A CFO's Guide to Controlling ACH Payment Processing Fees

A complete guide for CFOs on ACH payment processing fees. Learn to analyze costs, reduce expenses, and improve cash flow with strategic AR automation.

For finance leaders at professional services firms, payment processing fees are a persistent drag on the bottom line. Credit card costs are obvious, but ACH payment processing fees are more nuanced—a mix of direct costs, hidden charges, and operational inefficiencies.

Controlling these fees is the first step toward building an accounts receivable system that improves cash flow, rather than eroding it. This guide provides a finance operator's perspective on how to analyze and reduce your total cost of getting paid.

The Hidden Costs of Accepting Payments

Effective cost control requires looking beyond headline percentages. Seemingly small per-transaction ACH fees compound across thousands of invoices, quietly degrading profit margins.

Unlike the flat 2-3% for credit cards, ACH costs have multiple layers. The true expense includes the transaction fee plus monthly platform fees, penalties for returns (NSF), and batch processing charges. These variables obscure the actual cost of collections.

Visual Idea: A cinematic shot of a CFO at a large oak desk, late at night, a single lamp illuminating a tablet displaying a detailed cost analysis dashboard. The focus is on the screen, showing a line item for "non-itemized payment fees."

To gain clarity, you must analyze your processor’s fee schedule line-by-line. This is the only way to build an accurate financial model and make informed decisions. You can learn more about payment processing fundamentals for a deeper review.

Why ACH Cost Control Is a Strategic Priority

The ACH network is now central to B2B payments, making cost optimization a critical priority for any finance operator. The data signals a structural shift away from paper checks and expensive wire transfers.

In 2023, the ACH Network processed 31.5 billion payments worth over $80 trillion. This volume, driven by Same-Day ACH and B2B adoption, confirms the payment rail’s importance. For leaders managing AR, mastering ACH is fundamental to running a capital-efficient operation.

This guide provides an operator’s framework for deconstructing these fees. It equips you to evaluate your current setup, identify waste, and exert control over your accounts receivable function.

How ACH Fee Models Impact Your P&L

Focusing on a single transaction cost is a tactical error. Payment processors use several pricing models, and your choice has a material impact on firm profitability. A model that appears favorable can become costly if misaligned with your firm’s average invoice value and payment volume.

Selecting the right model is a strategic financial decision that directly affects your cost of collections and, by extension, your cash flow. Let's review the common structures to evaluate vendor proposals effectively.

The Predictable Choice: Flat-Fee Pricing

The most transparent model is flat-fee pricing. You pay a fixed dollar amount per transaction, regardless of its value. For a professional services firm with invoices typically valued in the thousands of dollars, this is almost always the most economical structure.

A $0.50 fee on a $10,000 invoice is a rounding error. This model provides cost certainty, simplifying financial forecasting. You know the precise cost of every client payment, with no variability.

The Costly Trap: Percentage-Based Pricing

Conversely, percentage-based pricing calculates the fee as a share of the total transaction amount. While the rate often appears low—typically 0.5% to 1.5%—it becomes a significant expense for high-value B2B payments.

This model is only viable for businesses with high volumes of low-dollar transactions. For a firm with a $10,000 average invoice, a 1% fee amounts to $100. This is a substantial increase over a flat fee and directly reduces your profit margin.

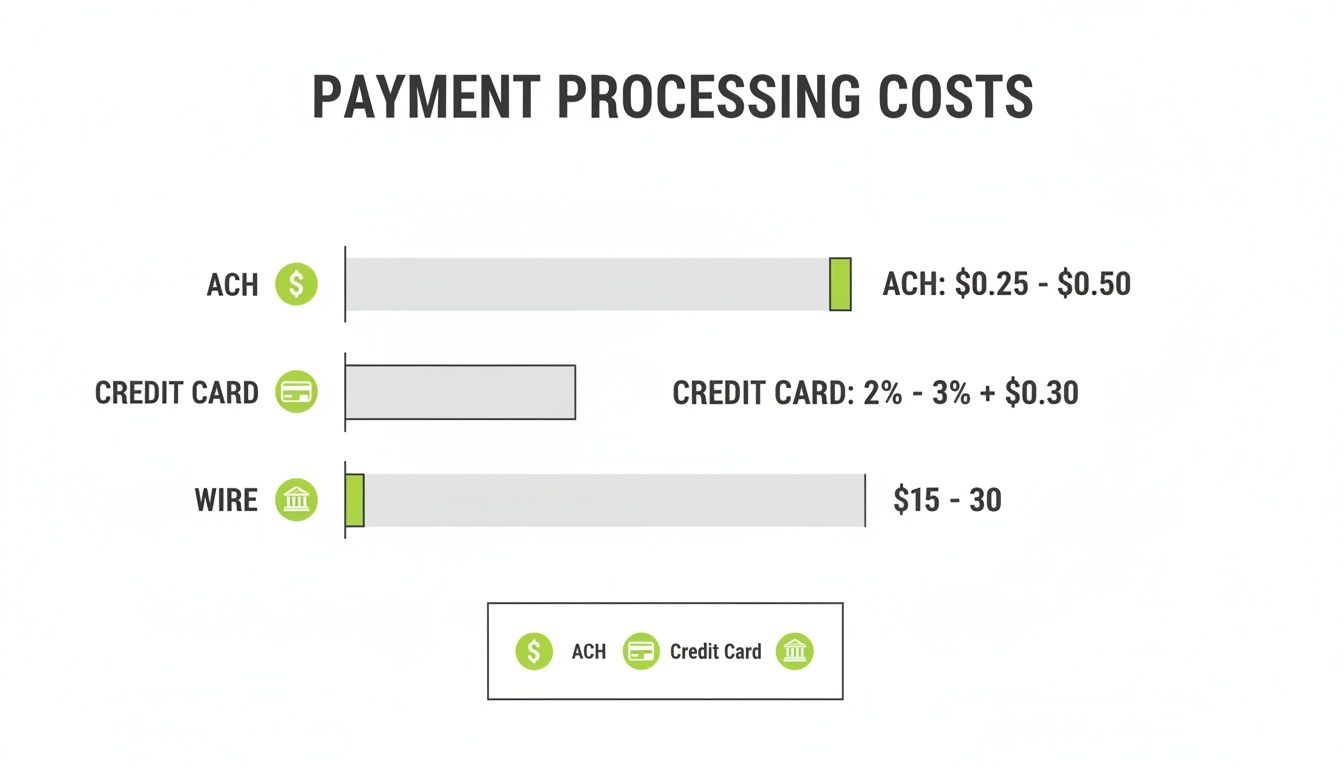

ACH processing remains highly cost-effective, typically costing $0.20 to $1.50 per transaction. This is 10 to 20 times cheaper than the 2.6%+ for credit cards or $15–$50 for a wire transfer. As you'll find in more detailed breakdowns, flat fees are usually $0.20–$1.50, while percentage-based fees are 0.5%–1.5%.

Tiered and Interchange-Plus: Adapted from Credit Cards

You may encounter two other models adapted from the credit card industry: tiered and interchange-plus.

- Tiered Pricing: This model groups transactions into "tiers," each with a different rate. The primary issue is a lack of transparency; the processor determines the classification, often to their own benefit.

- Interchange-Plus Pricing: The most transparent model, but typically reserved for very high-volume businesses. It applies a fixed markup over the base "interchange" rate set by Nacha (the ACH network operator).

For most professional services firms in the $3M–$50M revenue range, the decision is a direct choice between a flat-fee and a percentage-based model.

Watch for Ancillary Fees

The per-transaction fee is only one component of your total cost. Ancillary fees, often buried in the contract, can inflate your expenses. Ignoring these will lead to a significant underestimation of your true costs.

Common add-ons include:

- Monthly Account Fees: A fixed charge for maintaining an active account.

- Batch Fees: A small fee for submitting a group of transactions.

- Return Fees: A penalty, typically $2-$5, for payments that fail due to non-sufficient funds (NSF) or incorrect account data.

- Same-Day ACH Premiums: An extra charge, often $0.50-$1.00, for accelerated settlement.

When comparing providers, model these costs against your firm's actual payment data. This is the only way to accurately project the financial impact and avoid a costly misalignment.

Comparing ACH Fee Models for Professional Services

Fee Model | Typical Cost Structure | Best For | Potential Hidden Costs |

|---|---|---|---|

Flat Fee | $0.25 - $1.50 per transaction. | Firms with high average invoice values (>$500). Offers predictable, low costs for large B2B payments. | Monthly account minimums, batch fees, and higher-than-average return fees. |

Percentage-Based | 0.5% - 1.5% of the transaction amount. | Businesses with a high volume of small transactions (e.g., e-commerce, subscriptions). | Becomes extremely expensive for invoices over a few hundred dollars. May have a monthly fee. |

Tiered | Rates vary by transaction "tier." | Generally not recommended. Favors the processor and lacks transparency. | The processor decides tier placement, often resulting in higher effective rates than advertised. |

Interchange-Plus | (Interchange Rate + Fixed Markup). | Very large enterprises with massive transaction volume. | Too complex for most professional services firms; the fixed markup can still be high. |

For most professional services firms, a quantitative analysis points decisively toward a flat-fee model. It delivers the cost predictability and low expense profile required for managing large B2B payments.

Calculating Your True ACH Transaction Cost

To accurately assess ACH costs, you must calculate your "effective rate"—the all-in cost per transaction after all fees are included. This requires running the numbers against your own transaction data.

Let's model two scenarios for a hypothetical $10M professional services firm to illustrate how fee structures perform under different transaction patterns.

Scenario 1: High-Value, Low-Volume Invoices

Consider a firm issuing 500 invoices per month with an average value of $1,667. This is common for consulting, legal, or specialized engineering firms.

Under a standard flat-fee ACH plan, monthly costs would be:

- Per-Transaction Fee: $0.50 x 500 invoices = $250

- Monthly Platform Fee: A standard gateway access fee = $40

- Batch Fee: A nominal charge for daily batch submission = $5

- Return Fee: A 1% return rate (5 returns) at $5 each = $25

The total monthly ACH cost is $320. The advertised $0.50 fee is actually $0.64 per transaction ($320 / 500). Annually, the cost is $3,840.

This visual highlights the cost differential between payment methods for this firm.

The chart demonstrates ACH's significant cost advantage, explaining its role as a workhorse for B2B payments.

Scenario 2: Low-Value, High-Volume Invoices

Now, consider a firm with the same revenue but a different model: 2,000 monthly invoices averaging $417 each, such as a marketing agency with numerous retainers.

The higher transaction volume alters the calculation:

- Per-Transaction Fee: $0.50 x 2,000 invoices = $1,000

- Monthly Platform Fee: Remains constant = $40

- Batch Fee: A minor cost for daily submission = $5

- Return Fee: A 1% return rate (20 returns) at $5 each = $100

The total monthly cost is $1,145. The effective rate per transaction declines to $0.57 ($1,145 / 2,000), but the total annual cost rises to $13,740. For specific provider examples, this breakdown of the Appfolio transaction fee can be instructive.

The Bottom Line Comparison

The strategic importance becomes clear when comparing ACH costs to alternatives.

If the firm in Scenario 1 processed those 500 payments via credit card at an average rate of 2.9%, the monthly cost would be $24,167. Annually, this totals $290,000. The $3,840 spent on ACH represents a 98.7% cost reduction.

This is a strategic decision impacting working capital. The hidden costs of paper checks, estimated at $4 to $20 per check, further solidify ACH's financial advantage.

Modeling the numbers for your own firm is the first step toward building the business case for a more intelligent payment strategy. To optimize related workflows, review our guide on what is payment reconciliation.

Actionable Strategies to Reduce ACH Processing Fees

Accepting ACH fees as a fixed cost is a missed opportunity. For finance leaders focused on capital efficiency, the objective is to actively manage these costs downward. Several operational and strategic adjustments can significantly lower your effective ACH rate.

This requires managing the how and when of payment processing to eliminate friction and unnecessary charges.

Negotiate from a Position of Strength

Your primary negotiating leverage is your transaction volume and total payment value. Processors seek high-volume, predictable business, which you can use to your advantage.

Enter negotiations prepared with data: average monthly transaction count, total dollar volume, and typical invoice size. A clear, data-backed profile of your payment activity strengthens your position to request lower per-transaction fees or waived monthly charges.

As the payment originator, your firm bears most ACH costs. While already low, there is room for optimization. Within the $93 trillion ACH ecosystem, companies with significant volume can negotiate rates down to the $0.05–$0.30 range. For more context, learn more about the dynamics of ACH fees from Rho.

If your firm processes over 500 transactions monthly or handles multi-million dollar volumes, a rate review is a fiduciary responsibility. If your current provider is inflexible, it is a clear signal to evaluate competitors.

Implement Intelligent Payment Routing

Different payment methods have different costs. Guiding clients toward the most economical option is a powerful strategy. Modern AR software for professional services can automate this with intelligent payment routing.

The technology analyzes transaction value and defaults to the lowest-cost payment method. For a $20,000 invoice, the system can present ACH bank transfer instead of a credit card, saving hundreds of dollars on a single payment.

This subtly influences client behavior without creating friction, aligning their convenience with your financial objectives—a core principle of effective accounts receivable automation.

Minimize Costly Returns with Proactive Controls

ACH returns, costing $2–$5 each, are largely preventable. Each return represents not just a fee, but a cash flow delay and administrative rework. A proactive approach is essential.

Implement these three controls:

- Bank Account Verification: Use a pre-verification service during client onboarding to validate account and routing numbers before initiating a transaction. This prevents errors at the source.

- Automated Payment Reminders: QuickBooks AR automation tools can send reminders 1-2 days before a scheduled debit. This prompt helps clients ensure sufficient funds are available, reducing NSF returns.

- Strategic Batch Processing: If your processor charges per-batch fees, consolidate payments into a single daily batch. This small operational adjustment delivers consistent, incremental savings.

By actively managing these variables, you can systematically reduce your ach payment processing fees. This operational discipline leads directly to a healthier bottom line and more predictable cash flow.

How AR Automation Optimizes Your Total Cost of Getting Paid

A narrow focus on ACH payment processing fees overlooks the larger cost driver: administrative overhead. The hours your finance team spends on manual collections, payment matching, and reconciliation represent a significant, often unmeasured, expense.

Effective cost control means analyzing the entire collections workflow. The total cost of any payment is the transaction fee plus the associated labor. This is where the strategic value of accounts receivable automation becomes apparent.

Embedding payment processing within an automated collections workflow transforms a reactive, high-cost process into a proactive, low-cost system.

Driving Down Direct Costs with Integrated Payments

Modern AR platforms with a client self-service portal change the payment dynamic. Instead of manual outreach, you empower clients with simple, low-cost options that align with your firm's financial goals.

For large invoices, the portal can present a direct bank transfer as the default option. This steers clients away from expensive credit cards without manual intervention, potentially slashing direct processing costs by over 90% on high-value B2B payments.

This transforms the payment experience into a strategic cost-reduction tool. You can explore how to automate accounts receivable to see these workflows in practice.

Eliminating the Manual Cost of Cash Application

A major hidden cost in AR is manual cash application. When a payment arrives, a team member must locate the corresponding invoice in your ERP or accounting system and mark it as paid.

This process is slow, error-prone, and expensive. Every hour an employee spends on this task is a direct operational cost and diverts them from higher-value activities like financial analysis or credit risk management.

True AI AR automation eliminates this. When a client pays via an integrated portal, the system instantly matches the payment to the correct invoice and reconciles it in your general ledger. This is a direct reduction in operational cost and a significant improvement in financial data accuracy.

The result is a leaner, more precise AR process that frees up personnel, reduces human error, and provides a real-time, accurate view of your cash position.

The Impact on DSO and Cash Flow

The ultimate measure of AR efficiency is Days Sales Outstanding (DSO). Every day an invoice remains unpaid, your firm is extending interest-free credit. Reducing DSO has a greater impact on working capital than lowering transaction fees alone.

AR automation directly addresses the root causes of high DSO.

- Automated Reminders: Consistent, systematic follow-ups ensure invoices remain top-of-mind.

- Convenient Payment Options: Offering easy ACH and bank transfers removes friction, accelerating payments.

- Instant Reconciliation: Immediate application provides an up-to-the-minute view of receivables.

By systemizing the collections process, firms consistently achieve a significant reduction in DSO, often by 10–20% or more. This directly accelerates cash flow, improves forecast accuracy, and strengthens the company’s financial position. The savings from lower ACH payment processing fees are just the starting point.

Building a Capital-Efficient Payment System

Controlling ACH payment processing fees is a key component of building a capital-efficient accounts receivable function. For a professional services firm, this system is a competitive advantage that strengthens the balance sheet and enhances operational resilience.

The process begins with data. Before engaging any vendor, thoroughly analyze your transaction patterns: invoice volume, average payment size, and client payment frequency. This data is your primary leverage for negotiation and for selecting a properly aligned fee model.

Visual Idea: A clean, minimalist line chart showing two trend lines. One line, labeled "Manual AR Costs," stays flat and high. The second line, "Automated AR Costs," starts at the same point but trends sharply downward over time. Key milestones are marked: "Reduced DSO," "Lowered Transaction Fees," "Eliminated Manual Entry."

The Role of Intelligent AR Automation

Modern accounts receivable automation creates a guided, low-friction payment path for clients that is also the lowest-cost path for your firm.

An intelligent system can:

- Dynamically Route Payments: Present bank transfers or ACH as the default for larger invoices, steering clients away from high-cost credit card fees.

- Automate Cash Application: Eliminate the hidden labor costs of manual payment matching, lowering your total cost of collections.

- Proactively Reduce Errors: Use instant bank verification and automated reminders to prevent costly returns and the resulting cash flow disruptions.

From Cost Center to Strategic Asset

When implemented correctly, AR transforms from a reactive cost center into a strategic asset that actively improves cash flow. The combination of low-cost payment rails, automated outreach, and precise cash application creates a predictable and efficient system.

By mastering ACH fee structures and embedding payments into an intelligent workflow, you can meaningfully reduce DSO and build a stronger financial operation. For more on financial strategy, our guide on what is receivables financing offers additional perspective.

Frequently Asked Questions

Finance leaders at professional services firms frequently ask the same critical questions about ACH fees and AR automation. Here are the most common.

What Is a Realistic All-In Cost for ACH Processing?

The advertised per-transaction fee of $0.20 to $1.50 is only a starting point. Your true, all-in cost includes that fee plus monthly platform fees ($20–$50), batch processing fees ($1–$5), and any return fees ($2–$5 each).

For a firm processing 500 invoices monthly, the total cost could exceed $400, pushing your effective per-transaction rate above the initial quote. Even so, this is almost always more economical than credit cards.

How Can We Reduce Costly ACH Return Fees?

Proactive prevention is the most effective strategy for reducing return fees. This saves both the fee and the administrative burden of rework.

First, implement a bank account verification service at client onboarding to catch data entry errors. Second, your AR software for professional services should send automated payment reminders before the debit date, prompting clients to ensure funds are available.

When Should We Use Same-Day ACH?

Same-Day ACH is a strategic tool, not an everyday utility. Its premium cost is justified when speed provides a clear financial benefit.

Use it for critical, high-value payments needed to meet month-end cash flow targets or reduce DSO. It is also effective for final invoice settlement. In these cases, the incremental cost is offset by the immediate improvement to your cash position.

How Difficult Is It to Switch ACH Processors?

Switching processors can be complex, primarily due to vendor lock-in, where client payment data is held in a proprietary system.

The solution is to work with an AI AR automation platform that uses payment tokenization. This technology converts sensitive bank data into a secure, non-proprietary token. If you switch providers, you can migrate the tokens without requiring clients to re-enter their information.

The principle is control. With tokenization, you own the client payment relationship, not the processor. This provides the flexibility to negotiate better rates as your firm's volume grows and your leverage increases.

--- Resolut automates AR for professional services—consistent, accurate, and human. Learn more at https://www.resolutai.com.