2 net 10: A CFO's Guide to Better Cash Flow

Unlock better cash flow with 2 net 10 payment terms. This guide for CFOs covers the financial impact, accounting, and how to automate AR to reduce DSO.

A familiar finance problem looks like this. The P&L says the firm is healthy, but payroll, partner draws, contractor payments, and tax deposits still feel tight. Work is done, invoices are out, and cash is late.

For professional services firms, that gap is rarely about demand. It is about timing. When clients pay on day 30, day 45, or later, the business funds delivery with its own balance sheet. That is manageable for a while. It becomes expensive when hiring, bonuses, software spend, or owner distributions depend on receivables converting on schedule.

The Hidden Cost of Waiting for Payment

A services firm can show solid monthly billings and still operate defensively. The reason is simple. Revenue does not pay bills. Cash does.

In practice, slow payment creates second-order problems. Leadership delays hires. Controllers hold invoices for review because one billing mistake can trigger a dispute. Partners hesitate to press good clients too hard. Collections become personalized and inconsistent.

That is where 2 net 10 matters. Used properly, it is not just invoice language. It is a cash flow policy.

Where the problem shows up first

The first signs are operational, not accounting-related.

- Project delivery gets financed internally because payroll runs before collections clear.

- Client concentration risk grows when a few large invoices age at the same time.

- Finance teams spend time chasing exceptions instead of controlling the process.

- Owners confuse profitability with liquidity and then get surprised by a cash squeeze.

Professional services firms feel this acutely because there is usually no inventory to turn into cash and limited collateral to lean on. The business runs on labor, utilization, and billing discipline.

Trade terms as a control tool

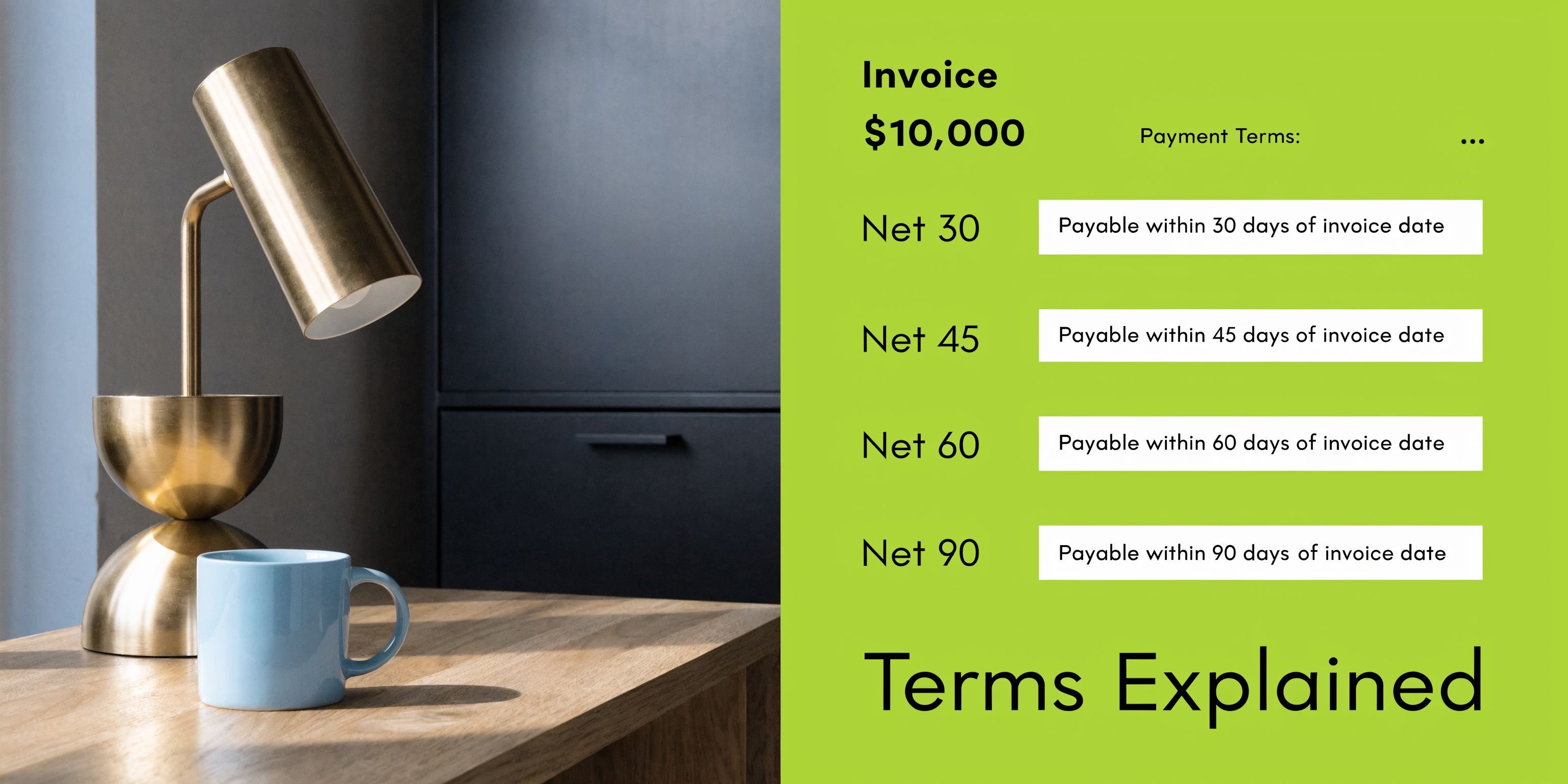

Trade credit terms let you shape behavior before an invoice is overdue. Net 30 is the baseline. Early payment terms add a financial reason to act sooner.

That matters because the broader AR environment is not forgiving. Businesses lose $200 billion annually to unpaid invoices, and average DSO of 45 to 60 days is common in industries facing collection pressure, according to Mural Pay’s explanation of net terms and calculations.

A finance team gains greater influence from changing client payment behavior at invoice issuance than from chasing the same invoice after it ages.

For a CFO or controller, the shift is important. The question is not, “How do we collect harder?” The better question is, “Which clients should receive terms that pull cash forward without creating billing noise or margin leakage?”

That is the primary use of 2 net 10.

Deconstructing 2 Net 10 and Other Trade Credit Terms

A services firm sends a $10,000 invoice on the first of the month. Payroll hits on the fifteenth. If the client pays $9,800 within ten days instead of $10,000 at day thirty, the firm gives up $200 of revenue to pull cash forward by twenty days. That is the core decision behind 2 net 10.

2 net 10 is an early payment discount term. The more common invoice format is 2/10 net 30.

The client can deduct 2% if payment arrives within 10 days. After that, the full amount is due by 30 days. In U.S. B2B billing, Net 30 and its discount variants are common, but many eligible buyers still miss the discount because approval workflows, AP queues, and timing constraints get in the way.

How it works on an invoice

For a $10,000 invoice under 2 net 10, the client pays $9,800 if payment clears inside the discount window. On day 11 through day 30, the amount due returns to the full $10,000.

The term itself is simple. Execution is where firms lose control.

Professional services firms need four things locked down before offering any early payment discount: the invoice date, the discount deadline, the final due date, and the exact charge base that qualifies for the discount. If taxes, pass-through expenses, retainers, or prior balance amounts are included incorrectly, the client may short-pay in a way your AR team cannot validate quickly. That creates write-off risk, rework, and client friction.

A clean invoice policy also needs to answer operational questions that accounting software will not resolve on its own. Does the discount apply to reimbursable expenses. Does it apply to milestone invoices but not recurring advisory fees. If a client disputes part of the bill, can they still take the discount on the undisputed portion. Those policy decisions matter more than the shorthand on the invoice.

Why the 2% matters more than it looks

A 2% discount for paying 20 days early is expensive capital if clients use it consistently. Under a standard 2/10 net 30 structure, the implied annualized cost for the buyer is high if the discount is taken consistently.

That does not mean you should avoid it. It means you should treat it as a financing decision, not a courtesy.

For firms with high gross margins, uneven collections, and limited access to cheap working capital, paying that implied rate can make sense for a narrow group of accounts. For firms already collecting predictably in under 30 days, it often just gives margin away. The right answer depends on client behavior, invoice size, and how much earlier cash reduces borrowing, owner draws, or payroll pressure.

Related terms worth knowing

Different terms fit different client profiles and operating models.

Term | What it means | Typical use |

|---|---|---|

Net 30 | Full amount due in 30 days | Default for many B2B relationships |

Net 60 | Full amount due in 60 days | Large clients with procurement-heavy payment cycles |

1/10 net 30 | Smaller discount for payment within 10 days | When margin is tighter but earlier cash still matters |

2 net 10 | 2% discount for prompt payment | Useful when speed of cash matters more than small price erosion |

In practice, professional services firms should not offer the same term to every client. A recurring retainer client with clean AP processes may not need a discount at all. A project-based client with slow internal approvals might respond well if the invoice, reminder sequence, and payment link are configured correctly.

If your team is standardizing terms across proposals, SOWs, and invoices, this guide on how to define payment terms for invoices and contracts is a useful reference.

The Financial Impact on Your Books and Cash Flow

A services firm can show a healthy month on the P&L and still feel squeezed on cash. Payroll clears every two weeks. Contractors want faster payment. Tax deposits do not wait for clients. That is where 2 net 10 changes the operating cadence, if the term is set up and enforced correctly.

The accounting is simple. The cash impact is where the core decision sits.

The accounting treatment

Assume a $10,000 invoice with 2 net 10 terms.

Scenario | Entry at invoicing | Entry at payment |

|---|---|---|

Client pays within discount window | Debit Accounts Receivable $10,000. Credit Revenue $10,000. | Debit Cash $9,800. Debit Sales Discounts $200. Credit Accounts Receivable $10,000. |

Client pays after discount window | Debit Accounts Receivable $10,000. Credit Revenue $10,000. | Debit Cash $10,000. Credit Accounts Receivable $10,000. |

The journal entries rarely cause trouble. The operational controls do.

Finance needs a clear rule for when the clock starts, what counts as payment received, who approves exceptions, and how short-pays are coded in the ERP or accounting system. For professional services firms, tax treatment can also get messy if the client takes a discount after a billing correction, scope change, or partial dispute. If the team cannot distinguish a valid discount from an unauthorized deduction, AR aging becomes less reliable and write-off risk rises.

The cash flow effect

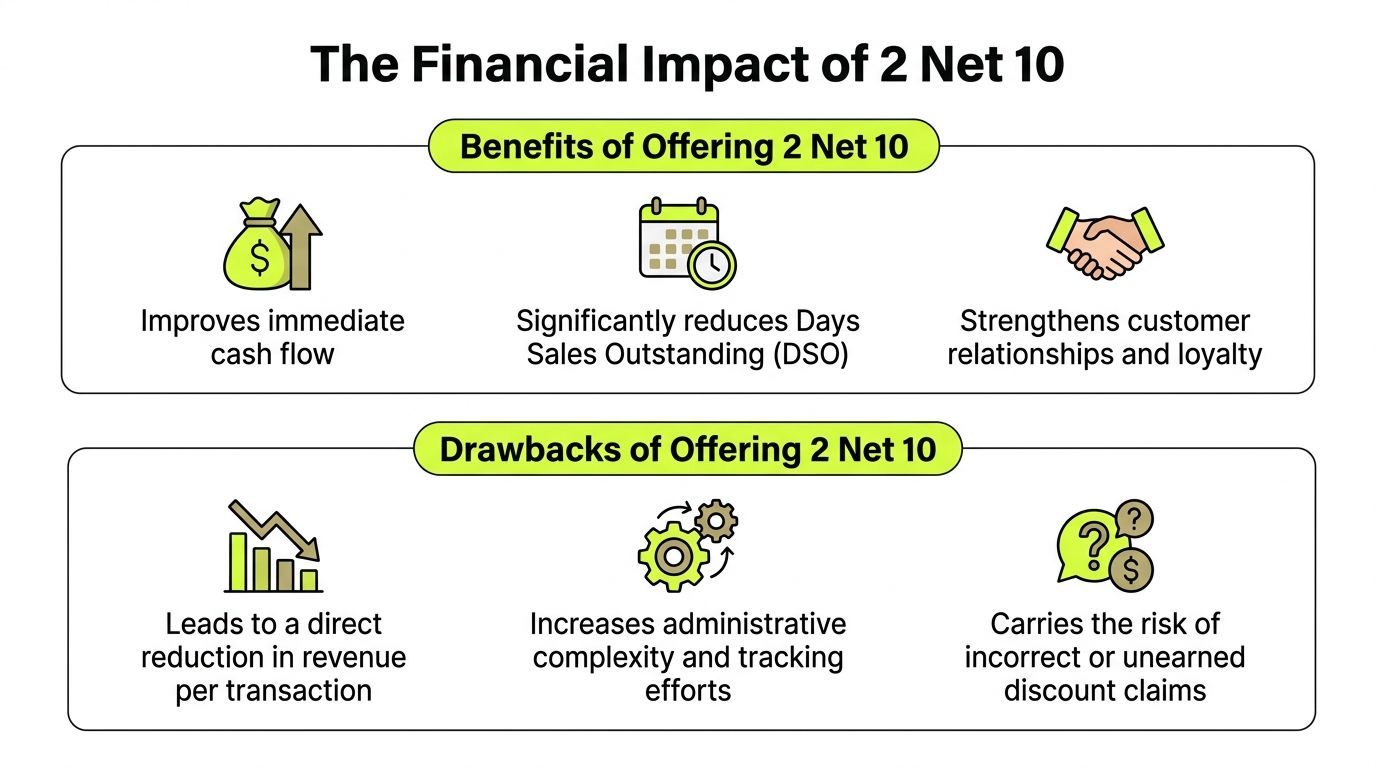

The financial trade is straightforward. You give up 2% of invoice value to pull cash forward by about 20 days if the client would otherwise pay on day 30. As explained in HighRadius' 2/10 net 30 analysis, that works out to a very high annualized return for the buyer.

For the seller, the benefit is different. Faster collections can reduce borrowing, smooth payroll funding, and lower the number of invoices that drift into manual follow-up. In a professional services firm, those gains matter most when revenue is lumpy, labor costs are fixed in the short term, and a few large invoices drive most of monthly cash receipts.

This is also why finance should track the result on a cash basis, not just a margin basis. A discount that trims revenue can still improve the business if it pulls enough cash into the right week.

What to model before rollout

Model the policy at the client and invoice level before offering it broadly.

Start with four inputs: average invoice size, current days to pay, expected discount take-rate, and the weekly cash gap the business is trying to close. Then test the result against actual operating pressure. Does earlier cash reduce draws on the line of credit? Does it prevent partner cash calls? Does it let the firm pay bonuses, taxes, or subcontractors without stretching AP?

A practical model should include:

- Invoices eligible for the program

- Clients likely to use it consistently

- Discount cost by month

- Average days accelerated

- Effect on weekly cash balance

- Change in collections workload

- Short-pay and dispute risk

If the goal is to improve collections efficiency, measure discount-eligible invoices separately from the rest of AR. Track payment timing, exception volume, and net cash collected. Firms that need a cleaner baseline for this analysis should first understand how DSO affects cash collection timing.

Where firms gain margin back operationally

The gain comes from matching policy, invoice language, reminders, and reconciliation, not just from printing “2 net 10” on a PDF.

That matters more in services than in product businesses because invoices often tie back to milestones, time entries, change orders, and client approval workflows. If billing sends one due amount, the payment portal shows another, and cash application books whatever the client remits, the discount quickly turns into leakage.

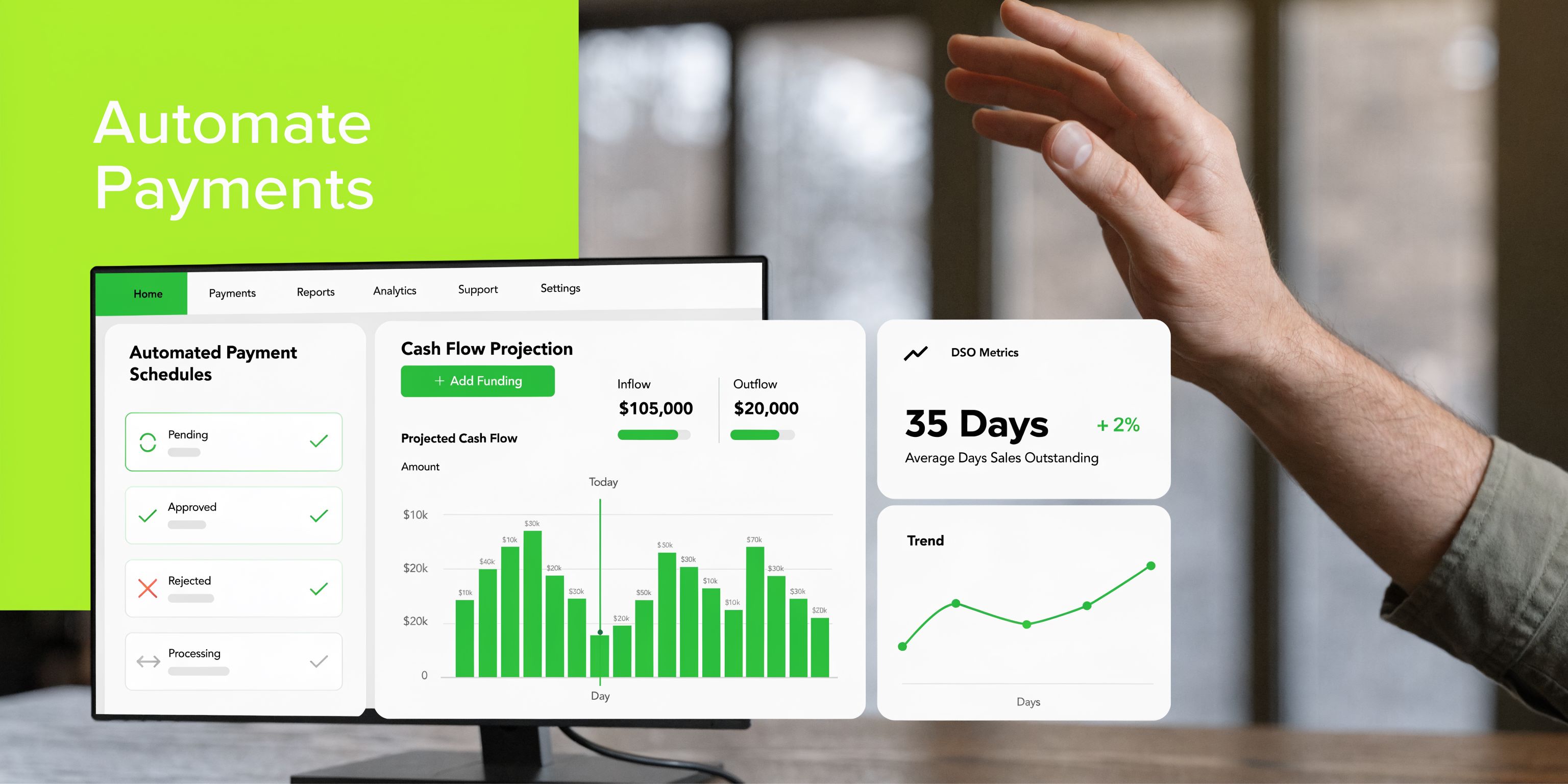

In practice, firms get better results when they define the policy in writing and automate the steps around it. A platform like Resolut can help by applying terms consistently, sending payment reminders inside the discount window, presenting the correct payable amount, and flagging deductions that fall outside policy for review. That reduces manual interpretation by coordinators and gives finance cleaner data on whether the program is shortening collection time.

Poor execution creates two predictable problems. Clients take discounts after the deadline, or the team spends so much time reviewing short-pays that the administrative cost offsets the cash benefit. Good execution avoids both.

Deciding When to Offer or Accept Early Payment Discounts

A professional services firm sends $120,000 of invoices at month-end, makes payroll on the 15th, and waits three to four weeks for cash to arrive. On paper, margins look fine. In practice, the firm is using its line of credit to cover timing gaps that a tighter payment policy could reduce.

That is the fundamental decision behind early payment discounts.

For the seller, the question is not whether 2 net 10 sounds attractive. The question is whether giving up 2% on selected invoices improves liquidity, lowers collection effort, and reduces borrowing or partner cash strain enough to justify the cost. For the buyer, the question is whether preserving cash for a few extra weeks is worth more than the discount.

When sellers should offer it

Offer an early payment discount when faster cash has a clear operational use.

In services firms, that usually means uneven billing cycles, heavy payroll exposure, contractor payments due before client cash clears, or a client base that pays slowly but predictably. A discount can also work well when the firm wants a cleaner incentive than repeated collection calls. It gives AP teams a reason to prioritize your invoice without turning every follow-up into a negotiation.

It is less effective in firms with billing quality problems. If invoices are disputed because of missing backup, vague scope language, or frequent change order confusion, discount terms will not fix the delay. They will add another exception for AR to review.

Use a tighter screen before offering it:

- Margins can absorb the concession. A 2% discount on high-labor work hits harder than on recurring advisory retainers with stable delivery costs.

- Clients have established payment patterns. The best candidates are slow payers with low default risk, not distressed accounts.

- Billing is accurate and timely. The invoice has to be right the first time.

- Your team can enforce the cutoff. If account managers override finance every time a client deducts late, the policy turns into a permanent price reduction.

- The cash benefit is measurable. Model whether earlier receipts reduce revolver use, smooth payroll funding, or shorten the time partners wait for distributions.

For many firms, the right answer is not a blanket program. It is a targeted offer by client segment, service line, or invoice type.

When buyers should take it

From the buyer's side, early payment discounts often make financial sense if cash is available or low-cost financing is available.

The harder constraint is usually process, not economics. Many AP teams cannot consistently release payment inside a 10-day window because approvals sit with engagement leads, invoice coding is inconsistent, or vendors submit invoices through multiple channels. That matters for sellers deciding whether to offer the terms. Clients with disciplined AP workflows are far more likely to respond than clients with fragmented approval chains.

If you are advising a buyer, test three points before deciding:

- Cash position. Paying early should not create a separate liquidity problem.

- Cost of funds. Compare the discount against the actual borrowing rate or treasury return on cash.

- Execution ability. If the AP process cannot approve and release payment inside the window, the discount is theoretical.

A practical decision screen

Before rolling this out, model it like an operating policy, not a pricing idea.

Start with a small group of clients and estimate the effect on cash receipts by week, not just by month. Then compare the discount cost against the financing cost avoided and the staff time saved in collections. In a services environment, those savings can be meaningful if AR coordinators stop chasing invoices that now clear in the first 10 days.

A useful screen is:

- Which clients pay on time once approved, but move slowly through AP Those clients often respond best to structured discount terms.

- Which invoices are clean and repeatable Recurring retainers and scheduled advisory fees are easier to discount than milestone invoices tied to scope review.

- What happens if adoption is partial Model the result if only a portion of eligible clients take the discount. That gives finance a realistic base case.

- Can the payable amount be presented correctly at every touchpoint Invoice PDF, reminder email, payment portal, and cash application rules need to match.

- Who owns exceptions Someone needs authority to approve or reject late deductions quickly, or the back office will lose time reviewing avoidable short-pays.

For firms using AR automation, this decision gets easier to test. Resolut, for example, can help apply terms consistently, trigger reminders inside the discount window, and flag deductions that fall outside policy so finance can see whether the program is producing earlier cash or just creating more exceptions.

The firms that get value from early payment discounts usually treat them as a controlled collections tool. They define where the terms apply, model the cash impact before rollout, and automate enough of the process that the policy holds under real client behavior.

Building and Implementing a Discount Policy

A workable 2 net 10 program needs policy before software.

If the rule lives only in a controller’s head or inside a few custom client arrangements, it will create exceptions, not control. The goal is a documented standard that billing, client service, and accounting all apply the same way.

What the policy should cover

A short policy is enough if it answers the operational questions clearly.

Include:

- Eligible clients. New clients, all clients, or only approved segments.

- Eligible invoices. Recurring fees, project invoices, retainers, or specific service lines.

- Discount window. Define whether the count starts on the invoice date and whether weekends and holidays count.

- Exclusions. Disputed invoices, milestone billing, reimbursable expenses, or tax amounts if applicable to your setup.

- Approval authority. Who can grant exceptions.

- Short-pay handling. What happens if a client deducts the discount late.

A simple policy template

Use language your team can follow.

Early Payment Discount PolicyApproved clients may deduct 2% from eligible invoices if full payment is received within 10 days of the invoice date. After the discount window, the full invoice amount is due according to the stated payment terms. Discount eligibility does not apply to disputed invoices, unauthorized deductions, or invoices specifically marked as excluded. Any exception requires finance approval.

That is enough to govern behavior internally. You can add client-specific rules outside the core policy if needed.

Invoice language that reduces confusion

Do not make clients interpret your terms.

Use direct wording such as:

- Option 1 Payment terms: 2% discount if paid within 10 days. Full amount due in 30 days.

- Option 2 Pay by [date] and remit 98% of invoice total. After [date], full payment is due.

- Option 3 Early payment discount applies only if payment is received within the stated discount period.

Internal rollout matters more than most firms expect

The policy fails when sales promises one thing, billing sends another, and accounting enforces a third.

Train the people who touch the invoice lifecycle:

Team | What they need to know |

|---|---|

Sales or partners | Which clients qualify and who approves exceptions |

Billing staff | Exact invoice wording and due date setup |

AR team | How to validate earned versus unearned deductions |

Controllers | How discounts are booked and reviewed |

A good policy should reduce judgment calls. If every invoice becomes a debate, the policy is not finished.

Automating Early Payments to Reduce DSO

Manual 2 net 10 administration breaks down quickly.

Someone has to calculate the deadline, send reminders at the right time, show the correct amount due, accept payment, and reconcile a partial payment without creating an exception. That is a lot of handoffs for a small discount program.

Why manual workflows underperform

Most firms start with spreadsheets, calendar reminders, and invoice notes in QuickBooks or the PSA system. That can work at low volume. It usually fails once invoice count rises or multiple client contacts are involved.

Common failure points look familiar:

- Discount windows pass without outreach

- Clients ask what amount to pay

- AR teams receive the right payment but post it as a short-pay

- Partners intervene inconsistently

- Reporting cannot distinguish earned discounts from leakage

Tipalti notes that suppliers report 18-22% DSO reduction when 50%+ of invoices are prompted effectively, and that AR automation platforms can increase discount capture by 20-35% using dynamic billing and personalized outreach, according to its review of 2/10 net 30 workflows.

The automation workflow that works effectively

For professional services, the winning setup is not complicated. It is structured.

Trigger the right reminder cadence

The system should know the invoice date, discount deadline, and final due date.

A solid reminder sequence might include:

- Invoice delivery message with discount terms stated clearly

- Mid-window reminder before the discount expires

- Final same-day prompt on the discount deadline

- Post-window notice confirming the invoice has reverted to full balance

The message should be concise. Clients should not have to calculate anything.

Example:

Your invoice is eligible for the early payment discount through [date]. Pay within the discount window to close the balance at the discounted amount.

Present the correct payable amount

At this point, many firms lose the benefit.

If the client portal or payment link shows only the gross invoice amount, clients hesitate or pay incorrectly. The payment experience should reflect the valid discounted amount automatically while the window is open.

That is especially important for accounts receivable automation, AR software for professional services, and teams using QuickBooks AR automation workflows. The invoice terms and payment screen need to agree.

Reconcile without creating noise

When the discounted payment comes in, cash application must recognize it as valid, not as an underpayment that triggers follow-up.

That is where straight-through posting matters. Finance teams that want cleaner operations should think in terms of straight-through processing, not just reminder emails.

AI AR automation is useful when it improves timing and consistency

The phrase AI AR automation only matters if it fixes execution. In a discount program, effective automation does four things well:

- chooses the right contact and channel

- sends reminders before the decision point

- reflects the correct payable amount

- posts the result accurately

For firms exploring the broader operational side of this, this piece on how automation can streamline your business processes is worth reading because it frames automation as process design, not just software replacement.

After the reminder and portal logic are in place, video walkthroughs can help internal teams align on what the client experience should feel like.

Where QuickBooks users should be careful

Many firms in the $3M to $50M range rely on QuickBooks as the source of truth. That is workable, but only if the AR workflow around it is disciplined.

Watch for these gaps:

- Invoice terms entered manually with inconsistent formatting

- No automated reminder tied to discount cutoff

- Client payment links that ignore discount eligibility

- Manual cash application that misclassifies valid deductions

The best automation setup is boring. Terms are applied consistently, reminders go out on time, clients see the right amount, and accounting closes the loop without intervention.

That is how you use 2 net 10 to improve cash flow. Not as a one-time pricing trick, but as an operating system for getting paid earlier with fewer exceptions.

Your Next Move for Smarter Cash Flow

2 net 10 is small on paper and meaningful in operation.

For a professional services firm, it can create earlier cash, better payment predictability, and less collection friction. But only when finance treats it as a controlled program. Not a casual invoice note.

The practical sequence is straightforward.

First, identify which clients and invoices are good candidates. Then document the policy, standardize invoice language, and decide how your team will validate earned discounts. After that, automate the reminders, payment presentation, and reconciliation so the policy works the same way every time.

If the process stays manual, the firm usually gets the downside without the benefit. Margin leaks. Deadlines get missed. Valid payments turn into avoidable exceptions.

If the process is tight, 2 net 10 becomes one of the cleaner ways to improve cash flow, support accounts receivable automation, and help reduce DSO without making client relationships adversarial.

Resolut automates AR for professional services with the kind of control finance teams need. Consistent outreach, accurate cash application, and human judgment where it matters. Learn more at Resolut.