Payment Term Definition: A Guide to Cash Flow Control

A clear payment term definition for CFOs. Learn to manage DSO, improve cash flow, and leverage AR automation to enforce terms and get paid faster.

Unpaid invoices drain significant amounts from enterprise cash flow every year. For a finance leader, that should change the way you define payment terms.

Too many firms still treat terms as standard invoice language that sits in the footer and never gets reviewed. In practice, term design affects when cash lands, how much follow-up AR needs, and how often the business ends up extending credit without pricing that risk.

In professional services, a payment term definition sets more than a due date. It establishes the operating rule for how revenue converts into cash, who carries the financing burden, and what actions the team can take when a client pays late. That makes payment terms part of working capital management, not just contract administration.

The finance impact is measurable. Term structure influences DSO, forecast accuracy, borrowing needs, and the amount of receivables that slip into aging buckets. It also determines whether AR automation can enforce reminders, escalations, and collections discipline, or whether the team is stuck working around exceptions.

A useful payment term definition gives finance control from contract to collection. That is the standard worth using.

Payment Terms as a Strategic Financial Instrument

Controllers usually see the damage first. Revenue looks healthy. Pipeline looks healthy. Yet cash remains tight because invoices sit open longer than expected, exceptions pile up, and collections depends on whoever remembers to follow up.

That is why payment terms belong in the same conversation as pricing, staffing, and working capital management. They are not paperwork. They are a direct lever on liquidity.

Why finance should treat terms like policy

A weak term structure creates silent risk:

- Sales introduces exceptions: One client gets Net 45. Another gets milestone billing with no deposit. A third pays only after internal approval.

- AR inherits ambiguity: The team cannot enforce what was never clearly defined.

- Cash forecasting degrades: Expected receipts become guesses instead of scheduled cash events.

The balance sheet feels all of it. Receivables age. Borrowing needs rise. Internal confidence in the forecast drops.

What works and what does not

What works is a deliberate design. You decide which clients qualify for standard terms, which engagements require upfront payment, and which projects need staged billing. You link that structure to invoice delivery, reminder timing, and escalation rules.

What does not work is relying on relationship goodwill alone.

Key takeaway: A payment term definition only matters if it changes client behavior and can be enforced operationally.

In professional services, this point is sharper because delivery often precedes billing discipline. Teams complete work, send the invoice late, and then accept loose terms to preserve the relationship. That sequence forfeits an advantage twice.

A stronger approach is simple. Set terms at the proposal stage. Repeat them in the contract. Carry them into the invoice. Then let your AR process enforce them consistently. When terms become part of financial architecture, not an afterthought, cash flow becomes more predictable and the balance sheet gets stronger.

The Anatomy of an Effective Payment Term

Analysts at Tipalti note that clear payment term design combines six specific fields and that firms using configurable terms see better first-time payment performance (Tipalti). That matters because payment terms do more than define when cash is due. They set the rules your billing system, AR team, and client AP process will follow. If any field is missing or vague, DSO usually moves in the wrong direction.

An effective term has to survive contact with operations. It has to be clear enough for a client to pay without clarification, specific enough for your system to calculate automatically, and structured enough for collections to enforce without making exceptions on every invoice.

The six elements that remove ambiguity

Every payment term should spell out six points.

- Amount owed Errors start here. Partial billing, approved change orders, pass-through expenses, taxes, and credits all need to roll into one amount the client recognizes. If the invoice total surprises the buyer, the due date becomes irrelevant because the invoice is headed for dispute.

- Invoice date This is the date your clock starts. If the contract says Net 30 but the invoice date is delayed, edited, or inconsistent across systems, your collection timeline slips before AR even begins follow-up.

- Payment due date State the calendar date, not only shorthand like Net 30. Buyer AP teams route invoices by explicit due dates. Your collectors also need a fixed trigger for reminder sequences and escalation.

- Accepted payment methods Say exactly how you expect to be paid. ACH, wire, card, check, portal, and any restrictions should be visible on the invoice and aligned with the contract. Payment friction often comes from avoidable questions, not unwillingness to pay.

- Geographical payment location This field matters whenever legal entities, remittance addresses, lockboxes, or banking instructions differ. It matters even more in cross-border billing, where a missing remittance detail can delay payment for reasons that have nothing to do with client intent.

- Discounts or penalties If you offer 2/10 Net 30, define the discount window and calculation clearly. If you charge late fees, specify when they begin, how they are calculated, and whether they are enforced in practice. A clause AR will never apply is not a control.

For finance teams that want a practical reference, these invoice payment terms examples show how the wording changes by billing model and risk profile.

Why the details matter

Small wording decisions produce measurable downstream effects. A missing due date leads to inconsistent reminder timing. An unclear payment method pushes the client back to email. A vague penalty clause gives sales room to negotiate after the invoice is already late.

I have seen firms focus on headline terms like Net 30 and miss the operating detail that decides whether Net 30 functions like 30 days or 47. The contract says one thing. The invoice says another. Collections improvises. Cash arrives when the client gets around to sorting it out.

Clear terms improve payment speed because three sources of delay are removed early:

- The billed amount matches approved work

- The due date is explicit

- The remittance path is simple

Practical tip: If AR repeatedly answers questions like “When is this due?” or “Which account should we use?”, the term is incomplete, even if the contract looks legally sound.

The controller’s test

Before approving a standard term, run it through four control questions:

Control question | Why it matters |

|---|---|

Can a client understand it without contacting us? | Cuts avoidable payment delay |

Can our billing system calculate it automatically? | Reduces manual error and invoice rework |

Can AR enforce it the same way every time? | Supports consistent collections and cleaner aging |

Can cash application reconcile it without guesswork? | Improves close speed and receivable visibility |

A payment term is effective when legal language, invoice configuration, and collection workflow match. That is the point where a definition becomes a financial control.

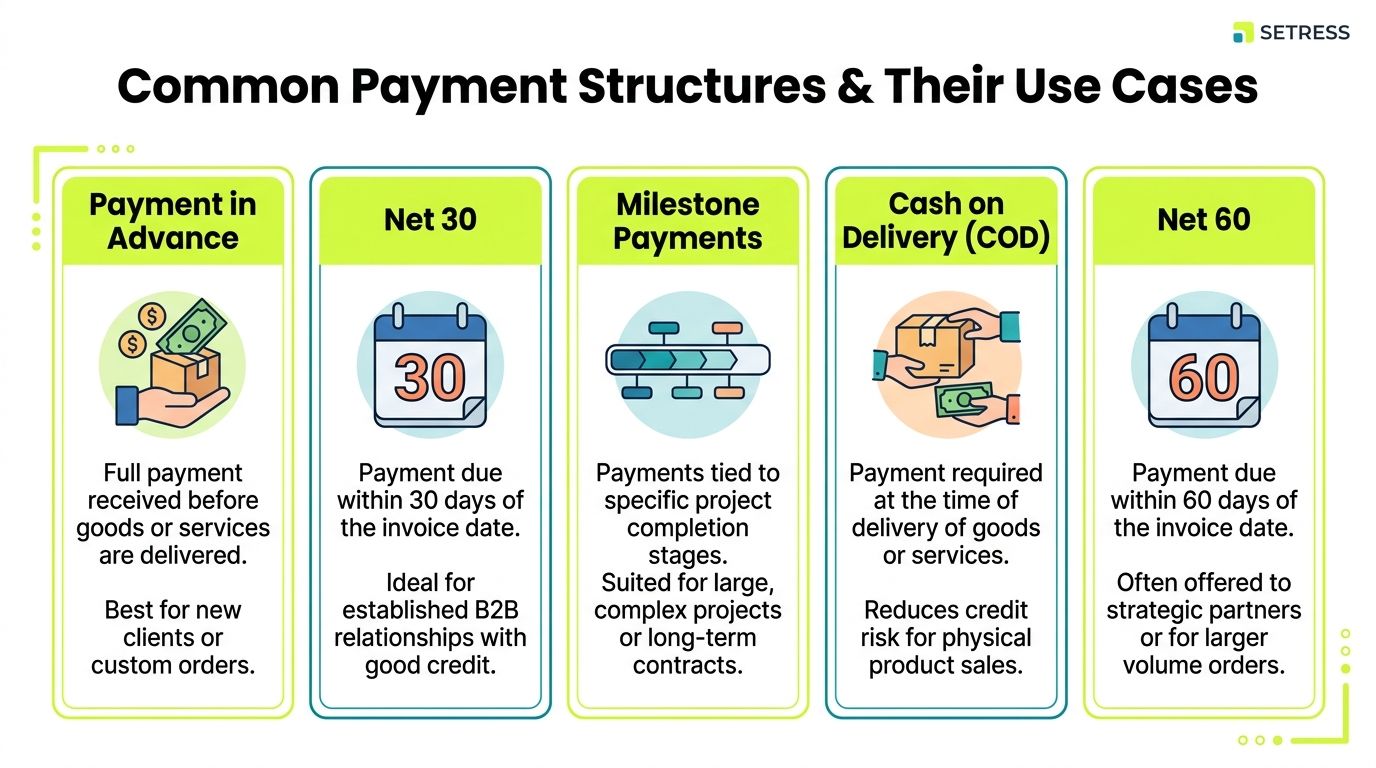

Common Payment Structures and Their Use Cases

Not every client should receive the same terms. The right structure depends on risk, project shape, negotiation power, and how much working capital your firm is willing to fund.

Net 30 became the most widely adopted standard across industries because it balances seller financing needs with buyer cash management capabilities. Standard variations include Net 15, Net 45, Net 60, and Net 90 depending on industry norms (Swipesum).

For professional services firms, the decision is less about tradition and more about fit.

Payment in advance

Best for new clients, custom work, urgent projects, or any engagement where the scope may move quickly.

This structure protects margin and reduces collection risk before work starts. It also tests buyer seriousness. If a client resists a reasonable deposit, the issue is usually not process. It is commitment.

Use it when onboarding risk is high or delivery begins immediately.

Net 30

This is often the cleanest baseline for established B2B relationships.

It gives the client enough time to route the invoice internally while keeping your receivables within a manageable cycle. For many firms, Net 30 is the default term that supports both client convenience and internal cash discipline.

For more examples of how firms phrase these clauses in practice, this guide to invoice payment terms examples is useful.

Net 60

Net 60 is usually a commercial concession, not a neutral default.

It may be justified for strategic accounts, larger enterprise buyers, or situations where procurement power sits heavily with the customer. But finance should treat it as a deliberate investment of working capital. Longer terms can be appropriate. They should never be accidental.

End of month terms

EOM structures can work well when the client runs a rigid monthly AP cycle.

These terms often reduce internal friction on the client side because the due date aligns with their close process. They are useful when a calendar-based payment habit is more realistic than a straight day-count rule.

Milestone payments

For long projects, milestone billing often fits better than a single invoice at the end.

A few examples:

- Discovery completed: Bill after the first defined deliverable is accepted.

- Build phase approved: Trigger the next invoice when a project stage closes.

- Final delivery: Reserve the last invoice for the handoff or go-live point.

This structure reduces the financing burden on your firm and keeps commercial accountability aligned with delivery.

Use case rule: The more customized, longer, or labor-heavy the engagement, the less sense it makes to wait until the end to bill.

A simple decision lens

Structure | Best fit | Main advantage | Main risk |

|---|---|---|---|

Payment in advance | New or higher-risk clients | Protects cash before delivery | Can create sales friction |

Net 30 | Established service relationships | Balanced and familiar | Easy to weaken through exceptions |

Net 60 | Strategic enterprise accounts | Supports larger buyer demands | Extends cash cycle materially |

EOM | Clients with fixed AP runs | Matches buyer workflow | Can obscure the true collection timeline |

Milestone billing | Long or complex projects | Shares cash burden across delivery | Requires strong project discipline |

What works is choosing terms based on economics and enforceability. What does not work is using one default for every client and then negotiating from weakness later.

Quantifying the Impact on DSO and Cash Flow

A five-day reduction in DSO can release a meaningful amount of cash from receivables. The exact figure depends on revenue scale, but the mechanics are simple. Shorter terms, cleaner discount design, and tighter enforcement pull cash forward. That improves liquidity without adding debt.

Payment terms belong in the same conversation as borrowing costs, hiring plans, and covenant headroom. A term change from Net 30 to Net 60 is not an administrative preference. It is a working capital decision. A 2/10 Net 30 structure is also a financing decision, because you are paying 2% to accelerate cash by 20 days. Oracle’s explanation of discount terms shows that the implied annualized rate on that tradeoff exceeds 36%, and notes that tiered discount structures can reduce DSO by 5 to 10 days on average while preserving customer relationships (Oracle).

A simple model on a $100,000 invoice

Use a single invoice to make the trade-off visible.

Payment Term | Cash Received by Day 10 | Cash Received by Day 30 | Total Cash Received | Effective Cost to Firm |

|---|---|---|---|---|

Payment in advance | $100,000 | $100,000 | $100,000 | No collection float |

Net 30 | $0 | $100,000 | $100,000 | Cash tied up for 30 days |

2/10 Net 30 if client pays early | $98,000 | $98,000 | $98,000 | 2% discount for faster cash |

2/10 Net 30 if client pays on day 30 | $0 | $100,000 | $100,000 | No discount, standard delay |

Net 60 | $0 | $0 | $100,000 | Cash tied up for 60 days |

The headline number is not the discount. It is the timing.

If receivables are funding payroll, subcontractors, or tax payments, 20 to 30 extra days outstanding can force the business to draw on a line of credit or slow investment elsewhere. I have seen firms approve longer terms to win a deal, then give back margin through financing cost and collection effort over the next two quarters. The invoice still gets paid. The balance sheet does the waiting.

What to measure before approving a concession

CFOs usually get better decisions by testing three variables together instead of looking only at the invoice amount:

- Cash conversion effect: How many days does this term add or remove from expected collection?

- Margin effect: Does the discount or delay erase the economics of the deal?

- Behavioral effect: Will the customer reliably follow the agreed term, or treat it as a starting point for paying even later?

That is where payment terms become a strategic financial instrument instead of boilerplate. The term on paper matters, but the measured outcome matters more. If Net 45 customers pay on day 58, your real policy is not Net 45.

A practical review starts with segmenting customers by payment behavior, margin profile, and strategic value. Then model the likely DSO outcome for each segment. Teams that need extra modeling capacity sometimes bring in outside Financial Analysts to build scenario views by customer class, discount policy, and expected collection pattern.

Controller's test for term quality

Use four questions:

- How much cash does this term trap in AR? Calculate the receivables increase from the added days outstanding.

- What are we getting in return? Higher volume, better pricing elsewhere, longer contract duration, or partial prepayment are all valid offsets.

- Can operations enforce it? A well-written term that billing, collections, and sales do not follow will not improve DSO.

- What happens if the customer misses it? If there is no reminder sequence, escalation path, or account hold, the term is weaker than it looks.

The firms that manage DSO well do not stop at defining terms. They quantify the cost of each exception, track payment behavior against the contract, and adjust the policy when results drift. That is how a payment term definition turns into cash flow control.

Negotiating Terms and Establishing a Firm Policy

A term sheet does not improve cash flow by itself. Policy does, because policy decides who can offer Net 60, when a deposit is required, and what happens when a customer misses the date.

The practical failure point is usually not the standard term. It is uncontrolled exceptions. Sales agrees to extended terms to close a deal. Delivery teams promise to wait for payment until project sign-off. Finance sees the change only after the invoice ages past due. At that point, DSO is already drifting and the balance sheet is carrying the cost.

Start by setting one default term for the bulk of revenue and writing down the conditions for any deviation. That creates a control point before the contract is signed, not after the invoice is overdue. For many teams, the policy should sit beside the quoting and billing workflow, supported by accounts receivable automation practices that make exceptions visible and enforce approval rules.

Set policy around approval rights, not preferences

A useful policy is short, specific, and tied to authority. It should answer five operational questions:

- What is the default term? Net 30, due on receipt, milestone billing, or another standard structure.

- Which accounts require stricter terms? New customers, low-margin work, custom projects, or clients with weak payment history.

- Who can approve exceptions? Sales manager, controller, CFO, or legal, depending on the size and risk of the deviation.

- What must appear on the invoice? Clear due date, accepted payment methods, dispute instructions, and any late payment language allowed by contract.

- When does collection escalate? Reminder timing, collector outreach, service hold, shipment hold, and outside counsel review.

That is the difference between a policy people can execute and a policy that gets ignored.

Negotiate for cash outcome, not just term language

Longer terms are not always bad business. They are expensive business unless you get something back. If a strategic customer asks for Net 60, quantify the trade. Higher annual volume, stronger pricing, partial prepayment, auto-debit, or tighter billing milestones can offset the added days in AR. If none of those offsets exist, the company is funding the customer without a return.

The best negotiation question is simple: what operational issue is driving the request? Sometimes AP runs on a fixed monthly cycle. Sometimes the customer cannot process invoices until a purchase order or receiving document is attached. Sometimes procurement drops in standard language that no one reviewed against payment behavior. Those are different problems, and they call for different fixes.

A controller should push for terms that collections can enforce. If the customer wants a long approval chain before payment, split the billing into milestones. If invoice intake is manual, fix the submission process or use tools such as OCR software for invoices so required fields and supporting documents reach AP correctly the first time.

Cross-border contracts need more than a day count

International terms need tighter review because enforceability, invoice rules, tax treatment, and local payment practice can all affect collection speed. A contract that says Net 30 may still pay much later if the legal entity is wrong, the invoice format does not meet local requirements, or the late payment clause is weak under the governing law.

For cross-border accounts, review these points before execution:

Policy element | What to define |

|---|---|

Default terms | Your standard day count or billing structure |

Exceptions | Which clients or deals qualify for deviations |

Approval rights | Who signs off on nonstandard terms |

Invoice standards | Required wording, due date display, payment methods |

Escalation path | Reminder schedule and collections handoff |

Strong policy gives the commercial team room to win business without giving away working capital by accident. That is how payment terms move from contract language to financial control.

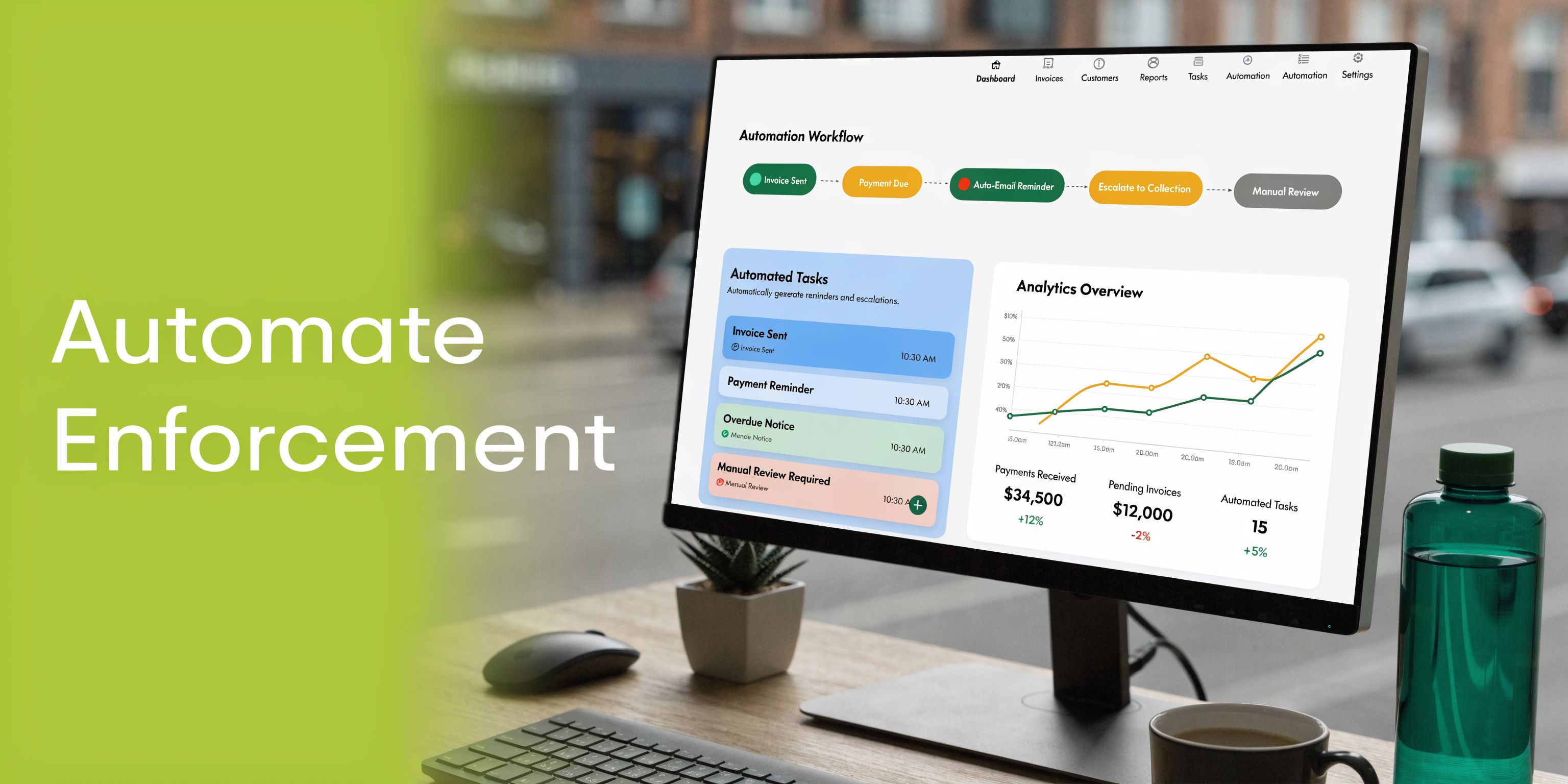

Enforcing Terms with AR Automation

Late payment usually looks like a collections problem on the surface. In practice, it often starts with execution gaps inside billing and receivables. Terms are agreed in the contract, but the invoice goes out days late, the due date is calculated inconsistently, or follow-up depends on a manual queue that slips during close.

Accounts receivable automation improves control by turning payment terms into scheduled, auditable actions.

The point is not to send more reminders. The point is to enforce the commercial agreement consistently, at scale, without adding headcount every time volume grows.

What automation should do

A useful AR workflow should apply the term logic correctly from the start. Net 30, milestone billing, retainers, deposits, and early-pay discounts need to calculate automatically and appear clearly on the invoice. If the system cannot interpret the agreed term structure, finance ends up policing exceptions by hand.

It should also run the collection calendar without manual intervention. Pre-due reminders, due-date notices, overdue follow-up, and internal escalation tasks should trigger based on policy, customer segment, and invoice status. That is how a term moves from invoice text to operating discipline.

Good automation also removes payment friction. ACH, card, and portal options shorten the gap between approval and settlement. For firms evaluating the full workflow, this guide on how to automate accounts receivable shows how collections, outreach, and cash application can sit in one controlled process.

Then there is exception handling. A collector needs one place to see disputes, promised payment dates, prior touches, and blocked invoices. Without that record, teams keep restarting the conversation, and aging stretches for preventable reasons.

AI AR automation and the control advantage

The strongest use of AI in AR is prioritization. It helps the team decide which invoice needs a reminder, which account needs a call, and which item should stay in a low-touch sequence. That matters because a $2,000 invoice due tomorrow and a $200,000 invoice stuck in approval are not equal risks.

Used well, AI AR automation supports judgment rather than replacing it. Finance still sets policy, approval thresholds, escalation rules, and tone. The system handles timing, pattern recognition, and queue discipline.

Data quality determines how far that control goes. If invoice fields arrive in inconsistent formats, due dates and workflow rules break downstream. Teams cleaning up intake often pair AR automation with document capture tools. This overview of OCR software for invoices is a practical starting point for standardizing invoice data before it reaches AR.

A short walkthrough helps make the shift tangible.

What works in practice

Teams that bring DSO down usually get three operating habits right.

- Invoice at the first valid billing trigger If the contract allows billing on delivery, milestone completion, or time approval, send it then. Waiting for month-end gives away days of cash conversion for no commercial benefit.

- Automate routine contact First reminders, payment links, and internal follow-up tasks should run on a schedule. Collectors should spend time on exceptions, not on assembling lists.

- Escalate based on risk and value High-balance accounts, repeat slow payers, and disputed invoices need different treatment from standard current balances. A flat sequence misses that distinction.

Practical tip: If your collector spends the week sending first reminders and correcting due dates, the business does not have an enforcement process. It has manual catch-up.

AR software for professional services works best when it reflects how those firms bill. Partial invoices, change orders, retainers, milestone schedules, and client-specific exceptions all need structured handling. Once that structure is in place, payment terms start doing what finance intended. They shape customer behavior, protect DSO, and give the balance sheet more predictable cash conversion.

From Definition to Financial Control

A strong payment term definition does more than explain when money is due. It sets the rules for how your firm converts revenue into cash.

That requires precision in the contract, discipline in the invoice, judgment in negotiations, and consistency in collections. When those pieces line up, DSO becomes easier to manage and forecasting becomes more credible.

The difference between average and strong AR performance is usually not one heroic collector. It is a system. Clear terms. Limited exceptions. Timely billing. Consistent follow-up. Good tooling.

For finance leaders in professional services, that is the key opportunity. Payment terms are not administrative language. They are part of financial control.

Resolut automates AR for professional services with a practical focus on consistency, accuracy, and human oversight. If you want a cleaner way to enforce payment terms, reduce manual follow-up, and improve cash flow without making client communications feel robotic, you can learn more at Resolut.