What Are Net Cash Flows? A CFO's Essential Guide

Understand what are net cash flows. This CFO guide covers calculations, reconciliation, and how to boost cash flow with AR automation & reduce DSO.

Your P&L says the quarter was strong. Utilization held up. Billings were healthy. The partner group feels like the firm is moving in the right direction.

Then you open the bank portal and see a different story.

Payroll is coming due. A tax payment is near. Two large clients are “processing” invoices. The line of credit is doing more work than you want to admit. For a professional services firm, this is a familiar tension. Revenue can look solid while cash gets tighter every month.

That is not a contradiction. It is what happens when accrual accounting and cash reality drift apart.

A consulting, legal, accounting, or agency firm can post profit while collections lag, retainers run down, partner draws stay fixed, and operating costs keep hitting the account on schedule. Profit records economic activity. Cash determines whether you can fund payroll, make tax payments, invest in hires, and sleep at night.

When owners ask me what are net cash flows, they usually are not asking for a textbook definition. They are asking why a firm that appears healthy still feels fragile. They want to know why growth creates stress instead of relief.

The answer usually sits in working capital, especially accounts receivable.

If you are tightening reporting discipline, a practical companion to this discussion is Zaro’s piece on strategies to improve cash flow. It is useful because the issue is rarely just “more sales.” The issue is timing, control, and conversion of invoices into cash.

Profit on Paper Cash in Crisis

A services firm can have a record month and still feel cash pressure by the end of it.

That happens when the income statement recognizes revenue before the cash arrives. Meanwhile, payroll, software, contractors, rent, and tax obligations clear in real time. The firm looks profitable on paper and constrained in practice.

Why this happens in services firms

Professional services firms are especially exposed because they often operate with:

- Large monthly payroll commitments: Labor is the main cost, and it is paid on a fixed schedule.

- Client-specific billing friction: Approvals, invoice revisions, and matter coding can slow collections.

- Partner distribution pressure: Owners may draw cash based on reported performance, not collected cash.

- Weak AR follow-through: Teams avoid pushing clients because they do not want to damage relationships.

The result is predictable. The firm extends credit without calling it credit.

A profitable quarter does not fund payroll. Collected cash does.

What the pressure feels like operationally

You see it in small decisions before it shows up in a formal cash forecast.

Controllers delay vendor payments. CFOs hold back hires. Owners debate distributions. Finance spends more time reconciling aging than planning the next quarter. None of that means the business model is broken. It means cash conversion is under-managed.

That is the core reason net cash flow matters. It measures what changed in your cash position over a period, not what accounting says you earned.

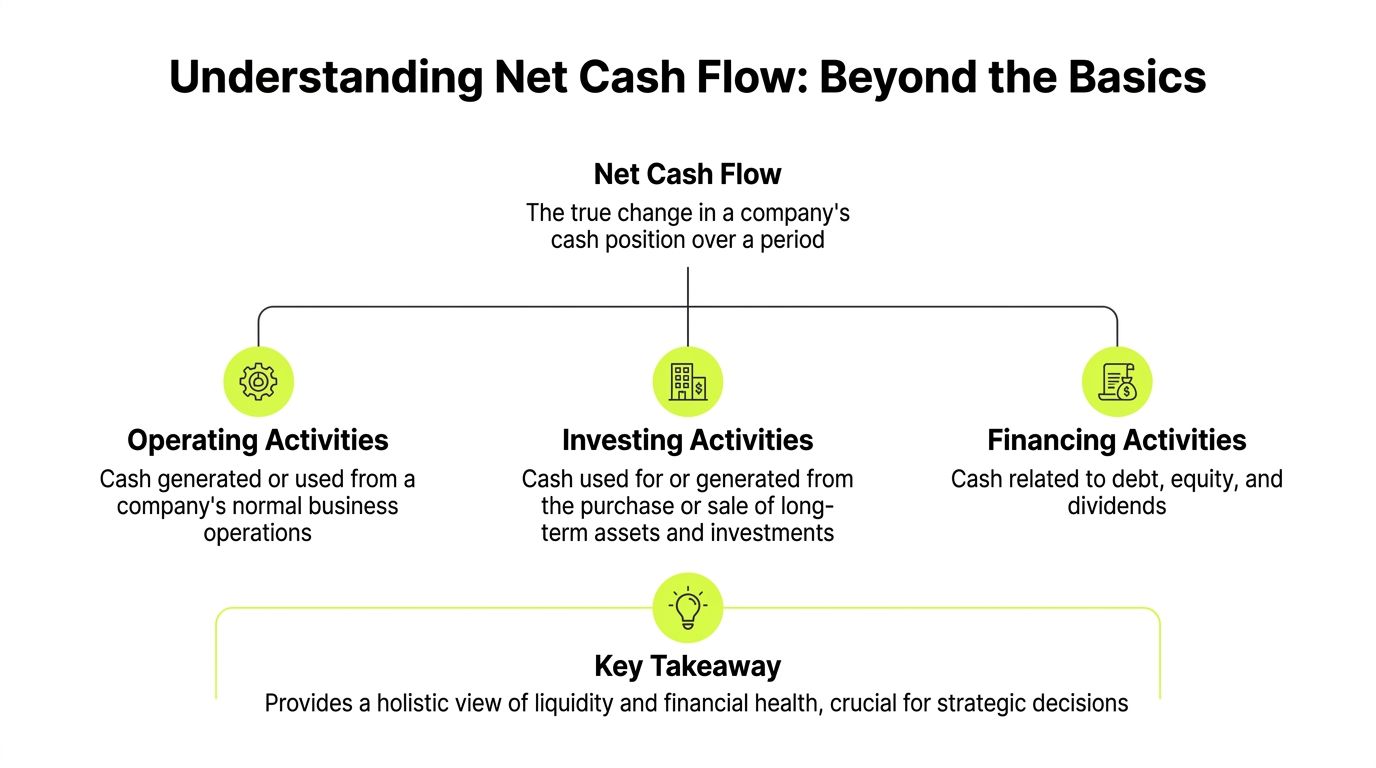

Defining Net Cash Flow Beyond the Formula

Net cash flow is the change in your cash balance over a period. Formally, it combines cash from operations, investing, and financing. In practice, it answers a more immediate question. Did the business add usable cash, burn it, or rely on outside funding to stay stable?

For a services firm, that distinction drives decisions every week. Reported revenue can look strong while cash tightens because collections lag, invoices sit in approval queues, or partners draw ahead of receipts. Net cash flow cuts through that noise and shows what changed in the bank account.

Profit tells you revenue was earned under accounting rules. Net cash flow shows whether cash arrived in time to fund payroll, taxes, vendors, and distributions.

That difference matters because several items move profit and cash in opposite directions. Depreciation reduces accounting income without reducing current cash. Accounts receivable does the reverse. It can lift reported revenue while leaving the firm short on liquidity. For professional services firms, that is usually the pressure point. If DSO stretches, net cash flow weakens even when utilization and margins look acceptable.

What net cash flow tells a CFO

For a CFO or controller, net cash flow helps answer four operating questions:

Question | What net cash flow reveals |

|---|---|

Can we meet near-term obligations | Whether current cash generation supports payroll, vendors, and taxes |

Are operations self-sustaining | Whether the core business produces cash without relying on debt or owner support |

Is growth affordable | Whether hiring and expansion are funded by collections or by financing |

Are distributions prudent | Whether owner payouts fit the firm’s actual liquidity position |

The practical importance of the definition

A clear definition changes what management reviews and what the team gets held accountable for.

Leaders who focus only on profit tend to celebrate booked revenue and overlook collection speed. Leaders who track net cash flow start asking harder and better questions. How quickly are invoices going out? Which clients are slowing payment? Where is cash getting stuck in billing approval? Are retainers sized correctly? Is finance applying cash fast enough to keep the aging accurate?

Those are operating levers, not accounting theory.

For that reason, “what are net cash flows” is not just a glossary question. It is a control question. In a professional services firm, net cash flow shows whether revenue is converting into liquidity at a pace that supports the business. If it is not, the first place to look is usually accounts receivable.

The Three Engines of Cash Flow

Most firms do not have one cash story. They have three. Each one matters, but they do not carry the same weight.

Operating cash flow

For a professional services firm, Cash Flow from Operations, or CFO, is the main engine.

This is cash produced by the business itself. Client receipts come in. Payroll, taxes, software, rent, and vendor payments go out. If this engine is weak, the rest of the structure starts compensating for it.

Under the indirect method, CFO starts with net income and adjusts for non-cash items and working capital changes. A cited example shows the mechanics: net income of $80M, plus $15M of depreciation, minus a $10M increase in accounts receivable, plus a $5M increase in accounts payable, produces CFO of $90M, as outlined by Enerpize’s net cash flow formula guide.

That example matters for one reason. The increase in accounts receivable reduced cash from operations. Revenue may have been recognized. Cash was not collected.

Enerpize also notes healthy CFO benchmarks at 10 to 15% of revenue for tech and services firms in that same guide. I would use that less as a universal target and more as a prompt. If your operating cash flow is thin relative to revenue, review AR before you blame growth or seasonality.

What usually helps CFO

In services firms, the biggest operating levers are rarely exotic. They are execution issues.

- Invoice faster: Send accurate invoices immediately after work is approved.

- Collect earlier: Follow up before due dates, not only after they are missed.

- Apply cash quickly: Unapplied receipts hide the true aging picture.

- Tighten scope control: Disputed invoices often begin with poor engagement discipline.

Investing cash flow

Cash Flow from Investing, or CFI, tends to be smaller in many professional services firms.

You may buy laptops, office equipment, a software implementation, or build out office space. Those uses of cash matter, but they usually do not create the recurring pressure that receivables do.

Negative CFI is not automatically bad. If the firm is investing in systems that improve billing accuracy or delivery capacity, the cash outflow may be sensible. The issue is whether operations are strong enough to fund it.

Financing cash flow

Cash Flow from Financing, or CFF, is where leadership often papers over an operating problem.

A line of credit draw, partner capital contribution, term loan, or delayed distribution can stabilize the bank balance for a while. That can be useful. It is not the same as healthy operations.

If a services firm repeatedly needs financing to cover routine operating needs, management should inspect receivables, billing discipline, and payment timing before discussing expansion.

A practical way to read the three engines

Use this lens each month:

Cash flow category | Good sign | Warning sign |

|---|---|---|

Operating | Client receipts consistently fund payroll and overhead | AR grows faster than collections |

Investing | Outflows support better delivery or reporting | Purchases happen without a cash plan |

Financing | Used selectively for strategy or flexibility | Used repeatedly to cover ordinary operations |

For most professional services firms, operating cash flow is the score that matters most. If that engine works, the others stay strategic. If it does not, financing starts carrying weight it should never have to carry.

Reconciling Cash Flow with Your Financial Statements

Most finance teams already have the numbers they need. The problem is not access. It is reading the three statements as one connected system.

The income statement tells you what the firm earned. The balance sheet shows what it owns and owes at a point in time. The cash flow statement explains why the cash account changed.

Start with net income, then undo accrual effects

This is the logic behind the indirect method.

You begin with net income from the income statement. Then you remove items that affected profit but not cash, such as depreciation. After that, you adjust for changes in working capital accounts from the balance sheet.

An increase in accounts receivable is the classic example. Revenue increased profit, but if the client has not paid yet, cash did not come in. So the increase in AR reduces operating cash flow.

A rise in accounts payable works in the opposite direction. If the firm has delayed paying vendors, cash stayed in the business longer, so operating cash flow increases for the period.

One balance sheet movement can explain a cash squeeze

Controllers often know this intellectually but do not use it enough as a management tool.

If revenue is up and cash is down, compare beginning and ending AR first. A growing receivables balance often explains the gap faster than any commentary deck.

This is also why bank reconciliation discipline matters. If cash application and reconciliations lag, the finance team may be looking at an aging report that does not reflect real receipts. A clean process for matching bank activity to invoices gives you a more reliable operating picture. This guide to bank account reconciliation is useful if your cash reporting is slowed by unapplied or misapplied receipts.

Why standardization helps

Cash flow reporting became easier to compare globally after IAS 7 in 1992 required separation into operating, investing, and financing activities, and by 2000 more than 100 countries had adopted similar frameworks, according to HeyGoTrade’s overview of net cash flow reporting.

That consistency matters even for a mid-market services firm. It gives lenders, investors, and outside advisors a common language for evaluating cash generation quality.

The same source notes that S&P 500 firms averaged $2.5 trillion in aggregate net cash flows in 2021. You are not benchmarking your firm against those companies directly, but the reporting structure is the same. The logic scales down cleanly.

A good controller does not read the cash flow statement as a separate report. They use it to reconcile the story told by the income statement and balance sheet.

A simple reconciliation lens

When cash changes unexpectedly, work through this sequence:

- Check profit first: Did earnings improve, or was the quarter weaker than assumed?

- Review AR movement: Did revenue turn into receivables instead of cash?

- Review AP and accrued liabilities: Did timing of payments temporarily support cash?

- Inspect investing activity: Did equipment, software, or office spend absorb cash?

- Look at financing: Did debt draws or owner contributions fill the gap?

That sequence usually gets to the answer quickly.

A Practical Calculation for a Services Firm

A services firm can post a strong month on the P&L and still feel pressure in the bank account. The usual reason is simple. Payroll, tax payments, software, and partner draws leave on schedule. Client cash often does not.

Start with cash, not revenue.

A practical operating view looks like this: the firm collects $40,000 during the month and pays out $25,000. Net cash flow for that period is $15,000.

Net Cash Flow = Total Cash Inflows - Total Cash Outflows

That sounds basic because it is. The discipline comes from counting only cash that moved.

For a professional services firm, inflows usually include collected invoices, retainers received, and occasional financing proceeds. Outflows usually include payroll, payroll taxes, contractor payments, rent, software, debt service, and owner distributions. If cash in exceeds cash out, liquidity improves. If it does not, the firm funds the gap from reserves or a credit line.

Here is a clean operating snapshot:

Item | Direction | Example for a services firm |

|---|---|---|

Client cash receipts | Inflow | Payments collected on current and prior invoices |

Loan proceeds | Inflow | Draw on working capital facility |

Payroll and taxes | Outflow | Salary, bonus, payroll tax |

Rent and software | Outflow | Overhead and tools |

Owner distributions | Outflow | Partner draws or shareholder distributions |

Now take the version I see more often. The firm bills $60,000, collects only $40,000, and still pays $25,000 of monthly obligations. Reported revenue may look fine. Net cash flow is still based on the $40,000 collected, not the $60,000 invoiced. That gap is where many firms lose control.

This is why AR management sits at the center of cash flow in services businesses. If collections slip by even a couple of weeks, DSO rises, borrowing needs increase, and management starts solving a cash problem that did not have to exist. Teams that need a refresher on the mechanics should review how to calculate accounts receivable with whoever owns billing, collections, and client follow-up.

The calculation errors are predictable. Controllers count invoices instead of receipts. Partners approve distributions before confirming collection timing. Department leaders treat utilization as a cash proxy. It is not. Utilization can be strong while cash conversion is weak.

For firms operating across entities or serving international clients, consistent statement reading matters too. A region-specific reference like Financial Statements UAE can help teams align how they interpret statement structure across jurisdictions.

The operational takeaway is straightforward. Net cash flow improves faster when a firm shortens the time between delivering work, issuing the invoice, and collecting the money. For most services firms, that is the first lever to pull.

Why Net Cash Flow Is Your Ultimate Health Metric

A services firm can post a strong month on paper and still create risk if cash generation is weak.

If I need one metric to judge whether the business is under control, I start with net cash flow. Profit reflects accounting choices, timing, and estimates. Net cash flow shows whether the firm produced enough cash to support payroll, tax payments, partner draws, debt service, and planned investment.

It shows whether the business can fund itself

The formula matters. Net cash flow equals cash from operating, investing, and financing activities. What matters more is the pattern underneath it.

A firm with consistent operating cash flow has options. It can hire ahead of demand, invest in systems, absorb a slow-paying client, and pay owners without weakening liquidity. A firm that relies on debt, delayed vendor payments, or owner capital to cover routine obligations has less margin for error.

In professional services, that gap often comes back to receivables discipline. Work gets delivered. The invoice goes out. Cash still arrives late. Net cash flow captures that failure quickly, even when reported revenue still looks healthy.

If leadership wants a practical playbook, these ways to increase cash flow in a business are usually more useful than another review of margin percentages.

Net cash flow exposes whether operations are carrying the business

Short-term fixes can hide strain for a quarter or two. Leaders can postpone discretionary spending, slow hiring, or use a credit line to smooth timing. Those choices buy time. They do not solve weak cash conversion.

Over a longer period, net cash flow answers a harder question. Is the firm producing enough cash from normal operations to support the model it has built?

A healthy pattern usually looks like this:

- Operations generate cash: Client receipts cover the normal cost base.

- Investments are planned: Technology, recruiting, and capacity spending follow a cash plan.

- Financing is selective: Debt or equity supports a specific decision, not recurring operating shortfalls.

An unhealthy pattern looks different:

Pattern | What it suggests |

|---|---|

Profit rises while cash remains tight | Collections, billing accuracy, or working capital discipline are slipping |

Financing repeatedly fills the gap | Operations are not funding the business consistently |

Distributions continue despite weak cash generation | Liquidity discipline is giving way to internal pressure |

It changes management behavior

Teams behave differently when net cash flow is on the monthly dashboard.

Billing disputes get escalated sooner. Practice leaders pay more attention to collection timing. Hiring plans get tested against liquidity, not just backlog. Owner distributions become a cash decision, not a habit.

That is why I treat net cash flow as a health metric, not just a reporting line. It ties strategy to operating reality. For a services firm, it also creates accountability around the lever that usually matters most: turning receivables into cash before growth, compensation, or expansion decisions outrun collection performance.

Net cash flow is not just a scorecard. It is a management discipline.

Strategic Levers to Improve Your Net Cash Flow

For a professional services firm, the fastest route to stronger net cash flow is usually not cost cutting. It is better cash conversion.

That means reducing the delay between doing the work, issuing the invoice, collecting the payment, and applying the cash correctly.

Start with accounts receivable discipline

Many firms still run collections with inboxes, spreadsheets, and good intentions. That works until invoice volume grows, client complexity increases, or ownership gets fragmented.

The first operating lever is to define a real collection process:

- Invoice cleanly: Make sure billing data, PO details, matter codes, and approvers are correct before the invoice leaves.

- Follow up before due dates: Reminders should begin ahead of delinquency, not after it.

- Segment outreach: A strategic client, an occasional late payer, and a disputed invoice should not get the same message.

- Escalate with rules: Collections needs timing, ownership, and thresholds, not ad hoc chasing.

At this point, accounts receivable automation starts to matter. Not as a buzzword, but as operating infrastructure.

Use tools that reduce friction, not just reporting lag

Good AR software for professional services should do four things well.

First, it should orchestrate outbound follow-up across email and other channels without turning the process into harassment.

Second, it should support easy payment. If a client wants to pay by card, bank transfer, or another method, the path should be clear.

Third, it should help with cash application so receipts are matched quickly and accurately.

Fourth, it should fit the accounting stack the team already uses. For many firms, that means QuickBooks AR automation is more relevant than an enterprise platform that requires a heavy rollout.

If you want a broader operating checklist, this guide on ways to increase cash flow is a practical place to compare immediate actions with longer-horizon process changes.

Where AI fits

AI AR automation is useful when it improves timing and consistency.

It can help tailor follow-up tone, choose outreach timing, flag at-risk invoices, and reduce manual sorting. It is less useful when it adds another dashboard but does not change collector behavior or shorten the collection cycle.

A tool should support the finance team’s workflow, not create another one.

One example in this category is Resolut, which combines credit assessment, collections outreach, dynamic billing, payment options, and cash application in one system for receivables operations. For a services firm, that matters because fragmented tools often create more handoffs than control.

A short demo of AR automation in practice is helpful here:

What works and what does not

The firms that improve cash usually make a few disciplined changes and hold them.

What works:

- Clear invoice ownership: Someone owns disputes through resolution.

- Standard reminder cadence: Clients hear from the firm consistently.

- Payment convenience: The easier it is to pay, the fewer avoidable delays.

- Daily cash application habits: Open cash gets matched quickly.

- Controller-level visibility: Aging, unapplied cash, and exceptions are reviewed together.

What does not:

- Sending invoices late and chasing hard later

- Letting partners override collection rules without a cash rationale

- Treating collections as a back-office courtesy instead of a control function

- Relying on month-end cleanup to understand receivables

Build the process around client relationships

A common objection in professional services is that tighter collections will damage the client experience.

In reality, clients usually respond better to a clear, professional process than to silence followed by sudden escalation. Predictable billing, clean invoices, timely reminders, and convenient payment options feel organized, not aggressive.

That is the point of good automation. It makes the process more consistent, accurate, and human.

From Financial Metric to Strategic Control

Net cash flow tells you whether the firm is converting work into usable cash. That makes it more than a reporting line. It is a measure of control.

For professional services firms, the biggest swing factor is rarely the formula itself. It is the discipline around billing, receivables, and cash application. Profit still matters. But cash is what funds payroll, supports growth, and protects optionality when clients pay slowly.

When you understand what are net cash flows in operating terms, you stop treating liquidity as a surprise and start managing it as a system.

Resolut automates AR for professional services with workflows that support consistent follow-up, accurate cash application, and a more controlled collections process. Learn more at Resolut.