Financial Statement Impact: AR, Working Capital & Automation

Discover the financial statement impact of AR on P&L, balance sheet & cash flow. CFOs: Reduce DSO & boost working capital with automation in 2026.

Your P&L says the month was solid. Revenue is up, utilization looks healthy, and the team delivered the work.

Then payroll hits, partner distributions are due, and cash feels tighter than it should.

That gap is where many professional services firms live for longer than they should. The problem usually isn't revenue production alone. It's the lag between booking revenue and collecting it, plus the accounting effects that make the business look stronger on paper than it feels in the bank.

For a CFO, Controller, or firm owner, that gap creates a specific kind of frustration. You can see profitability. You can defend the revenue. But you still have to slow hiring, delay vendor payments, or lean on a line of credit because receivables are carrying too much weight.

This is the financial statement impact of accounts receivable. It isn't just a collections nuisance. It changes what your statements say about earnings, liquidity, and working capital. It also changes the decisions you make from those statements.

The Widening Gap Between Revenue and Cash

A common version of this problem looks like this. A consulting firm closes the month with strong billings, but cash receipts don't follow at the same pace. The owner sees revenue on the income statement and expects breathing room. Instead, the finance team spends the next few weeks managing timing risk.

That usually starts as an operational issue. Invoices go out later than they should. Client approvals take longer than expected. A dispute sits with an engagement manager who is focused on delivery, not collection. None of that looks dramatic in isolation. Together, it weakens control.

What the owner feels first

The first symptom is rarely a bad debt write-off. It's unpredictability.

You start making decisions with partial confidence. Can you add staff next quarter. Can you fund a software rollout. Can you make partner distributions without compressing operating cash. These aren't abstract planning questions. They're direct consequences of how quickly billed work turns into collected cash.

For firms trying to tighten that operating rhythm, practical reading on cash flow forecasting and collections is useful because it frames the issue as a management discipline, not just an accounting cleanup exercise.

Healthy revenue with weak collections is not a growth story. It's a working capital problem wearing a revenue label.

Why this matters on the statements

The balance sheet can show rising accounts receivable at the same time cash remains constrained. The income statement can show profit while the cash flow statement tells a much less comfortable story. That's why owners who rely on one statement in isolation often feel blindsided.

Working capital management sits right in the middle of that tension. If you need a concise refresher on the operating side of the equation, this overview of working capital management is worth keeping close to your monthly review process.

What matters most is this. Revenue recognition and cash collection are connected, but they aren't the same event. Until AR is managed with discipline, the statements can drift away from operating reality.

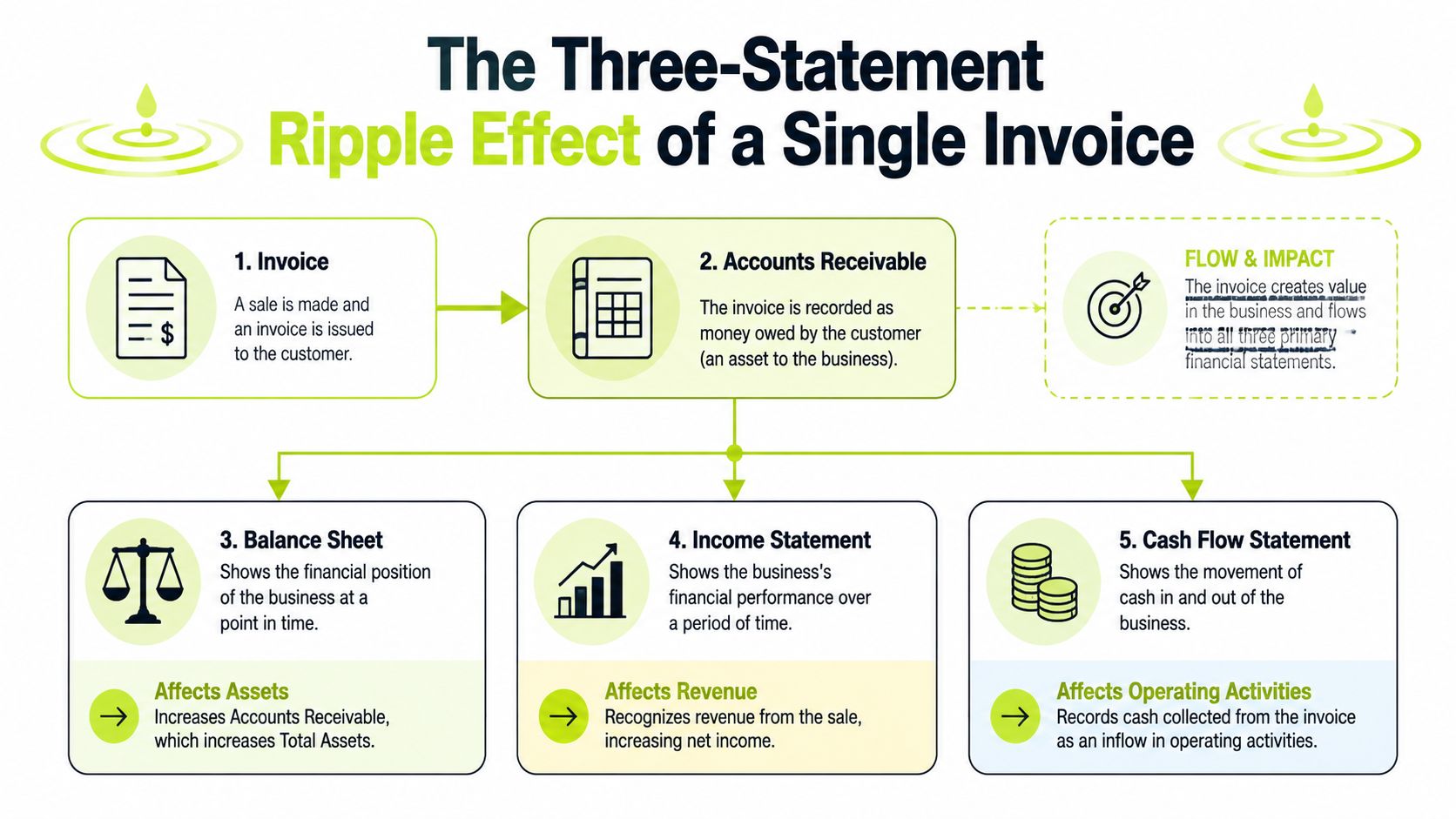

The Three-Statement Ripple Effect of a Single Invoice

Take a simple example. Your firm completes a project milestone and issues a $10,000 invoice.

At the moment the invoice is sent, accounting records revenue. That's correct under accrual accounting when the performance obligation has been satisfied. But no cash has arrived yet.

What happens immediately

The invoice touches all three financial statements, but not in the same way.

- Income statement Revenue increases by $10,000. If costs have already been recognized appropriately, net income improves.

- Balance sheet Accounts Receivable increases by $10,000. That's an asset, but it's an asset made of expectation, not cash.

- Cash flow statement There is no cash inflow at issuance. The operating cash benefit doesn't appear until the client pays.

This is the core distinction many owners understand intuitively but don't always use rigorously in decisions. Revenue can be earned, billed, and reported while liquidity remains unchanged.

If your team needs a clean accounting baseline for when revenue should enter the books, the revenue timing rules matter. This primer on the revenue recognition principle is a good technical companion.

When the invoice doesn't convert to cash

The financial statement impact becomes more serious when collection slips or fails entirely. When 1 in 10 invoices go unpaid, it creates a direct negative ripple effect, reducing net income, increasing bad debt expenses, and inflating the 'Accounts Receivable' asset on the balance sheet while failing to generate corresponding cash flow. This failure rate costs enterprises approximately $200 billion annually according to this analysis of accounts receivable and financial statement distortion.

That single sentence captures the operational truth controllers deal with every month. AR isn't just an asset category. It's a claim on cash with varying levels of reliability.

An unpaid invoice is not neutral. It first flatters earnings and assets, then weakens both if collection doesn't happen.

Why finance leaders should care

For a professional services firm, this can distort performance in three ways:

- Profitability looks stronger than liquidity The income statement reflects earned revenue, but the bank account doesn't.

- Assets rise without improving flexibility Receivables increase current assets, yet they can't fund payroll until collected.

- Cash planning gets harder The cash flow statement eventually exposes the lag, often after management has already made commitments based on reported earnings.

That's why disciplined AR management isn't just about follow-up emails. It's about preserving the integrity of what the statements are telling you.

The Mechanics of AR Events and Their Journal Entries

Controllers don't need vague advice here. They need the mechanics to line up with the reports.

Accounts receivable creates a series of accounting events. Each event changes the shape of the balance sheet, the income statement, or both. If the process is loose operationally, the financial statement impact shows up with a delay, usually when it's least convenient.

Four events that matter most

The AR lifecycle in a professional services firm usually turns on four moments:

- Invoicing the client Revenue is recognized and receivables are established.

- Collecting cash The asset shifts from Accounts Receivable to Cash.

- Recording a provision Management recognizes that some receivables may not be collectible.

- Writing off a specific balance A receivable is removed when collection is no longer expected.

Each entry is standard. What varies is timing, judgment, and follow-through.

Journal entries for key AR events

Event | Debit | Credit | Statement Impact |

|---|---|---|---|

Invoicing a client | Accounts Receivable | Revenue | Increases assets on the balance sheet and revenue on the income statement |

Collecting cash | Cash | Accounts Receivable | Changes asset mix on the balance sheet, no new revenue recognized |

Creating a provision for doubtful accounts | Bad Debt Expense | Allowance for Doubtful Accounts | Increases expense on the income statement and offsets receivables on the balance sheet |

Writing off an uncollectible invoice | Allowance for Doubtful Accounts | Accounts Receivable | Reduces gross receivables on the balance sheet, no new expense if previously reserved |

Event one, invoicing

Assume your firm completes a project phase and bills the client for $10,000.

Entry

- Debit Accounts Receivable $10,000

- Credit Revenue $10,000

Before the entry, the work may exist only in WIP or in operational tracking. After the entry, the statements now present earned revenue and a current asset.

Owners sometimes get overly comfortable. The P&L improves immediately. Cash doesn't.

A useful checkpoint at this stage:

- Invoice timing If billing waits for manual review, partner approval, or project closeout housekeeping, DSO starts rising before the invoice even leaves.

- Invoice accuracy If the billing support, PO detail, or time backup is incomplete, disputes are almost guaranteed.

- Client routing If the invoice goes to the wrong approver, the accounting entry is correct but collection timing stretches.

Event two, collection

When the client pays, the entry is simple.

Entry

- Debit Cash $10,000

- Credit Accounts Receivable $10,000

No additional revenue is recognized. That's the point many non-finance operators miss. Collection doesn't create profit. It converts a recorded claim into usable liquidity.

Practical rule: If your AR aging is rising while revenue is stable, don't treat that as a sales success. Treat it as delayed cash conversion.

From a statement perspective, this is the healthiest AR event. One asset decreases, another increases, and liquidity improves without changing reported earnings.

Event three, provision for doubtful accounts

Now consider a different reality. The client is slow, communication is inconsistent, and the engagement partner has lost confidence in collection. At that point, waiting for certainty is usually poor finance practice. A reserve is often more honest than optimism.

Entry

- Debit Bad Debt Expense

- Credit Allowance for Doubtful Accounts

It lowers current period earnings before the final outcome is known. Many owners resist this entry because it feels punitive. In practice, it makes the statements more credible.

The before-and-after effect looks like this:

- Before provision Gross AR is high, earnings are higher, and the balance sheet may look stronger than the underlying receivables quality supports.

- After provision Net income comes down, and net realizable value of receivables is presented more realistically.

That is financial control. Not because it feels good, but because it prevents management from making cash commitments based on overstated asset quality.

Event four, write-off

Eventually, some invoices stop being collectible in substance, even if they remain collectible in theory.

If the firm has already reserved for the loss, the write-off usually looks like this:

Entry

- Debit Allowance for Doubtful Accounts

- Credit Accounts Receivable

The write-off removes the specific receivable from the books. It doesn't create a fresh hit to earnings if the reserve was established earlier.

That distinction matters operationally. Firms that delay provisions often take a sudden income statement hit later. Firms that reserve on time absorb the risk in a more controlled way.

What works and what doesn't

The accounting entries are standard. The operating discipline behind them is where firms separate.

What works:

- Fast invoicing after service delivery That shortens the gap between earned revenue and collection activity.

- Visible ownership of disputes Someone must own resolution, not just note it.

- Regular reserve review Allowance decisions should reflect current collection evidence, not hope.

What doesn't work:

- Using AR aging as a passive report Aging only helps if someone acts on it.

- Leaving collectors without context Collections teams need contract terms, engagement history, and dispute status.

- Treating write-offs as isolated events They usually reflect earlier failures in billing, follow-up, or escalation.

In professional services, AR quality isn't separate from financial reporting quality. It's one of the clearest places where daily process becomes reported performance.

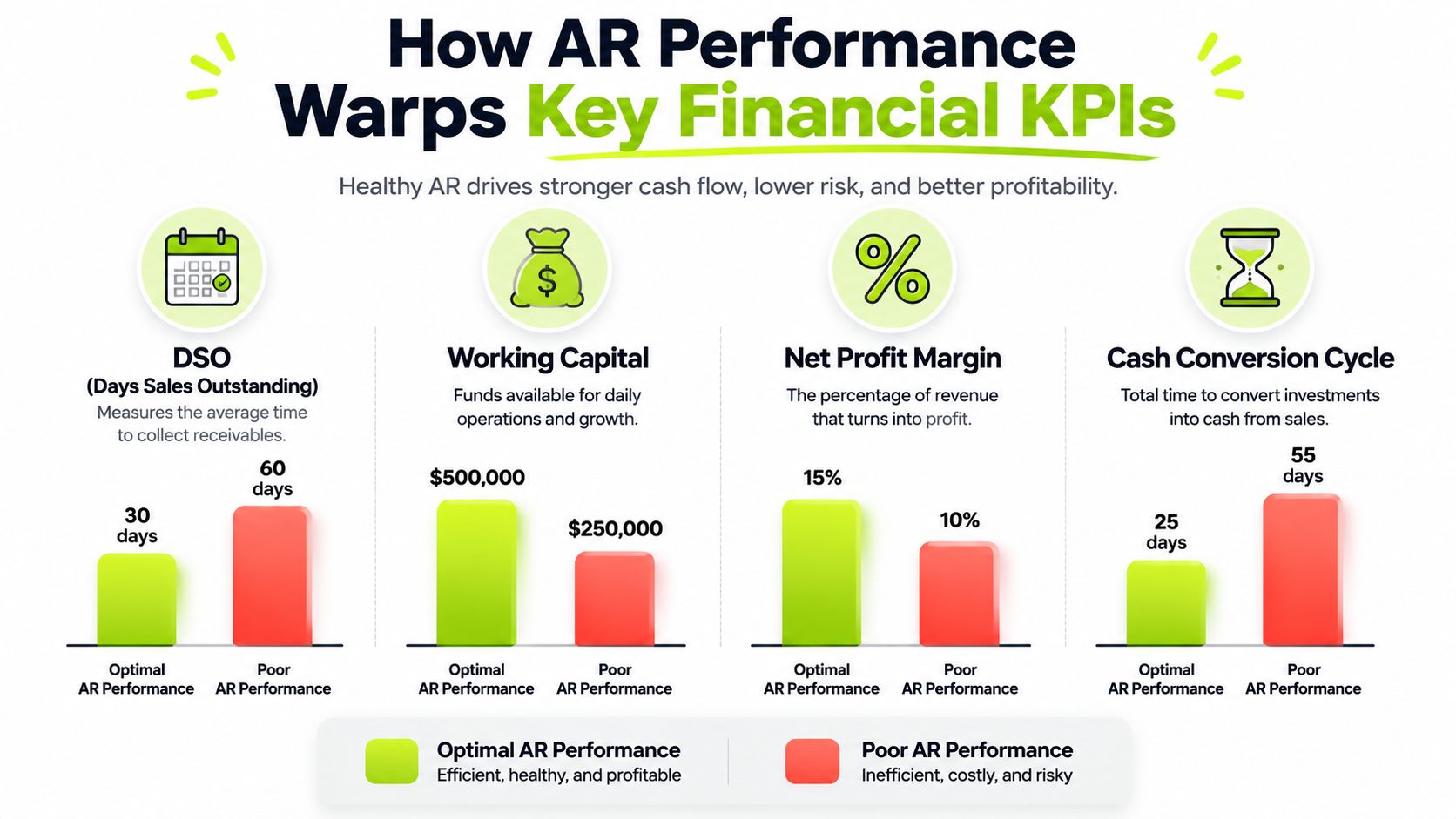

How AR Performance Warps Key Financial KPIs

Most owners don't manage to journal entries. They manage to outcomes.

That means AR has to be translated into the metrics leadership watches. Once receivables age beyond expectation, the effect shows up in DSO, working capital pressure, and the length of time it takes to turn billed work into spendable cash.

DSO is the operating signal

If invoicing is late, follow-up is inconsistent, or disputes sit unresolved, Days Sales Outstanding rises. DSO is one of the cleanest indicators of whether the firm is turning recognized revenue into cash with discipline.

That doesn't make DSO a standalone scorecard. A lower DSO achieved by damaging client relationships isn't a win. But in most firms, DSO drifts up because process quality drifts down.

Working capital absorbs the damage

Aging receivables tie up funds that could support payroll, hiring, software, tax payments, or partner distributions. On paper, current assets may still look acceptable. In practice, those assets are less useful because they haven't converted.

Many finance leaders shift their focus from collections to control. Weak AR performance doesn't just create slower cash receipts. It narrows operating options.

Resolve disputes and deductions quickly. They hold cash hostage longer than most teams realize.

A practical formula for cash unlocked

Controllers need a way to quantify the opportunity, not just describe it. One useful tool is the cash realization formula published in this DSO reduction playbook:

Cash Released = (Current DSO − Target DSO) × Average Daily Sales

That formula gives you a direct estimate of the liquidity sitting inside receivables. It also forces a better management conversation. Instead of saying, "We should improve collections," you can say, "If we move DSO from current performance to target performance, here's the cash impact."

The KPI chain in practice

When AR weakens, the effect usually runs in a sequence:

- Invoices go out late or with errors Fresh DSO starts building immediately.

- Disputes and deductions aren't resolved Receivables move into older aging buckets.

- Cash arrives later than planned The cash conversion cycle stretches.

- Working capital tightens Management relies more heavily on credit facilities or defers spending.

A short review cadence helps here. Each month, look at these items together:

- Fresh DSO movement This tells you whether today's billing process is creating tomorrow's aging problem.

- Dispute backlog Delayed resolution often matters more than collection effort.

- Aged AR concentration This signals where risk is already embedded in the balance sheet.

The strategic point is simple. AR performance is not a side metric. It is one of the clearest operational drivers of financial statement impact.

Using Automation to Reshape Financial Outcomes

Manual AR processes usually fail in ordinary ways. Invoices wait in draft folders. Follow-ups depend on who remembers. Cash application slows down because remittance detail is incomplete or scattered across inboxes.

That doesn't create a dramatic accounting failure on day one. It creates small delays that accumulate into weaker financial outcomes.

Manual AR versus automated AR

For professional services firms in the $3M to $50M range, the trade-off is usually not headcount versus software in the abstract. It's control versus variability.

Manual AR tends to look like this:

- Billing depends on handoffs Project teams finish work, finance waits for approvals, and invoices go out later than they should.

- Collections depend on individual effort One collector is excellent. Another is overloaded. Outreach quality changes by person and by week.

- Cash application stays fragmented Payments arrive, but reconciliation lags because data isn't centralized.

By contrast, accounts receivable automation standardizes those points of failure. Invoicing happens faster. Follow-up sequences run consistently. Payment and remittance information can be matched with less manual effort. That doesn't eliminate judgment. It removes preventable delay.

If you're evaluating categories and terminology, this overview of AR automation is a useful baseline.

What the measurable outcomes look like

The case for automation gets stronger when you tie it to statement-level results instead of convenience alone.

According to this benchmark on accounts receivable automation for professional services, companies that automate AR processes achieve an average reduction in DSO of 33 days and increase collections productivity by threefold. The same benchmark notes that this is especially relevant for firms aiming to reduce DSO by 15 days and cut receivables over 120 days by 40% in a single rollout.

Those are not abstract efficiency metrics. They change the financial statement impact directly.

- Lower DSO Cash reaches the balance sheet sooner.

- Higher collections productivity Teams spend more time on disputed, risky, or strategic accounts instead of repetitive reminders.

- Lower aged receivables concentration The need for reserves and write-offs can become more manageable.

A separate benchmark reports that fully embraced AR automation can drive a 40%+ reduction in Days to Pay, and that 95% of organizations report increased efficiency through process automation, while operational payroll costs may fall by 20% to 30% in the process according to this analysis of the ROI of accounts receivable automation.

Why AI AR automation changes the sequence

Basic automation handles reminders and workflows. AI AR automation goes further by prioritizing attention.

Instead of treating every client the same, the system can identify at-risk invoices earlier, adapt outreach timing, and direct staff time toward exceptions that need judgment. In practice, that means the accounting consequences discussed earlier happen on a better timetable:

- Invoices are issued faster, which helps reduce DSO

- Follow-up happens consistently, which can improve cash flow

- Cash application occurs sooner, so receivables convert to cash with less lag

- Staff can focus on disputes, credits, and client conversations that software alone shouldn't handle

Good AR software doesn't replace finance judgment. It preserves it for the accounts that actually require judgment.

This matters in professional services because collections are relational. Clients aren't freight invoices or retail checkouts. The tone and sequence have to stay professional.

That same operational discipline shows up in other billing-heavy sectors. For teams studying how automation principles can streamline transport billing, the lesson is familiar. Faster invoice delivery, fewer handoff errors, and cleaner exception handling improve outcomes without making client communication feel robotic.

Where QuickBooks AR automation fits

Many firms already use QuickBooks as the accounting system of record. That creates a practical question. Do you force the AR process to live entirely inside the general ledger workflow, or do you add a dedicated layer around it.

For smaller firms, QuickBooks AR automation can improve consistency when paired with a purpose-built AR workflow. The ledger remains authoritative for accounting. The AR layer handles cadence, prioritization, reminders, payment experience, and application support.

The important point is architectural, not ideological. Your GL is built to record events. Your AR process needs to drive outcomes.

A short product walkthrough helps make that distinction concrete:

What usually works in rollout

The best implementations stay narrow at first. They don't attempt to redesign the whole finance stack in one motion.

A practical sequence looks like this:

- Start with invoice speed If invoices don't leave promptly, no collection workflow can recover the lost time.

- Automate standard follow-ups Routine reminders shouldn't depend on memory.

- Escalate based on risk and aging High-value and disputed accounts need human review sooner.

- Tighten cash application Collected cash only improves visibility when it is posted accurately and quickly.

That is where AR software for professional services earns its place. Not because it adds more dashboards, but because it makes reported receivables more likely to become actual cash on a predictable schedule.

From Reactive Collections to Proactive Financial Control

When a firm treats AR as a back-office chore, the statements absorb the consequences. Revenue gets recorded. Receivables rise. Cash lags. Then leadership has to interpret mixed signals.

A better approach is to treat receivables as part of financial control. Every invoice is an accounting event, a working capital event, and a management event at the same time. If the process is disciplined, the statements stay aligned with operational reality. If the process is inconsistent, that misalignment spreads into forecasting, hiring, partner decisions, and borrowing needs.

The mindset shift that matters

Reactive collections usually sound like this: follow up when something gets old, chase the loudest accounts first, and clean up exceptions at month-end.

Proactive control looks different:

- Billing is prompt Fresh DSO doesn't build unnecessarily.

- Disputes are visible Finance can act before balances age into risk.

- Cash expectations are grounded Forecasts reflect collection behavior, not just booked revenue.

The goal isn't to pressure clients harder. It's to create a steady, professional system that turns earned revenue into cash with fewer surprises.

That is the financial statement impact of AR management. It shapes earnings quality, asset quality, liquidity, and management confidence all at once. For CFOs, Controllers, and firm owners, that makes AR one of the most practical levers in the business.

Resolut automates AR for professional services with a focus on consistency, accuracy, and a human tone. If you're looking to improve cash flow, reduce DSO, and bring more predictability to billing and collections, take a look at Resolut.