reaches clients via their preferred channel—email, SMS, or an automated call—to ensure the message is received.

- Self-Service Payment Portals: Reducing payment friction is critical. A dedicated client portal to view invoices, ask questions, and remit payment via ACH or credit card removes common logistical hurdles.

These are not merely features; they are systematic solutions to the root causes of slow payments. Learn more about the specific benefits of accounts receivable automation.

Eradicating Errors and Gaining Financial Insight

True AR automation extends beyond reminders to provide deeper financial control. It eliminates the costly errors inherent in manual processes and delivers clear visibility into client payment behaviors.

Automated cash application, for instance, replaces hours of manual payment-to-invoice matching in QuickBooks. This eliminates reconciliation errors that consume staff time and compromise the accuracy of financial reports. Effective QuickBooks AR automation ensures the integrity of your general ledger.

By systematizing outreach and reconciliation, automation transforms AR from a cost center defined by manual labor into a strategic function that produces predictable cash flow and actionable financial intelligence.

An intelligent system also provides predictive insights. By analyzing payment patterns, it can flag at-risk accounts, allowing for proactive intervention before an invoice becomes severely delinquent. When necessary, the system should also clarify the process to collect unpaid invoices effectively.

This proactive approach is the key to systematically reduce DSO and stabilize revenue forecasts. It shifts the operational focus from collecting aged debt to ensuring current invoices are paid on time.

The Path to Financial Control and Clarity

Mastering accounts receivable is not about more aggressive collection tactics; it is about implementing an intelligent, consistent system.

The traditional manual approach to AR is a liability. It is unpredictable, labor-intensive, and creates friction with clients, trapping finance teams in a reactive cycle.

By implementing smart accounts receivable automation, finance leaders transform AR from a cost center into a strategic asset. This systemic shift provides the tools to improve cash flow with precision.

Systematize for Stability

An automated system delivers predictable financial outcomes. It enables firms to:

- Reduce DSO by enforcing net 30 days terms with unwavering consistency.

- Gain a clear, data-driven view of payment trends and client behaviors.

- Reallocate finance team resources from tedious follow-ups to high-value analysis.

This is the definition of financial control: moving beyond managing debt to strategically orchestrating the firm's most critical asset—cash.

A Few Lingering Questions

Implementing a disciplined AR process often raises practical questions. Here are the most common inquiries from financial leaders.

When Should We Offer Terms Longer Than Net 30?

Extended terms like Net 60 should be viewed as a strategic concession, reserved for high-value, established clients with impeccable payment histories, typically in the context of a major, long-term contract.

Before agreeing to such terms, model the impact on working capital. For the vast majority of clients, a firm net 30 days policy is the most prudent approach to maintaining predictable cash flow.

Extended terms are a form of financing provided to your client. The decision should be subject to the same scrutiny as any other allocation of capital. Does the expected return justify the cost to your balance sheet?

How Does AR Automation Integrate with QuickBooks?

Leading AR software for professional services is not a standalone silo. It integrates directly with accounting systems like QuickBooks via a secure, two-way API.

This ensures that all invoice, customer, and payment data is continuously synchronized. When a payment is made through the AR platform's portal, it is automatically recorded, matched to the correct invoice, and reconciled in QuickBooks. This QuickBooks AR automation eliminates manual data entry, prevents errors, and ensures your books are always accurate.

Won't Automating Collections Annoy Our Clients?

On the contrary. A well-designed automation system enhances professionalism. It makes the payment process predictable, transparent, and convenient for your clients. A timely, automated reminder is perceived as a helpful service, not an aggressive demand.

Providing a simple, self-service portal to view and pay invoices improves the client experience. Accounts receivable automation manages the consistent, polite follow-ups, freeing your team to engage with clients on substantive matters rather than payment logistics.

--- Resolut automates AR for professional services—consistent, accurate, and human.