A CFO's Guide to Mastering Positive Cash Flow

A practical guide for CFOs on how to achieve and sustain positive cash flow. Learn to reduce DSO and improve liquidity using AR automation.

There's an old saying in finance: "Profit is an opinion, but cash is a fact." For professional services firms, this isn't a clever line—it's an operational reality. A strong P&L can show profitability, but it doesn't guarantee you have the cash on hand to make payroll, invest in growth, or fund operations.

The Critical Difference Between Profit and Positive Cash Flow

Many finance leaders have learned that reported profit and actual cash in the bank are two very different metrics. Profit, typically calculated on an accrual basis, records revenue when earned, not when the client's payment hits your account. This timing difference is where financial risk originates.

You can appear profitable on paper after signing a large engagement, all while your cash reserves are dwindling.

This is where positive cash flow becomes the central focus. Think of it as the operational lifeblood of your firm. It's the real, tangible cash moving into and out of your business. When you have strong, positive cash flow, you have control—the ability to make strategic moves, weather unexpected challenges, and confidently fund your firm's future.

Why Profit Doesn't Equal Cash

So, where does this disconnect originate? For professional services firms, it almost always begins with accounts receivable. That $100,000 invoice for a completed project looks good on your income statement, but it does nothing for your bank balance until that payment is collected.

Here’s a direct comparison. Imagine your firm just completed a major project.

Profit vs Cash Flow at a Glance

Metric | Profit (Accrual Basis) | Cash Flow (Cash Basis) |

|---|---|---|

Revenue Recognition | Records the $100,000 invoice as revenue immediately, boosting your "profit." | No revenue is recognized until the $100,000 is actually deposited in your bank account. |

Operational Impact | Shows the business is earning money and appears healthy on the P&L statement. | Reflects the reality that you don't yet have the cash to cover operating expenses like payroll. |

Timing | Focuses on when the revenue was earned. | Focuses on when the cash was received. |

This isn't an accounting nuance; it's a fundamental business reality. Several factors widen the gap between reported profit and usable cash:

- Accrual Accounting: As shown, booking revenue when services are rendered creates "paper profit" in your accounts receivable long before cash arrives.

- Non-Cash Expenses: Items like depreciation reduce taxable profit but don't involve a cash outlay in the period.

- AR Lag Time: The time it takes to collect on an invoice—your Days Sales Outstanding (DSO)—is the biggest driver of cash gaps. A high DSO means earned revenue is stuck in limbo.

- Financing and Debt: A loan increases cash reserves but isn't revenue. Interest payments, however, reduce both profit and cash.

The numbers confirm this. A recent Fitch Ratings' Global Corporates Cash Flow Monitor found that companies with a DSO under 45 days had 22% higher free cash flow margins than firms with DSOs over 60 days. This is a powerful testament to how disciplined cash collection matters.

For a finance leader, the income statement shows your firm’s potential. The cash flow statement shows its reality. One without the other provides an incomplete picture.

Navigating these dynamics is what effective cash management is all about. If you want to explore this topic further, our guide on cash flow management for small businesses offers more in-depth strategies.

Achieving positive cash flow means shifting your firm's focus from simply earning revenue to efficiently collecting it. This discipline transforms a profitable firm into a resilient one.

Diagnosing the Root Causes of Negative Cash Flow

When you have a negative cash flow problem, the first step is diagnosis, not a search for new solutions. Before you can fix the leaks, you must find them. For professional services firms, these issues are almost always buried in the quote-to-cash cycle.

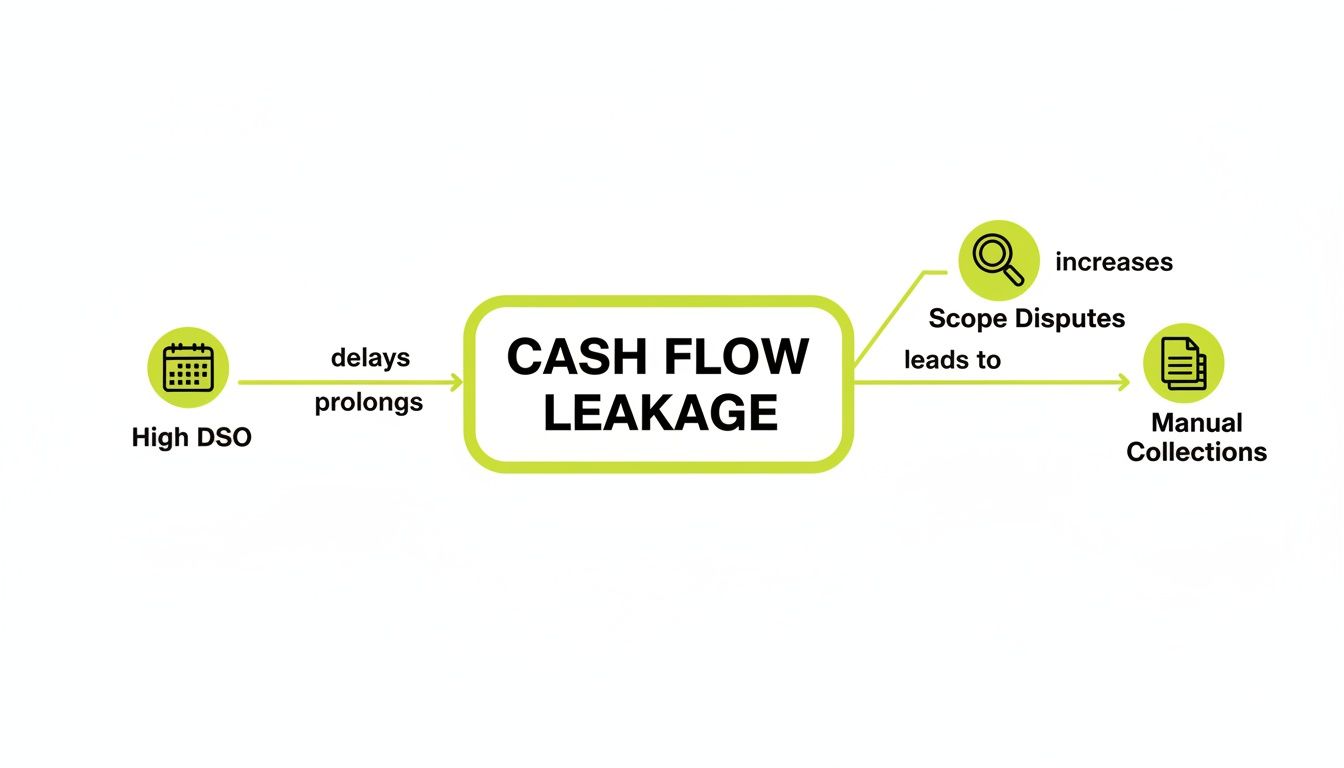

The most visible culprit is a high Days Sales Outstanding (DSO). Put simply, DSO is the average time it takes to get paid after invoicing. As that number climbs, your earned revenue sits in your clients’ bank accounts instead of yours. This directly erodes working capital and stifles operations.

The Anatomy of Cash Flow Leakage

A high DSO is rarely the whole story. Think of it as a fever—it confirms a problem but doesn't identify the cause. It's a symptom of deeper, connected issues within your accounts receivable process. Finance leaders who stop at the DSO number miss the real opportunity for improvement. You must dig into the why.

These are the most common drivers of cash leakage we see:

- Complex Billing Cycles: Milestone payments, retainers, and variable charges often create invoices that cause clients to pause, ask questions, and delay payment.

- Disputes Over Project Scope: Nothing stops a payment faster than a dispute. Unclear agreements or "scope creep" lead to invoice questions, freezing the payment process for weeks.

- Manual Collections Processes: Chasing payments with spreadsheets and calendar reminders is a recipe for inconsistency and human error. It's nearly impossible to follow up on time with every client when doing it by hand.

A firm’s ability to grow is directly tied to its operational efficiency. When finance teams spend their time chasing late payments and resolving disputes, they are diverted from strategic activities that drive real value.

Key Metrics to Monitor

To get a true handle on your cash flow health, look beyond just DSO. A few key performance indicators can act as your diagnostic toolkit, pinpointing where your AR process is failing and what’s standing between you and sustained positive cash flow.

(Visual Idea: Cinematic imagery of a single domino falling, triggering a chain reaction. This represents how a small collections issue can escalate into a major cash flow problem.)

Here are three critical metrics that will give you the clarity you need:

- Days Sales Outstanding (DSO): As covered, this is your headline number for collection speed. If it's consistently high or trending upward, that’s your first major red flag.

- Collection Effectiveness Index (CEI): This metric is more specific, measuring how effective your team is at collecting what’s owed in a given period. It shows the percentage of collectible dollars you actually collected.

- Aged AR Percentages: This is where the rubber meets the road. Break down your outstanding receivables by age (e.g., 1-30 days, 31-60 days, 61-90+ days). A high percentage in the 61+ day bucket signals a serious collections issue and a growing risk of bad debt.

The financial drain from these inefficiencies is significant. A global economic analysis found that businesses waste $200B annually on inefficient AR processes. The same report showed that firms using dynamic billing and automated risk tools can reduce DSO by 30% on average, resulting in a 15-20% boost in monthly cash flow. You can explore the full findings on disciplined cash management from Deloitte.

(Visual Idea: A chart visually demonstrating the growing problem of aging receivables over time, showing a clear trend of invoices moving into older buckets.)

By diagnosing these root causes with data, you can stop fighting fires and start building a resilient financial operation. This is the foundation needed before deploying tools like AI AR automation or QuickBooks AR automation for maximum impact.

Resolut automates AR for professional services—consistent, accurate, and human.

7 Practical Ways to Improve Your Cash Flow

To gain control over your firm's financial health, you must move from analysis to action. Achieving and maintaining positive cash flow isn’t about working harder; it’s about implementing disciplined systems that deliver predictable results. As a finance leader, that means focusing on measurable actions that directly improve working capital.

These are not quick fixes. They are fundamental changes to how you manage the quote-to-cash cycle. Understanding the practical strategies to improve cash flow is a good starting point for building system-driven improvements.

1. Establish Disciplined Credit and Billing Policies

The most effective way to improve collections is to prevent payment problems before they begin. This starts with a structured approach to how you onboard and bill clients—not just a handshake and a hopeful invoice.

First, implement a clear credit risk policy. Before signing a contract, run a basic risk assessment. This doesn't need to be a forensic investigation; a simple check can spot red flags. For larger projects, a more formal review is prudent and can prevent major write-offs.

Next, examine your billing structure. For many professional services firms, switching from a single end-of-project invoice to milestone-based billing can accelerate payments dramatically. This approach ties invoices directly to delivered value, making each payment request logical and easier for clients to approve.

We saw this with a $15M consulting firm that moved from net-60 terms to billing at project milestones. Within six months, their average DSO fell from 72 days to 48. That one policy change unlocked over $986,000 in working capital.

2. Deploy Structured Omnichannel Collections

If your collections process relies on manual emails, you are leaving money on the table. That approach is inefficient and easy for busy clients to ignore. A structured, omnichannel outreach program ensures reminders are consistent, professional, and visible where clients are most likely to see them. This is what modern AR software for professional services is built to do.

Think of it as creating smart, automated sequences that react to client behavior. For instance:

- Days 1-15 Past Due: A series of polite, automated email reminders are sent.

- Days 16-30 Past Due: The system adds an automated SMS notification with a direct link to a payment portal.

- Days 31-45 Past Due: A task is automatically generated for your finance team to place a personal phone call, armed with a full communication history.

This multi-channel strategy ensures persistence without manual chasing, turning your follow-up process into a system designed to improve cash flow.

The diagram below shows the main operational drags that a good automated system is designed to eliminate.

By automating outreach and standardizing billing, you directly attack high DSO and slash the administrative drain of manual collections.

3. Implement AI-Powered AR Automation for Precision

The next level of control comes from AI AR automation. While standard automation follows set rules, AI-driven systems learn from your data to make those rules smarter. These platforms analyze payment histories to pinpoint which clients are likely to pay late—often before an invoice is past due.

This allows for proactive intervention. For example, an AI system can flag an invoice for a client who consistently pays 30 days late and automatically adjust the communication strategy for them. Instead of a generic reminder, it might trigger an earlier, more personalized message. You can find more tactical ways to increase cash flow in our other articles.

Platforms offering QuickBooks AR automation can integrate directly with your existing accounting software, pulling invoice data and applying this intelligence without requiring a change in your core bookkeeping. This shifts accounts receivable from a reactive chore into a proactive, data-driven system built to reduce DSO and stabilize your cash position.

Resolut automates AR for professional services—consistent, accurate, and human.

Implementing AR Automation for Lasting Control

The strategies discussed are powerful, but making them stick requires a system. This is where technology becomes the backbone of your financial operations. For a professional services firm, AR automation isn't about replacing your team; it's about providing a smarter way to work, ensuring consistency and visibility.

Think of accounts receivable automation as a control layer that puts best practices into motion. It translates your collections strategy into predefined, intelligent workflows for every invoice. This systematic approach strips away the inconsistencies and human errors of manual processes, creating a predictable path to positive cash flow.

Operationalizing Your Collections Strategy

An advanced AR platform translates policy into automated action. It’s the difference between having a playbook and having a team that executes every play flawlessly. The technology allows your finance team to stop chasing paper and start managing by exception.

This operational shift is significant. Instead of your team spending 80% of its time on low-value, repetitive follow-ups, they can invest that energy into the 20% of activities that matter—resolving complex disputes, negotiating payment plans, and strengthening client relationships. This is how you reduce DSO while protecting the client experience.

Here’s what that looks like in practice:

- Automated Omnichannel Outreach: The system executes your communication strategy automatically across email, SMS, and prioritized call lists. It guarantees persistent, professional follow-up without manual effort.

- Intelligent Prioritization: Smart algorithms analyze payment histories to flag at-risk accounts before they become seriously late. This directs your team’s attention where it is needed most.

- Frictionless Payment Portals: A simple, consumer-style online portal for clients to view invoices and pay by card, ACH, or digital wallet removes common barriers to on-time payment.

From Reactive Chasing to Proactive Management

Perhaps the biggest win with AR automation is the shift from a reactive to a proactive collections mindset. Traditional AR is a constant fire drill—reacting to invoices as they creep past 30, 60, and 90 days. An intelligent system changes the game.

By analyzing payment patterns, the platform can predict which invoices are likely to be paid late. For example, if a client consistently pays 15 days after the due date, the system learns this and automatically adjusts its communication cadence for that account, perhaps starting follow-up earlier.

A system that identifies risk proactively is a force multiplier for a finance team. It provides the foresight needed to prevent small payment delays from escalating into significant bad debt write-offs, directly protecting the bottom line.

This proactive stance builds financial resilience. As a recent McKinsey analysis points out, strong operational infrastructure is key to generating resilient cash flows. The report found that B2B businesses with optimized collections see 25% faster payments. That cash funds growth and buffers against downturns, where poor cash management has historically made recessions 40% worse for businesses. You can discover more insights on the importance of resilient infrastructure from McKinsey.

Unifying Systems for Unmatched Visibility

For any CFO or Controller, disconnected data is a major operational risk. When AR data is in one place, CRM data in another, and your accounting software in a third, you lack a single source of truth. A platform built for QuickBooks AR automation, for example, should integrate seamlessly to provide a unified view.

This unification connects the finance department with sales and account management. Imagine a salesperson seeing a client's real-time payment status right before an upsell call. That visibility helps create a cash-aware culture across the organization. Our guide on accounts receivable automation software breaks down how these integrations work.

Ultimately, this unified command center gives leadership a clear, live look into critical cash flow metrics. You can monitor DSO, CEI, and AR aging in real time, filtering by client, project, or service line. This clarity empowers sharp, strategic decisions based on current data—not last month’s reports.

By implementing a dedicated AR automation platform, you are not just buying software. You are installing a permanent system of control that will anchor your firm’s financial stability.

Measuring the ROI of Improved Cash Flow

To a CFO, an initiative without a clear, measurable return is an expense, not an investment. Shifting to a disciplined, automated AR process is a direct investment in your firm's financial strength.

Calculating the ROI of achieving positive cash flow means focusing on the tangible value unlocked from your balance sheet. These are the numbers that get the attention of leadership and investors.

Quantifying the Impact on Working Capital

The most immediate return comes from reducing your Days Sales Outstanding (DSO). Every day cut from your DSO translates directly into cash in the bank. This is real working capital that was previously tied up in unpaid invoices.

Here’s the simple calculation:

(Annual Revenue / 365 Days) * Number of Days DSO is Reduced = Working Capital Freed Up

Let’s take a $10M professional services firm with a current DSO of 60 days. By implementing accounts receivable automation and tightening their collections process, they aim to lower DSO to 45 days—a 15-day improvement.

- Daily Revenue: $10,000,000 / 365 = $27,397

- Working Capital Unlocked: $27,397 * 15 days = $410,955

The firm now has $410,955 in cash that is no longer locked away. This capital can fund a strategic hire or be invested in technology, all without taking on new debt. To monitor these improvements, a good cash flow calculator can be a valuable tool.

A lower DSO isn’t just about getting paid faster. It’s about turning a static asset—your receivables—into dynamic capital that can actively fuel growth and make your firm more resilient.

To put this into perspective, here's how reducing DSO can impact cash flow for professional services firms of different sizes.

Projected ROI from AR Automation

Annual Revenue | Current DSO (Days) | Target DSO (Days) | Annual Cash Flow Improvement |

|---|---|---|---|

$5 Million | 75 | 60 | $205,479 |

$10 Million | 60 | 45 | $410,959 |

$25 Million | 55 | 40 | $1,027,397 |

$50 Million | 45 | 35 | $1,369,863 |

As you can see, the impact is substantial. The cash unlocked by even a modest DSO reduction provides a significant, immediate boost to a firm's financial flexibility.

Calculating Broader Financial Returns

The benefits extend beyond working capital. A smarter AR process creates a ripple effect of financial gains that build a more profitable and stable operation.

Here are other key areas where you’ll see a return:

- Reduced Bad Debt: A structured follow-up process, powered by AR software for professional services, means fewer invoices age out and become uncollectible. For a $10M firm, cutting write-offs from 1.5% to 0.5% adds $100,000 to the bottom line.

- Lower Labor Costs: AI AR automation takes over repetitive work. If automation frees up just 50% of one employee's time, you've recaptured thousands in annual salary that can be redirected to high-value financial analysis. This is a game-changer for lean teams, especially those using QuickBooks AR automation.

When you add the unlocked working capital, the drop in bad debt, and the operational savings, the business case for investing in your cash flow engine is undeniable.

Resolut automates AR for professional services—consistent, accurate, and human.

Sustaining Positive Cash Flow for Long-Term Resilience

Achieving positive cash flow is a critical milestone. Sustaining it is the mark of a strategically resilient business. This requires building a "cash-aware" culture that extends beyond the finance department. The goal is to move from reacting to cash flow problems to proactively controlling your financial destiny, turning the CFO into a key strategic operator.

This final stage is about using the data and systems you've put in place. An accounts receivable automation platform is a source of business intelligence. When shared, it empowers other departments to directly improve the firm's financial health.

(Visual Idea: Cinematic imagery of an air traffic controller in a calm, dark room, monitoring screens with flight paths. This symbolizes the clarity and control a CFO gains over accounts receivable.)

Fostering a Cash-Aware Culture

Financial strength is a team effort. When you give your sales and account management teams a clear view of a client's payment habits, they can have smarter, more productive conversations.

An account manager preparing for a renewal meeting can see if that client consistently pays late. This insight allows them to discuss payment terms as part of the strategic picture, rather than leaving it for finance to clean up later.

When your entire client-facing team understands the direct link between prompt payments and the firm’s ability to invest in delivering excellent service, collections cease to be just a finance problem. It becomes a shared responsibility.

This unified approach, backed by platforms like QuickBooks AR automation, gets everyone working with the same real-time data. It aligns the entire organization to improve cash flow.

Advanced Tactics for Long-Term Stability

With a solid automated system running, you can deploy more advanced strategies. This is where AI AR automation excels, moving beyond task automation to intelligent risk detection. The system can flag accounts showing early warning signs of payment trouble, letting you intervene before an invoice becomes a serious problem. That foresight is invaluable for maintaining a healthy cash position.

Ultimately, mastering positive cash flow elevates the finance function. It transforms the CFO and Controller from scorekeepers to strategic operators who directly shape the company's capacity for growth. By implementing a system to automate and analyze accounts receivable, you are building the foundation for lasting financial control.

Resolut automates AR for professional services—consistent, accurate, and human.

Common Questions About Positive Cash Flow and AR Automation

Making a change to a process as fundamental as accounts receivable naturally brings up questions. Here are straightforward answers to common concerns about using AR automation to boost positive cash flow.

How Quickly Can We See Results?

Results are visible quickly. While the exact timeline depends on your current DSO and client base, most firms see a measurable lift in cash flow within the first 60-90 days.

The first wins come from automating reminders and offering an easy online payment portal. This alone accelerates collection of current invoices. More significant gains, like a 20-30% drop in DSO, typically appear within the first two quarters as the system learns client payment behaviors.

Will Automation Harm Client Relationships?

This is a fair question. The goal of modern AI AR automation isn't to sound robotic—it’s to be more precise and professional. Think of it as a precision tool, not a blunt instrument.

You can customize the message tone, timing, and communication channel to match your firm's voice. By letting the system handle routine follow-ups with perfect consistency, your team is free to manage exceptions and have more strategic client conversations. This often strengthens relationships, it doesn't strain them.

Can We Use This if We Rely on QuickBooks?

Absolutely. QuickBooks is an excellent accounting tool, but it was not built as a dedicated collections engine. As a professional services firm grows, managing AR effectively requires more specialized workflows.

Think of a dedicated platform for QuickBooks AR automation as an intelligent command center that sits on top of your accounting system. It syncs with QuickBooks, pulls the necessary invoice data, and then executes a sophisticated collections playbook.

This approach lets you dramatically improve cash flow and reduce DSO without the disruption of replacing your core accounting software. You gain a powerful system for managing receivables while keeping your trusted system of record.

***

Resolut automates AR for professional services—consistent, accurate, and human.