Cash Flow Issue Playbook for Professional Services

Fix your cash flow issue with our playbook for CFOs. Learn to diagnose problems, improve AR, reduce DSO, and use automation to stabilize your firm's finances.

Revenue can look solid and still leave you short on cash by Friday.

That’s the pattern professional services owners describe when they call in a fractional CFO. Utilization is high. The pipeline is healthy. Clients say they’re happy. Then payroll lands, a tax payment hits, a large invoice is still sitting in someone’s approval queue, and the business feels tight for reasons nobody can explain quickly.

That’s a classic cash flow issue. It isn’t always a sales problem. Often it’s a timing problem, a process problem, or a visibility problem.

A landmark study by Jessica Hagen of U.S. Bank found that 82% of businesses that failed experienced cash flow issues (Preferred CFO). For firm owners, that number matters because it shifts the conversation. The risk usually isn’t that the work has no value. The risk is that cash arrives too late, too unevenly, or with too little warning.

Professional services firms are especially exposed. You fund labor before you collect cash. You often wait until the end of a phase to invoice. Partners want to protect client relationships, so collections get softened or delayed. Meanwhile, payroll, software, and tax obligations stay on schedule.

I’ve seen firms calm this down once they stop treating collections as an awkward afterthought and start treating cash movement as an operating system. If you want a useful parallel, healthcare groups have had to build disciplined workflows around claims, collections, and follow-up for years. That’s one reason resources on Healthcare Revenue Cycle Management can be useful outside healthcare too. The underlying lesson is simple. Cash improves when the process is designed, owned, and measured.

If the symptoms sound familiar, this practical guide on cash flow problems in business is worth keeping open beside your AR aging report.

Introduction The Silent Threat to Profitable Firms

A profitable firm can still feel fragile.

The usual version looks like this. The month closes with a healthy P&L. WIP is strong. New work is signed. Then two large clients pay late, one invoice has a coding error, and a partner asks to hold follow-up because “the client is sensitive.” Cash tightens immediately.

That disconnect creates confusion because the income statement says one thing while the bank account says another.

Practical rule: Profit is an opinion until cash is collected.

The most dangerous part is how ordinary it feels while it’s building. A firm can absorb one delayed payment. It can absorb one weak month of billing discipline. It can usually absorb one project that ran long without a billing milestone. Stack those together, and management starts making defensive decisions. Hiring pauses. Vendor payments slip. Owners delay distributions. The team feels pressure before leadership has named the cause.

That’s why this problem deserves operational attention, not just accounting attention.

What makes services firms vulnerable

Professional services firms sell expertise and time, but they fund delivery up front. Salaries, contractor costs, software, occupancy, and taxes don’t wait for client approval cycles.

A few habits make the problem worse:

- Late invoicing after work is complete because billing depends on partner review

- Loose scope control that delays client sign-off

- Collections handled informally by account leads instead of a disciplined AR process

- Large invoices at project end instead of staged billing throughout delivery

None of this means the firm is unhealthy. It means cash is being managed too far downstream.

What control looks like

Control starts when finance stops asking only, “How much cash is in the bank?” and starts asking better questions.

A short list matters most:

Question | Why it matters |

|---|---|

Are invoices going out immediately? | Billing lag creates avoidable cash lag |

Which clients consistently pay slowly? | Patterns matter more than excuses |

Are terms aligned with how labor is incurred? | Mismatch creates predictable strain |

Can leadership see likely shortfalls early? | Time creates options |

Most owners don’t need a more complicated finance function. They need one that is tighter, faster, and clearer.

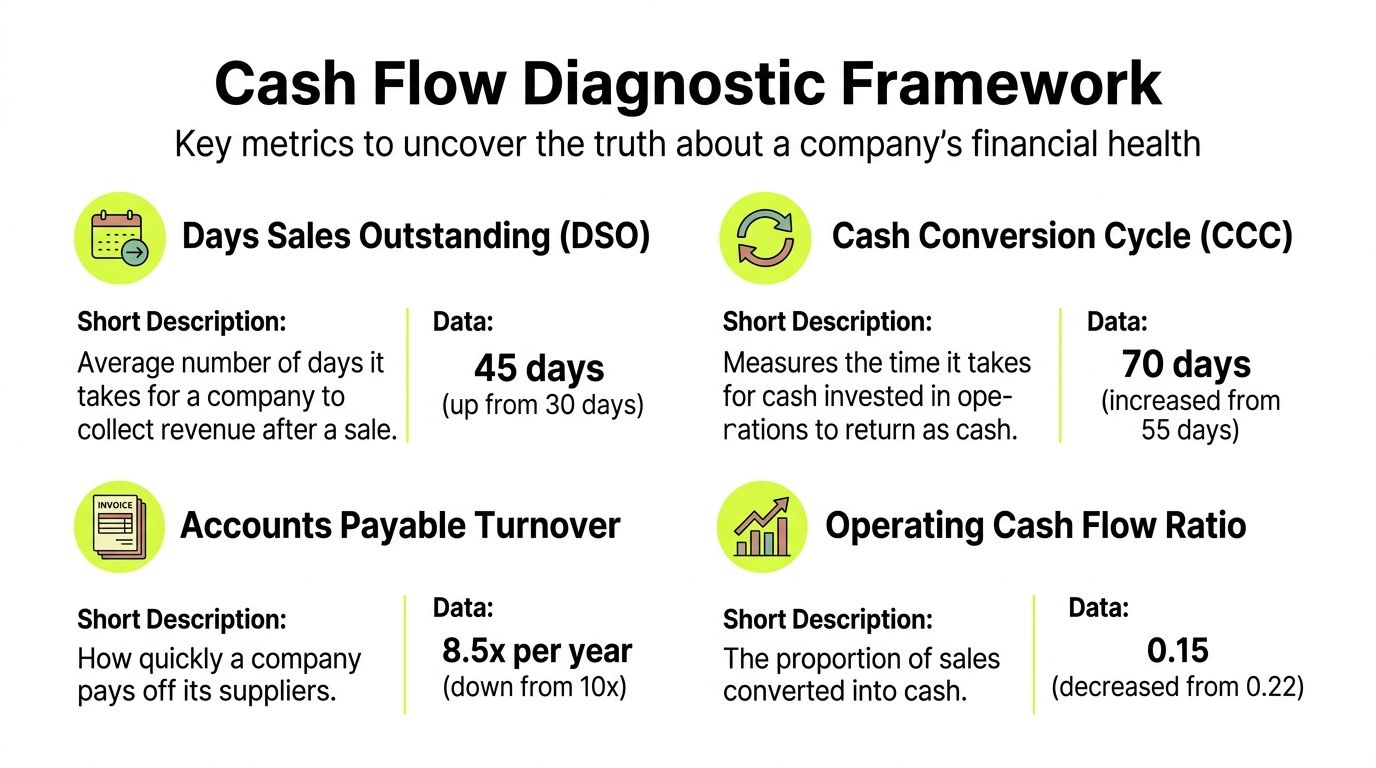

Your Diagnostic Framework Key Metrics to Uncover the Truth

Most firms look at cash too late.

By the time the bank balance feels uncomfortable, the cause has already been sitting in receivables, billing delays, or payment terms for weeks. Diagnosis starts with a small set of operating metrics, not a stack of reports.

Start with DSO

Days Sales Outstanding, or DSO, tells you how long it takes to collect after a sale. In major markets, DSO averages 45 to 60 days (Taulia). For a professional services firm, that range is often enough to create pressure even when revenue looks strong.

The formula is straightforward:

DSO = (Accounts receivable / total credit sales) x days in period

The value of DSO isn’t the formula. It’s the discipline of tracking it every month by client, by partner, and by service line.

A few observations matter:

- Rising DSO with rising revenue usually means growth is consuming cash faster than collections are returning it.

- Stable revenue with rising DSO often points to weak follow-up, invoice disputes, or poor billing timing.

- High DSO concentrated in a few clients is a relationship management issue, not just an AR issue.

If you want a simple refresher on definitions and interpretation, this explanation of https://www.resolutai.com/blog/what-is-dso is useful for teams that need a common language.

Don’t stop at DSO

A services firm should also track the timing gap between paying obligations and collecting from clients. That’s where Days Payable Outstanding, or DPO, and the Cash Conversion Cycle, or CCC, become useful.

DPO tells you how long you take to pay vendors.

The usual formula is:

DPO = (Accounts payable / cost of sales or purchases) x days in period

In a services business, DPO may be less dramatic than in manufacturing, but it still matters when you rely on contractors, software vendors, and outsourced partners. If your clients pay slowly and you pay vendors quickly, cash gets squeezed in the middle.

CCC is the broader timing measure. It tracks how long cash is tied up before it returns to the business. In service firms, inventory is usually low or absent, so the practical lens is simpler. How long after you incur labor and delivery costs do you collect cash?

A healthy services firm can still carry a weak cash cycle if invoicing, approvals, and collections move slower than payroll.

Read the AR aging report like an operator

Most AR aging reports are underused.

Teams glance at the total overdue balance, then jump into reminders. That misses the value. A strong aging review shows where cash gets stuck and why.

Break the report in a few ways:

By aging bucket

Look at current, slightly overdue, and heavily overdue balances separately.

Recent overdue invoices are often the easiest to recover because the work is still fresh and the client relationship is active. Older balances often involve disputes, missing documentation, or low internal ownership.

By client

Some clients pay late once. Others always pay late.

Those are not the same problem. A one-time delay may need follow-up. A habitual pattern may require tighter terms, milestone billing, or stronger pre-bill review.

By partner or account lead

Many firms find the truth in such comparisons.

One partner invoices immediately, confirms receipt, and supports follow-up. Another delays billing, tolerates scope drift, and treats collections as beneath the client relationship. The aging report will show you both behaviors clearly.

Use trend lines, not snapshots

One month of AR data can mislead you.

Three months of movement starts to tell the truth. Watch for these shifts:

- Receivables growing faster than sales

- More invoices slipping from current into overdue

- A concentration of overdue balances in long-running projects

- Repeated re-billing or credit memo activity

Those trends usually point to process defects before they become liquidity events.

Anchor the metrics in cash flow statements

Good diagnostics connect the balance sheet to the cash flow statement.

Controllers who want a clean walk-through can use this guide to understanding your statement of cash flows to align operating performance with actual liquidity movement. That matters because many leadership teams understand margin faster than they understand timing.

Here’s the operating view I use most often:

Metric | What it reveals | Typical concern in services firms |

|---|---|---|

DSO | Collection speed | Invoices are paid too slowly |

DPO | Payment timing to vendors | Outflows happen before inflows |

CCC | Total time cash is tied up | Delivery-to-cash cycle is too long |

AR aging | Where invoices are stalling | Follow-up is inconsistent or late |

What diagnosis should lead to

A diagnostic framework is useful only if it changes behavior.

If DSO is high, the answer usually isn’t “work harder on collections” in the abstract. The answer is narrower. Send invoices faster. Fix approval bottlenecks. Segment clients by payment behavior. Push billing into milestones. Escalate disputes earlier.

The firms that improve cash don’t stare at reports longer. They use the reports to assign ownership.

Immediate Actions to Stabilize Liquidity

When cash is tight, speed matters more than elegance.

You don’t need a transformation plan in the first three days. You need enough liquidity to reduce pressure and enough clarity to stop making rushed decisions.

Pull a live collections list

Start with a same-day list of open invoices, sorted by amount, due date, and client owner.

Then work the list in this order:

- Large recent overdue invoices These are often the fastest path to cash because the work is still top of mind and the client hasn’t yet built a long delay habit around the invoice.

- Invoices with no confirmed receipt Don’t assume the client has the bill, the backup, or the payment instructions. A surprising amount of delay comes from simple handoff failure.

- Accounts with multiple open items Bundle them into one outreach thread. Fragmented follow-up creates confusion and slows payment approval.

- Invoices tied to an unresolved dispute Pull these out and assign a real owner. “Finance is following up” usually doesn’t work if the issue sits with delivery or the relationship lead.

Change the outreach tone

At this stage, collections should be direct and professional.

A simple script works better than a vague nudge:

We’re reviewing open receivables this week and want to confirm status on invoice [number]. Can you confirm receipt, approval status, and expected payment date?

That language does three things. It confirms there’s a specific invoice. It asks for status, not a promise. It pushes for a date.

If a partner insists on handling the conversation personally, finance should still draft the message and require a documented response.

Manage payables deliberately

Cash triage isn’t only about accelerating inflows. It’s also about controlling timing on outflows without damaging trust.

Use a quick review with three categories:

- Critical payables that protect payroll, tax compliance, and essential systems

- Negotiable payables where a vendor relationship is strong enough to support a short extension

- Deferrable spend that can wait without creating downstream cost

Call key vendors early if you need flexibility. Silence does more damage than a direct request.

If you need terms relief, ask before the due date. Vendors react better to a plan than to an excuse.

Freeze nonessential commitments

This isn’t the moment for broad cost-cutting theater.

It is the moment to pause spend that doesn’t affect delivery, collections, or compliance. Delay discretionary software additions, noncritical hiring, and nice-to-have project spend until the short-term picture is clear.

A short freeze creates room to think.

Use financing as a bridge, not a habit

A line of credit can be the right move when timing is the problem and collections are credible.

It’s the wrong move when billing is disorganized and overdue balances have no owner. In that case, debt only masks process failure.

Use short-term financing if it buys time for confirmed receivables to convert. Don’t use it to avoid fixing the receivables process.

Run a simple 14-day cash view

In the middle of a cash flow issue, the annual budget won’t help much.

Build a narrow, practical list:

Next 14 days | Include |

|---|---|

Expected inflows | Client payments with confirmed dates |

Fixed outflows | Payroll, taxes, rent, debt obligations |

Flexible outflows | Vendors that can be rescheduled |

Decision items | Payments that need owner approval |

This gives leadership a realistic view of what must happen now, not what should happen eventually.

Systemic Fixes for Your Accounts Receivable Process

Temporary collection pushes help, but they don’t solve the underlying problem.

In professional services, recurring cash stress usually starts upstream. It starts when invoicing is delayed, when project structure doesn’t support billing, when account leads treat collections as optional, or when nobody owns the handoff from delivery to cash.

Fix invoicing hygiene first

Most firms with chronic AR friction don’t need more effort. They need cleaner execution.

That starts with invoicing hygiene:

- Send invoices immediately after milestone completion rather than waiting for a month-end batch.

- Make backup documentation easy to review so the client approver doesn’t have to request it separately.

- Use consistent invoice descriptions that match the statement of work and the client’s purchase process.

- Confirm the right billing contact and submission path before the invoice goes out.

A technically correct invoice can still be hard to pay if the client has to decode it.

Stop waiting until the end of the project

This is one of the biggest structural mistakes in services firms.

Long projects consume labor steadily, but many firms still bill too much at the back end. That creates a funding gap the business has to absorb.

For 2025 to 2026 projections, professional services firms with long project timelines face sharper cash flow gaps because labor is incurred up front while clients stretch payments to 60 to 90+ days. The same analysis notes that milestone-based invoicing tied to AI-driven risk assessment can significantly shorten the cash conversion cycle (CapFlow Funding).

That projection fits what operators already know. End-loaded billing creates avoidable strain.

Better billing structures for services firms

Project type | Weak billing structure | Stronger billing structure |

|---|---|---|

Advisory retainer | Invoice after month-end review | Invoice at period start or fixed monthly cadence |

Long implementation | Large final invoice | Stage billing by milestone or phase |

Time and materials | Delayed internal approval before billing | Weekly or twice-monthly billing cycle |

Strategy project | Billing after final deck delivery | Deposit plus scheduled milestone invoices |

Build a collections cadence that doesn’t depend on memory

Many firms think they have a collections process when they really have a few reminders sent by whoever has time.

That isn’t a system.

A functioning cadence has:

Clear timing

Decide exactly when outreach happens before due date, on due date, and after due date. If every collector improvises, clients learn that your process is negotiable.

Defined ownership

Finance can own the sequence, but relationship leads must own dispute resolution and executive escalation. If those roles are blurred, invoices sit in limbo.

Standard language

Not every message should sound the same, but the structure should be consistent. Confirm invoice receipt. Confirm approval status. Request payment timing. Escalate when needed.

Clients rarely object to professional follow-up. They object to confusion, inconsistency, and surprises.

Tighten client acceptance and scope control

A hidden AR problem sits inside project delivery.

When deliverables aren’t clearly accepted, invoices become negotiable. When scope changes aren’t documented, the client disputes timing or amount. Finance sees a receivable problem, but the cause began in delivery governance.

A few practical controls help:

- Written milestone acceptance

- Documented change orders

- Pre-bill review focused on client readiness, not just formatting

- A rule that billing can’t be held indefinitely for relationship reasons

That last point matters. Protecting the relationship by delaying hard conversations usually hurts the relationship later, when balances are older and options are narrower.

Match terms to economic reality

Payment terms need to reflect how the firm incurs cost.

If you pay employees every two weeks and a client pays in a long cycle, you need structure that narrows the gap. That may mean deposits, milestone invoices, retainers, or stricter terms for custom work.

Not every client will agree. That’s the trade-off.

But many firms make the mistake of never asking. They finance the client by default, then wonder why growth creates strain.

What doesn’t work

Some common habits feel polite but create repeat cash problems:

- Sending invoices in batches because that’s how it’s always been done

- Letting partners hold invoices without a deadline

- Treating every late payment as a one-off

- Waiting for month-end to review AR

- Escalating only after a balance has become old and contentious

These practices don’t preserve relationships. They transfer risk from the client to your business.

Accelerating Cash Flow with AR Automation and AI

Manual AR can work for a small book of business.

It breaks down once invoice volume grows, approval chains get more complex, or client behavior varies across accounts. At that point, finance spends too much time chasing status, matching payments, and rewriting the same reminders.

What accounts receivable automation actually changes

Good accounts receivable automation doesn’t just send reminders.

It standardizes timing, centralizes account history, reduces follow-up gaps, and removes the dependence on someone remembering who to contact next. That matters in professional services because client communication needs to stay consistent without becoming robotic.

A practical system should handle:

- Invoice delivery and confirmation

- Scheduled reminders based on due date and risk

- Shared visibility across finance and account teams

- Payment links and easy settlement options

- Cash application and reconciliation support

That’s where AR software for professional services starts to pay off. It shortens the lag between completed work and usable cash by reducing friction on both sides of the transaction.

AI AR automation is useful when it changes priority

The strongest use of AI AR automation isn’t flashy. It’s operational.

If the system can identify which invoices are most likely to slip, finance can intervene earlier. If it can flag unusual payment behavior or route accounts into different follow-up paths, the team spends less time treating every invoice the same way.

That’s the difference between basic reminders and orchestration.

For firms already working inside accounting systems, QuickBooks AR automation can be a practical first step if it improves invoice timing and follow-up discipline. But once collections, risk signals, approval friction, and cash application start to sprawl across email, spreadsheets, and team handoffs, a broader AR workflow platform usually makes more sense.

One useful reference on process benefits is https://www.resolutai.com/blog/accounts-receivable-automation-benefits.

Payment friction is still a collections problem

A client may intend to pay and still delay because the payment path is clumsy.

That’s why portal design matters. If the approver can’t find the invoice, doesn’t have backup, or has limited payment options, cash slows for reasons that have nothing to do with willingness.

A good AR experience removes those obstacles. Clients should be able to view the invoice, understand what it covers, and pay through a straightforward channel without unnecessary back-and-forth.

This short overview is useful before evaluating platforms:

Technology should support relationships, not replace them

A common concern from partners is that automation feels impersonal.

That’s true if the system is blunt. It isn’t true if the workflow reflects account context. High-value relationships often need a different cadence, tone, or escalation path than smaller transactional accounts. Good tools let finance automate the routine while preserving human judgment where it matters.

The goal isn’t to remove people from collections. It’s to remove manual drift from the process.

One example is Resolut, which combines AI-driven collections workflows, risk identification, payment orchestration, and automated cash application in one AR process. For firms trying to reduce DSO and improve cash flow, that kind of setup is most useful when finance wants consistency without losing control over account-level decisions.

What to look for in a platform

If you’re evaluating software, focus on operating fit.

Capability | Why it matters in professional services |

|---|---|

Workflow automation | Keeps follow-up on schedule without relying on memory |

Client segmentation | Treats strategic accounts differently from routine accounts |

Payment portal | Reduces friction at the moment of payment |

Cash application | Speeds accurate visibility into collected cash |

Risk flags | Helps teams act before invoices become seriously late |

The test is simple. If the tool reduces manual handoffs, improves visibility, and makes payment easier for the client, it’s helping. If it mainly adds another dashboard, it probably won’t move cash.

Building a Proactive Cash Management Culture

A firm doesn’t get stable cash flow from one cleanup effort.

It gets stable cash flow when cash discipline becomes part of how the business operates every week. That requires forecasting, clearer ownership, and a culture where booked revenue is not treated as the finish line.

Forecasting needs to be operational

Insufficient revenue forecasting is a primary cause of cash flow issues in growing firms, and weak monthly closes plus overly optimistic projections can lead to hiring and inventory mistakes while undermining investor confidence. The same source argues that real-time AR visibility is more critical than revenue volume for stability (Brex).

For a professional services firm, that means the forecast can’t live only in sales assumptions. It has to reflect when invoices will be sent and when cash is likely to arrive.

Build a rolling 13-week cash view

A rolling forecast works because it’s close enough to drive action.

Use a weekly view with these lines:

- Beginning cash

- Expected collections

- Payroll and contractor outflows

- Tax payments

- Rent, software, and debt service

- Owner distributions or discretionary spend

- Ending cash

- Key assumptions and risks

Then refresh it every week. Don’t wait for month-end.

What belongs in the assumptions line

Detailed annotation improves forecast quality.

Instead of listing “AR collections” as one lump, annotate the major expected receipts with practical notes such as pending approval, client confirmed payment date, invoice dispute open, or partner escalation needed. That turns the forecast into a management tool rather than a spreadsheet ritual.

Assign cash ownership beyond finance

Finance can run the process, but it can’t carry the culture alone.

The strongest firms align cash ownership across roles:

Role | Cash responsibility |

|---|---|

Partner or owner | Support billing discipline and client escalation |

Project lead | Confirm milestones and acceptance quickly |

Controller | Maintain visibility, aging discipline, and forecast accuracy |

AR team | Execute follow-up cadence and document status |

Sales or account lead | Set terms that the business can carry |

If sales celebrates signed work while finance absorbs the collection risk, the business creates tension by design.

Review client concentration and payment behavior

A proactive culture also pays attention to who creates exposure.

Ask a few questions regularly:

- Does one client represent too much of expected near-term cash?

- Which accounts repeatedly pay late despite strong revenue contribution?

- Are new clients getting terms before credit discipline is discussed?

- Are relationship leads overriding collections rules too often?

These are commercial decisions with cash consequences.

A healthy client isn’t just one who buys. It’s one who pays in a pattern the firm can sustain.

Tighten the monthly close

Weak closes create blind spots.

If revenue is booked but WIP, billing status, and receivables quality are still unclear deep into the next month, leadership ends up steering from stale information. A better close links three things quickly: what was delivered, what was billed, and what is likely to convert to cash.

That’s also where recurring process failures become visible. If the same accounts need manual explanation every close, the firm has a workflow problem that accounting alone won’t fix.

Make cash part of operating rhythm

This doesn’t need to be dramatic.

A short weekly review can be enough if it covers:

- open invoices that need action

- upcoming cash pressure points

- billing delays by owner

- disputed balances

- forecast changes that affect hiring or spending

Once that rhythm is in place, the firm stops reacting to surprises and starts seeing them earlier.

Conclusion From Reactive Measures to Financial Control

A persistent cash flow issue usually follows a predictable pattern. Billing slips. Collections lose cadence. Visibility weakens. Leadership responds late.

The fix is also predictable. Diagnose the timing problem. Stabilize liquidity. Repair the AR process. Use automation where manual work is slowing cash. Forecast tightly enough to act early.

Professional services firms don’t need perfect certainty. They need better control.

Resolut automates AR for professional services with a practical focus on consistency, accuracy, and human follow-up. If your team is trying to improve cash flow, reduce DSO, or bring more discipline to collections without making the client experience worse, you can learn more at Resolut.