Debt Recovery Letter Template: CFO-Approved Guide 2026

Get our CFO-approved debt recovery letter template & playbook. Automate reminders, demand letters & escalations to reduce DSO & improve cash flow.

When AR slips, cash gets trapped in work you've already delivered. That's not a collections problem. It's a capital efficiency problem.

The numbers are blunt. Structured debt recovery letters can reduce recovery time by 20 to 40 percent when used as the final amicable step after email and SMS reminders, and a registered formal demand letter can recover 65 to 85 percent of overdue B2B invoices within 30 days when it includes specifics like invoice numbers and overdue dates, according to Tratta's debt collection letter analysis.

Most firms still handle this with scattered emails, one-off follow-ups, and partner-driven judgment. That's expensive. It creates inconsistent client experience, weak documentation, and avoidable delays in payment.

My view is simple. A debt recovery letter template is useful, but a template alone won't fix AR. What fixes AR is a sequenced system: clear triggers, controlled tone escalation, accurate invoice detail, and automation that adapts to customer behavior.

That matters most in professional services. Your receivables are usually concentrated. A few slow clients can distort month-end cash, create avoidable borrowing pressure, and waste controller time that should go into forecast accuracy and margin control. If you want to reduce DSO, improve cash flow, and stop relying on manual chasing, build the process first. Then automate it.

Beyond Reminders The Financial Drag of Unsystematic Collections

60 days past due rarely starts as a customer dispute. It usually starts as a weak process.

Finance teams feel it in small failures that pile up fast. Billing goes out on schedule. Follow-up does not. One account gets chased because someone remembers it in a weekly meeting. Another sits untouched because ownership is vague. Partners step in selectively, collection notes live across inboxes, and the AR team spends time deciding what to send instead of running a controlled sequence.

That operating gap carries a real cost. The U.S. Chamber of Commerce's reporting on late payments and small business cash flow pressure shows how delayed customer payments strain working capital and force businesses to spend more time managing short-term cash needs. That is the hidden tax of unsystematic collections. You burn staff time, weaken forecast accuracy, and normalize slower payment behavior.

Practical rule: If your team is writing collection messages from scratch, your AR process is already off-policy.

I see four predictable consequences when collections depend on memory and individual judgment:

- Cash conversion slows: Work is complete, but cash stays tied up in receivables longer than it should.

- DSO rises: Delay becomes the default because no trigger forces the next action.

- Customer treatment varies: reliable clients get clumsy follow-up, and habitual slow payers learn your team lacks discipline.

- Records break down: if escalation is needed, the communication trail is scattered and harder to defend.

The fix is not tougher wording. The fix is a managed communication system.

A debt recovery letter template helps with consistency, but static templates only solve a small part of the problem. Collection performance improves when letters are part of a timed sequence with clear ownership, defined escalation rules, and behavior-based adjustments. If a customer opens emails and ignores them, the next step should change. If a long-standing client pays after the first notice every quarter, the tone and timing should reflect that pattern. That is the difference between sending reminders and running AR as an operating function.

If your team needs a clearer structure for managing customer communication across accounts and escalation paths, start there. Then connect that structure to your AR software so the next action happens on time, every time.

That is how you protect client relationships and improve cash flow at the same time.

The Foundation Systemizing Your AR Communication Strategy

Most template libraries start with wording. I start with segmentation.

If you send the same message to every overdue client, you create avoidable friction. A long-term client with a solid payment history shouldn't get the same tone as a repeat slow payer who ignores reminders until legal language appears. Your policy has to reflect that reality.

A static debt recovery letter template also misses the real opportunity. Many existing templates focus on sequential communications but fail to address dynamic personalization based on debtor behavior and AI-driven timing. AI-personalized outreach boosts recovery rates by 35 to 50 percent, and 1 in 10 invoices go unpaid globally, as summarized in Chaser's write-up on collection letter gaps.

Segment before you escalate

I recommend three practical segments for professional services firms.

- Reliable clients with a likely oversight: These accounts get a softer opening. Assume process friction, not bad intent.

- Clients with inconsistent payment habits: These need tighter follow-up, shorter deadlines, and clearer next steps.

- Habitual late payers or disputed accounts: These should move quickly into formal documentation and tighter internal oversight.

This isn't theory. It protects relationships and improves collection discipline at the same time.

A client who normally pays on time may just need a clean reminder with the invoice attached and a direct payment path. A chronic slow payer needs a message that shows your team is tracking every touchpoint and will follow through.

Define the internal triggers

Before your team sends anything, lock the policy.

You need clear rules for:

- When the first reminder goes out

- How long you wait between stages

- Who approves a formal demand

- When sales or account management gets involved

- When service restrictions or legal review are considered

Without that structure, collections become personality-driven. That's where firms lose time and credibility.

Good AR communication isn't aggressive. It's consistent.

Use your CRM, ERP, or billing system to surface the facts that should drive message choice. Invoice age. Payment history. Open disputes. Prior promises to pay. Engagement with prior reminders. If your team doesn't centralize those signals, they can't personalize intelligently.

For firms trying to tighten process discipline, I also recommend reviewing how you handle broader client messaging. This guide on managing customer communication is useful because collections tone usually reflects wider communication habits across the firm.

Build a relationship-safe escalation policy

A good policy does two things at once. It protects cash flow and protects commercial trust.

That means your letters should escalate in tone, but not in chaos. Every message should feel like the next logical step in a professional process. Not an emotional reaction from finance.

Use this test before approving your workflow:

Policy area | Weak practice | Strong practice |

|---|---|---|

Client segmentation | Same sequence for everyone | Message path based on payment behavior |

Ownership | Partner or AR “handles it” informally | Clear owner at each stage |

Escalation | Triggered by frustration | Triggered by defined invoice age and account status |

Personalization | Name merge only | Timing and tone adapt to customer history |

Documentation | Notes scattered across inboxes | Central record of all touches |

If you do this well, your debt recovery letter template stops being a standalone document. It becomes part of a controlled AR system.

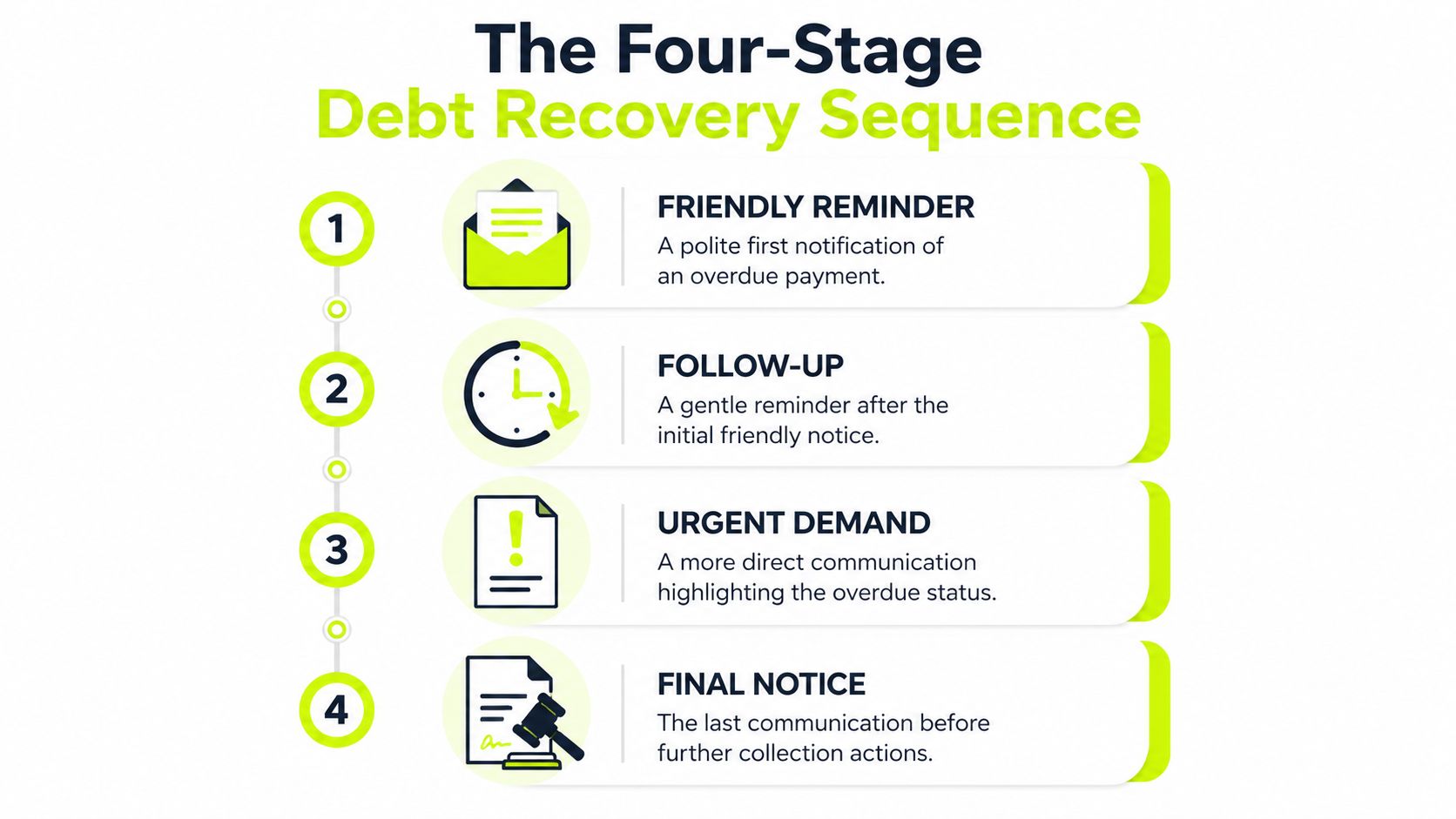

The Four-Stage Debt Recovery Letter Sequence Templates And Timing

The sequence matters more than the individual letter.

Effective debt collection uses a 3 to 4 letter sequence spaced about 14 days apart, with progressive tone escalation and context-based personalization. Key metrics include Recovery Rate by Stage, Average Response Time, and Dispute Rate, according to Moveo's debt collection letter framework.

Use that cadence as your baseline. Then adapt it for invoice size, client history, and account risk.

Early in the process, I want clarity and ease. Later, I want documented firmness. Every stage should answer four questions for the client: what is owed, what needs to happen now, by when, and what changes if they ignore it.

Here's the sequence I use.

Debt Recovery Letter Sequence At-a-Glance

Stage | Timing (Days Past Due) | Tone | Key Objective |

|---|---|---|---|

Friendly Reminder | 14 | Polite and helpful | Prompt payment by assuming oversight |

Firm Inquiry | 28 | Direct and professional | Confirm status and require response |

Formal Demand | 42 | Clear and authoritative | Set deadline and document escalation |

Final Notice | 56 | Controlled and serious | Force resolution or move to next action |

Stage 1 Friendly reminder

This is not the place for threats. It is the place for precision.

Your first debt recovery letter template should assume the invoice was missed, routed incorrectly, or delayed in internal approval. That framing lowers resistance and gets you paid faster.

Operational goal: make payment easy and remove excuses.

Include:

- Invoice detail: invoice number, issue date, due date, amount due

- Payment path: payment portal, bank transfer instructions, remittance contact

- Simple call to action: confirm payment or reply with a question

- Relationship language: acknowledge the client relationship without sounding soft

Subject line options:

- Friendly reminder on invoice [Invoice Number]

- Invoice [Invoice Number] is now overdue

- Payment reminder for outstanding invoice [Invoice Number]

Template

Dear [Client Name], Our records show that invoice [Invoice Number], dated [Invoice Date] and due on [Due Date], remains unpaid. The outstanding balance is [Amount Due]. If payment has already been sent, please reply with remittance details so we can update our records. If not, please arrange payment using the link or instructions below. Payment options: [Payment Portal / ACH / Card / Other Method] If there's a billing question or approval issue on your side, reply to this message and we'll resolve it quickly. Thank you, [Name] [Title] [Company]

The first letter should sound like finance is paying attention, not panicking.

If your team also manages other reminder-based workflows, it helps to study message clarity outside collections. A good example is this breakdown of a best survey reminder email, because the same principle applies: one action, one deadline, no clutter.

Stage 2 Firm inquiry

If the first reminder is ignored, stop being vague.

At this point, your message should reference prior outreach and require a response. You're still professional, but you've moved from “just checking” to “we need action.”

Operational goal: surface the reason for non-payment and force movement.

Tone guidance:

- Calm

- Specific

- No apology

- No open-ended language

Subject line options:

- Second notice for invoice [Invoice Number]

- Action required on overdue invoice [Invoice Number]

- Response needed for outstanding balance

Template

Dear [Client Name], We contacted you previously regarding invoice [Invoice Number], which remains unpaid. The balance of [Amount Due] was due on [Due Date]. Please confirm one of the following by [Response Date]: 1. Payment has been submitted 2. Payment will be submitted by a specific date 3. There is a billing issue requiring review If we don't hear from you by [Response Date], we will continue with our standard collections process. Payment options and invoice details are included below for convenience. Regards, [Name] [Title] [Company]

This stage works because it narrows the client's options. You aren't asking for a story. You're asking for status.

Stage 3 Formal demand

Many firms fail by either overreacting with hostile language or staying too soft because they're afraid of upsetting the client.

Both are mistakes.

A formal demand letter should be structured, documented, and unmistakably serious. It should include the specific invoice references, the total amount owed, any agreed fees if applicable, and a firm deadline. It should also make clear what internal action follows if the deadline passes.

Use this stage when prior reminders have not produced payment or a credible response.

A short video overview can help teams align on escalation standards before they start automating the workflow.

Operational goal: create formal pressure and preserve a clean documentation trail.

Checklist for this letter:

- Accurate debt breakdown: total due, invoice references, dates, any prior partial payments

- Explicit deadline: exact date, not “as soon as possible”

- Consequences stated carefully: internal review, service hold, third-party escalation, legal review as permitted

- Reply path: one direct contact person

Subject line options:

- Formal demand for payment on invoice [Invoice Number]

- Immediate attention required for overdue balance

- Formal notice regarding unpaid invoice [Invoice Number]

Template

Dear [Client Name], This letter serves as a formal demand for payment of the following overdue balance: Invoice Number: [Invoice Number] Invoice Date: [Invoice Date] Due Date: [Due Date] Amount Due: [Amount Due] Despite prior reminders, we have not received payment or an agreed resolution. Please ensure payment is received by [Deadline Date]. If we do not receive payment or a substantive response by that date, your account will be forwarded for further review as permitted by law and under our standard credit control process. If you believe this balance is incorrect, contact us immediately with supporting detail. Otherwise, remit payment using the instructions below. Sincerely, [Name] [Title] [Company]

Keep consequences real. If your team won't follow through, don't write it.

Stage 4 Final notice

The final notice is not louder. It's narrower.

At this point, you're telling the client the amicable window is closing. The letter should summarize prior communication attempts, restate the balance cleanly, and identify the next internal step if payment isn't received by the stated date.

Don't add emotional weight. Add procedural certainty.

Operational goal: close the file one way or another. Payment, dispute, payment plan, or escalation.

Subject line options:

- Final notice before further action on invoice [Invoice Number]

- Final payment deadline for outstanding balance

- Final collection notice for [Invoice Number]

Template

Dear [Client Name], This is our final notice regarding the overdue balance listed below. We have previously contacted you regarding this matter and have not received payment or a confirmed resolution. Invoice Number: [Invoice Number] Due Date: [Due Date] Outstanding Amount: [Amount Due] Final Response Deadline: [Deadline Date] If payment or a substantive response is not received by [Deadline Date], we will proceed with the next step in our collections process in accordance with our policies and applicable law. To resolve this matter, please submit payment or contact [Contact Name] immediately. Regards, [Name] [Title] [Company]

What each letter must contain every time

Many firms lose effectiveness because they improvise the basics. Don't.

Every debt recovery letter template in your library should contain:

- Who owes what: debtor name, creditor name, exact invoice references

- What happened: issue date, due date, current overdue status

- How to pay: portal, transfer, card, cheque if relevant

- What happens next: deadline plus a lawful, real next step

- How to challenge it: a clear route to raise a dispute or billing error

That structure matters. It protects the relationship because it removes ambiguity.

It also helps your team measure what works. Review each stage by:

- Recovery Rate by Stage

- Average Response Time

- Dispute Rate

- Payment plan acceptance when offered

If one stage produces replies but not payments, fix the call to action. If disputes spike at a certain stage, review your invoice accuracy or tone. The point isn't to send more letters. It's to make each stage do a specific job.

Activating Your Playbook with AR Automation

Templates are only useful if your team sends them on time, with the right data, through the right channel.

That's why I push firms toward accounts receivable automation instead of manual follow-up. Once your policy is defined, the software should handle the sequence. Humans should handle exceptions, disputes, and high-value relationship calls.

What to automate first

Start with the triggers, not the wording.

In QuickBooks AR automation or a dedicated AR platform, set workflows around operational events:

- Invoice past due status: trigger stage one automatically when the invoice crosses your threshold

- No response after prior contact: move the account into the next letter stage

- Promise-to-pay broken: accelerate tone and shorten the next deadline

- Dispute flag added: pause escalation and route to a human owner

- Payment received: stop the sequence immediately

That's the core shift. You move from “who needs a reminder today?” to “which rule fired, and what does the workflow do next?”

Personalization should go beyond mail merge

Most firms think personalization means inserting a first name and invoice number.

That's weak.

Real AI AR automation uses customer behavior to change timing, tone, and channel. A client who usually pays after one email shouldn't get the same escalation path as a client who ignores email but responds to a call. A client with multiple open invoices may need a consolidated message instead of fragmented reminders. A high-value strategic account may require partner visibility before a formal demand goes out.

The software should pull in:

- Account history: payment patterns, broken promises, prior disputes

- Invoice context: age, amount, service line, concentration risk

- Engagement data: opened message, clicked portal, replied, ignored

- Operational owner: account manager, controller, collector, or partner

If you need help mapping those workflows into your finance stack, teams sometimes work with specialists such as an AI automation agency to design operational automations across billing, outreach, and back-office processes.

Measure behavior, not just sends

Finance teams often stop at send volume and open rates. That's marketing thinking. AR needs tighter measures.

Track:

Metric | Why it matters |

|---|---|

Recovery rate by stage | Shows which letter actually moves cash |

Average response time | Reveals whether timing and channel are working |

Dispute rate | Highlights billing accuracy issues or bad tone |

Payment conversion after portal visit | Tells you whether the payment path is frictionless |

Those metrics come straight from the workflow. If stage two gets replies but stage three gets payments, your first messages may be too soft. If clients click but don't pay, your portal or approval chain may be the problem.

For firms evaluating systems, this overview of accounts receivables automation is a practical reference point because it connects workflow design, collections orchestration, and payment handling.

One platform in this category is Resolut, which combines credit risk, collections workflows, omnichannel outreach, payment options, and cash application in one AR operating layer. For professional services firms, that matters because the handoff between invoicing, follow-up, and reconciliation is usually where process breaks.

The point of automation

Automation doesn't replace judgment. It protects it.

Your controller shouldn't spend the morning deciding which overdue invoice deserves attention. The system should handle standard sequence execution. Your people should step in when an account needs negotiation, exception handling, or relationship management.

That's how you improve cash flow without turning the finance function into a call center.

Managing Legal Guardrails And Professional Tone

A bad collection letter creates two risks at once. It weakens your legal position and damages your reputation with the client.

Even in B2B collections, I recommend using FDCPA-style discipline as a house standard for written communication. In the United States, the Fair Debt Collection Practices Act requires debt collectors to send a validation notice within five days of initial contact, and the debtor has 30 days to dispute the debt. Non-compliance can risk fines averaging $1,000 per violation, based on Etactics' summary of debt collection letter requirements.

That doesn't mean every B2B firm is operating under the same rule set in the same way. It means the principles are sound: accuracy, clarity, documentation, and no misleading threats.

What to say and what to avoid

The safest tone is firm, factual, and restrained.

Use language like:

- Clear deadline: Payment is requested by [date].

- Lawful next step: If we do not receive payment or a response by [date], your account will be forwarded for further review as permitted by law.

- Dispute route: If you believe this balance is incorrect, reply with the supporting detail so we can review it.

Avoid language like:

- Fake urgency: You must pay today or we will sue immediately.

- Threats you won't execute: This matter will definitely go to court.

- Personal accusation: You have ignored your obligations.

- Harassing tone: repeated hostile wording, shaming, or exaggerated consequences

The strongest collection letter sounds controlled, not angry.

Use compliance as an operating discipline

Your legal guardrails should live inside the workflow, not in a policy memo nobody reads.

That means:

- Approved templates only: no freehand escalation from junior staff

- Required fields: invoice number, amount, due date, payment instructions, contact path

- Central records: every message stored against the account

- Escalation approval: final notices and legal-style demands reviewed before release

Many firms get sloppy. They rely on partner emails, ad hoc wording, and verbal follow-up that never gets recorded. Then a dispute appears and no one can reconstruct the timeline.

If the matter progresses beyond internal collections, the process changes from communication management to legal enforcement. For firms dealing with post-judgment recovery questions in a specific jurisdiction, this guide to collecting a judgment in Georgia is a practical example of how enforcement mechanics differ from pre-judgment collection work.

For day-to-day controls, it also helps to standardize the language in your formal notices. This example of a legal letter of demand for payment is useful because it shows the level of specificity finance teams should require before an account moves into a more serious stage.

Professional tone is part of the asset

Professional services firms sell trust. Your collections language should reflect that.

Clients can be late and still be valuable. A well-run AR function keeps pressure on the invoice without creating unnecessary conflict. That's why good debt recovery letter template design matters. It keeps the message tied to facts, deadlines, and process.

The tone you want is simple: calm authority.

From Templates to an Intelligent AR Operation

A debt recovery letter template is a starting point. It is not the system.

Improvement happens when you combine four things: segmentation, a defined escalation path, precise letter content, and automation that executes without drift. That's how firms move from reactive chasing to controlled collections.

For CFOs and controllers, the business case is straightforward. Better AR process means faster collection, tighter forecast confidence, less manual follow-up, and fewer surprises at month end. It also creates cleaner accountability. Everyone knows when an invoice moves stages, who owns the exception, and what the next action is.

The bigger shift is cultural. When the firm stops treating collections as an awkward afterthought, cash flow improves because the process improves. Clients see consistency. Finance gains efficiency. Partners spend less time intervening in avoidable payment delays.

A mature AR function doesn't rely on heroic follow-up. It runs on policy, timing, and evidence.

If you're reviewing AR software for professional services, don't just ask whether it can send reminders. Ask whether it can adapt by account behavior, track stage-level outcomes, support QuickBooks AR automation, and give your team a clean handoff from reminder to payment to reconciliation.

That's the difference between static templates and an intelligent AR operation. One produces activity. The other produces control.

Resolut automates AR for professional services with workflows that keep follow-up consistent, accurate, and human. If you're tightening collections, trying to reduce DSO, or looking at AI-driven accounts receivable automation that fits the way finance teams work, Resolut is worth a look.