What is credit worthiness? A Guide for Financial Operators

What is credit worthiness? Learn how B2B firms assess client risk, boost cash flow, and protect margins with AR automation.

For a professional services firm, creditworthiness isn't an abstract score. It's a forward-looking operational question: "Will this client pay us on time?"

This question moves the focus from generic metrics to payment reliability and its direct impact on your firm's cash flow. It is the foundation of disciplined financial control.

What Creditworthiness Means in Professional Services

As a CFO, Controller, or firm owner, your perspective on client relationships must be that of a financial operator. Every time you deliver services before payment, you extend operational credit.

This is a standard business practice, akin to what is trade credit. Each project is a calculated risk—an investment of expertise and hours with the expectation of prompt payment.

From Abstract Scores to Operational Data

Large credit agencies serve a different market. Their ratings primarily apply to large-scale corporate and government finance, which accounts for approximately 65% of credit rating demand, according to the credit rating market report from businessresearchinsights.com.

Your firm requires a more tactical approach focused on tangible indicators of a client's financial stability and payment behavior.

The most reliable indicators are often directly observable:

- Payment History: What is their track record of paying you and other vendors? A consistent history of on-time payments is the strongest positive signal.

- Operational Stability: Is their leadership team consistent, or is it a revolving door? A stable business is a more predictable payer.

- Industry Reputation: What is your professional network observing? Informal intelligence can reveal payment habits that formal reports miss.

Proactive credit assessment is not about avoiding all risk; it is about making informed decisions to protect your cash flow and prevent your Days Sales Outstanding (DSO) from escalating. You can learn to calculate and reduce your DSO in our guide.

This discipline is a core component of modern financial operations and a prerequisite for sustainable growth.

The Cost of Extending Credit to Unreliable Clients

Extending payment terms to a client who is not creditworthy is a direct and measurable drain on your firm's resources. It creates operational drag long before an invoice is written off as bad debt.

The most immediate impact is on your Days Sales Outstanding (DSO). A single large client paying on Net 90 terms instead of Net 30 can disrupt your entire cash flow forecast, tying up working capital and complicating financial planning.

The Hidden Operational Drag

Financial statements do not capture the administrative hours consumed by chasing late payments. Each follow-up call and internal meeting is time diverted from high-value work like financial modeling or strategic analysis.

For a mid-sized firm, a single high-risk client can easily consume 10-15 hours of administrative time per month in collections efforts. This is an unbilled cost that erodes profitability.

This creates a cycle of inefficiency. Understanding what is credit worthiness becomes a critical tool for maintaining operational control.

* **Visual Idea: A simple line chart showing DSO for two hypothetical firms. Firm A (using proactive credit assessment) has a stable, low DSO. Firm B (reactive) has a volatile, high DSO. ***

Quantifying the Financial Consequences

The costs extend beyond lost time. A disciplined vetting process helps sidestep tangible financial consequences:

- Increased Borrowing Costs: Unpredictable cash flow may force you to draw on your line of credit to cover payroll, adding direct interest expenses.

- Delayed Vendor Payments: Inconsistent cash inflows can strain your supplier relationships and damage your firm's reputation.

- Missed Growth Opportunities: Capital that should be fueling strategic investments—hiring, technology adoption—is trapped in accounts receivable.

Failing to assess a client’s payment reliability is a direct threat to your firm’s financial agility. While platforms offering QuickBooks AR automation provide early warnings, a robust initial assessment is your first line of defense.

How to Assess a B2B Client's Creditworthiness

Determining a new B2B client's ability and willingness to pay is a core business process. For professional services firms, this means developing a practical, repeatable method to protect cash flow using accessible data.

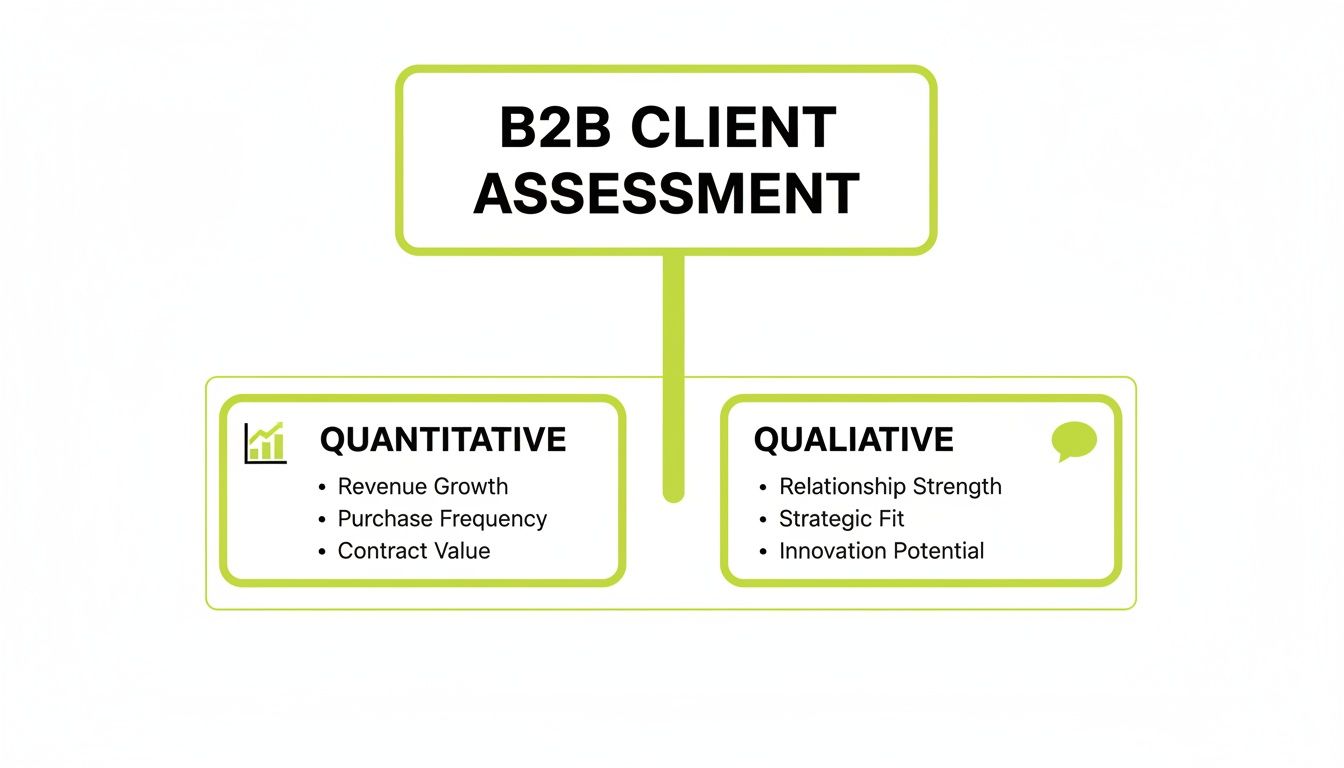

The approach should combine quantitative data with qualitative signals. Financial data provides a baseline, but the context behind the numbers often reveals a client’s true payment disposition.

Start with the Numbers

Your firm's own data is the most reliable starting point. Firsthand experience is the clearest indicator of future behavior.

- Direct Payment History: Analyze their payment record with your firm. Consistent on-time payments are a strong signal. An AR software for professional services can surface these trends instantly, as detailed in our guide to understanding the accounts receivable aging report.

- Public Financial Data: For public companies, financial statements provide insight into stability. Look for consistent revenue, healthy profit margins, and manageable debt. A sudden drop in profitability or a spike in borrowing is a red flag.

- Days Payable Outstanding (DPO): This metric reveals how long a client takes to pay its own bills. A high or rising DPO suggests they may be using vendors as a source of financing.

These metrics provide an objective, data-backed foundation for your assessment. A balanced evaluation combines this hard data with market intelligence.

B2B Credit Assessment Data Sources

Data Source | Information Provided | Accessibility | Cost |

|---|---|---|---|

Internal Payment History | Client's past payment speed, consistency, and any disputes. | High (within your AR system) | Low |

Public Financial Statements | Revenue, profitability, debt levels, and cash flow (for public companies). | Medium (requires some research) | Low |

Credit Bureaus (e.g., Dun & Bradstreet) | Formal credit scores, risk ratings, and payment history with other vendors. | Medium (requires subscription) | Medium to High |

Industry & Network Checks | Real-world reputation, payment habits, and leadership stability. | Low (relies on personal network) | Low (time investment) |

Using a combination of these sources provides the most complete picture of a client's financial health.

Layer in the Qualitative Factors

Qualitative signals often serve as early warnings for payment issues that have not yet appeared in financial data.

- Industry Volatility: Are they in a sector facing headwinds from regulation, consolidation, or economic downturns? External pressures can impact their ability to pay.

- Leadership and Operational Changes: High turnover in the C-suite or finance team can signal internal disruption that may de-prioritize vendor payments.

- Market Reputation: Discreet inquiries within your professional network can uncover valuable, on-the-ground intelligence about a client's payment practices.

By weaving together quantitative and qualitative insights, you build a comprehensive profile of what creditworthiness means for each client. This systematic approach allows you to set appropriate credit terms and manage risk proactively.

Modern Forces Redefining Client Credit Risk

Relying solely on past payment history is insufficient. It shows where a client has been, not where they are going. Broader economic and structural shifts can have a greater impact on a client’s ability to pay than their individual performance.

A forward-looking view of what is credit worthiness requires monitoring external pressures. This allows you to identify payment risks before they materialize.

A client's strong payment history is no longer a guarantee. Geopolitical events, regulatory changes, or supply chain disruptions can turn a reliable client into a late payer.

This new reality demands a shift from static, one-time credit checks to dynamic, real-time risk monitoring.

* **Visual Idea: Cinematic, high-contrast shot of a calm CFO looking at a dashboard displaying risk signals (e.g., rising DSO, industry alerts) on one screen and a clear cash flow forecast on another. The image conveys control amid complexity. ***

Beyond the Balance Sheet

The nature of credit risk is evolving. Structural forces like political fragmentation and increasing environmental pressures are changing the landscape. For example, recent trade policies are creating uncertainty for international business, a trend noted in Moody's analysis of global credit conditions.

This client assessment diagram breaks down the evaluation into its quantitative and qualitative components.

A complete risk profile requires balancing measurable financial data with a clear view of the larger market.

A disciplined approach using accounts receivable automation helps manage these modern risks. AI AR automation can continuously track payment behaviors and flag clients showing signs of financial strain, allowing you to adjust your collections strategy proactively.

The right AR software for professional services integrates this dynamic risk assessment into your daily workflow. For firms using QuickBooks, AR automation can sync payment data to create an early warning system, helping to reduce DSO and improve cash flow.

This proactive stance, supported by the right systems, turns accounts receivable into a strategic tool for navigating economic uncertainty.

Crafting Your Company’s Credit Management Policy

A formal credit management policy is your operational blueprint for risk. It translates your understanding of what is credit worthiness into a consistent, repeatable business process.

A clear policy ensures every client is evaluated through the same financial lens, aligning sales efforts with cash flow objectives. This is not about adding bureaucracy; it is about establishing financial controls.

The Core Components of a Strong Credit Policy

A practical credit policy should clearly cover four critical areas.

- Risk-Based Credit Terms: Establish standard terms (e.g., Net 30) with built-in flexibility. A new, higher-risk client might require an upfront deposit, while an established, low-risk client could earn more generous terms.

- Credit Application and Approval Workflow: Define the information required from new clients and map out the internal approval process. For example, the Controller might approve credit up to $50,000, with amounts above that requiring CFO sign-off.

- Setting and Reviewing Credit Limits: Each client should have a credit limit based on their creditworthiness assessment. The policy should mandate regular reviews—annually for low-risk clients, quarterly for higher-risk ones—to adjust limits based on payment behavior.

- Collections Escalation Protocol: Detail the step-by-step process for handling overdue invoices, from automated reminders to personal outreach. Accounts receivable automation excels at executing this protocol consistently.

A well-defined credit policy removes guesswork from AR. It transforms collections from a reactive function into a proactive system for managing financial risk.

Using AI Automation for Dynamic Credit Monitoring

A formal credit policy provides the framework; technology provides the execution. This is where intelligent automation turns credit management into a proactive, data-informed workflow that protects your firm's cash flow.

One-time credit checks are no longer sufficient. Accounts receivable automation provides continuous monitoring of client financial behavior, tracking payment patterns and spotting subtle changes in real time.

This automated oversight provides early warnings, allowing you to act before an account becomes seriously delinquent.

From Manual Chasing to Intelligent Orchestration

The strength of AI AR automation lies in its precise execution of your credit policy at scale. It directs a smart collections process based on the specific risk profile of each client, leveraging intelligent document processing to analyze payment data.

An automated system gives you control. It methodically applies your firm’s collections strategy without emotion or error.

Platforms like Resolut automatically segment your customer portfolio into risk tiers based on payment behavior, enabling a customized collections approach.

- Low-Risk Clients: Receive gentle, automated reminders that maintain a professional tone.

- Medium-Risk Clients: The system initiates a more structured follow-up sequence.

- High-Risk Clients: The system methodically escalates outreach according to predefined rules.

Measurable Outcomes for Your Firm

The transition from manual to automated credit monitoring delivers measurable results. Firms adopting this technology often achieve a reduction in DSO of 25% or more. This directly improves cash flow and frees up working capital.

For businesses on QuickBooks, AR automation syncs data seamlessly, liberating your finance team from chasing invoices to focus on high-value analysis. A modern receivable management system embeds this capability into your operations.

By integrating AI-powered monitoring, you transform credit management into a strategic asset that enhances financial stability and control.

Your Path to Confident and Consistent Cash Flow

Actively managing client creditworthiness is a fundamental discipline for any financially healthy professional services firm. The key is to shift from static, one-time checks to a dynamic, continuous approach to risk management.

This guide has outlined how the right combination of process and technology puts you in control of your accounts receivable. A clear credit policy is the first step; automation is the second.

A proactive approach transforms accounts receivable from a reactive chore into a strategic asset. It is the foundation for predictable revenue and operational stability.

By defining risk-based terms, setting credit limits, and using technology for ongoing monitoring, you build a more resilient financial foundation. AI AR automation acts as an early warning system, spotting deteriorating payment habits before they become critical issues.

From Process to Performance

This systematic approach directly impacts your bottom line. An effective credit management strategy, supported by the right AR software for professional services, delivers tangible results.

- Reduce DSO: Flagging and addressing late payments sooner shortens the cash conversion cycle.

- Improve Cash Flow: Predictable collections create a steady stream of working capital for operations and investment.

- Increase Team Efficiency: Automating follow-ups through integrations like QuickBooks AR automation frees your finance team to focus on strategic planning.

Mastering the discipline of assessing and managing what is credit worthiness is about taking control of your firm's financial future. It is how you build resilience, improve profitability, and enable sustainable success.

Resolut automates AR for professional services—consistent, accurate, and human. Learn more about how Resolut can help your firm.