Small Business Credit Risk Management: A Playbook

Master small business credit risk management. Our playbook helps CFOs reduce DSO, improve cash flow, and automate AR for professional services firms.

A client doesn’t have to go bankrupt to create a cash crisis for your firm. They only have to pay late, dispute a bill at the wrong time, or keep promising that payment will go out “next week.”

If you run finance for a professional services firm, you know the pattern. Revenue looks healthy. WIP is moving. The pipeline is solid. But one large receivable slips past terms, two smaller accounts follow it, and suddenly payroll timing, partner distributions, hiring plans, and your own borrowing needs all get tighter than they should.

That’s why small business credit risk management matters more than most firms admit. It isn’t just a lending topic. It sits inside daily operations. It affects who you take on, what terms you offer, how invoices go out, how quickly your team intervenes, and whether cash arrives when the P&L says it should.

Beyond Bad Debt A New Model for Credit Risk

Most firms still treat credit risk as a one-time check at onboarding. They look at the client, make a judgment call, set terms, and move on. That approach breaks down fast in professional services, where work often starts before the full commercial risk is clear.

A familiar example is the strategic client who always pays, until they don’t. The first late invoice gets explained away. The second becomes a collections exception because the partner owns the relationship. By the time finance is pulled in, the firm is funding the client’s working capital.

That isn’t bad luck. It’s a control issue.

According to the Federal Reserve’s 2024 Small Business Credit Survey, 59% of employer firms sought new financing in the past 12 months, but only 41% received the full amount requested, with nearly one-quarter denied all financing. High-risk firms were significantly more likely to be denied or receive only partial funding (Federal Reserve data summarized by Nav). For small firms, weak risk discipline doesn’t just create bad debt exposure. It can also limit access to outside capital when cash tightens.

Credit risk starts long before write-off. It shows up first in slower collections, heavier exceptions, rising partner intervention, and growing dependence on short-term cash fixes.

A better model treats risk as continuous, not binary. The question isn’t only whether a client is creditworthy at engagement. The question is whether their behavior, billing pattern, organization changes, and payment habits still support the amount of unsecured exposure you’re carrying today.

In practice, that shifts the finance team from reacting to overdue balances to managing a live portfolio. Some clients can handle open terms without much oversight. Others need retainers, milestone billing, tighter follow-up, or more senior review before additional work is released.

That’s the playbook. Policy first. Then disciplined assessment. Then a collections system that acts early, consistently, and without drama.

Establishing Your Foundation The Credit Policy

A firm without a written credit policy doesn’t have a credit function. It has a series of exceptions.

That might sound harsh, but it’s how most receivables problems start. Sales wants flexibility. Partners want to protect relationships. Operations wants the work moving. Finance gets involved after the account is already aging.

A credit policy fixes that by making risk decisions explicit. It gives your team a common language for retainers, payment terms, credit limits, invoice release, escalation, and work stoppage. It also creates consistency. That matters because research shows that organizations using structured credit management tools report default rates of 25% versus 50% for businesses without them, a 50% reduction in defaults (credit management research).

What the policy needs to settle

Start with your firm’s risk appetite. Not in abstract terms. In operating terms.

Ask questions like these:

- Client mix: Are you serving established companies with formal AP processes, or founder-led businesses where payment depends on one owner’s cash position?

- Service model: Are engagements project-based, monthly recurring, or success-fee driven?

- Tolerance for unsecured exposure: How much unbilled or unpaid work are you willing to carry before finance approval is required?

- Authority lines: Who can approve exceptions, and who can’t?

If those decisions live in hallway conversations, they won’t hold under pressure.

Core Components of a Professional Services Credit Policy

Component | Objective & Key Details |

|---|---|

Credit mission | Define the balance between growth and cash protection. A strong version states that the firm extends credit to support profitable client relationships, but only within documented limits and review rules. |

Approval authority | Set clear decision rights for standard terms, elevated limits, exceptions, and account holds. Partner preference should not override documented approvals without visible sign-off. |

Client onboarding requirements | Specify what finance needs before terms are granted. This may include legal entity name, billing contacts, tax details, references, signed engagement terms, and deposit requirements. |

Payment terms | Standardize baseline terms such as due on receipt, retainer-based billing, milestone billing, or Net 30 where appropriate. Don’t let every engagement team invent its own structure. |

Credit limits | Cap unsecured exposure by client based on assessed risk, engagement type, and expected billings. Tie future work release to those limits. |

Retainer rules | State when retainers are mandatory, how they’re applied, and when they must be replenished before additional work begins. |

Invoicing standards | Require complete invoices, correct PO or matter references, named client contacts, and prompt delivery. A weak invoice is a collections problem created upstream. |

Collections cadence | Define reminder timing, escalation sequence, call ownership, dispute handling, and when an account moves to hold status. |

Stop-work triggers | Establish objective triggers for pausing new work or deliverables. This protects finance from negotiating account by account under stress. |

Legal escalation | Document when outside counsel, demand letters, or formal recovery channels are appropriate. |

Review cycle | Require periodic review so the policy reflects actual client behavior, not last year’s assumptions. |

Practical term design for service firms

Professional services firms usually need more than one billing model. One rule for everyone sounds fair, but it often creates the wrong exposure.

A sensible structure often looks like this:

- New or thin-file clients: Use an upfront retainer or deposit before work starts.

- Defined-scope projects: Bill by milestone, not only at the end.

- Long-running advisory work: Consider monthly billing with short terms and fast dispute windows.

- Large strategic accounts: Offer open terms only if invoicing discipline and payment behavior justify it.

Practical rule: If the work is hard to repossess after delivery, credit discipline has to be stronger before delivery.

There’s also a governance benefit. A written policy reduces internal friction because finance stops looking arbitrary. The team can point to a documented framework instead of sounding like the department that always says no.

For firms still tightening their legal and operating foundation, this is also the stage where entity structure and contracting discipline matter. If you’re cleaning up basics, the Ontario business incorporation guide is a useful reference for understanding how legal setup and governance decisions affect commercial operations.

What doesn’t work

Three patterns fail almost every time.

- Relationship-only underwriting: If the partner likes the client, the client gets terms. That’s not underwriting. That’s delegation of credit to sales.

- Hidden exceptions: Teams negotiate side terms in email, then AP pays against what they remember, not what finance approved.

- Collections without policy backing: If the collector can’t enforce a hold, a deposit requirement, or a revised term, they’re sending reminders without enforcement power.

A good policy isn’t rigid. It’s controlled. You can allow exceptions. You just force them into the light.

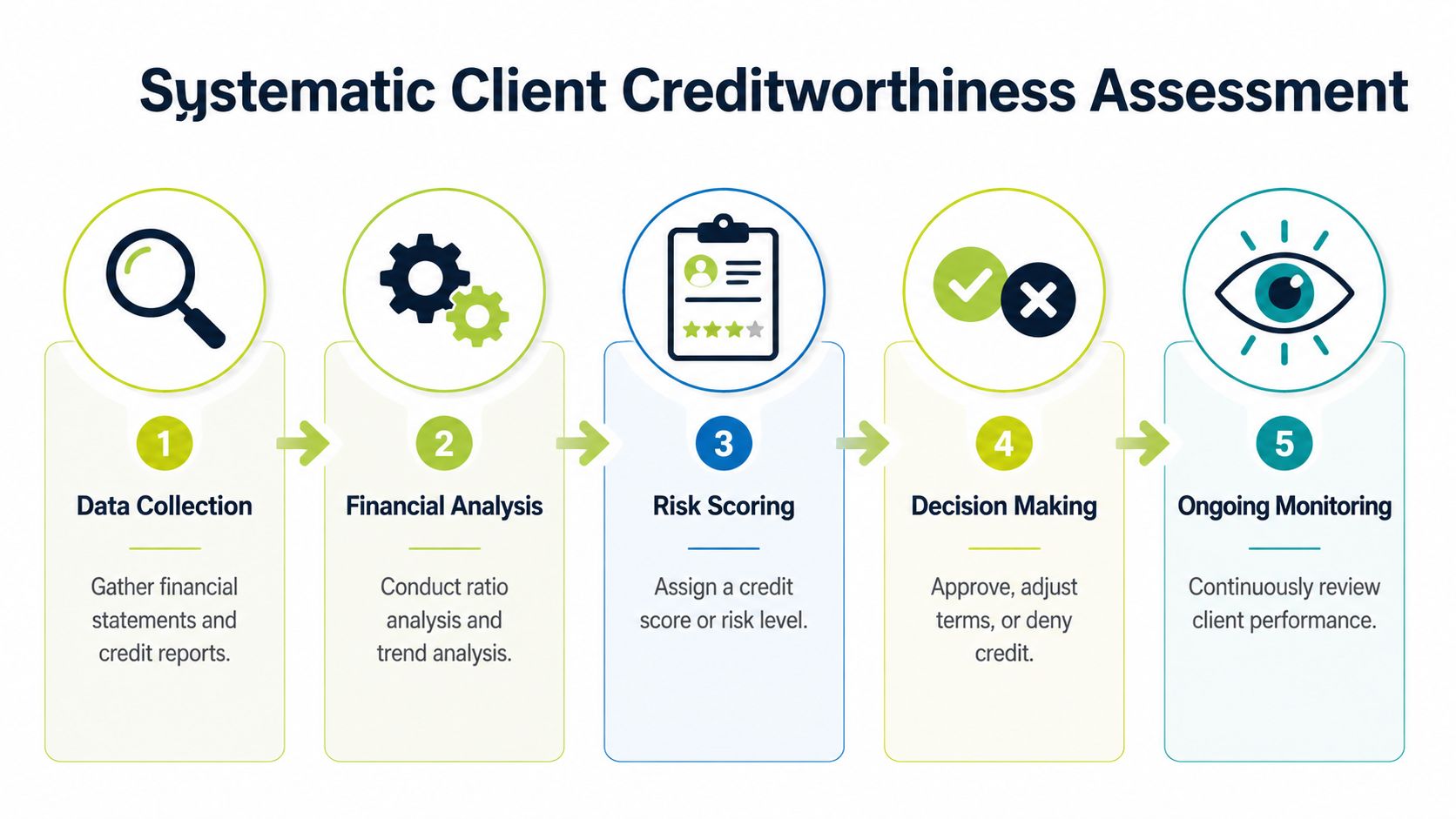

Systematic Client Creditworthiness Assessment

Once the policy is written, the next question is simple. How do you decide what any one client should receive?

At this point, many firms drift back into instinct. They rely on brand recognition, partner confidence, or the fact that a prospect “sounds organized.” That can work for a while. It doesn’t scale, and it doesn’t hold up when the account turns.

A better approach is a repeatable assessment process that produces a documented decision. Not a perfect prediction. A defensible one.

Start with the application, not the handshake

A proper client credit application should collect enough information to answer four things: who the legal counterparty is, who controls payment, what financial signals are available, and how much exposure you may carry.

For most service firms, that means gathering:

- Legal and billing identity: Full legal name, registered address, billing address, tax details, and AP contact.

- Operating contacts: The person approving work, the person approving invoices, and the person releasing payment.

- Commercial details: Expected monthly billings, contract value, service start date, PO requirements, and payment term requests.

- References and history: Trade references, prior work history, and any prior dispute pattern your own team knows about.

If the client is a small private company and formal business records are thin, owner information may matter more than firms like to admit. Research on default prediction found that integrating personal credit data with business-level variables improves predictive accuracy by over 6.4%, with AUROC moving from about 0.78 for business-only models to over 0.83, and personal credit attributes ranking among the strongest predictors (machine learning credit risk findings).

That doesn’t mean every professional services firm should run advanced models in-house. It does mean weak-file clients require more than a logo and a verbal promise.

Use a simple internal scorecard

Most firms don’t need a complex rating engine. They need a short, practical scorecard that creates consistent decisions.

A workable internal model can rate clients across a few dimensions:

Assessment area | What finance should look for |

|---|---|

Entity strength | Is this an established operating entity with clear billing controls, or a newly formed business with thin operating history? |

Payment process maturity | Does the client have a defined AP process, purchase order rules, and named approvers, or does payment depend on one overloaded executive? |

Exposure size | How large will your unpaid balance get relative to the client relationship and engagement structure? |

Information quality | Are financial and reference details complete, verified, and consistent? |

Behavioral indicators | Did the client negotiate terms reasonably, return documents promptly, and align on billing mechanics before work began? |

From there, assign internal tiers such as low, medium, and high risk. The label matters less than what it triggers.

For example:

- Low risk: Open terms may be acceptable within a preset limit.

- Medium risk: Lower credit limit, tighter review, and milestone billing.

- High risk: Retainer, shorter billing cycles, or no unsecured exposure.

This is also where educational alignment helps. If commercial teams still treat “creditworthy” as a vague impression, a practical explainer like this overview of what credit worthiness means in B2B terms can help get sales, finance, and client service onto the same page.

Don’t score clients to create paperwork. Score them so the next decision is automatic.

Match terms to risk, not to persuasion

The mistake I see most often is giving terms first and trying to manage risk later. Terms should come out of the assessment.

Here’s what that looks like in practice:

- Set the initial credit limit based on expected invoice volume and the maximum balance you’re willing to leave unsecured.

- Choose the billing rhythm that reduces exposure. Monthly billing works for stable accounts. Milestones work better when scope or client funding is less predictable.

- Define the trigger for review before balances drift. If unpaid exposure hits the limit, new work should require approval.

- Document any exception in one place, with owner and expiry.

That last point is important. Permanent exceptions usually start life as temporary accommodations.

What trade references can and can’t do

Trade references are useful, but only if someone checks them and asks operational questions.

Don’t ask, “Are they a good customer?” Ask:

- Do they pay within agreed terms?

- Do they dispute invoices frequently?

- Has their payment pattern changed recently?

- Did you reduce or tighten exposure at any point?

References are one input. They shouldn’t outweigh obvious risk signals such as unclear billing authority, resistance to deposits, or repeated pressure for looser terms before the relationship has earned them.

Reassess after the first invoices

Initial assessment is only the opening view. The first few invoices tell you whether the client’s stated process matches reality.

Watch for these signs:

- Invoice routing confusion: Nobody knows who approves payment.

- PO friction: The client requires controls they never disclosed.

- Dispute behavior: Questions appear only after due date approaches.

- Partial payment habits: They pay selectively without explanation.

Those aren’t just collections annoyances. They are credit signals.

A disciplined small business credit risk management process treats onboarding as provisional until actual payment behavior confirms the original decision.

Designing a Proactive Collections Workflow

Most firms don’t have a collections problem. They have a workflow problem.

Invoices go out late. Reminder timing depends on who notices. Follow-up tone varies by collector. Partners intervene inconsistently. Finance spends too much time deciding what to say instead of deciding what action to take.

That reactive model usually hurts both cash flow and relationships. Clients get either silence or sudden escalation. Neither feels professional.

The invoice has to do its job first

Collections starts with invoice quality. A perfect collections cadence can’t rescue a weak invoice.

For professional services, the invoice should be easy for the client’s AP team to approve without a side conversation. That means:

- Clear service description: Enough detail to support approval, without reading like a time dump.

- Correct references: PO number, matter number, project code, or engagement identifier if the client uses them.

- Named contact path: AP contact plus operational sponsor when needed.

- Clean math and dates: Errors create delay and destroy your credibility on follow-up.

- Simple payment options: The easier it is to pay, the fewer excuses survive.

If your team is still debating whether invoice language sounds too firm, it helps to separate tone from structure. The note can stay courteous. The invoice still needs precision.

Build a fixed outreach cadence

A strong collections workflow shouldn’t depend on memory. It should run on dates, status changes, and account rules.

A practical cadence often looks like this:

Timing | Message purpose | Owner |

|---|---|---|

Before due date | Confirm receipt and surface issues early | Automated reminder |

Due date | Prompt action while the invoice is still current | Automated reminder |

Early past due | Ask for status and expected payment date | Automated outreach with reply path |

Continued past due | Escalate tone, confirm commitment, flag risk of hold | Collector or AR lead |

Serious delinquency | Direct call, partner involvement, hold review, legal review if needed | Finance leadership |

The point isn’t aggression. It’s consistency.

Clients rarely object to organized follow-up. They object to confusion, mixed messages, and reminders that arrive after the issue has already become embarrassing.

Keep the wording professional and short

Reminder language should match the stage of the account. The mistake is jumping from overly soft to overly sharp.

Here are concise examples.

Pre-due reminder

Subject: Invoice receipt and scheduled payment Hi [Name], sharing a quick reminder that invoice [number] is coming due on [date]. Please let us know if any documentation is needed on your side to keep payment on schedule.

Due-date note

Subject: Invoice due today Hi [Name], invoice [number] is due today. Sending this over in case it helps your AP queue. Please confirm the scheduled payment date when convenient.

Early past due

Subject: Follow-up on overdue invoice Hi [Name], invoice [number] is now past due. Can you confirm status and expected payment date? If there’s an approval issue, we’d like to clear it quickly.

Escalation

Subject: Action needed on overdue balance Hi [Name], we haven’t received payment or a confirmed payment date for invoice [number]. Please respond today with status. If needed, we can review the balance together and confirm the next step.

For teams that want a cleaner framework for tone, subject lines, and follow-up phrasing, the ReachInbox email reminder tips are useful as a communication reference.

Automation handles repetition. Humans handle exceptions.

Many controllers hesitate, worrying that automation will make collections feel cold.

In practice, the opposite happens when it’s designed well. Automation handles routine reminders on time, every time. That frees the finance team to make better human interventions where they matter.

Use people for the moments that require judgment:

- Strategic client calls

- Dispute resolution

- Temporary payment arrangements

- Partner coordination

- Hold or stop-work decisions

Use automation for the things that should never be missed:

- Reminder timing

- Status nudges

- Promise-to-pay tracking

- Aging-based escalation

- Documentation of outreach

If your staff is still making live calls without a standard script, this collections call script guide is a useful baseline for keeping calls firm, clear, and non-combative.

What usually goes wrong

Three failure points show up repeatedly in service firms.

- Finance waits too long to engage: By the time AR reaches out, the client has learned that your due dates are flexible.

- Partners override process: They ask finance to “hold off for now” without resetting the risk.

- Disputes and nonpayment get mixed together: A true dispute needs resolution. A stalling tactic needs a deadline.

A proactive workflow doesn’t eliminate late payment. It stops late payment from turning into unmanaged exposure.

Leveraging AI Automation for Early Warning and Recovery

Static credit checks were built for a slower operating model. You reviewed a client, set terms, sent invoices, and waited to see what happened.

That isn’t enough now. Risk changes while work is underway. Payment behavior changes before balances become seriously aged. The primary opportunity in accounts receivable automation and AI AR automation is that finance no longer has to wait for an invoice to become visibly late before acting.

What changes when risk is monitored in real time

The biggest shift is moving from customer-level judgment to invoice-level signal detection.

AI-driven real-time credit risk assessment integrated into AR management can predict and mitigate invoice-level risks early. That matters because traditional strategies often focus on static customer assessment instead of dynamic receivables behavior. The gap is especially costly in a market where low-credit-risk firms see 76-83% bank approval rates while high-risk firms are under 50%, pushing many toward more expensive alternatives (AI-driven risk assessment in AR).

For a professional services firm, that means the system can flag risk patterns such as:

- A client who starts opening invoices later

- Repeated short payments or partial remittances

- Promises to pay that slip without explanation

- A growing mismatch between current work and unpaid exposure

- A sudden increase in dispute frequency

None of those signals alone proves default risk. Together, they tell finance where to intervene before the account rolls deep into aging.

AI is only useful if it changes workflow

Finance teams sometimes overestimate technology and underestimate process. A dashboard that says “high risk” doesn’t fix cash flow by itself.

The system has to trigger action. In practice, effective AR software for professional services should connect risk signals to concrete workflow decisions such as:

Signal | Operational response |

|---|---|

Payment behavior deteriorates | Tighten reminder cadence and review open exposure |

Invoice likely to slip | Start outreach earlier, before formal delinquency |

Exposure exceeds comfort level | Route to finance for term review or retainer request |

Strategic client shows stress | Move from automated reminders to direct account outreach |

Repeat friction appears | Coordinate finance, delivery, and account leadership before more work is released |

That’s the part many firms miss. Good automation doesn’t replace judgment. It tells the right person where judgment is needed.

Integration matters more than feature count

A lot of teams end up with one tool for invoicing, another for reminders, a spreadsheet for disputes, and a separate view for collections notes. That setup creates delay because nobody trusts one source of truth.

For firms that run on QuickBooks, QuickBooks AR automation thereby becomes practical rather than theoretical. The win isn’t just fewer manual reminders. The win is that billing status, outreach history, payment activity, and account risk are visible together, so your team can respond without reconciling five systems first.

If you’re evaluating platform architecture, this overview of a receivable management system is a useful way to think about the operating model, not just the software category.

The finance team doesn’t need more alerts. It needs fewer blind spots and clearer next actions.

A helpful outside perspective on the broader operating model is this guide to AI in financial risk assessment, especially for teams trying to understand where predictive analysis fits inside day-to-day finance controls.

What the tooling should actually do

When finance leaders say they want automation, they often mean different things. Some want dunning emails. Others want cash application. Others want risk scoring.

The more useful view is end-to-end control. A modern setup should support:

- Risk identification tied to actual receivables behavior

- Automated outreach across the channels your clients will respond to

- Payment flexibility so the client can move from reminder to payment without friction

- Cash application visibility so collections effort isn’t wasted on balances already in motion

- Escalation rules for holds, legal review, or leadership involvement

Here’s a useful walkthrough of how that looks in practice:

One option in this category is Resolut, which combines credit risk assessment, collections workflow, omnichannel outreach, payment options, and cash application in one AR operating system for firms that want tighter control without running the process manually.

What works and what doesn’t

What works is targeted automation with human review points. Let the system detect signals, launch routine outreach, and surface exceptions. Let finance decide when to revise terms, involve the relationship owner, or pause exposure.

What doesn’t work is bolting generic reminder software onto a messy process and calling it transformation. If invoice quality is weak, ownership is unclear, and exceptions aren’t documented, AI won’t save the workflow. It will only make the disorder run faster.

For firms trying to reduce DSO and improve cash flow, the best use of AI AR automation is practical. Earlier signals. Faster intervention. Better prioritization. Less time spent guessing which account needs attention first.

KPIs Escalation and Continuous Improvement

If you can’t see the portfolio clearly, you can’t control it. Credit risk management becomes real when it shows up in a small set of operating measures that people review regularly and act on.

This is one reason the category keeps expanding. The Credit Risk Assessment Market is projected to grow from USD 9.52 billion in 2025 to USD 23.97 billion by 2032 at a 14.1% CAGR, driven by high lending volumes and demand for AI-enhanced frameworks to analyze dynamic credit data (credit risk assessment market projection). The demand makes sense. Finance teams want faster decisions, clearer visibility, and fewer surprises.

The dashboard I’d want on one screen

For a professional services firm, the most useful AR dashboard is not the busiest one. It should show enough to answer three questions quickly:

- Are we getting paid when expected?

- Which accounts need intervention now?

- Is our process improving or drifting?

A practical dashboard usually includes:

- DSO: Your broad measure of how quickly receivables convert to cash.

- CEI: A better read on how effectively the team collects what became due in the period.

- Average Days Delinquent: Useful for separating true lateness from volume effects.

- Aging by client and partner owner: So concentration risk is visible.

- Promise-to-pay status: Because a promised payment is not cash.

- Dispute queue: Open amount, owner, and age of unresolved disputes.

- Credit limit exceptions: Accounts operating outside approved bounds.

- Collection activity coverage: Which overdue accounts have had recent action and which have not.

Review by exception, not by anecdote

The monthly AR review shouldn’t turn into a storytelling session where each relationship owner explains why their client is special.

Run it by exception. Put the outliers in front of the room.

A disciplined review asks:

Review area | Decision question |

|---|---|

Rising delinquency | Is this a temporary slip or a pattern that requires tighter terms? |

Repeated disputes | Do we have a billing quality issue, a scope issue, or a stalling issue? |

Exposure concentration | Are we carrying too much unsecured balance with one client or one partner book? |

Broken promises to pay | Do we escalate, hold work, or move to leadership intervention? |

Exception accounts | Should the exception remain, expire, or be reversed? |

That style of review changes behavior. It keeps the conversation tied to controls and outcomes, not optimism.

A late account becomes dangerous when it stays in “monitor closely” status for multiple review cycles without a named next action.

Escalation should feel procedural, not personal

Firms get into trouble when escalation feels emotional. Either they avoid it too long because they don’t want to damage the relationship, or they escalate abruptly because patience has run out.

A better approach is a predefined path.

- Stage one: Standard reminder cadence and collector follow-up.

- Stage two: Direct outreach from AR lead or controller. Confirm payment date and reason for delay.

- Stage three: Involve the relationship owner and decide whether future work should continue.

- Stage four: Formal notice, outside collections review, or legal counsel involvement where appropriate.

That sequence protects the relationship because the client experiences a clear process rather than random pressure.

Feed the results back into policy

Continuous improvement is where most firms leave value on the table. They track DSO, discuss the aging, and move on. The better move is to use portfolio results to update the original policy.

If a client segment consistently disputes time-detail invoices, change the invoice design. If a service line repeatedly needs deposits to stay current, make that standard. If a partner’s book produces a disproportionate share of exceptions, the issue probably isn’t collections. It’s front-end credit discipline.

Small business credit risk management works when the loop closes. Policy drives assessment. Assessment sets terms. Terms shape collections. Collections data rewrites policy.

Conclusion From Risk Management to Financial Control

The firms that manage receivables well usually don’t look dramatic from the outside. They look organized.

They have a written credit policy. They assess clients systematically. They match terms to risk. They run a proactive collections cadence. They use automation where consistency matters and judgment where relationships matter. Then they measure the portfolio and adjust.

That’s the shift. Small business credit risk management stops being an administrative side task and becomes part of financial control.

For CFOs, controllers, and firm owners, that control shows up in practical ways. Fewer surprises in the aging. Fewer internal debates about exceptions. Better confidence in cash planning. Better discipline around who gets unsecured terms and who doesn’t. Stronger footing when growth creates working capital pressure.

It also changes how the finance team is perceived. Instead of chasing old balances after the damage is done, finance becomes the group that protects capacity, supports profitable growth, and keeps client relationships on commercially sound terms.

If you’re looking at accounts receivable automation, AI AR automation, AR software for professional services, or a more reliable QuickBooks AR automation workflow, the objective isn’t to add more software for its own sake. It’s to build a system that sees risk earlier and responds faster.

For professional services firms that want that system without building it manually, Resolut automates AR for professional services, consistent, accurate, and human.