Cash Flow Forecasting for Professional Services: A Guide to Financial Control

Discover what is cash flow forecasting and how to build an accurate model. Learn practical steps to improve financial planning and control for your business.

For a professional services firm, cash flow forecasting is not an accounting exercise. It is your operational early warning system.

A forecast predicts the movement of cash in and out of your business over a specific period—typically a rolling 13-week window. This is not a theoretical report. It is the core tool for managing your firm's liquidity and stability.

This guide details how to build a forecast that delivers clarity and control, enabling you to make operational decisions based on data, not assumptions.

From Hindsight to Foresight

In a services business, high revenue does not guarantee cash. The gap between sending an invoice and receiving payment creates uncertainty.

This gap can stall hiring, delay investments, or put payroll at risk. An accurate cash flow forecast closes this gap.

It transforms historical financial data into a forward-looking operational tool. You shift from reacting to financial surprises to anticipating them. This builds a rhythm of visibility that supports confident, strategic decisions.

Predictability is the Objective

The primary value of a forecast is predictability. Accurate visibility into your cash position weeks or months out provides a significant operational advantage.

A reliable forecast directly informs critical decisions:

- Hiring and Expansion: Know precisely when you have the cash reserves to add talent or launch a new service line. A firm with a $5M run rate can use its forecast to confirm it can support three new senior hires, modeling the $45,0-00 monthly payroll increase against projected inflows.

- Capital Expenditures: Plan for major investments, such as a new CRM system or office lease, without jeopardizing working capital.

- Debt Management: Proactively manage cash cycles to avoid unnecessary reliance on your line of credit, saving on interest costs.

- Accounts Receivable Strategy: Identify clients with slow payment patterns, allowing you to tailor your collections approach and **improve cash flow**.

To understand the mechanics, here is a breakdown of its core components.

Core Components of a Cash Flow Forecast

Component | Description | Example for a Professional Services Firm |

|---|---|---|

Beginning Cash Balance | The amount of cash you have at the start of the period. | The firm starts the month with $150,000 in its checking account. |

Cash Inflows | All sources of cash coming into the business. | Invoiced client payments, retainer fees, project deposits. |

Cash Outflows | All payments going out of the business. | Payroll, rent, software subscriptions, contractor fees, taxes. |

Net Cash Flow | The difference between cash inflows and outflows for the period. | $100,000 in client payments minus $80,000 in expenses = $20,000 net cash flow. |

Ending Cash Balance | Your beginning balance plus your net cash flow for the period. | $150,000 (Beginning) + $20,000 (Net) = $170,000 ending balance. |

This simple structure is the engine of your forecast, providing a clear snapshot of your financial health over time.

The Heart of the Matter: Managing Cash Flow

At its core, cash flow management and forecasting translates your accounts receivable and payables into a clear timeline.

For services firms, the largest variable is the timing of client payments. Modern tools like accounts receivable automation have a significant impact here.

By using data to predict payment timing and systemizing follow-ups, automation turns the most unpredictable part of your forecast into a more reliable data point, helping to reduce DSO.

Choosing Your Forecasting Method

Selecting the right forecasting method is about gaining the right visibility for specific decisions without creating unnecessary work.

For professional services firms, the choice between the direct and indirect method depends on the question you need to answer: Are you managing weekly bank balances or developing a three-year growth plan?

The Direct Method for Tactical Control

The direct method is the foundation of operational cash management. It tracks every expected cash transaction—client payments, payroll, rent, software subscriptions—logged by the date the cash is expected to move.

It is intentionally granular and ignores non-cash items like depreciation. Its sole purpose is to project your actual cash balance.

For a professional services firm, the direct method is non-negotiable. It provides the ground-level truth needed to manage working capital and cover payroll without unnecessarily tapping your line of credit.

This approach yields your most powerful operational tool: the 13-week cash flow forecast. It is a rolling, forward-looking view of your liquidity for the next quarter.

The Indirect Method for Strategic Planning

The indirect method starts with your P&L's net income and adjusts for non-cash items and changes in working capital.

This is not for managing daily bank balances. It is for connecting cash flow to overall financial health and is used for the formal Statement of Cash Flows.

It helps answer strategic questions:

- Is our profitability converting to cash?

- How efficiently are we collecting receivables?

- Can projected earnings fund our growth plans?

While crucial for annual planning and investor discussions, the indirect method is ineffective for day-to-day cash decisions. A profitable quarter on paper can hide a cash crunch from rising receivables.

Comparison of Forecasting Methodologies

Effective finance leaders use both methods for different purposes. The direct method is for navigating the immediate road ahead; the indirect method is for checking the long-term map.

Methodology | Best For | Time Horizon | Key Benefit |

|---|---|---|---|

Direct Method | Operational liquidity management and weekly cash planning. | Short-term (1-13 weeks) | Provides granular, actionable visibility into your actual bank balance. |

Indirect Method | Strategic financial analysis and long-term planning. | Long-term (1-3 years) | Aligns cash flow with financial statements and profitability metrics. |

For leaders of professional services firms, the direct method is the weekly operational guide. The indirect method is the annual strategic check-in.

A disciplined forecasting process relies on the direct method. The accuracy of this forecast—especially cash inflows—separates firms that control their cash from those controlled by it.

This is where tools like QuickBooks AR automation or more advanced AR software for professional services become critical.

By systemizing collections with AI AR automation, you can reduce DSO and make cash inflows—the most volatile piece of any forecast—far more predictable.

Building a Forecast You Can Actually Trust

An accurate forecast is a disciplined reflection of business operations, built on clean data and consistent process.

Your cash flow is tied to project billing, milestone payments, and client payment habits. This variability is where most forecasts fail.

The Raw Materials of a Good Forecast

Building an accurate forecast requires focusing on the right data inputs.

The essentials include:

- AR Aging Report: Ground zero for forecasting inflows. It must be clean and current.

- Historical Payment Data: Reflects how and when specific clients actually pay.

- AP Schedule: A clear view of all upcoming vendor and contractor payments.

- Payroll & Tax Schedule: Your largest and least flexible outflows, mapped with precision.

- Sales Pipeline Data: Weighted by probability to forecast future project starts and deposits.

Common Errors That Kill Accuracy

A few common errors can render a forecast useless. The most dangerous is over-optimism, especially assuming clients will pay on time.

Ignoring a client's payment history is another major pitfall. If a client averages 47 days to pay a 30-day invoice, forecasting payment at 30 days builds a fundamental flaw into your model.

This error compounds, leading to unexpected cash shortfalls. A firm projecting a $50,000 payment in week 4 that arrives in week 6 creates a $50,000 variance that can disrupt operations.

From Messy Data to Real Control

Building a high-fidelity forecast begins with data discipline. The goal is to replace broad assumptions with specific, evidence-based inputs.

Start with your AR aging report. Analyze it by client, not just by age. Segment clients by payment behavior to apply more realistic collection timelines, which will dramatically improve cash inflow projections.

For firms using spreadsheets, you can integrate Excel AI into your workflow to sharpen analysis.

This is where accounts receivable automation provides an advantage. An AI AR automation platform analyzes payment histories at the client level to build a predictive model of your cash inflows. This systematic approach helps reduce DSO and provides a much more reliable data feed for your forecast.

A reliable forecast is about control. It provides the financial narrative needed to make decisions with confidence.

Your Step-by-Step Forecasting Playbook

A forecast's value is in the discipline behind it. A consistent, operator-focused rhythm is more important than complex software.

For a professional services firm, that rhythm is built on the reality of your accounts receivable. The goal is reliable visibility, not perfect prediction.

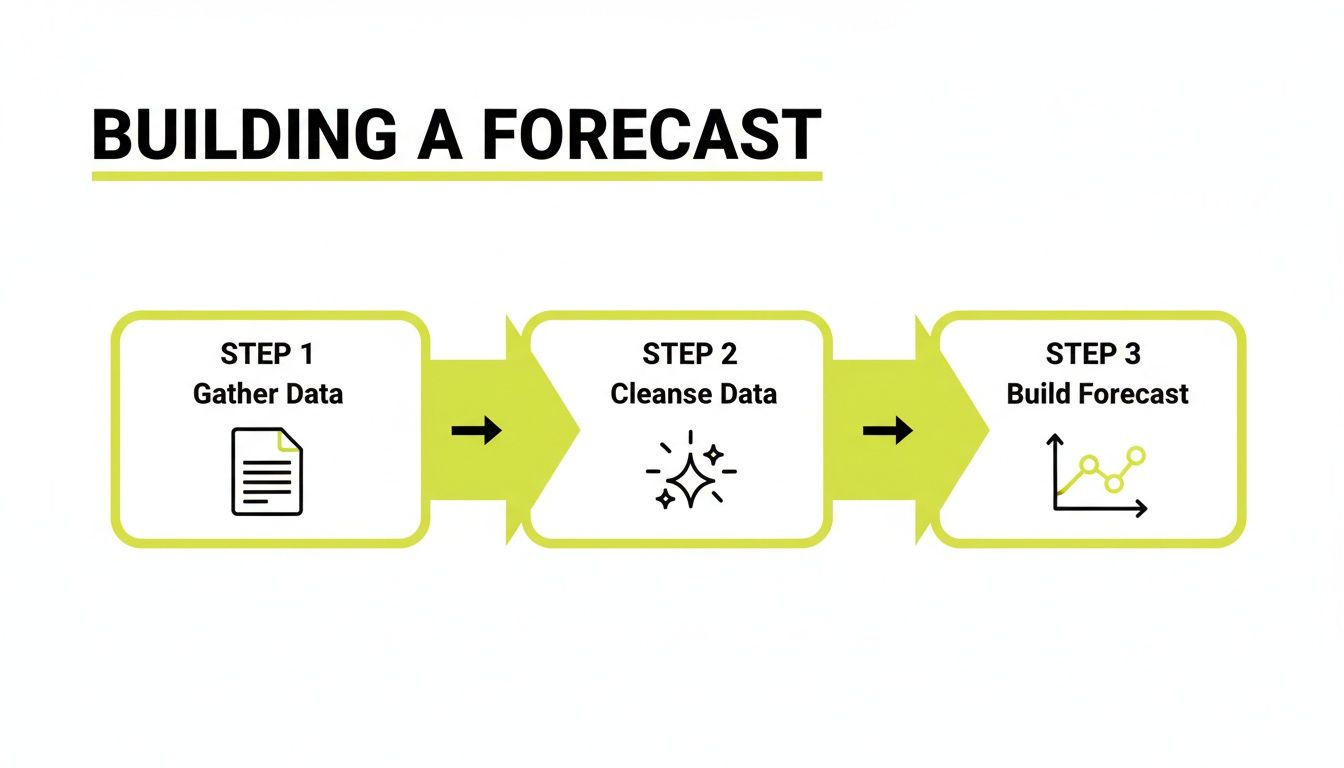

The process is straightforward: gather raw data, ensure its accuracy, and then build the forecast.

Step 1: Gather Your Historical AR Data

The starting point is what your clients have actually done.

Pull at least 6–12 months of detailed AR history from your accounting system, like QuickBooks. For each invoice, identify the gap between the invoice date and the payment date. This is the raw data for understanding true client payment behavior.

Step 2: Segment Clients by Payment Behavior

Not all clients pay the same way. Lumping them into a single DSO calculation obscures reality.

Sort clients into simple, clear categories:

- Prompt Payers: Consistently pay on or before the due date.

- Consistent Late Payers: Reliably pay, but consistently 15-20 days past due.

- Erratic Payers: Have no discernible payment pattern and require a more conservative forecast.

This segmentation moves you from a generic, firm-wide DSO to a client-specific payment timeline. This adjustment will dramatically improve cash flow forecast accuracy.

Step 3: Build Your Cash Inflow Model

With client segments defined, build a realistic cash inflow model for the next 13 weeks.

Apply the appropriate payment delay from your AR aging report to each invoice based on its client segment. A "Prompt Payer" invoice due in week 2 is forecasted for week 2. A "Consistent Late Payer" invoice due in week 2 is forecasted for week 4 or 5.

This bottom-up approach produces a forecast grounded in reality.

Step 4: Layer in Your Cash Outflows

Forecasting outflows is more straightforward, as most are fixed or predictable.

Compile a complete list of all expected payments for the next 13 weeks:

- Payroll and Tax Payments

- Rent and Utilities

- Software Subscriptions

- Vendor and Contractor Invoices

- Debt Service

Plot these on your 13-week calendar. This provides a clear picture of your cash commitments to measure against your realistic inflow projections.

The discipline of this weekly process forces a review of who owes you money, who is likely to pay, and what your commitments are. This rhythm builds financial control.

Step 5: Establish a Weekly Review Cadence

A forecast is a living document. The final step is a non-negotiable weekly meeting to review and update the 13-week rolling forecast.

In this review, compare the prior week's forecast to actual cash movements. This comparison helps you fine-tune assumptions about client behavior. This cycle of forecasting, measuring, and refining creates true financial clarity.

How AR Automation Enhances Forecast Accuracy

A cash flow forecast is only as reliable as its inputs.

For professional services firms, the most volatile variable is the timing of cash inflows. Manual forecasting relies on broad assumptions, like a firm-wide DSO, which often hide the reality of individual client payments.

AI AR automation improves the accuracy of this critical variable by replacing assumptions with granular, client-level data.

From Historical Averages to Predictive Insights

Traditional forecasting uses a historical average DSO, treating all clients identically.

AI AR automation analyzes the specific payment history of each client to predict when they are likely to pay a specific invoice. An AI model can predict with over 95% accuracy that Client A, despite 30-day terms, will pay in 42 days, while Client B will pay in 28.

This transforms a generic forecast into a dynamic, client-by-client prediction.

Actively Accelerating Cash Inflow

Effective automation does not just predict payments; it accelerates them.

A smart system orchestrates a tailored communication sequence for each client. This systematic, personalized outreach cannot be replicated manually at scale.

This proactive approach provides two direct benefits:

- Systematic DSO Reduction: By making it easier for clients to pay and reminding them at optimal times, automation consistently works to reduce DSO. A 10-day reduction in DSO for a $10M firm can free up over $270,000 in working capital.

- Behavioral Change: Consistent, professional follow-up trains clients to pay more promptly, creating a positive feedback loop that improves forecast reliability over time.

By improving underlying payment behavior, AR software for professional services makes your inflow data cleaner and projections more stable.

Providing a Single Source of Truth

Manual forecasting often involves pulling data from accounting software, spreadsheets, and collector notes.

A platform like QuickBooks AR automation or a dedicated system unifies collections data into a single dashboard.

This unified view provides immediate clarity:

- Real-Time Status: See where every invoice stands and its complete communication history.

- Team Performance: Track key metrics against collections goals.

- Risk Identification: AI can flag invoices at high risk of late payment, enabling proactive intervention.

When your AR process is centralized, the data feeding your forecast is cleaner and more trustworthy. The accounts receivable automation benefits are tangible, eliminating the guesswork that plagues traditional methods.

Turning Your Forecast into Financial Control

A reliable cash flow forecast is an active, strategic tool that provides control over your firm's financial future.

It is the difference between reacting to problems and anticipating them. Your forecast stops being a historical report and becomes the basis for critical decisions.

From Data to Decisions

A trustworthy forecast allows you to answer major questions with confidence.

- When can we hire? The forecast shows when recurring inflows can support another salary, turning a plan into a calculated action.

- Can we fund an investment? It models the real impact of a capital expense, so you can invest without constricting working capital.

- How do we handle a shortfall? A potential cash gap can be seen weeks in advance, allowing you to solve it by adjusting AR efforts instead of drawing on an expensive line of credit.

This foresight is the cornerstone of effective receivable management services and the mark of a financially disciplined firm.

A forecast transforms financial data from a historical record into a forward-looking command center. You stop being controlled by your cash flow and start controlling it.

Building and maintaining an accurate forecast provides the clarity required to lead with confidence. It puts you back in control of your firm's future.

Common Questions from Financial Operators

Here are direct answers to common questions about implementing a cash flow forecast.

How often should we update our forecast?

For operational decisions, a 13-week rolling forecast updated weekly is the standard. This provides sufficient runway to manage short-term liquidity without excessive administrative burden.

For strategic planning, your long-term (annual) forecast can be updated monthly or quarterly, aligned with your financial review cadence.

What is the biggest mistake firms make with this?

The most common and costly mistake is basing a forecast on assumptions instead of data. This means using contractual payment terms or sales projections as a proxy for actual cash receipts.

An accurate forecast is built on historical payment behavior and a realistic, data-driven DSO segmented by client. Assuming an invoice will be paid on its due date is a direct path to an unreliable forecast.

Can AR automation really make our forecast more accurate?

Yes, significantly. The largest variable in a professional services forecast is predicting when clients will pay. AI AR automation is designed to solve this problem.

Instead of a blended firm-wide DSO, AI platforms analyze payment data to predict, at the individual client level, when a specific invoice will be paid. You replace broad assumptions with precise, client-level intelligence.

Furthermore, by systemizing reminders and simplifying payments, effective AR software for professional services also works to reduce your DSO. Cash becomes more predictable and arrives faster. Systems from QuickBooks AR automation add-ons to more sophisticated platforms provide the clean, reliable data that makes forecasting a valuable operational tool.

--- Resolut automates AR for professional services—consistent, accurate, and human.