A CFO's Guide to the Accounts Receivable Loan

Explore if an accounts receivable loan is right for your firm. This guide helps CFOs weigh the costs, risks, and alternatives to improve cash flow.

Waiting on client payments is a familiar operational reality for professional services firms. An accounts receivable loan is a financial instrument that converts unpaid invoices—your accounts receivable—into immediate working capital, bridging the 30, 60, or 90-day gap until clients pay.

This guide provides a clear, operator-focused view of how these loans function, their true cost, and how they compare to other financing options.

Understanding the Accounts Receivable Loan

An accounts receivable loan is a revolving line of credit secured by the money your clients owe you. Unlike a traditional term loan, it provides a flexible financial facility. You draw funds against your eligible invoices as needed, granting you control over cash flow rather than letting client payment cycles dictate your operations.

For a CFO or Controller, the primary value is predictability. You no longer need to hope a large check arrives before payroll is due. You can access the value of your work on demand, turning accounts receivable from a static balance sheet item into an active source of liquidity.

A Tool for Strategic Control

At its core, an AR loan smooths cash flow volatility. For example, a professional services firm with $500,000 in outstanding invoices from creditworthy clients could typically access 75-90% of that value—$375,000 to $450,000—within days.

This capital can be deployed to:

- Meet payroll and cover operating costs without draining cash reserves.

- Fund growth initiatives, such as hiring key personnel or launching a new service line.

- Bridge seasonal revenue gaps common in project-based firms.

This is fundamentally different from invoice factoring. With an AR loan, your firm retains control over collections. Your clients are unaware of the financing arrangement, preserving client relationships. Factoring involves selling invoices to a third party that takes over collections, which can disrupt the client experience.

Control over the client relationship is paramount. An AR loan provides financing without inserting a third party into your collections process. You manage your accounts your way.

Financial Health and Internal Optimization

While an AR loan is a powerful tool for financial stability, the most effective strategy begins with internal process optimization. Improving your firm's ability to collect receivables can significantly reduce or eliminate the need for external financing. You can learn more about related options in our guide on what is receivables financing.

This is where accounts receivable automation is critical. Automating invoicing, reminders, and payment processing directly helps reduce DSO and improve cash flow. Tools like QuickBooks AR automation or specialized AR software for professional services are designed for this function.

Pairing strong internal collections with intelligent financing options creates a resilient financial foundation for your firm.

How An AR Loan Works: The Mechanics

An accounts receivable loan converts unpaid invoices into immediate cash without disrupting client relationships. The process begins with a lender's underwriting of your accounts receivable portfolio.

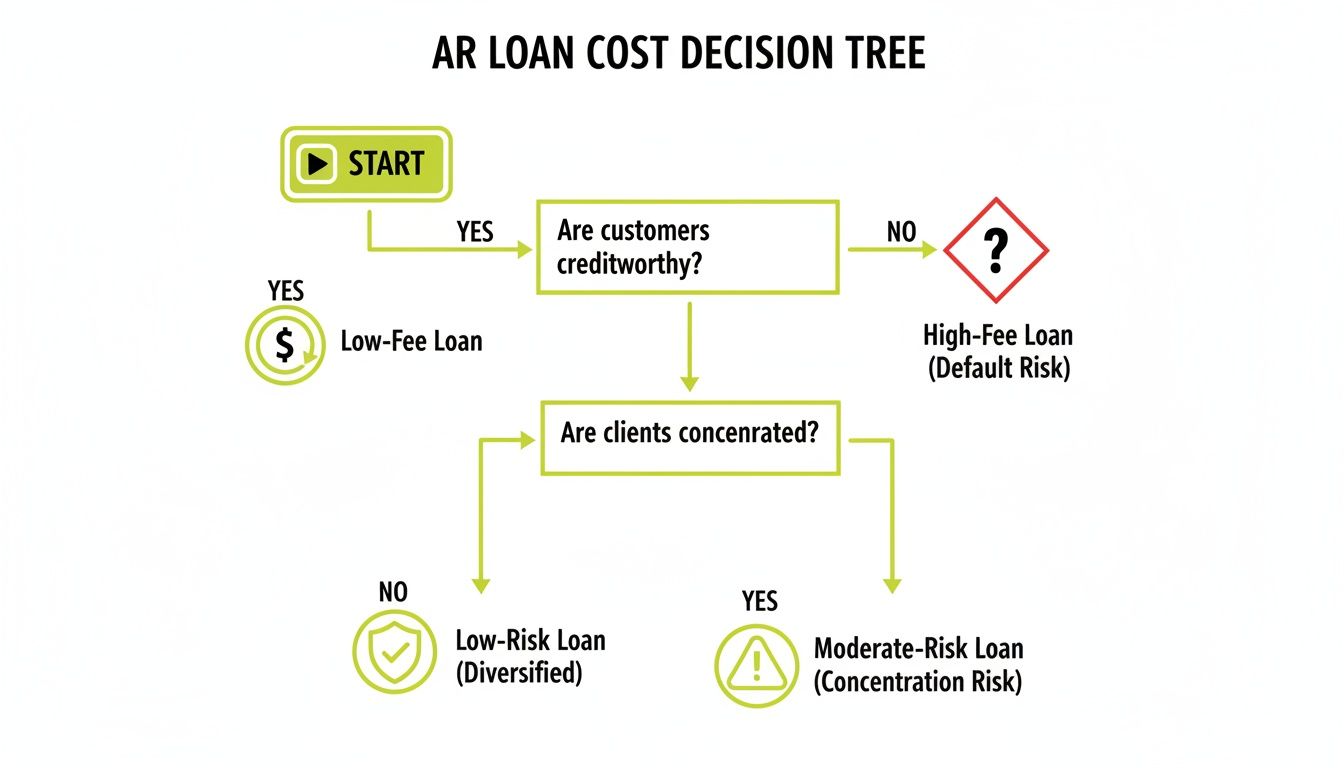

The lender's primary focus is not on your firm's overall profitability but on the quality of your invoices and the creditworthiness of your clients. They analyze customer payment histories, invoice aging, and client concentration. This analysis determines which invoices are "eligible" for financing.

Establishing The Borrowing Base

From the pool of eligible invoices, the lender establishes a borrowing base—the total amount of capital you can access. Lenders typically advance 75% to 90% of the eligible receivables' value. This percentage is the advance rate.

For a professional services firm with $1,000,000 in qualified invoices and an 85% advance rate, the borrowing base is $850,000. This often functions as a revolving line of credit. As clients pay their invoices, that portion of your credit line is replenished, providing a reliable, ongoing funding source.

The global accounts receivable financing market is projected to reach $182.63 billion by 2026 as businesses seek to unlock trapped cash. With the average U.S. Days Sales Outstanding (DSO) at 38.2 days, the pressure to reduce DSO and improve cash flow is a significant operational challenge. You can review market shifts in this report on accounts receivable financing trends.

Recourse vs. Non-Recourse: A Critical Distinction

A key structural decision is choosing between a recourse or non-recourse agreement. This choice fundamentally alters your firm’s financial risk and the cost of the loan. It is a strategic decision for any finance leader.

A recourse loan means your firm is liable if a client fails to pay. If a customer defaults, you must buy back the bad debt from the lender or replace it with a new, eligible invoice.

While this introduces risk, the trade-off is lower fees and more favorable interest rates because the lender assumes less risk. This structure is often suitable for firms with a stable base of reliable clients and effective internal collection processes.

A non-recourse loan transfers the risk of non-payment to the lender. If a client declares bankruptcy or fails to pay for a credit-related reason, the lender absorbs the loss. This provides significant balance sheet protection but comes at a higher cost.

A Practical Example: A $5M Services Firm

Consider a $5M architectural firm with a $500,000 borrowing base.

- Recourse Scenario: The firm secures favorable financing terms. When a major client becomes insolvent, leaving a $50,000 unpaid invoice, the firm must repay the $50,000 advance to the lender.

- Non-Recourse Scenario: The firm pays higher fees. When the same client defaults, the lender absorbs the $50,000 loss. The firm’s cash flow is insulated from the credit event.

The decision depends on your firm's risk tolerance and the credit quality of your client portfolio. Implementing accounts receivable automation can make recourse financing more viable by improving collection outcomes. Whether using dedicated AR software for professional services or an integrated tool like QuickBooks AR automation, a disciplined collections process is your best risk mitigation tool.

Calculating the True Cost of an AR Loan

The quoted interest rate on an accounts receivable loan is only one component of its total cost. To understand the effective cost of capital, you must analyze the complete pricing structure.

The two primary components are the advance rate and the discount fee. The advance rate determines your upfront cash access, but the discount fee represents the primary cost. This fee is the lender's charge, calculated as a percentage of the invoice's total value.

How the Discount Fee Works

The discount fee is not a simple interest rate. It is a dynamic cost tied directly to your collections performance. The longer an invoice remains unpaid, the more the financing costs.

For instance, a lender might charge a 1.5% fee for the first 30 days. If the invoice ages into the 31-60 day bucket, an additional fee, perhaps 1.0%, could be applied. This structure directly links your cost of borrowing to your collections efficiency.

A firm with a 35-day Days Sales Outstanding (DSO) will pay substantially less for financing than a firm with a 65-day DSO. Each additional day an invoice is outstanding directly impacts your profit margin on that engagement.

The total cost of an AR loan is not a fixed number; it is a function of your operational performance. It rewards firms with tight control over their collections cycle and penalizes those without.

In addition to the discount fee, other charges can accumulate. Key items to clarify include:

- Origination Fees: A one-time fee to establish the credit facility, often 1-2% of the total line.

- Servicing Fees: A recurring monthly fee for account maintenance, payable regardless of borrowing activity.

- Early Termination Penalties: A fee assessed if you close the facility before the contract term ends.

The Underwriting Viewpoint: What Lenders Evaluate

To secure the most favorable terms, it's helpful to understand the lender's perspective. Their primary concern is the quality of the asset backing the loan—your invoices. Lenders are underwriting your customers' ability and willingness to pay.

They will scrutinize the payment histories, credit scores, and financial stability of your largest accounts. A portfolio of invoices from investment-grade or reputable companies is a much lower-risk asset than one concentrated in small, unproven businesses.

Key Underwriting Factors

Lenders focus on several key metrics to price risk and set terms:

- Client Concentration: If a single customer represents more than 20-25% of your receivables, it creates concentration risk. A diversified client base is always preferable.

- Collections History and DSO: A consistent and low DSO demonstrates predictable cash flow and effective collections controls, making you a lower-risk borrower.

- Invoice Aging: The age of your receivables is critical. Lenders will heavily discount or exclude invoices over 90 days old, as the probability of collection decreases significantly.

This underwriting focus creates a powerful incentive to optimize internal processes. Implementing effective accounts receivable automation directly improves these metrics. A well-configured AI AR automation system helps reduce DSO and maintain a clean aging report, making your firm a more attractive borrower.

Whether using specialized AR software for professional services or tools like QuickBooks AR automation, the objective is the same: first, improve cash flow by optimizing your own collections.

AR Loans Versus Other Financing Options

Not all working capital solutions are created equal. For a professional services firm, the choice between an accounts receivable loan, invoice factoring, and a traditional bank line of credit is a strategic decision that affects cost, operational control, and client relationships.

An accounts receivable loan functions as a private, revolving line of credit collateralized by your outstanding invoices. Crucially, you maintain complete ownership of your collections process. Your clients remain unaware of the financing, a non-negotiable for firms built on trust.

AR Loans vs. Invoice Factoring: Who Owns the Relationship?

While both are tied to invoices, an AR loan and invoice factoring are operationally distinct.

With factoring, you are not borrowing against your invoices; you are selling them to a third-party company (the "factor") at a discount. In most arrangements, the factor then assumes control of the collections process, contacting your clients directly for payment. You receive cash quickly but introduce another party into your client relationships.

For many professional services firms, this loss of control is a significant drawback. An AR loan is confidential. Your client communications and relationships remain unchanged.

An accounts receivable loan is a private loan against your invoices. Factoring is the sale of your invoices to a third party who collects from your client. That distinction changes everything.

For a more detailed analysis, see our full guide explaining what invoice factoring is and its appropriate use cases.

What About a Traditional Bank Line of Credit?

A bank line of credit is another common option, often with a lower stated interest rate. The challenge is that banks underwrite the entire business—historical profitability, assets, balance sheet, and overall credit history.

This makes bank lines difficult to secure, particularly for high-growth firms or those with cyclical revenue. They also tend to come with restrictive covenants, such as maintaining specific debt-to-equity ratios, which can limit financial flexibility.

A Side-by-Side Look at Your Options

Comparing these financing tools directly on the metrics that matter most to a finance leader clarifies the trade-offs.

Comparison of Working Capital Financing Options

Financing Tool | Basis of Funding | Control of Collections | Typical Cost Structure | Best For |

|---|---|---|---|---|

Accounts Receivable Loan | Value of eligible outstanding invoices. | You retain full control. Financing is invisible to clients. | Discount fee on advanced funds (similar to an interest rate). | Firms needing flexible, confidential cash flow while protecting client relationships. |

Invoice Factoring | Value of specific invoices sold to the factor. | The factor usually takes control. They contact your clients. | Higher percentage-based fee, as the factor performs collection work. | Businesses prioritizing immediate cash and willing to outsource collections. |

Traditional Line of Credit | The company's overall creditworthiness and financial health. | You retain full control. | Lower interest rate, but often has strict covenants and reporting. | Established companies with strong, predictable financials and credit history. |

The decision balances cost, control, and qualification difficulty.

A lender's risk assessment, which determines your cost, is driven by factors like customer credit quality and revenue concentration.

A diversified roster of creditworthy customers is the most direct path to favorable financing terms.

While manufacturing and wholesale enterprises account for roughly 70% ($350 billion) of this financing market annually, small and medium-sized B2B firms still represent a significant $150 billion segment. It is a proven tool for unlocking cash trapped in receivables.

If maintaining absolute control over the client experience is paramount, an accounts receivable loan is almost always the superior choice. It provides liquidity to smooth cash flow and reduce DSO without disrupting operations or client relationships.

The Best Alternative to Debt? First, Fix Your Cash Flow

An accounts receivable loan can be an effective tool, but the most efficient dollar is one already earned. Before taking on debt, the first and most logical step is to optimize internal collections. By improving the efficiency of your order-to-cash cycle, you can significantly reduce—or even eliminate—the need for a loan.

This is about shifting focus from treating the symptom (cash shortage) to curing the cause (a slow collections process). A reliable, efficient collections engine creates a level of financial self-sufficiency that no loan can provide.

Unlock Trapped Cash by Reducing Your DSO

The key metric is Days Sales Outstanding (DSO). It measures how much of your revenue is tied up in your clients' accounts payable. For professional services firms, a high DSO can severely constrain operations.

The financial impact is direct. For a firm with $10M in annual revenue, reducing the collection cycle by just 10 days unlocks over $270,000 in cash.

$10,000,000 (Annual Revenue) / 365 days = $27,397 (Daily Revenue)$27,397 x 10 days = $273,970 (Freed Working Capital)

This is capital you recover without paying interest or fees. It can be used for payroll, growth investments, or building cash reserves—all without the covenants attached to an AR loan.

Implement AR Automation for Systematized Collections

The most direct way to lower DSO is with accounts receivable automation. Manual follow-up is inconsistent, time-consuming, and prone to error. Automation creates a systematic, professional, and scalable process.

Practical applications include:

- Automated Reminders: A system that sends programmatic, professional reminders before, on, and after an invoice due date ensures no invoice is forgotten.

- AI-Powered Outreach: Modern AI AR automation can analyze client payment patterns to tailor its approach. A historically slow-paying client might receive more frequent communications, while consistently prompt clients receive gentler reminders.

- Client Payment Portals: Reducing payment friction is key. A dedicated online portal where clients can view invoices and pay via ACH or credit card simplifies the process and accelerates payment.

This technology is no longer exclusive to large enterprises. Effective AR software for professional services can integrate directly with accounting platforms like QuickBooks. This QuickBooks AR automation provides immediate control and a clear view of your receivables. For more detail, see our guide on how to automate accounts receivable.

By focusing on internal processes first, you address the root cause of cash flow gaps, building a more resilient business and maintaining control over your firm's financial future.

Building a Financially Resilient Firm

An accounts receivable loan can serve as a tactical bridge over a cash flow gap, but it should not be a long-term solution. Chronic reliance on lending to fund operations often indicates a deeper issue in the order-to-cash cycle.

The strategic goal is to build a firm with the financial resilience to operate from its own cash flow. This resilience is achieved internally—by gaining control over your accounts receivable and turning them into a predictable source of cash, not stress.

The Real Fix: Automating Your Accounts Receivable

The most direct path to financial self-sufficiency is accounts receivable automation. By systematizing the entire AR process—from invoicing and reminders to cash application—you regain control and unlock cash that is already yours, faster.

Firms adopting AI AR automation typically see their DSO (Days Sales Outstanding) fall by 10-20% within months. For a $10M revenue firm, a 10-day DSO reduction frees up over $270,000 in working capital.

Automation replaces unpredictable cash flow spikes and troughs with a smoother, more predictable inflow. This financial clarity enables more confident, strategic decision-making.

It also improves client relations. An automated system delivers professional, consistent follow-ups, which is preferable to awkward, manual reminder calls. Using tools like QuickBooks AR automation or a specialized AR software for professional services is not just an efficiency play. It is a core strategy to improve cash flow and build a stronger financial foundation.

Frequently Asked Questions

Clear answers are essential when evaluating any financing option. Here are the most common questions from business owners and finance leaders regarding accounts receivable loans.

How Quickly Can I Receive Funds?

Initial setup with a new lender typically takes one to two weeks for due diligence, where the lender underwrites your receivables and establishes the credit facility.

Once the facility is in place, you can draw funds against new invoices almost immediately. It is common to receive funds in your account within 24 to 48 hours. This speed allows you to meet urgent payroll or act on time-sensitive growth opportunities.

Will My Customers Know I Am Using an AR Loan?

No. An accounts receivable loan is a private agreement between your firm and the lender. You retain full control of your client relationships and the collections process. From your customer's perspective, nothing changes.

This confidentiality is a key advantage for professional services firms where trust is paramount. It is the opposite of most invoice factoring arrangements, where the factor takes over collections and contacts your clients directly.

A key feature of an AR loan is its confidentiality. You get the cash flow needed without disrupting the client trust you have worked to build.

What Are the Typical Qualification Requirements?

Lenders focus less on your firm's profitability and more on the health of your accounts receivable. They are underwriting your customers' history and ability to pay on time. Optimizing your cash flow and ensuring timely collection of outstanding invoices can be boosted by utilizing a proven demand letter template proven to get invoices paid.

Key underwriting criteria include:

- Client Quality: A client list of reputable, creditworthy companies is your strongest asset.

- Collection Performance: Lenders analyze your Days Sales Outstanding (DSO). A history of efficient collections indicates lower risk.

- Invoice Concentration: A high concentration of revenue from one or two clients creates risk. Lenders prefer a diversified customer base.

A history of on-time payments from a reliable, diverse client portfolio will put you in a strong position to secure an AR loan with favorable terms.

--- Resolut automates AR for professional services—consistent, accurate, and human. Learn more at https://www.resolut.com.