What Is Cash Forecasting? A Guide to Financial Control

Understand what is cash forecasting and why it's critical for professional services firms. Learn methods and KPIs to improve accuracy and stabilize cash flow.

Cash forecasting isn't an academic exercise. For a professional services firm, it's the flight control system.

It provides the visibility to navigate uncertainty, make calculated decisions, and avoid a sudden cash crunch.

Think of it as the central nervous system for your firm's financial health. It transforms historical data into a forward-looking tool for decisions on hiring, investment, and debt.

Without it, you're reacting. With it, you're in control.

This is about turning guesswork into predictable growth. It’s the answer to a core pressure every finance leader feels: how to scale the business without losing stability.

The Problem with Old Habits

The familiar spreadsheet is a liability for this task.

Static spreadsheets are prone to manual errors, create data silos, and cannot keep pace with a services business. This isn't a minor issue; it's a costly blind spot in corporate finance.

The data is clear. Only 28% of companies achieve cash forecast accuracy within a 10% variance. This points to a fundamental weakness in how businesses manage liquidity, forcing them to operate by looking in the rearview mirror.

This gap turns manageable operational hurdles into significant financial risks.

From Looking Back to Planning Ahead

Effective forecasting requires a shift from reactive reporting to proactive strategy.

A precise forecast gives you the power to:

- Anticipate Cash Shortfalls: Identify potential liquidity gaps weeks or months out. This provides time to arrange financing or adjust spending without last-minute pressure.

- Optimize Capital Allocation: Make confident decisions on key hires, technology investments, or partner distributions based on projected cash positions.

- Improve Stakeholder Confidence: Provide lenders, investors, and board members with a clear, data-driven view of the firm’s stability. Predictability builds trust.

For a deeper dive, this guide on mastering cash flow projection is a valuable resource.

Predictability starts with your receivables. The most effective way to increase cash flow is to know exactly when client payments will arrive.

The Two Horizons of Cash Forecasting

Effective cash forecasting operates on two horizons simultaneously.

Finance leaders need a ground-level view for daily operations and a high-level view to steer the firm's long-term direction.

These two perspectives—tactical and strategic—are distinct but interdependent. They work together to ensure stability today and readiness for tomorrow.

Short-Term Tactical Forecasting

The short-term forecast is your 13-week rolling cash plan. Its purpose is singular: manage liquidity.

This is the first line of defense against surprises, ensuring you can cover payroll, supplier invoices, and tax obligations without friction.

The inputs are not assumptions; they are hard data pulled from operational systems.

Key components include:

- Accounts Receivable Aging: A precise schedule of outstanding invoices and expected payment dates. This is where reliable accounts receivable automation delivers immediate clarity.

- Accounts Payable Schedules: A clear view of payment obligations and due dates.

- Payroll Projections: Fixed labor costs that must be met.

- Operating Expenses: Predictable overhead like rent and software.

This forecast answers one critical question: "Do we have sufficient cash to operate smoothly for the next quarter?" It is the bedrock of financial control.

Long-Term Strategic Forecasting

The long-term forecast extends 12 months or more. This is your strategic roadmap.

It moves beyond daily cash management to inform the high-stakes decisions that define the firm’s future.

This is the forecast used to model scenarios for:

- Major Capital Investments: Deciding when to fund new technology or office expansion.

- Securing Financing: Providing lenders a credible, data-backed narrative for growth and repayment.

- Mergers and Acquisitions: Modeling the financial impact of a transaction.

- Strategic Hiring: Planning for key leadership or team expansions required for the next growth phase.

Inputs are broader and more assumption-driven, incorporating sales pipelines, annual revenue targets, and economic trends. Accuracy here is directional, not transactional.

A well-executed long-term forecast is the financial narrative you present to your board, partners, and lenders. It demonstrates a clear, defensible vision of where the firm is headed.

The distinction between the two horizons is crucial.

Short-Term vs. Long-Term Cash Forecasting

Attribute | Short-Term Forecast (13-Week) | Long-Term Forecast (12+ Months) |

|---|---|---|

Primary Goal | Manage immediate liquidity and working capital. | Inform strategic decisions and capital planning. |

Timeframe | 1 to 13 weeks, on a rolling basis. | 12 to 60 months, updated quarterly or annually. |

Key Inputs | AR aging, AP schedules, payroll, known expenses. | Sales forecasts, revenue targets, market trends. |

Focus | Tactical and operational. | Strategic and financial planning. |

Main Use | Avoid cash shortfalls, manage debt covenants. | Plan for M&A, secure financing, capex. |

Accuracy | High. Based on confirmed transactions. | Directional. Based on assumptions and models. |

Understanding how to build and integrate both forecasts is what separates reactive finance teams from proactive ones. It turns financial data into a competitive advantage.

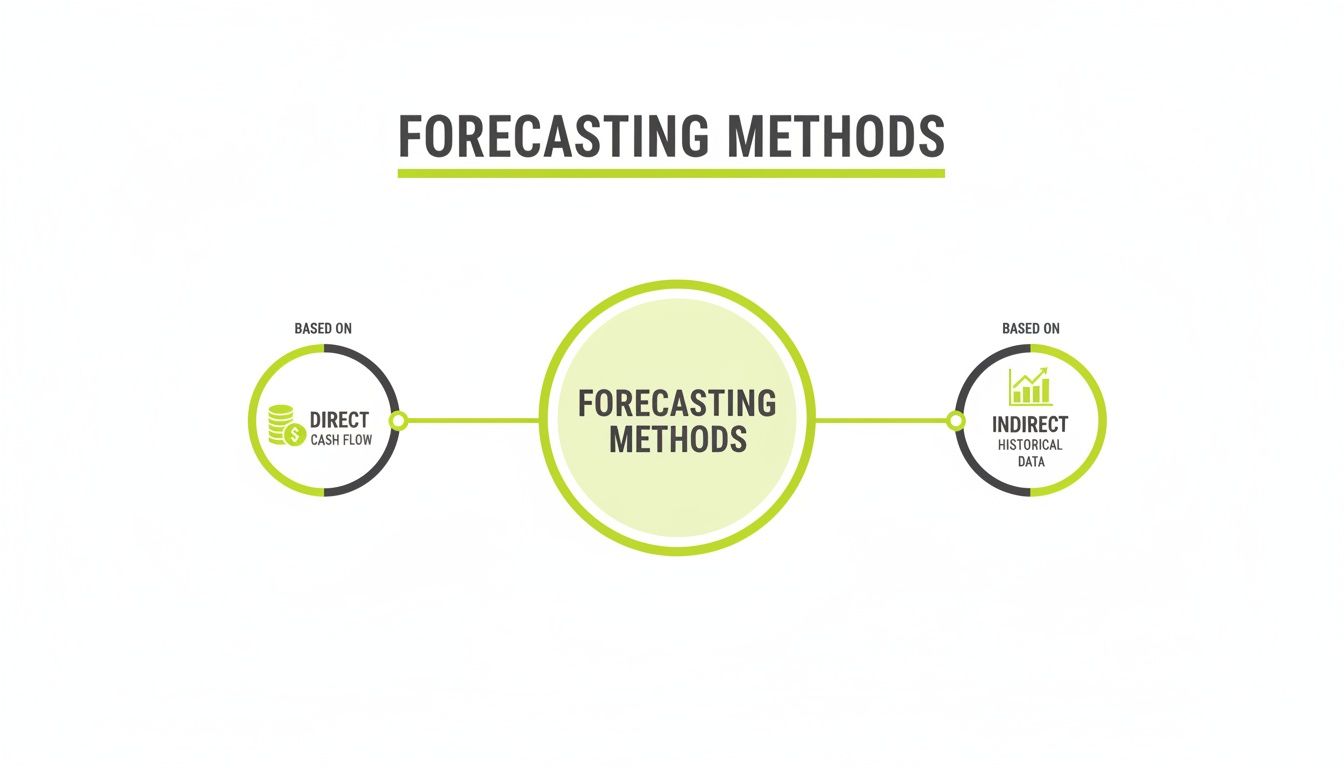

Understanding Direct and Indirect Forecasting Methods

Two primary methods exist for forecasting cash: direct and indirect.

They are designed for different purposes. The choice depends on whether you are managing next week’s payroll or planning next year’s capital budget.

For a professional services firm, one provides ground-level control over cash; the other offers a 30,000-foot view. Using the wrong tool for the job introduces unnecessary risk.

The Direct Method: Your Operational Toolkit

The direct method is designed for the day-to-day management of the business. It is a detailed register of all anticipated cash inflows and outflows.

This method ignores accrual accounting concepts like net income. It is exclusively concerned with cash moving in and out of your bank accounts.

Key inputs include:

- Cash Inflows: This is centered on accounts receivable—projected payments from existing invoices, expected retainers, and new work to be billed and collected within the forecast period.

- Cash Outflows: This includes all planned disbursements: payroll, vendor payments, contractor invoices, rent, taxes, and other fixed operating costs.

Because it is built on confirmed and near-certain transactions, the direct method is the only reliable way to manage working capital. It answers the critical question: "Will we have enough cash to make payroll?"

For firm owners and controllers, the direct method is a primary control mechanism. It provides the visibility to manage collections and time vendor payments, directly impacting stability.

The Indirect Method: A Strategic Compass

The indirect method is built for long-range planning and financial statement reconciliation.

It starts with net income from the P&L and then adjusts for non-cash items—such as depreciation and amortization—to arrive at a projected cash position.

The purpose is to bridge the gap between accrual-based profit and actual cash.

While essential for ensuring strategic plans align with financial statements, this high-level approach is ineffective for managing daily liquidity.

Even with sound methods, accuracy remains a challenge. Forecasting is shifting from static spreadsheets to AI-driven tools, yet messy data and disparate systems persist. You can read more about these cash management trends on Nomentia.com.

Choosing the Right Tool for the Job

These methods are not mutually exclusive. They are different tools for different time horizons.

- Use the Direct Method for: Your 13-week rolling forecast, managing working capital, and making tactical decisions on collections and payments.

- Use the Indirect Method for: Your annual budget, long-range strategic plans (12+ months), and demonstrating financial health to lenders and investors.

For any professional services firm, mastering the direct method is non-negotiable. The fastest way to improve its reliability is to automate inputs, particularly from accounts receivable, to improve cash flow visibility.

The Inputs and KPIs of a Reliable Forecast

A forecast is only as reliable as its underlying data. Garbage in, garbage out.

A poor forecast is not an inconvenience; it is a direct threat to liquidity.

Building a robust forecast is a disciplined process of gathering the right inputs and measuring the right outputs, sourced from operational systems, not a static spreadsheet.

The Essential Inputs: Cash Inflows

Inflows are the most volatile part of the forecast, making their accuracy critical.

For professional services, this comes down to the timing and certainty of client payments.

The core data points you need are:

- AR Aging Reports: The foundation of any short-term forecast, detailing who owes what and for how long.

- Sales Pipeline Data: Informs the longer-term view but requires honest analysis of close probabilities and converting them into future billing schedules.

- Client Retainers and Recurring Revenue: The most predictable inflows. Isolate them to establish a baseline of guaranteed cash.

A best practice is to analyze the historical payment behavior of key clients. If a client consistently pays in 45 days, forecast them that way, regardless of "Net 30" terms. This is where AI AR automation provides a significant advantage by predicting payment dates based on behavior, not contracts.

The Essential Inputs: Cash Outflows

Outflows are generally more predictable but require diligent tracking.

Key sources for your outflows include:

- Accounts Payable Schedules: A log of all approved vendor invoices and their due dates.

- Payroll and Commissions: Your largest and most predictable expense, including taxes and benefits.

- Fixed Operating Expenses: Rent, utilities, software subscriptions, insurance.

- Variable Project Costs: Subcontractor payments and other direct costs.

- Taxes and Debt Service: Scheduled payments that cannot be missed.

Together, these inputs provide a clear picture of committed spending.

The KPIs That Measure What Matters

Once built, the forecast's accuracy and impact must be measured.

- Days Sales Outstanding (DSO): The average number of days to collect payment after work is completed. A high DSO is a primary indicator of a cash flow problem. The goal is always to reduce DSO.

- Formula: (Accounts Receivable / Total Credit Sales) x Number of Days in Period

- Cash Conversion Cycle (CCC): The time it takes to convert your team's work into cash from clients. A shorter cycle signifies a more efficient and cash-generative business.

- Formula: Days Inventory Outstanding + DSO – Days Payables Outstanding

- Forecast Variance: The ultimate measure of your forecast's reliability. It calculates the difference between projected and actual cash positions.

- Formula: ((Actual Cash Balance - Forecasted Cash Balance) / Actual Cash Balance) x 100

A variance consistently below 5% indicates a well-controlled process. A higher variance often points to problems with your inputs—almost always tied to unpredictable receivables.

Improving these KPIs starts with tighter control over your receivables. To learn more about this, see our guide on receivable management services.

Common Forecasting Pitfalls and How to Avoid Them

Knowing what breaks a forecast is as important as knowing how to build one.

A few common errors can render forecasting useless, creating risk where you intended to build stability.

These are operational problems with direct, actionable solutions.

Over-Relying on Historical Data

The past is a guide, not a guarantee. Averaging the last six months of receipts to predict the next six ignores current business realities.

- Scenario: A marketing agency projects strong Q3 cash flow based on a successful Q2, forgetting Q2 was driven by a single large project that has now concluded. The result is a predictable but unplanned cash shortage.

- Solution: Combine historical data with forward-looking inputs from your current sales pipeline and project backlog. This provides a view of where the business is headed, not just where it has been.

Disconnected Sales and Finance Teams

This is a common and damaging pitfall. The sales team forecasts revenue based on signed deals, while finance understands that collecting the cash is a different challenge.

- Scenario: An engineering firm forecasts $500,000 in new Q1 revenue based on signed contracts. Finance builds its cash plan accordingly. However, two new clients historically pay on 60-day terms, not 30. The forecast is now off by tens of thousands, jeopardizing payroll.

- Solution: Implement a weekly sync between sales and finance to align the revenue forecast with a realistic collections forecast, adjusted for actual client payment behavior.

Ignoring Inflow Lumps and Bumps

Professional services revenue is inherently lumpy, driven by project milestones and variable client payment cycles. A forecast that smooths this into even monthly averages is a work of fiction.

An effective forecast must embrace this volatility. By accurately mapping the uneven nature of your inflows, you can plan for the valleys, not just celebrate the peaks. This is the essence of operational control.

Counteracting these pitfalls requires improving the quality and timeliness of your inputs. A system that provides real-time visibility into payment timelines is the most direct way to improve cash flow predictability.

How Automation Sharpens Your Forecast

The greatest variable in a manual cash forecast is not sales or expenses; it's when clients will actually pay.

This single uncertainty degrades a data-driven projection into an educated guess. Automation removes this guesswork.

It's not about replacing judgment; it's about providing a foundation of hard data. Automation delivers a single, dynamic source of truth for your most critical cash inflow: accounts receivable.

From Reactive Collections to Predictable Cash Flow

Most AR processes are reactive. An invoice receives attention only after it becomes past due. This forces finance teams into a constant cycle of chasing payments.

Accounts receivable automation establishes a consistent, proactive collections process. Scheduled reminders and standardized communication normalize on-time payments. This consistency directly translates into more reliable forecast inputs and a measurable ability to reduce DSO.

This level of control is critical. The cost of financing has more than doubled since 2021, making cash resilience a top priority. A reported $707 billion is currently tied up in working capital among S&P 1500 companies—a 40% increase from pre-pandemic levels.

This isn't just about efficiency. It's about creating a predictable rhythm for your inflows. To understand the bottom-line impact, review our guide on accounts receivable automation benefits.

The Power of AI in Predicting Who Pays When

The significant advance is AI AR automation. These platforms analyze historical payment data to predict when each client is likely to pay.

- Client-Specific Insights: An AI learns that Client A, despite "Net 30" terms, consistently pays 15 days late, while Client B always pays on the due date.

- Invoice-Level Predictions: The system identifies patterns, such as larger invoices being paid slower, and adjusts its predictions accordingly.

- Early Risk Detection: It flags invoices showing early signs of late payment before they become a problem, enabling proactive intervention.

This predictive capability replaces contractual hope with operational reality. Your forecast is no longer based on terms you set but on behaviors your data proves. The strategic use of Automation in banks is accelerating this trend.

A Single Source of Truth

Finally, automation eliminates the data silos that undermine accurate forecasting.

AR software for professional services, especially one that integrates with your ERP like QuickBooks AR automation, centralizes all client communication and payment data.

This provides a real-time, accurate view of your receivables.

Your cash forecast transforms from a backward-looking report into a strategic tool, giving you the clarity to improve cash flow with confidence.

A Few Questions We Hear Often

How Often Should We Update Our Cash Forecast?

Operate on two speeds.

Your short-term, 13-week forecast requires a weekly update. This is your operational dashboard for managing immediate liquidity.

Your long-term, 12+ month strategic forecast can be updated quarterly. Revisit it for any major event, such as a large new client or a significant capital investment.

What’s the Biggest Thing That Throws Forecasts Off?

For nearly every professional services firm, the answer is the timing of client payments.

The root cause of most cash flow surprises is in accounts receivable. Forecasts built on contract terms instead of actual client payment behavior are inherently flawed. The most direct path to an accurate forecast is predictable AR.

* **Visual Idea 1: A simple line chart titled "Forecast vs. Reality." One line shows a smooth, optimistic cash forecast. The second line shows the actual, volatile cash balance, highlighting the gap caused by late payments. ***

Can We Start This Without Buying Expensive Software?

Yes. A well-designed spreadsheet is an effective starting point. It builds the discipline of gathering inputs and establishing a consistent update rhythm.

However, spreadsheets have a low ceiling. As a firm grows, they become a liability due to manual errors, stale data, and a lack of predictive insight. Migrating to an integrated platform with QuickBooks AR automation is not just about saving time—it’s about improving the accuracy and strategic value of the forecast itself.

* **Visual Idea 2: A cinematic shot of a controller calmly reviewing a clean dashboard on a tablet, with a serene, organized office in the background. The mood is one of control and confidence, not stress. ***

--- Resolut automates AR for professional services—consistent, accurate, and human.