A CFO's Guide to the Revenue Recognition Principle

Understand what is revenue recognition principle under ASC 606. This guide shows finance leaders how to improve reporting, cash flow, and financial control.

When do you earn your money? It's not when the invoice is sent or when cash hits the bank.

The revenue recognition principle is clear: you recognize revenue only when you have earned it. This means you have delivered the promised value, regardless of payment status.

This is the foundation of accrual accounting. It shifts the focus from cash collection to value delivery, providing a true measure of your firm's performance.

The Foundation of Financial Clarity

For a professional services firm, this isn't just about compliance. It’s about operational control.

Proper revenue recognition ties your financial statements directly to client project progress. It provides an accurate measure of your firm's health.

This clarity supports more reliable forecasting and better strategic decisions, turning your financials into a forward-looking tool.

As business models evolved beyond simple cash-for-goods transactions, accounting standards had to adapt. Recognizing revenue when earned became the standard, fundamentally changing how profitability is measured.

Why This Isn’t Just a Finance Problem

The principle directly impacts key operational metrics. A misalignment between recognized revenue and invoicing distorts your financial reality.

It connects directly to operational performance:

- Accurate Performance Measurement: Your income statement reflects value delivered in a period, not just cash collected.

- Improved Cash Flow: Understanding earned revenue enables more accurate cash forecasting, separating performance from billing cycles.

- Reduced DSO: Linking revenue to performance obligations helps identify and resolve invoicing delays that inflate Days Sales Outstanding (DSO).

If you’ve completed 70% of a project, your books should show 70% of the earned revenue. The timing of the invoice is a separate, downstream event.

This principle, standardized by frameworks like ASC 606, is a key part of broader rules like the UAE Accounting Standards and Regulations. When applied correctly, it provides a clear map of your firm's financial position.

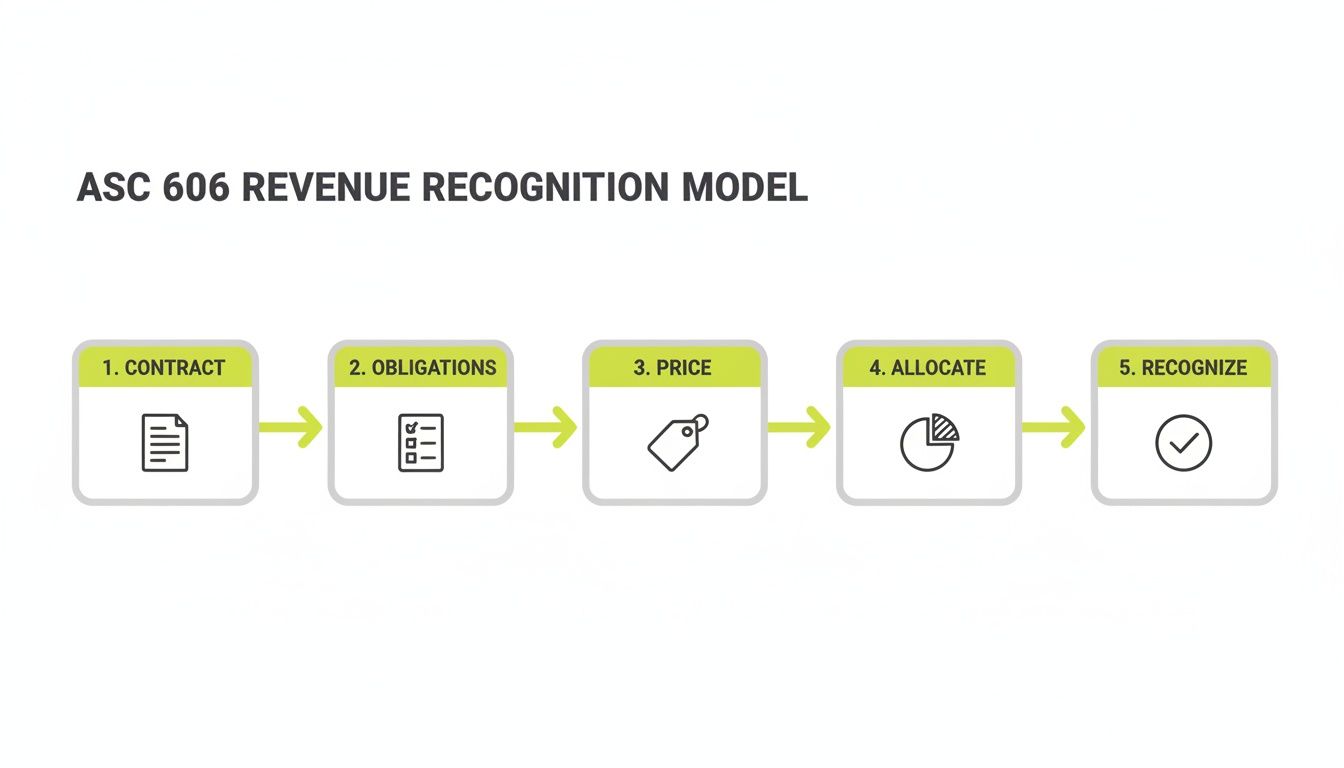

Executing The Five-Step ASC 606 Model

ASC 606 provides a five-step framework for revenue recognition. It is an operator's manual for financial clarity, replacing subjective assessments with a consistent process.

The modern framework (ASC 606 in the U.S. and IFRS 15 globally) was issued by FASB and IASB in 2014. It replaced complex, industry-specific rules to improve comparability and shift focus from invoicing to when the client gains control of a service. You can learn about the history and impact of this revenue recognition standard.

Let's walk through each step in the context of a professional services firm.

Step 1: Identify The Contract With The Customer

First, a legally enforceable agreement must exist. This is typically a Master Service Agreement (MSA) combined with a specific Statement of Work (SOW).

Under ASC 606, a valid contract must meet these criteria:

- Approval and Commitment: Both parties are committed to their obligations.

- Identifiable Rights: Each party’s rights are clearly defined.

- Identifiable Payment Terms: The SOW specifies payment terms.

- Commercial Substance: The transaction meaningfully impacts both parties' financial positions.

- Probable Collection: You have a reasonable expectation of being paid.

If these conditions are not met, revenue cannot be recognized.

Step 2: Pinpoint Performance Obligations

A performance obligation is a distinct promise to deliver a service. ASC 606 requires unbundling these promises.

Consider a $100,000 technology implementation SOW. It likely includes:

- Phase 1: Discovery and strategic planning.

- Phase 2: System configuration and integration.

- Phase 3: User training and go-live support.

- Ongoing: 12 months of post-launch technical support.

Each of these is a separate performance obligation because the client can benefit from each one independently. This step is critical for accurate allocation.

The objective is to deconstruct the SOW into its core promises. If a service can be sold separately or provides distinct value to the client, it is a separate performance obligation.

Step 3: Determine The Transaction Price

The transaction price is the total consideration you expect to receive. This can become complex with variable components.

You must account for all elements:

- Fixed Fees: The baseline project price.

- Performance Bonuses: Incentives tied to specific outcomes.

- Retainers: Recurring fees for ongoing services.

- Discounts or Rebates: Any offered price reductions.

For variable consideration, you must estimate the most likely amount you will earn and include it in the transaction price, based on historical data and contract terms.

Step 4: Allocate The Price To Performance Obligations

Next, allocate the total transaction price (Step 3) across each distinct performance obligation (Step 2). This allocation must be based on the standalone selling price (SSP) of each component.

SSP is the price you would charge for a service if sold separately. If an SSP is not readily available, estimate it using a reasonable method, such as market assessment or a cost-plus-margin approach.

Allocation Example For our $100,000 project, you determine the SSP for each component:

- Phase 1 (Discovery): SSP of $15,000

- Phase 2 (Configuration): SSP of $50,000

- Phase 3 (Training): SSP of $10,000

- Support (12 months): SSP of $30,000

The total SSP is $105,000. You then allocate the $100,000 contract price proportionally across the four obligations based on these standalone values.

Step 5: Recognize Revenue When Obligations Are Satisfied

The final step is to recognize revenue as each performance obligation is fulfilled. Revenue is recognized either at a point in time or over time.

- Point in Time: Revenue is booked when control of the service transfers to the client, such as upon formal sign-off of a project phase.

- Over Time: Revenue is recognized progressively as the service is delivered. The 12-month support contract is a clear example; you would recognize 1/12th of its allocated price each month.

This five-step process ensures your financials accurately reflect value delivery, providing a clear and compliant view of performance.

Putting The Revenue Principle Into Practice

Translating theory into compliant journal entries is where control is established. For professional services firms, application of the revenue recognition principle shapes your financial narrative.

Misapplication distorts your firm’s true financial health and creates compliance risks.

Let’s examine how this looks on the general ledger for two common scenarios: a fixed-fee project and a 12-month advisory retainer.

Recognizing revenue is a systematic process, not a single event. It requires a sequence that ensures accuracy and compliance.

Scenario 1: A Multi-Phase Consulting Project

Your firm secures a $150,000 contract for a three-phase project and invoices the full amount upfront. Under ASC 606, revenue can only be recognized as each phase is completed.

Assume each phase has an equal standalone value:

- Phase 1: Discovery & Assessment ($50,000)

- Phase 2: Implementation ($50,000)

- Phase 3: Training & Go-Live Support ($50,000)

When the $150,000 invoice is sent, you record an accounts receivable and a corresponding liability called Deferred Revenue. This represents the value of services you still owe the client.

The initial journal entry: Debit Accounts Receivable for $150,000 and credit Deferred Revenue for $150,000. Your income statement remains unchanged.

Upon completion of Phase 1, you have earned that portion of the fee. You then recognize the $50,000 through an adjusting entry, moving it from the liability account to a revenue account.

Journal Entry Example For A Multi Phase Project

Transaction Event | Account Debited | Amount | Account Credited | Amount |

|---|---|---|---|---|

Initial Invoice Sent | Accounts Receivable | $150,000 | Deferred Revenue | $150,000 |

Phase 1 Completed | Deferred Revenue | $50,000 | Service Revenue | $50,000 |

Phase 2 Completed | Deferred Revenue | $50,000 | Service Revenue | $50,000 |

Phase 3 Completed | Deferred Revenue | $50,000 | Service Revenue | $50,000 |

After Phase 1, your balance sheet shows $100,000 in remaining deferred revenue, and your income statement reflects $50,000 in earned revenue. This process repeats, matching revenue to performance.

Scenario 2: A 12-Month Advisory Retainer

Consider a $60,000 annual retainer, paid upfront. The performance obligation is satisfied evenly over time, requiring a straight-line recognition method.

When the client pays, you debit Cash for $60,000 and credit Deferred Revenue for $60,000. No revenue has been recognized.

Each month, as services are delivered, you earn 1/12th of the total contract value, or $5,000. At the end of each month, your team makes this adjusting entry:

- Debit: Deferred Revenue $5,000

- Credit: Retainer Revenue $5,000

This systematically reduces the deferred revenue liability while booking earned revenue. After 12 months, the Deferred Revenue account is zero, and you've recognized the full $60,000. To see how this fits into the broader order-to-cash process, review our guide.

Executing these entries requires disciplined systems. An effective accounting system integration is essential to prevent manual errors and ensure revenue is recognized at the correct cadence.

Connecting Revenue Recognition To Invoicing And Cash Flow

Proper revenue recognition is a diagnostic tool. It exposes the gaps between value delivery and cash collection.

A mismatch between recognized revenue and invoicing distorts your cash conversion cycle and masks operational friction that drains working capital.

The Diagnostic Power of ASC 606

Viewing operations through the lens of revenue recognition turns financial reports into catalysts for improvement.

For example, recognizing significant revenue long before sending an invoice is a common issue in professional services. This artificially inflates DSO, restricts cash flow, and signals problems in project management or client communication.

The timing of revenue recognition materially affects key financial metrics. A majority of public companies reported needing substantive process changes to comply with ASC 606, as shifts in timing altered reported growth rates and key performance indicators.

Aligning revenue recognition with invoicing produces a more accurate DSO calculation. It pinpoints when value is transferred and measures the subsequent delay until billing, revealing hidden operational bottlenecks.

From Compliance To Operational Control

This alignment moves the conversation from accounting theory to operational reality. You can see inefficiencies that were previously invisible.

Proper revenue recognition brings these operational gaps to light:

- Delayed Milestone Approvals: If revenue recognition depends on client sign-off, approval delays become direct roadblocks to converting earned value into cash.

- Inefficient Invoicing Workflows: A lag between project managers signaling work completion and finance issuing an invoice directly extends your cash cycle.

- Scope Creep: Tracking revenue against specific performance obligations makes it clear when your team is delivering unbilled work.

Addressing these issues directly helps reduce DSO. This is one of the most effective ways to increase cash flow.

Automating The Link Between Performance And Payment

Manually tracking performance obligations to trigger invoices is prone to error and delay. Accounts receivable automation provides a critical layer of control.

Modern AI AR automation translates SOW terms into intelligent workflows, creating a real-time link between service delivery, revenue recognition, and invoicing. For firms on QuickBooks, QuickBooks AR automation is essential for maintaining this discipline.

This ensures that once a performance obligation is met, the system can automatically generate and send the correct invoice. It removes the human latency that separates earned revenue from billed revenue, directly improving cash flow.

Achieving Compliance And Control With AR Automation

Managing revenue recognition in spreadsheets is fragile. The process is a maze of manual entries, prone to error, and a significant time commitment for finance teams. It is a compliance risk.

AR automation provides stability and control.

Automation integrates financial discipline into daily operations, shifting revenue recognition from a reactive, manual task to a proactive, systematic workflow.

Codifying Contracts Into Repeatable Workflows

The power of accounts receivable automation is its ability to translate complex contracts into simple, trusted workflows. The system tracks project milestones and triggers invoicing automatically.

This creates a clean, auditable link between work delivered and numbers reported.

- Automated Revenue Schedules: The platform builds revenue schedules directly from the performance obligations in your SOWs.

- Precision Invoicing: Invoices are sent automatically the moment a performance obligation is met, closing the gap that inflates DSO.

- Reduced Manual Entry: Integration, such as with QuickBooks AR automation, eliminates manual data entry that leads to errors.

The goal is to perfectly reflect project activity in your financials, in real time.

From Data Lag To Real-Time Visibility

Spreadsheets provide a rearview-mirror perspective. They show last month's performance, not the current state. This data lag makes accurate forecasting and proactive cash flow management impossible.

An AI AR automation platform provides a live, dynamic view.

The goal is to move from periodic reporting to continuous financial intelligence. An automated system offers a real-time dashboard of recognized versus deferred revenue, giving leadership an accurate pulse on the firm's health.

This real-time visibility enables faster, smarter decisions. It allows you to manage finances proactively instead of reacting to outdated data. These principles align with broader strategies in receivable management services that optimize the entire order-to-cash cycle.

Strengthening Internal Controls And Reducing Risk

For CFOs and Controllers, internal controls are paramount. Manual processes are inherently risky; a single formula error can cause a material misstatement of revenue.

AR software for professional services reinforces controls by creating a transparent, auditable system of record.

- Systematic Documentation: Every action, from contract signing to final payment, is logged, creating a solid audit trail.

- Error Reduction: Automation removes the risk of human error in revenue calculations and journal entry timing.

- Consistency: The system applies the same logic to every contract, ensuring your revenue recognition policy is enforced uniformly.

The right technology makes financial discipline achievable. It takes the principles of revenue recognition and makes them an operational reality, helping you reduce DSO and improve cash flow with confidence.

Common Revenue Recognition Questions Answered

Applying the revenue recognition principle to real-world scenarios like contract modifications or client retainers can be complex.

Incorrect handling of these situations can distort your financials and create significant compliance issues. Clarity is key to maintaining control.

How Do We Handle Contract Modifications Under ASC 606?

When a contract changes, you must determine if it is a modification of the existing contract or a new one.

If the change adds distinct services priced at their standalone value, it can be treated as a separate contract. If the new work is interdependent with the original scope, you will likely need to adjust the transaction price and reallocate it over the remaining obligations. Document the rationale for your decision.

What Is The Biggest Mistake Firms Make With Retainers?

The most common error is recognizing the entire monthly retainer fee as revenue when the cash is received.

This violates the revenue recognition principle. You must analyze the pattern of service delivery. If value is delivered consistently each month, a straight-line recognition method is appropriate. If the retainer covers intermittent, high-intensity work, revenue recognition must match that uneven delivery schedule.

The core question is always: "What value did we deliver this period?" Revenue must mirror the delivery cadence, not the payment schedule.

Booking cash directly to revenue is a compliance risk and provides a false measure of performance.

Does Using QuickBooks Make Us ASC 66 Compliant?

No. QuickBooks is a system of record, not a compliance engine. It records the transactions you input.

Your finance team remains responsible for the analysis, calculations, and journal entries required to defer and recognize revenue according to the five-step model. This often involves complex spreadsheets managed outside of your accounting software.

AR software for professional services is designed to fill this gap. A platform with QuickBooks AR automation adds the necessary revenue recognition logic on top of your accounting system, ensuring entries are calculated and timed correctly based on contract terms.

How Does ASC 606 Affect Sales Commission Expenses?

The standard changes how you account for costs to obtain a contract, particularly sales commissions. You can no longer expense the full commission when it is paid.

Instead, these costs must be capitalized as an asset on your balance sheet. This asset is then amortized over the same period that revenue from the contract is recognized. This approach aligns the cost of the sale with the revenue it generated, providing a more accurate view of contract profitability.

--- Resolut automates AR for professional services—consistent, accurate, and human.