What does 2 10 n 30 mean: A Guide for Financial Operators

Find out what does 2 10 n 30 mean for your business finances and cash flow. This concise guide explains its impact and how to apply it to improve liquidity.

The term "2/10, n/30" on an invoice is not accounting jargon. It is a lever for managing cash flow.

In practice, 2/10, n/30 offers clients a 2% discount for payment within 10 days. Otherwise, the full invoice amount is due in 30 days.

This is a direct tool for controlling working capital.

Decoding 2/10, Net 30 as a Financial Tool

For finance leaders at professional services firms, this term is a mechanism to accelerate cash receipts and tighten the revenue cycle. It is a calculated trade-off, not a giveaway.

By offering an early payment discount, you incentivize clients to prioritize your invoice. This has a direct, measurable impact on your firm’s liquidity.

Core Components and Operational Impact

A precise breakdown of "2/10, n/30" reveals its function:

- 2%: The discount offered for prompt payment.

- 10 days: The window from the invoice date to qualify for the discount.

- n/30 (Net 30): The final due date for the full invoice balance.

This is a direct strategy to reduce DSO (Days Sales Outstanding)—a critical metric for financial health. A lower DSO means cash returns to the business faster, reducing reliance on credit lines to cover payroll and operating expenses.

Summary of the Financial Trade-Off

The decision framework is clear.

2/10, Net 30 Terms at a Glance

Term Component | Meaning for Client | Impact for Your Firm |

|---|---|---|

2% Discount | A 2% reduction on the invoice total for early payment. | A calculated reduction in gross margin for a specific invoice. |

10-Day Window | A firm deadline to capture the discount. | An opportunity to receive cash up to 20 days sooner. |

Net 30 Due Date | Final payment deadline for the full, non-discounted amount. | The baseline expectation if the discount is not utilized. |

The table quantifies the exchange: a small margin concession for significantly accelerated cash flow.

Effective execution requires precision. Manually tracking discount eligibility across hundreds of invoices invites error. This is where accounts receivable automation provides operational control, enforcing the rules systematically to capitalize on every opportunity.

The Bottom-Line Impact on Working Capital

These payment terms have a direct and material impact on your firm's cash position. Let's analyze the numbers.

Consider a $25,000 invoice with 2/10, net 30 terms. If the client pays within 10 days, they remit $24,500—a $500 discount. Your firm receives payment a full 20 days ahead of the standard cycle. This is a direct injection of liquidity into your operations.

Accounting for the Discount

Properly recording these transactions is essential for accurate financial reporting. Using the gross method, the journal entries are straightforward.

Scenario 1: Client Utilizes the Discount Payment is received on day 8. The entry is:

- Debit Cash: $24,500

- Debit Sales Discounts: $500

- Credit Accounts Receivable: $25,000

The "Sales Discounts" account tracks the total cost of your early payment incentive program, enabling clear analysis of its ROI.

Scenario 2: Client Pays the Full Amount Payment arrives on day 25. The entry is:

- Debit Cash: $25,000

- Credit Accounts Receivable: $25,000

This is a fundamental component of effective revenue cycle management, ensuring the entire financial process from contract to cash is optimized.

The Underlying Financial Incentive

From the client's perspective, a 2% discount for paying 20 days early represents an annualized return of over 36%. This is a highly compelling, low-risk return on their cash, motivating them to place your invoice at the top of their payment queue.

This high effective interest rate is the core mechanic of 2/10, net 30. You are paying a premium for predictable, accelerated cash flow. For your firm, this liquidity means less reliance on credit and more capital available for strategic deployment.

Should Your Firm Offer an Early Payment Discount?

The decision to offer 2/10, net 30 terms is a strategic one, centered on accelerating cash flow. Faster payments directly reduce DSO and decrease dependence on costly lines of credit to manage operational cash gaps.

Predictable cash inflows strengthen financial forecasting. This enables more confident decisions regarding hiring, capital investment, and expansion. The result is a stronger balance sheet and greater control over your firm's financial trajectory.

* *

Balancing Margin Against Liquidity

The primary cost is the 2% discount, which reduces your gross margin on that specific transaction. This cost must be weighed against the value of improved liquidity.

For firms with tight margins, the 2% may be prohibitive. For many others, it is a nominal cost for significant financial stability and predictability. This trade-off is why 2/10, net 30 has been a B2B standard for decades—it provides a powerful, mutual incentive.

The Real-World Cost Analysis

Compare the discount to your current cost of capital. If you use a revolving line of credit at an 8% APR to cover payroll while awaiting receivables, the cost of that capital for 20 days is often greater than the 2% discount.

Offering a discount is frequently cheaper than financing your receivables. It transforms AR from a passive asset into an active financial instrument, providing immediate liquidity. This is where a clear policy, enforced by AI AR automation, becomes critical. An automated system ensures consistent application, removing manual tracking and errors. More on this is available in our analysis of what is receivables financing.

Executing Your Payment Term Strategy

A payment term strategy is only effective if executed consistently. Manual tracking of discount eligibility across numerous invoices is inefficient and prone to error.

The most reliable method for applying terms like 2/10, n/30 is through accounts receivable automation.

AR software automates the administrative process. It tracks the 10-day window for each invoice, sends timed reminders, and flags accounts that miss the cutoff. This ensures your policies are enforced systematically, without exception.

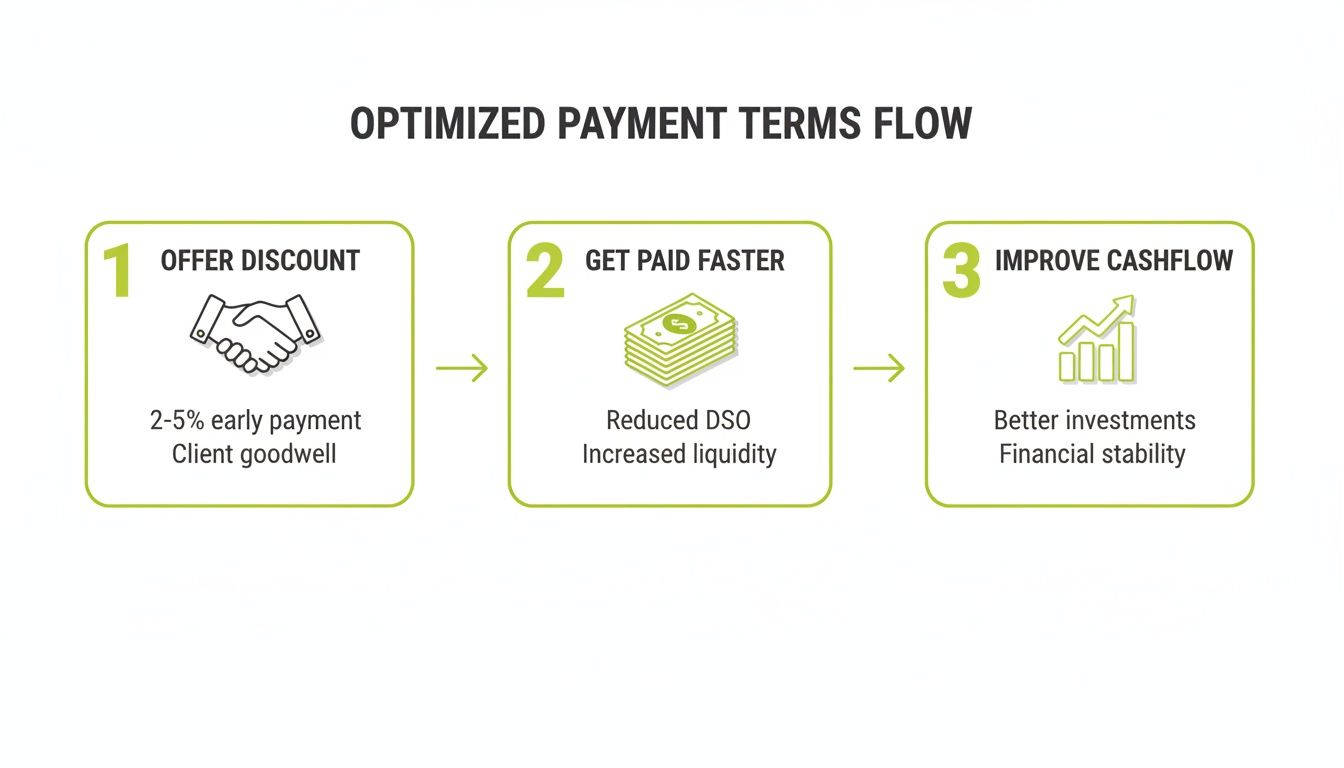

The operational flow is direct: a structured incentive leads to faster payment, which improves cash flow.

Enforcing Terms with Precision and Control

Late payments are a systemic issue in B2B transactions. Data shows that 40% of B2B invoices are paid late, creating a significant drag on productivity and cash flow.

AI AR automation provides a solution. By sending personalized, automated reminders, it can accelerate payments by up to 35%. The objective is to shift from reactive collections to a proactive payment culture. Automation ensures every client receives the right communication at the right time, maximizing early payments while minimizing manual follow-up.

This level of process control can be embedded early. For firms seeking end-to-end financial discipline, AI-driven contract solutions can enforce these payment terms from the initial agreement.

An automated system is the operational backbone that ensures the intended financial benefits of terms like 2/10, net 30 are fully realized. Our guide explains **how to automate accounts receivable** for maximum impact.

Adapting Credit Strategy by Client Segment

A one-size-fits-all credit policy is suboptimal. Payment terms like 2/10, net 30 should be deployed dynamically based on client data and strategic goals.

Not all clients warrant the same terms. A long-standing client with a history of slow but reliable payments might be a candidate for a more aggressive 3/10, net 30 offer to accelerate their payments.

Conversely, a new client with no payment history should likely start with firm net 30 terms. Offering a discount is an unnecessary risk until they have established a track record of timely payments. This protects your firm from potential bad debt.

Data-Driven Client Segmentation

Effective credit strategy relies on data-driven segmentation. With AR software for professional services, you can group clients by key financial metrics:

- Payment History: Identify clients who pay early, on time, or chronically late.

- Contract Value: Differentiate between high-value strategic accounts and smaller clients.

- Credit Risk: Assign risk scores to flag clients who may require shorter terms or deposits.

This is not about collections; it is about strategic financial management. Segmenting clients allows you to create credit policies that balance risk with relationship value. This is how AR evolves from a balance sheet item into a strategic asset. Platforms with QuickBooks AR automation can streamline this entire process.

This level of control moves the conversation beyond simply knowing what 2 10 n 30 means. It is about using those terms to actively manage your firm's financial health.

Making Payment Terms a Strategic Advantage

Ultimately, 2/10, net 30 is a tool to manage working capital and strengthen your firm’s financial position. A well-executed payment term strategy creates a direct link between invoicing policy and improved cash flow.

However, consistent execution is the primary challenge. For firms serious about leveraging payment terms, AI AR automation is the most practical path to achieving control and measurable results.

The right AR software for professional services significantly reduces DSO by enforcing your payment terms systematically. For example, systems providing QuickBooks AR automation can monitor discount windows, dispatch reminders, and flag exceptions without manual intervention.

This transforms a simple payment term from a suggestion into a reliable financial instrument that works to your firm's advantage.

Common Questions from Financial Leaders

Is the 2% Margin Concession Justified?

For most professional services firms, yes. The analysis is a direct comparison: is the 2% margin reduction greater than the cost of carrying that receivable for an additional 20 days?

If you rely on a credit line to manage cash flow, the interest expense over 20 days often exceeds the 2% discount. Furthermore, accelerated cash receipts provide capital that can be immediately reinvested into the business—for hiring, marketing, or technology. The 2% is an investment in liquidity and financial agility, a direct way to improve cash flow.

***

***

How Should These Terms Be Communicated to Clients?

Clarity and consistency are essential. Ensure "2/10, net 30" is clearly stated on all invoices and defined within your master service agreements.

The client onboarding process is the ideal time to frame this term as a benefit—a straightforward way for them to reduce costs. This communication is supported by accounts receivable automation, which can send polite reminders as the 10-day discount window nears its end. This is perceived as a helpful service, not a collection effort.

What Is the Protocol if a Client Takes an Unearned Discount?

This requires a firm and consistent policy. If a client pays on day 15 but takes the 2% discount, your AR team must act. The standard protocol is to issue a debit memo or a new invoice for the short-paid amount.

Allowing exceptions undermines the incentive structure and sets a poor precedent. Modern AR software for professional services automates the detection of these discrepancies, enabling your team to address them immediately before they become a recurring issue.

--- Resolut automates AR for professional services—consistent, accurate, and human.