Optimize Accounts Receivable Process: Reduce DSO

Optimize accounts receivable process with this 2026 guide for CFOs. Learn step-by-step KPIs, automation, & tech to reduce DSO and improve cash flow.

Cash flow problems in professional services often start long before a client misses payment. They start when billing is delayed, invoice data is inconsistent, follow-up lives in someone’s inbox, and disputes sit unresolved because no one owns the next step.

That’s why accounts receivable deserves operator attention, not just accounting cleanup. Businesses worldwide lose approximately $200 billion annually to inefficient AR processes, and 1 in 10 invoices remain unpaid, according to HighRadius on collecting accounts receivable. For firms that run on utilization, payroll, and project timing, that gap between earned revenue and collected cash is where growth gets squeezed.

For a professional services firm, the way to optimize accounts receivable process performance isn’t complicated. But it does require discipline. Measure the current state. Redesign the workflow. Choose technology that removes friction instead of adding another dashboard. Then implement it in phases your team can absorb.

The High Cost of an Unoptimized AR Process

Professional services firms can post strong revenue and still run short on cash. The gap usually shows up in accounts receivable first.

An unoptimized AR process creates financing pressure inside the business. Work gets delivered, invoices go out late, approvals stall, disputes sit open, and cash arrives on a schedule the firm did not choose. In a services model with fixed payroll and uneven client payment behavior, that delay reduces control fast.

The cost is not limited to collections effort. It hits staffing decisions, partner draws, tax planning, and the ability to fund growth without outside capital. I have seen firms with healthy margins tighten hiring because billing and collections were too inconsistent to trust the cash forecast.

The problem gets worse in firms with a concentrated client base. If a few accounts drive a large share of monthly billings, one delayed payment can change the operating plan for the month. Add incomplete billing support, a disputed milestone, or remittance that has to be matched by hand, and the finance team shifts from running a process to chasing exceptions.

That is why AR should be managed as an operating workflow tied to service delivery, not as a clerical task at month end. The firms that manage your cash flow effectively usually do three things well. They invoice quickly, assign clear ownership for follow-up and dispute resolution, and remove avoidable friction from payment.

One metric sits underneath all of it. If you need a tighter definition, this guide to what DSO means in practice gives the right baseline. DSO is not just a finance KPI. In a professional services firm, it reflects billing discipline, contract clarity, client communication, and how quickly the team resolves exceptions.

Poor AR performance also distorts management behavior. Leaders start delaying software purchases, watching payroll dates too closely, and making conservative decisions that have nothing to do with demand. The business starts acting cash-poor even when the pipeline is healthy.

That is the actual cost. Weak AR does not just slow collections. It limits the number of good decisions a firm can make with confidence.

Current-State Diagnostics Auditing Your AR Performance

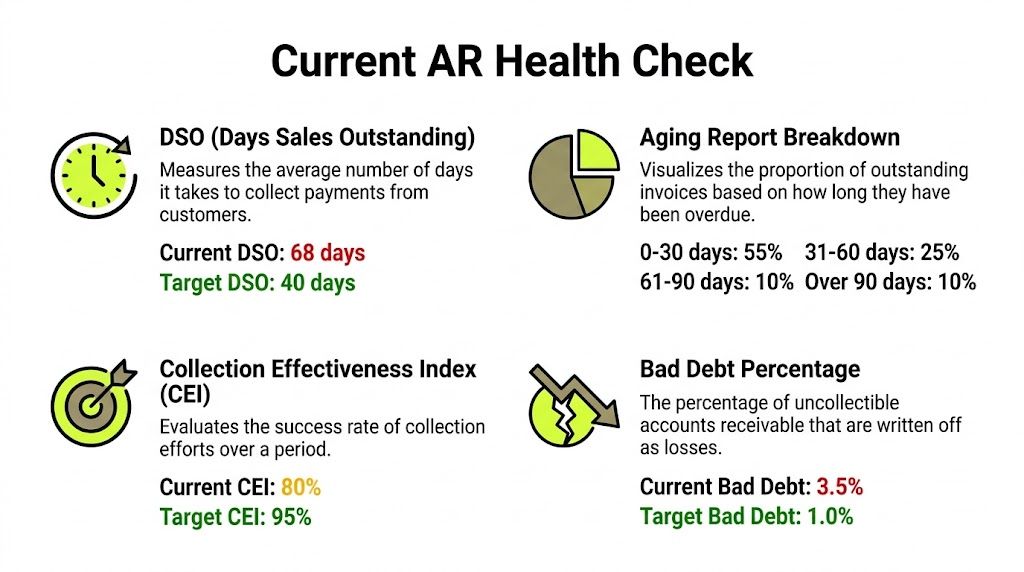

Top performers collect faster for a reason. APQC reports that top-performing organizations hold DSO at 30 days or less, while median performers sit at 45 days, based on its accounts receivable benchmark data. That spread usually comes from process design, not effort.

A useful diagnostic starts with a tight scorecard and a process map. In professional services, AR breaks down across proposal terms, project delivery, billing readiness, invoice submission, collections, cash application, and dispute resolution. If you only measure the back end, you miss where the delay starts.

Start with DSO

Days Sales Outstanding, or DSO, measures how many days receivables stay open after a sale. Finance leaders start here because DSO captures several operating variables in one number: invoice timing, client payment behavior, dispute cycle time, and follow-up discipline.

For a services firm, a high DSO usually points to one or more specific breakdowns:

- Billing lag: Time entry review, project signoff, or partner approval holds invoices after the work is already billable.

- Invoice friction: Missing backup, wrong billing contacts, missing PO numbers, or inconsistent submission methods delay acceptance.

- Collection inconsistency: Follow-up depends on who notices the aging, not on a defined cadence.

- Dispute drift: Finance, project leads, and account owners do not close client questions fast enough.

Treat DSO as a symptom first. Then trace the delay to its source. If invoices are going out ten days late, collections cannot make that up.

Use CEI to judge execution

DSO shows the outcome. Collection Effectiveness Index, or CEI, shows how well the team converted available receivables into cash during the period.

The formula is:

(Beginning AR + Monthly credit sales – Ending AR) ÷ (Beginning AR + Monthly credit sales – Ending AR from bad debt) × 100

APQC sets the target for an excellent CEI at 85% to 95%.

That makes CEI useful for operating review. A healthy CEI usually means the basics are under control:

- Invoices go out on time

- Follow-up starts early

- Cash is applied quickly

- Ownership of disputes is clear

A weak CEI does not automatically mean the team needs more people. In many firms, the issue is workflow drag. Collectors are checking invoice status by hand, waiting on delivery teams for backup, or trying to match remittances from incomplete payment detail. If that sounds familiar, tighten the handoffs before adding headcount. A documented set of accounts receivable procedures for billing, collections, and cash application usually fixes more than another inbox full of reminder emails.

Add AR turnover for collection velocity

AR Turnover Ratio measures how often receivables convert to cash over a year. The formula is straightforward:

Net Credit Sales ÷ Average Accounts Receivable

Used alongside DSO and CEI, turnover helps separate growth from execution. Revenue can rise while receivables slow down. That pattern shows up often in firms that scale delivery faster than they scale billing controls.

Here is a practical way to read the core metrics together:

Metric | What it tells you | Benchmark signal |

|---|---|---|

DSO | Average days to collect receivables | Top performers are 30 days or less |

CEI | How effectively receivables are collected in a period | Excellence is 85% to 95% |

AR Turnover Ratio | How often receivables convert to cash annually | Higher turnover means faster cash conversion |

One metric rarely gives a clean answer. A stable DSO with weak CEI can point to collection inconsistency hidden by fresh billings. A decent turnover ratio with poor aging in one client segment can point to concentration risk. The point of diagnostics is to isolate which part of the machine needs work.

Don’t ignore aging and bad debt

The aging report shows where process failure becomes visible. Review it by client, partner, project manager, invoice type, and aging bucket. That is how you find patterns that summary KPIs hide.

In services firms, I often see one of three aging profiles:

- Current bucket looks healthy, then drops sharply after 30 or 60 days. Follow-up is starting too late.

- Balances cluster around disputed milestones or change orders. Contract terms or approval workflows are weak.

- Older balances sit with a small number of clients. Concentration risk is being managed reactively.

Bad debt belongs in the same review. Write-offs should be split between true credit loss and process failure. If invoices were late, unsupported, disputed for weeks, or sent to the wrong contact, that is not just bad luck. It is an operating issue with a margin impact.

A monthly diagnostic cadence keeps the review useful:

- Track DSO trend: One month can mislead. Direction matters more.

- Review CEI: Test whether the team is converting available receivables efficiently.

- Check turnover: Confirm cash conversion is keeping pace with sales.

- Read aging by segment: Look for client concentration, dispute clusters, and billing bottlenecks.

- Classify write-offs: Separate credit risk from preventable process errors.

The goal is control. A small scorecard, tied to the actual AR workflow, gives you that. Without it, teams end up treating collections as a cleanup exercise instead of managing receivables as an end-to-end operating process.

A Blueprint for High-Performance AR Workflows

A services firm can post healthy revenue and still run short on cash if AR work breaks between project delivery, billing, collections, and cash application. The fix is process control. Teams need a defined operating model with clear owners, service levels, and escalation rules.

In professional services, I break the workflow into four linked motions: invoice readiness, payment execution, collections control, and dispute resolution. If any one of those runs late, cash timing slips and finance ends up chasing symptoms instead of managing the system.

Billing needs speed and precision

Invoice quality starts before the invoice exists.

Firms lose time when hours are still unapproved, expenses lack support, milestone language does not match the statement of work, or the billing contact has changed and nobody updated the record. By the time the invoice is finally corrected, the due date may still say net 30, but the effective collection window is already shorter.

A stronger billing workflow includes:

- Pre-bill validation: Confirm time, expenses, approvals, tax treatment, PO numbers, and required backup before invoice creation.

- Defined release timing: Set a service-level target from billable event to invoice delivery. In many firms, that should be measured in days, not weeks.

- Client-specific formatting rules: Match the invoice to how the client approves spend, including project codes, matter IDs, milestones, or cost centers.

- Clean delivery controls: Send to the right AP contact and the right channel every time, with remittance instructions and due date visible.

Many firms gain the fastest improvement. They do not need better collections language. They need fewer preventable invoice defects.

For some accounts, payment terms can also support faster conversion. Corcentric notes that automated billing, broader payment options, and selective use of terms such as 2/10 net/30 can improve productivity in receivables operations and shorten the path to cash for the right customer segments, as outlined in its AR best-practice guidance. The trade-off is margin. Early-pay discounts only make sense when the financing benefit or risk reduction is worth the cost.

If the workflow is still tribal knowledge, document it. A practical starting point is a written set of account receivable procedures that defines handoffs, approval points, and exception handling.

Payment collection should remove effort for the client

Clients pay faster when the path to payment is obvious.

If they have to ask for wiring instructions, search old emails for an invoice copy, or guess which balance to clear, delay is predictable. Good AR design removes those points of friction and gives finance better control over matching and follow-up.

Workflow area | Weak setup | Strong setup |

|---|---|---|

Payment method | Limited options, usually check or manual bank transfer | Options matched to client preference, such as ACH, card, wire, or portal payment |

Invoice access | PDF buried in email threads | Direct digital access to the invoice and supporting detail |

Payment matching | Cash posted later at the account level | Payment tied to the specific invoice when received |

Reconciliation | Unidentified cash reviewed in batches | Frequent review with quick exception handling |

Correct application matters as much as collection speed. In a services environment, a misapplied payment can create a false past-due balance, trigger unnecessary dunning, and force the account team to repair a problem finance created internally.

Collections should be systematic

Collections work best as a scheduled operating cycle, not a reaction to aging reports.

Set the cadence in advance. Assign owners by account segment. Standardize the message library. Escalate based on invoice age, value, and client history. That gives the team consistency without forcing every client into the same script.

A practical structure looks like this:

- Pre-due reminder: Confirm receipt, attach the invoice, and restate payment methods.

- Due-date notice: Restate amount due and expected payment date.

- Early overdue contact: Identify whether the issue is approval delay, missing documentation, short-pay, or dispute.

- Escalation: Route high-risk items to the account lead, partner, or finance manager based on a defined threshold.

Segmentation matters here. Strategic accounts may need account-manager involvement early. Smaller repeat clients usually respond well to automated reminders and a short exception queue. Habitually slow payers need tighter terms, earlier contact, and more discipline around work-in-progress release.

Disputes need ownership

Disputes should sit in a controlled queue with one accountable owner per item.

Without that, invoices bounce between project managers, finance, and client contacts until everyone loses track of the next action. Cash stalls. So does trust.

The operating design is straightforward:

- Log the issue clearly: Capture dispute type, amount, client contact, and date raised.

- Route by cause: Billing error goes to finance. Scope or milestone disagreement goes to delivery or the engagement lead.

- Set internal deadlines: Each dispute category needs a response target and an escalation point.

- Restart collection on resolution: Once resolved, confirm the revised invoice or approval and move the item back into the collection cadence immediately.

The trade-off is administrative effort up front versus fewer long-tail receivables later. I would take the front-end discipline every time. In professional services firms, unresolved disputes tie up not just cash, but partner attention, project margin review, and client relationship capacity.

High-performance AR is not one workflow. It is a set of connected controls that move an invoice from approved work to applied cash with as little rework as possible. That is the standard to build toward.

Selecting Your AR Automation Technology Stack

Technology should compress the AR cycle. If it adds another admin layer, skip it.

For professional services firms, the right stack supports the operating model you already designed. It should fit milestone billing, retainer invoicing, client-specific approval paths, and exception handling without forcing finance back into spreadsheets. Teams in the $3M to $50M range usually do not need the broadest platform on the market. They need one that keeps invoice status, collection activity, and cash posting accurate across systems.

Buy for integration first

Start with system fit, not feature volume.

If your accounting platform, project system, and payment data do not stay in sync, collectors work from stale balances, clients get the wrong reminder, and finance spends month-end cleaning up preventable errors. In firms using QuickBooks, Xero, NetSuite, or project accounting tools, that failure point shows up fast.

Review AR software against a short list of control points:

- Accounting sync: Invoices, credits, payments, and client records need to update reliably in both directions.

- Cash application design: The system should speed up matching and flag exceptions clearly.

- Collections workflow control: Finance needs to set timing, message rules, task ownership, and escalation paths.

- Client payment experience: Payment links, invoice access, and remittance instructions should be easy to follow.

- Exception handling: Disputes, short pays, missing remittance data, and unapplied cash need a visible queue with ownership.

User interface still matters. But in AR, clean screens do not fix broken handoffs. The better question is whether the tool makes the next action obvious for both finance and the client.

Apply AI to prioritization, not novelty

AI matters when it improves queue management and timing.

A useful system should analyze payment patterns, dispute history, and response behavior so the team can act earlier on accounts that are drifting. It should also help separate low-risk reminders from accounts that need human contact, tighter follow-up, or escalation. That improves collector productivity without turning every client touchpoint into a generic automated nudge.

The practical test is simple. Can the platform help answer questions like these?

Question | Why it matters |

|---|---|

Which accounts are likely to slip before they become overdue? | Early contact is usually easier and less disruptive than late escalation |

Which clients respond better to email, SMS, or human outreach? | Channel choice affects response rates and client experience |

Which invoices need a soft reminder versus direct escalation? | Tone should match account history, amount, and relationship value |

Where are repeat disputes or matching errors occurring? | Process fixes remove friction faster than repeated follow-up |

This capability is how AI AR automation earns its place. It supports judgment. It does not replace it.

Good automation handles routine volume. Good AI helps your team focus attention where human judgment changes the outcome.

Evaluate platforms by operating fit

Vendor selection usually breaks down when firms buy for the demo instead of the day-to-day workload. A long feature list means little if finance cannot configure the tool, trust the data, or adjust workflows without outside help.

Use five tests during evaluation:

- Implementation reality Can your team set up billing flows, reminders, user roles, and approval rules without a large consulting project?

- Workflow flexibility Can the system support different client segments, contract structures, and exception paths?

- Leadership visibility Can finance leaders see aging, disputed balances, collector activity, payment promises, and unapplied cash in one view?

- Human review controls Can staff approve, pause, or override outreach when context matters?

- Client experience Does the payment process reduce friction, or does it create another reason for clients to delay?

If you are comparing categories, this overview of accounts receivable automation software is a useful starting point. One option in that market is Resolut, which combines billing workflows, multichannel outreach, cash application, and risk identification in one platform. For many services firms, consolidation matters because every additional point tool creates another handoff to monitor.

The best AR stack is the one your team will run with discipline for the next two years. In practice, ROI comes from shorter cycle times between invoice release, follow-up, payment receipt, and reconciliation. That is an operating gain, not a software feature.

An Operator's Roadmap to AR Automation

Implementation is where AR projects either become a significant financial advantage or turn into another underused finance tool.

The safest path is phased. Don’t automate everything at once. Start where process friction is highest and behavior change is easiest to support.

Phase one focuses on billing and cash application

The first phase should tighten the two points that most directly affect cash visibility: invoice release and payment posting.

When invoices go out faster and payments are matched correctly, finance gets immediate control benefits. The team sees what’s open, what’s paid, and where follow-up is needed. That cleans up the queue before you layer in more advanced collections logic.

The early implementation checklist is usually straightforward:

- Standardize invoice triggers: Define when work is billable and who approves release.

- Confirm customer master data: Billing contacts, terms, and remittance requirements need to be current.

- Improve payment routing: Make sure clients know exactly how to pay.

- Automate matching where possible: Reduce the manual effort tied to cash application.

This phase also reveals process quality. If invoice data is inconsistent or client records are weak, automation will expose it quickly. That’s helpful. Better to fix root causes early than to automate confusion.

Phase two adds collections workflow and internal routing

Once invoice and payment data are more reliable, bring in automated reminders, escalation rules, and exception routing.

At this point, the goal isn’t to send more messages. It’s to stop relying on memory and manual lists. Every invoice should move through a defined path based on due date, payment status, dispute status, and account context.

A solid operating model usually includes these decisions:

Area | Control question |

|---|---|

Reminder timing | When does outreach start before and after due date? |

Message ownership | Which communications can run automatically, and which need review? |

Escalation rules | What triggers account-lead or controller involvement? |

Dispute routing | Who owns pricing, scope, PO, or billing errors? |

This is also the point where finance should coordinate with sales or account leadership. Cross-team collaboration improves outcomes because sales teams with access to payment history can step in earlier on payment term violations and often resolve unpaid invoices faster than collections teams acting alone, as noted by Zenskar’s accounts receivable process guidance.

That isn’t a reason to hand collections to sales. It’s a reason to give client-facing teams controlled visibility and a clear escalation path.

The collection note from an account lead often works because it carries relationship context. Finance should decide when to use that lever.

Phase three defines autopilot and co-pilot boundaries

Teams adopt automation faster when they know where human judgment still matters.

Routine reminders, invoice delivery, cash matching, and basic escalation can run on autopilot. Sensitive accounts, large balances, strategic clients, and disputed invoices often need a co-pilot model where the system recommends action and a human approves it.

That split reduces fear inside the finance team. Staff don’t feel replaced. They feel relieved of repetitive work and more useful on exceptions that need real judgment.

A practical rollout cadence looks like this:

- Pilot with a narrow client group

- Review exceptions weekly

- Tune templates, routing, and timing

- Expand by segment, not all at once

- Keep one owner accountable for adoption

Most firms get into trouble when implementation is treated as a software event. It’s an operating change. The team needs cleaner habits, clearer ownership, and feedback loops that hold after go-live.

From Optimization to Orchestration Advanced AR Strategies and ROI

Once the core workflow is stable, the next layer is orchestration. That means the system doesn’t just process activity. It helps finance anticipate risk, shape outreach, and escalate with better judgment.

In practice, advanced AR control comes from three capabilities.

Predict risk before invoices age badly

The first is predictive identification of payment risk. Instead of waiting for a client to become overdue, finance can flag patterns earlier and intervene with the right message, contact, or payment path. That changes AR from reactive collections to controlled prevention.

For professional services firms, this is especially useful with clients that pay unevenly across projects or approval cycles. A static aging report shows what already happened. Predictive signals help the team act while there’s still room to preserve timing and tone.

Escalate selectively and with structure

The second is authoritative escalation. Not every late account requires a legal tone, and using one too early can damage a good client relationship. But some accounts do require firmer handling once routine outreach fails.

That’s where a structured escalation path matters. Finance should know when an internal escalation is enough, when executive involvement is appropriate, and when outside support becomes part of a commercial process. Firms that need a reference point on that end of the spectrum can review how Commercial Receivables Management Services are typically framed in a legal context.

Think in scenarios, not vanity ROI

The third is ROI discipline. Most firms don’t need a heroic transformation case. They need a believable operating case.

Consider two common examples:

- A growing advisory firm tightens invoice release, standardizes reminders, and gives account leads controlled visibility into payment status. The result is simpler forecasting and less time spent chasing internal answers before contacting clients.

- A multi-partner services practice centralizes disputes, improves payment routing, and automates cash application. Finance spends less time reconciling receipts and more time working genuine exceptions.

Neither example depends on aggressive collections. Both depend on orchestration. The firm knows what’s open, what’s blocked, who owns the next action, and when escalation is justified.

That’s the ultimate end state. Not just lower DSO. Better control.

Resolut automates AR for professional services with a practical mix of workflow automation, payment orchestration, and human review where it matters. If your firm wants more predictable collections, cleaner reconciliation, and a process that stays consistent without becoming impersonal, Resolut is built for that balance.