How to Collect Unpaid Invoices: A Guide for Finance Leaders

Learn how to collect unpaid invoices with a proven framework for professional services. Improve cash flow and reduce DSO with AR automation.

Collecting unpaid invoices is not an administrative task; it is a system of financial control. The objective is to diagnose the health of your accounts receivable, implement a disciplined outreach cadence, and leverage technology to automate repetitive work without alienating clients. This is how finance leaders shift from reactively chasing cash to proactively managing working capital.

Assessing Your Accounts Receivable Health

Before implementing any collection strategy, you must have a precise understanding of the financial risk embedded in your outstanding AR. This requires moving beyond a standard 30-60-90 day aging report, which often obscures underlying issues and fails to provide an actionable path forward. For a firm managing millions in revenue, a surface-level view is insufficient.

A significant portion of revenue for professional services firms is frequently tied up in overdue invoices. In the U.S., a staggering 55% of all B2B invoiced sales are overdue. This is not a minor operational friction; it is a systemic drag on cash flow that complicates everything from payroll to strategic investments.

Beyond Standard Aging Reports

An effective AR analysis segments receivables by more than just age. It categorizes clients based on a matrix of factors that signal both risk and value. This data-driven framework allows you to differentiate between a chronically late payer and a high-value client experiencing a temporary cash flow disruption.

This strategic segmentation must evaluate:

- Payment History: Analyze past payment behavior to identify patterns. Is this a one-off delay or a recurring issue?

- Client Value: Assess their total contract value and strategic importance. A key partner warrants a different approach than a small, transactional client.

- Communication Responsiveness: Gauge their response to initial outreach. A prompt reply signals engagement; radio silence is a red flag requiring immediate escalation.

If you use multiple communication channels, data from tools like WhatsApp Analytics and Reporting can provide useful metrics on communication effectiveness.

Creating a Client Risk-Scoring Model

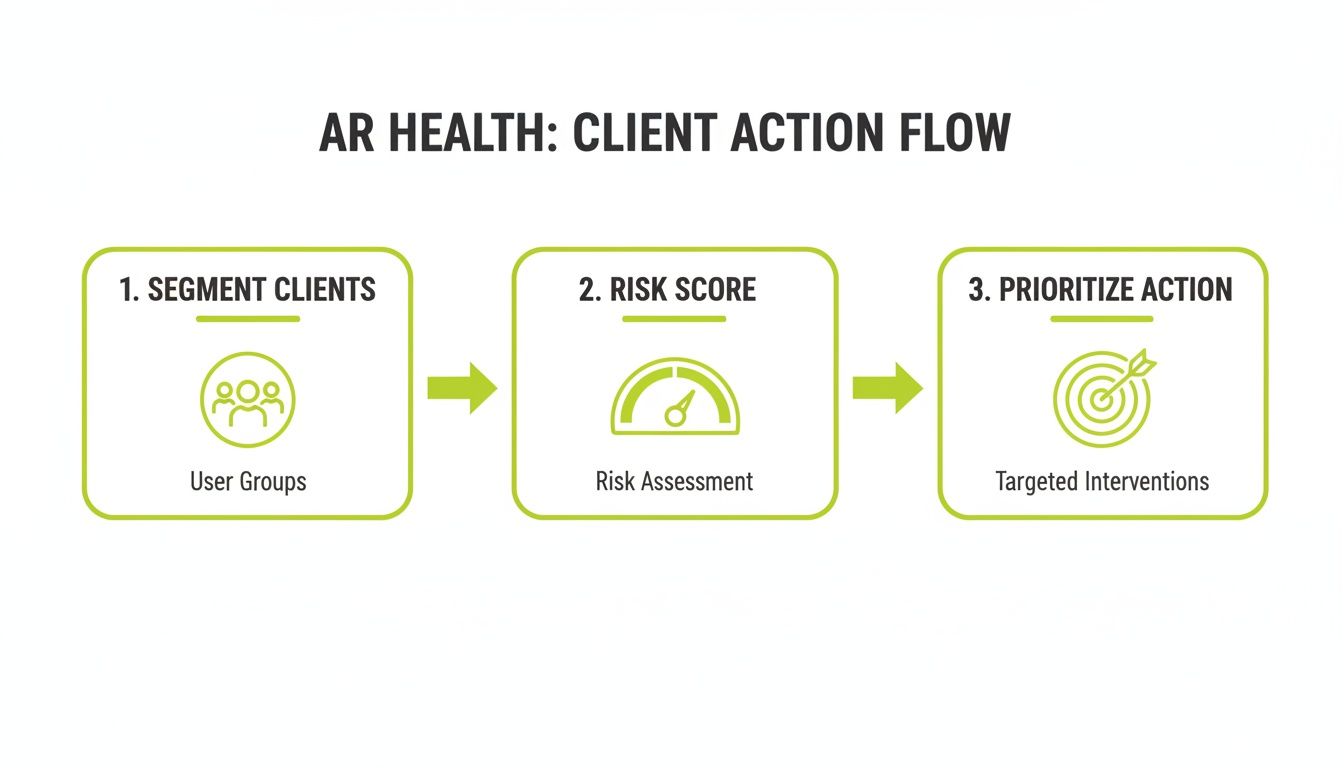

This analysis should inform a simple, actionable risk-scoring model. By assigning a score based on these criteria, your team can instantly identify where capital is trapped and which invoices demand immediate, focused attention. This moves your team from chasing every late invoice to strategically prioritizing efforts where they will have the greatest financial impact.

We utilize a framework called the AR Risk Segmentation Matrix. It enables CFOs and their teams to rapidly classify outstanding invoices and determine the most effective initial action.

AR Risk Segmentation Matrix

Risk Category | Invoice Age (Days Past Due) | Client Profile | Recommended First Action |

|---|---|---|---|

Tier 1: Low Risk | 1-30 Days | High-value, long-term client with a strong payment history. | Gentle, automated email reminder. Focus on relationship preservation. |

Tier 2: Moderate Risk | 31-60 Days | Solid client, but with occasional payment delays or slow communication. | Personalized email from the account manager, followed by a professional phone call. |

Tier 3: High Risk | 61-90 Days | History of late payments, low responsiveness, or a smaller, transactional relationship. | Firm, direct phone call from the AR team. Outline a clear payment deadline. |

Tier 4: Critical Risk | 90+ Days | Consistently non-responsive, known financial issues, or a history of disputes. | Formal demand letter from finance leadership. Prepare for potential legal escalation. |

This matrix is not just for sorting invoices; it is a clear playbook that ensures your team applies the right level of pressure to the right accounts at the right time.

A data-driven risk model transforms your AR process from a cost center into a strategic function dedicated to cash flow optimization. It provides the clarity needed to apply appropriate pressure to the correct accounts at the optimal time.

This diagnostic phase is critical. We explore this in greater detail in our guide on https://www.resolutai.com/blog/account-receivable-aging. When you understand who owes you money, why they haven't paid, and their value to your firm, you can build a collections process based on strategy, not stress.

Building a Disciplined Collections Cadence

A single, generic reminder email is easily ignored. A systematic, multi-channel approach is not.

The key to moving from reactive chasing to proactive control is a disciplined collections cadence. This is not about random emails; it is a planned sequence of communications that adapts to client risk profiles and executes with operational precision.

A high-value, low-risk client requires only a gentle nudge. A chronically late, high-risk account demands a more direct and escalating series of touchpoints. The goal is to build a predictable process that communicates clear expectations without damaging the client relationship. This operational rigor is the foundation of a healthy cash flow cycle.

The process begins by converting your risk assessment into a clear, prioritized action plan.

This strategic flow ensures your team’s time is focused on accounts that pose a genuine financial risk, not diluted by chasing every outstanding invoice.

Designing a Multi-Channel Outreach Strategy

Relying solely on email is a common mistake. An effective cadence must integrate multiple channels to ensure the message is received.

Here is a structured cadence for a moderate-risk account:

- 7 Days Before Due Date: Automated email reminding the client of the upcoming payment. This is a professional courtesy.

- 3 Days After Due Date: Automated follow-up email confirming the invoice is past due. Include a direct payment link.

- 10 Days After Due Date: Automated SMS with a link to the invoice. This often cuts through email noise.

- 21 Days After Due Date: Personal phone call from the account manager or AR team to understand the delay and secure a payment commitment.

This multi-channel approach gradually and professionally increases pressure. For detailed guidance on messaging, our guide covers the essentials of a professional reminder for payment.

Scripting for Clarity and Control

Each touchpoint in your cadence requires a clear objective and a pre-defined script or messaging framework. This ensures consistency and removes emotion from the collections process.

The Pre-Due Nudge (Email):

Subject: Invoice [Invoice Number] Due in 7 Days >Body: Hi [Client Name], a reminder that invoice [Invoice Number] for [Amount] is due on [Due Date]. You can view and pay the invoice here: [Link to Portal].

The Firm Post-Due Reminder (Email):

Subject: Invoice [Invoice Number] is Overdue >Body: Hi [Client Name], this is a follow-up regarding invoice [Invoice Number], which was due on [Due Date]. Please submit payment via our portal: [Link to Portal]. If you have any questions, please let us know.

The Escalated Phone Call:

Objective: Secure a specific payment date. >Opening: "Hi [Client Name], I'm calling from [Your Firm] about invoice [Invoice Number] for [Amount], which is now 21 days past due. I wanted to connect to confirm if there was an issue and when we can expect payment."

A structured approach makes your collections process scalable, predictable, and less stressful for your team.

The Role of Accounts Receivable Automation

Executing these cadences manually across hundreds of clients is impractical and prone to human error. This is where accounts receivable automation is essential.

AI AR automation platforms execute complex, multi-channel cadences with precise timing. They can automatically segment clients, trigger outreach based on risk, and log every interaction without manual intervention.

This frees your finance team from repetitive follow-ups, allowing them to focus on high-value conversations and strategic negotiations with clients who require personal attention.

Platforms with QuickBooks AR automation, for instance, integrate directly with your accounting software, pulling invoice data and pushing payment updates in real-time. This transforms your AR process from an administrative burden into a system that will measurably reduce DSO and improve cash flow.

When standard reminders fail, the process shifts from process to negotiation. For finance leaders, this requires a firm but flexible approach. These conversations are not just about collecting a single late invoice; they are about protecting cash flow without destroying a valuable client relationship.

Late payments are a systemic problem. Across North America, nearly half of all B2B invoices are overdue. In the U.S., that figure is 44%. In this environment, you must master direct, productive negotiation. To understand the scale of this issue, it is worth reviewing the B2B accounts receivable landscape.

Preparing for the Collections Call

Successful collection calls are determined by preparation. Entering a conversation unprepared weakens your position and signals a lack of control. The goal is to have all necessary information readily available to lead with calm authority.

Before any call, your team needs a complete client dossier, including:

- A full invoice history: Not just what is overdue, but their entire payment record.

- All prior communications: Every automated reminder, email, and note from previous calls.

- Original contract and SOW: Be prepared to reference the exact terms they agreed to.

- Key relationship contacts: Identify both the decision-maker and your day-to-day contact.

This preparation transforms a potentially confrontational call into a straightforward, data-driven conversation.

Structuring Payment Plans and Partial Payments

When a client faces genuine cash flow challenges, demanding full payment immediately is often counterproductive. A structured payment plan can be a pragmatic tool to secure cash over a defined timeline while providing the client a viable path forward.

A good payment plan is simple and documented. For example, if a client owes $25,000 on an invoice that is 60 days past due, a plan might start with an immediate 25% partial payment of $6,250 as a sign of good faith, with the remaining balance split over the next three to four weeks.

Key takeaway: Every negotiated agreement must be documented and confirmed in writing immediately following the conversation. An email summarizing payment dates and amounts creates an official record and prevents future "misunderstandings."

This approach provides an immediate boost to your cash flow and locks in a firm, mutually-agreed upon collections timeline. For more on this, our guide on creating a payment plan agreement template is a useful resource.

Managing and Resolving Disputes

If non-payment is due to a service dispute or billing error, the collections process must halt immediately, and a resolution process must begin. A disputed invoice is effectively uncollectible until the root cause is resolved.

The key is to diagnose and route the issue quickly. If it's a billing mistake, direct it to finance for correction. If the client is unhappy with the service, escalate it to the Client Services or Sales lead who owns the relationship.

This is where AR software for professional services is invaluable. The best platforms allow your AR team to flag a disputed invoice, pause automated communications, and assign a resolution task to the appropriate person within the system. This creates a clear audit trail and ensures disputes are resolved quickly, unblocking payment and getting collections back on track.

Make It Easy for Them to Pay You

All the follow-up calls and firm negotiation in the world won't matter if the payment process itself is difficult. If paying you is confusing or outdated, you are creating your own collections problem.

Often, a late payment is a result of friction, not unwillingness. The goal should be simple: make paying your invoice the easiest task on your client’s to-do list.

Give Clients a Consumer-Grade Payment Experience

Clients expect the same seamless experience in B2B transactions as they get in consumer contexts. A clunky portal or forcing them to mail a physical check introduces delay. Every extra click is an opportunity for your invoice to be deferred.

Firms with the healthiest cash flow are obsessed with removing these barriers. An effective payment portal must be clean, intuitive, and flexible.

- Offer Multiple Ways to Pay: Accept ACH, all major credit cards, and digital wallets. The more options, the lower the friction.

- Design for Mobile: Decision-makers approve payments on the move. Your payment page must function flawlessly on a smartphone.

- Provide One-Click Access: Every reminder email should contain a direct, secure link to pay a specific invoice. No logins or invoice numbers required.

This is not just about convenience; it is about speed. When a client can settle a $15,000 invoice in under 90 seconds from their phone, your Days Sales Outstanding (DSO) will decrease.

The Hidden Power of Automated Cash Application

Collecting payment is only half the battle. Applying that cash correctly to the right invoice—a process known as cash application—is where many finance teams are buried in manual work.

For any firm operating at scale, integrating your payment portal with your accounting software is non-negotiable. Strong QuickBooks AR automation, for example, ensures that when a payment is made, it is instantly and accurately reconciled in your general ledger.

Real-time cash application provides a clear, up-to-the-minute view of your cash position—vital for accurate forecasting. Without it, you are making strategic decisions based on outdated data.

Automated reconciliation also prevents the cardinal sin of collections: chasing a client who has already paid. That is a fast way to damage a client relationship.

Turn Your Invoices into an Interactive Hub

A static PDF invoice is obsolete. Modern AR software for professional services transforms the invoice from a bill into an interactive online hub—a single source of truth for the transaction.

In this digital space, your client should be able to:

- See a full history of all their past and present invoices.

- Download receipts or account statements on demand.

- Ask a question or flag a dispute directly on the invoice page.

This last feature is a game-changer. When a client can ask a question directly on the invoice, it gets instantly routed to the right person. This prevents a minor query from turning into a 30-day payment delay.

This approach elevates the payment process from a one-way demand into a two-way communication channel, proactively clearing hurdles to payment.

Using AR Automation to Drive Performance

A sound strategy requires consistent execution to bring cash in the door. Accounts receivable automation transforms your collections process from a manual, inconsistent task into a disciplined system for financial control.

Think of it less as sending robotic reminders and more like conducting an orchestra, ensuring the right actions occur at precisely the right moments.

This fundamentally changes how your team operates, creating a clear distinction between two modes: autopilot and co-pilot.

- Autopilot Mode: For the majority of your accounts—low-to-moderate risk clients—the system handles everything. It sends reminders and multi-channel pings with perfect timing and zero human effort.

- Co-pilot Mode: For high-value, high-risk, or disputed invoices, the system acts as a co-pilot. It flags the account, gathers all relevant history, and presents it to a team member for nuanced, relationship-critical conversations.

This dual-mode approach delivers efficiency without sacrificing the human touch where it matters most.

From Manual Tasks to Intelligent Workflows

The best AR software for professional services is built around intelligent workflows, not just time-based triggers. These are conditional rules that react to client behavior.

For example, a workflow can automatically pause communications the moment a client disputes an invoice, while simultaneously assigning a resolution task to the account manager.

Another workflow might escalate an account from email to an SMS and phone call sequence if initial emails are not opened within 48 hours. This orchestration ensures your team's time is spent on strategic intervention, not routine chasing. This is how you truly improve cash flow, by plugging the leaks inherent in manual processes. For practical examples, see these business process automation examples in finance.

Defining the KPIs That Matter

If you cannot measure collections performance, you cannot manage it. Finance leaders must focus on a handful of core Key Performance Indicators (KPIs) that provide a clear view of AR health.

Tracking the right metrics allows you to stop guessing and start making data-driven decisions. These numbers reveal the true velocity of your cash flow and the efficiency of your collections, allowing you to fine-tune your strategy in real-time.

These are the three KPIs you must monitor:

- Days Sales Outstanding (DSO): The classic measure of collections efficiency. It shows the average number of days it takes to get paid. A lower DSO means you are converting revenue into cash faster. When a firm cuts its DSO from 60 to 45 days, it unlocks 15 days of operating cash.

- Collection Effectiveness Index (CEI): This provides a more nuanced view than DSO. It measures how much of the money that was available to be collected you actually collected in a given period. A CEI consistently above 90% signals a high-performing collections process.

- Aged Receivables Percentage: This KPI tracks the portion of your total AR in high-risk buckets (e.g., 90+ days past due). An increasing percentage is a major red flag. Firms that adopt AI AR automation often see a 25-40% reduction in their 90+ day bucket within the first six months.

Effective AR software presents these KPIs on a real-time dashboard. This visibility gives CFOs and Controllers true command over their cash flow, empowering them to identify issues early and make adjustments before they impact the bottom line.

Answering Your Key AR Questions

As a CFO or Controller, you must balance high-level strategy with daily operational details. A few critical questions about accounts receivable consistently arise. The answers involve blending smart technology with a clear strategy for when to escalate and when to partner.

At What Point Should We Escalate to a Collections Agency?

This should be a data-driven trigger, not an emotional decision. The industry standard is to consider an agency when an invoice is 90-120 days past due, particularly if the client has become non-responsive.

Before escalating, confirm there are no unresolved disputes and that a documented final notice has been sent. This provides the agency with a clean case. Also, assess if the invoice amount justifies the agency's contingency fee.

A good accounts receivable automation platform can automatically flag accounts that meet your escalation criteria, send the final notice, and package the communication history. Often, this final automated step secures payment without needing an agency.

How Can We Collect Without Damaging Client Relationships?

The key is to separate the relationship from the transaction. Frame collections as a standard business process, not a personal confrontation. It is simply how your firm operates: calm, confident, and consistent.

Automation removes emotion and inconsistency from early, routine reminders. Every client receives the same professional, timely follow-ups. When a direct conversation is necessary, your team can engage as problem-solvers, not enforcers.

Instead of demanding, "You need to pay this now," shift the conversation. Ask, "It looks like this invoice is overdue. Is there anything we can do to help get this resolved?" Offering flexibility, such as a structured payment plan, maintains professional respect and protects the long-term client relationship.

What Is the Single Biggest Mistake in AR Management?

The most common and costly mistake is inconsistency. When follow-up is manual and sporadic, you teach clients that your payment terms are suggestions.

This unpredictability trains them to pay you last because there are no clear consequences for delay. An automated, predictable collections cadence sends a powerful message: your firm is organized, serious about its finances, and expects to be paid on time. Consistency is the most direct lever you can pull to reduce DSO.

How Is AI AR Automation Different from Simple Reminders?

Simple reminder software is a blunt instrument, sending templated emails on a fixed schedule. AI AR automation is an orchestration engine.

An AI-driven system analyzes a client's payment history, communication engagement, and other data points to predict which invoices are at risk of delinquency.

Based on this insight, it personalizes outreach. An AI AR automation platform might intelligently adjust reminder timing, switch communication channels, or even modify message tone to improve response. It also manages complex back-end work like automated cash application and dispute routing. It transforms your AR function from a cost center into a strategic asset.

--- Resolut automates AR for professional services—consistent, accurate, and human.