Outstanding Invoice Meaning and Its Cash Flow Impact

Understand the true outstanding invoice meaning for CFOs. We cover its impact on DSO and cash flow, plus how AR automation helps you control receivables.

You open the AR aging report near month end and see a number that looks manageable. A large share of receivables sits in current. Nothing is technically late yet. But you already know the question isn't whether those invoices are unpaid today. It's which of them will roll from routine outstanding balances into collection problems next week.

That distinction matters more in professional services than many teams admit. A consulting invoice can be valid, approved internally, and still stall because a client wants a revised line description, an engagement lead forgot to confirm a milestone, or AP can't process it without a PO. On paper, it's outstanding. Operationally, it's at risk.

This is the practical core of outstanding invoice meaning. It isn't just an accounting label. It's a time-bound stage in the cash conversion cycle. Finance leaders who treat that stage as an early warning window usually protect liquidity better than teams that wait for invoices to become overdue before acting.

The Hidden Risk in Your Outstanding Receivables

A healthy services firm should have outstanding invoices. If you bill on Net 30, you'll always carry receivables that haven't been paid yet. That's normal. The mistake is assuming "current" means "safe."

I've seen the same pattern across firms with project-based billing. The aging report says most balances are still within terms, but a closer look shows missing billing contacts, unresolved time entry questions, and client-side approval bottlenecks. Those invoices haven't crossed the due date, yet the risk has already formed.

What the aging report often misses

An aging schedule tells you when an invoice was issued and how long it's been unpaid. It doesn't always tell you whether the invoice is collectible on schedule.

In professional services, the invoices most likely to age poorly often share a few traits:

- Approval friction: The client hasn't accepted a milestone, timesheet, or deliverable.

- Billing defects: The invoice lacks a PO number, entity name, matter code, or required backup.

- Relationship ambiguity: The partner owns the client relationship, but finance owns collections and nobody clearly owns the next step.

- Silent disputes: The client isn't rejecting the invoice outright. They're just not moving it forward.

Current AR can still be operationally late. Finance teams need to spot process delay before the due date exposes it.

That is why outstanding receivables need active management, not passive reporting. When a controller reviews current AR by client, by billing partner, and by invoice status detail, the discussion changes. Instead of "how much is unpaid," the question becomes "what is blocking payment while we still have time to fix it."

The Operator's Definition of an Outstanding Invoice

In day-to-day finance operations, an outstanding invoice is best defined as a bill you've sent to a customer that remains unpaid within the agreed payment period, before it becomes overdue. That framing aligns cleanly with the invoice lifecycle described in Upflow's explanation of outstanding invoices.

If you issue an invoice on March 1 with payment due on April 1, it stays outstanding through March. If the client hasn't paid by the due date, it moves into overdue status. That sounds simple, but many teams still mix the terms.

The clean operational distinction

For control purposes, use this working model:

Status | Meaning | Required action |

|---|---|---|

Outstanding | Sent, unpaid, still within terms | Monitor, confirm receipt, remove friction |

Overdue | Sent, unpaid, past due date | Escalate follow-up and collections action |

Paid | Cash received and applied | Close and reconcile |

This distinction matters because the actions are different. During the outstanding phase, the job is prevention. After the due date, the job shifts to recovery.

Why teams get tripped up

Some systems and teams use "outstanding" to mean any unpaid invoice, whether current or overdue. That broader definition can be acceptable for balance sheet discussions because unpaid invoices sit in accounts receivable either way. But it creates trouble if your collections workflow depends on timing, prioritization, and aging logic.

HighRadius notes that definitions vary, and that lack of consistency creates confusion for finance teams trying to track AR metrics and automation rules in a disciplined way, as outlined in its discussion of outstanding invoice terminology and reporting ambiguity.

If your ERP says "open," your staff says "outstanding," and your collector means "still within terms," your reporting starts to blur. DSO reviews become less reliable. Forecasts get noisier. Automation rules fire at the wrong point.

A practical standard for professional services firms

For firms in the $3M to $50M range, the most useful approach is this:

- Use "outstanding" for invoices still within terms.

- Use "overdue" the day after the due date.

- Use "open AR" as the umbrella label for all unpaid invoices.

That language gives your team a common operating model. It also makes accounts receivable automation more effective because status drives action.

Practical rule: Define terms once inside your AR policy, then match those definitions in QuickBooks, your aging report, and every collection workflow.

When finance teams don't standardize outstanding invoice meaning, they end up arguing about labels. When they do standardize it, they can focus on the work that gets cash in.

How Outstanding Invoices Shape DSO and Cash Flow

The fastest way to make outstanding invoice meaning relevant to a CFO is to connect it to cash timing. Every day an invoice stays unpaid is a day that cash remains unavailable for payroll, partner draws, hiring, software, and tax planning.

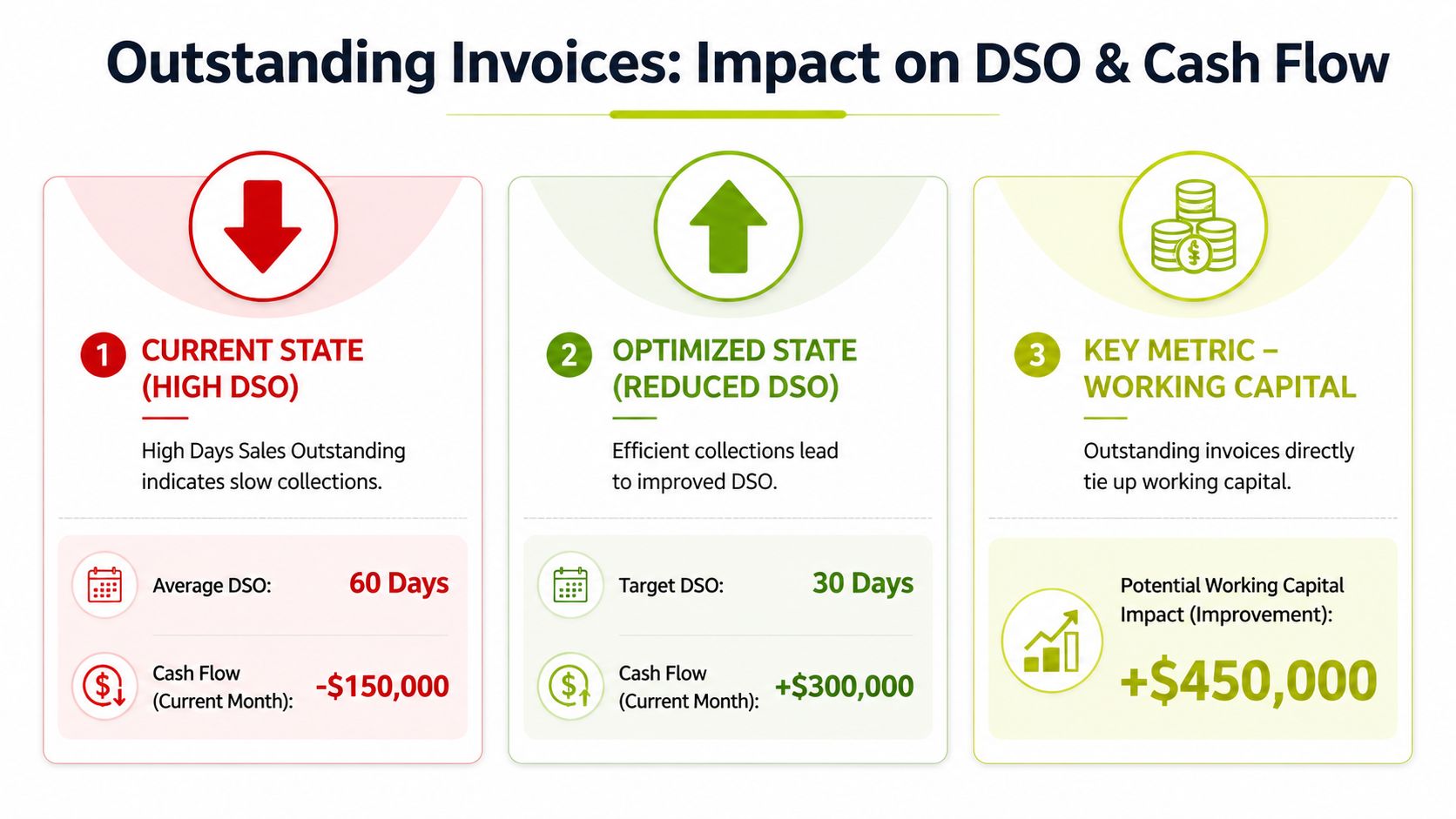

Globally, unresolved outstanding invoices contribute to 1 in 4 bankruptcies, and in 2024 US B2B data showed 50% of invoices are overdue, while in the EU 47% of firms reported issues from late payments. For mid-sized firms, that often means $500K to $2M in outstanding AR, and effective management can cut DSO by 20% to 30%, according to Xero's guide to chasing outstanding invoices.

Why current AR still drives DSO

A common mistake is to treat DSO as a collections metric only. It isn't. DSO reflects how long invoices spend in the full receivables cycle, including the time they sit in the outstanding phase.

If billing goes out late, if reminders start too late, or if a client needs backup documentation and nobody sends it promptly, DSO rises even before invoices become old enough to trigger concern.

That is why firms trying to understand what DSO means in practice should look upstream at invoice creation, delivery, approval, and pre-due communication. Collections performance starts before delinquency.

The working capital effect in services firms

Professional services firms tend to feel this pressure quickly because labor costs arrive on schedule even when clients don't pay on schedule. You can't delay payroll because a client hasn't approved a retainer draw or milestone invoice.

A simple operating view helps:

- Outstanding invoices represent expected cash, not usable cash

- Longer outstanding periods reduce forecast accuracy

- Aging current AR often signals future overdue balances

- Lower DSO improves flexibility across staffing and investment decisions

If you work with recurring or subscription-style billing models, some of the logic overlaps with AR insights for SaaS founders. The customer base is different, but the cash discipline is the same. Faster movement from billed to paid gives management room to operate.

A firm can look profitable on paper and still feel cash tight because receivables are slow, not because demand is weak.

That is why "reduce DSO" shouldn't be treated as a collections slogan. It's an operating mandate. And it starts with controlling outstanding invoices while they're still recoverable through routine action, not escalation.

Common Causes of Invoice Aging in Professional Services

In product businesses, an invoice often follows a shipment. In professional services, an invoice follows interpretation. Was the work complete. Was the scope accepted. Did the client expect that fee. Was the right legal entity billed. Those questions create aging risk long before an invoice turns overdue.

The most common friction points

When a services invoice stalls, the root cause is usually operational. The aging report helps, but the better diagnostic is invoice path analysis. Where did the invoice pause between draft, send, approval, payment, and application?

Here are the patterns that show up most often:

- Scope drift and vague line items: If the invoice description doesn't clearly tie back to the engagement, clients pause it.

- Missing client requirements: AP teams often need vendor forms, billing codes, backup, or a PO reference before they can process anything.

- Milestone ambiguity: Project leaders think the work is billable. The client sponsor thinks one more deliverable is pending.

- Delayed invoice issuance: Time gets approved late, billing goes out late, and the client payment clock starts later than finance expected.

- Split ownership internally: Billing sits with operations, relationships sit with partners, and follow-up sits with accounting. No one owns resolution end to end.

What aging actually looks like in motion

The invoice lifecycle is rarely linear in a services firm. It usually moves like this:

- Work is completed or a billing milestone is reached

- The invoice is drafted, reviewed, and sent

- The invoice sits outstanding while the client routes it internally

- A question, discrepancy, or silence slows progress

- The due date passes and finance treats it as a collections issue

At that point, the invoice appears to have "become late." In practice, the delay often started earlier.

A disciplined accounts receivable aging review should therefore include more than bucket totals. It should capture whether the invoice was received, whether the approver is known, whether supporting documents were accepted, and whether the relationship owner has confirmed payment status.

What doesn't work

Teams often respond to aging by sending more reminders. That helps only when the issue is forgetfulness. It doesn't help when the actual blocker is a billing defect or an approval mismatch.

If the client can't process the invoice, more follow-up just creates noise.

What works better is tracing the cause of delay before escalating tone. In professional services, many "slow payers" aren't resisting payment. They're waiting for the invoice package to become payable.

Best Practices for Manual Collections and Mitigation

A disciplined manual process still matters. Even firms that plan to adopt accounts receivable automation need a clean baseline. Automation scales judgment. It doesn't replace weak operating habits.

The strongest manual collections teams run a cadence, assign ownership, and document every promise date. They don't just email when an invoice is late. They manage the outstanding phase deliberately.

A practical manual cadence

A good process starts before the due date. The tone should change as the invoice ages, but the sequence should stay predictable.

- Before due date: Confirm receipt, verify the AP contact, and ask whether any backup is needed.

- On due date: Request payment confirmation or expected settlement date.

- Shortly after due date: Follow up directly with a clear action request and a specific response deadline.

- If silence continues: Move from email to phone and involve the relationship owner if needed.

If you want a concise outside reference on communication sequencing, Suby's dunning process guide is useful because it focuses on cadence and escalation rather than generic reminder advice.

Ownership matters more than templates

Many firms spend too much time polishing email copy and too little time assigning responsibility. A reminder sent by the wrong person at the wrong moment doesn't move cash.

Manual control works best when the rules are explicit:

Task | Best owner |

|---|---|

Invoice accuracy before send | Billing or project admin |

Receipt confirmation | AR or billing specialist |

Commercial dispute resolution | Engagement lead or partner |

Payment follow-up | AR with escalation support |

Final commitment tracking | Controller |

That split respects client relationships without letting invoices drift.

What to say when payment slips

Scripts should be short and specific. The point is to remove ambiguity and force a next step.

A basic collection call framework works well:

- Confirm the invoice was received.

- Ask whether it's approved for payment.

- If not, identify the blocker.

- Ask for an exact payment date or required action.

- Send a written recap the same day.

For teams that want a cleaner structure for live outreach, this collection call guide is a practical template to adapt by aging stage.

Manual collections fail when follow-up lives in individual inboxes instead of a shared process.

The limitation is consistency. As invoice volume grows, even good teams miss follow-ups, duplicate outreach, or fail to log client responses. That is usually the point where manual discipline stops being enough.

The Shift to AI-Powered Accounts Receivable Automation

Manual collections can work when volume is low and client behavior is predictable. Once a firm handles a larger invoice load, multiple service lines, and varied client approval paths, spreadsheets and calendar reminders stop giving finance real control.

That is where accounts receivable automation changes the equation. Instead of treating follow-up as a series of one-off tasks, the system treats receivables as a managed workflow from invoice issue through cash application.

What AI AR automation actually does

The useful form of AI AR automation isn't magic. It's structured execution. A platform classifies invoice status, triggers the right outreach, logs responses, and keeps cash posting aligned with what happened in the real world.

According to Ramp's discussion of outstanding invoice workflows and automation, each day an invoice is outstanding erodes liquidity. The same source explains that AI-driven workflows use state logic such as "outstanding" versus "overdue" to trigger action. It also notes that AI-powered reminders can lift on-time payments by 40%, automated cash application can achieve 99% accuracy, and automation can save 20 to 30 hours per week while delivering 5x to 7x ROI.

Those numbers matter because they map directly to pain points inside services firms:

- Inconsistent reminders become scheduled, policy-based outreach.

- Cash posting delays become automated matching and application.

- Partner-dependent follow-up becomes a tracked workflow with escalation logic.

- Weak visibility becomes a live receivables view by client, invoice, and risk state.

Why this matters for professional services

Services firms don't just need reminder emails. They need orchestration.

An effective AR software for professional services should handle pre-due nudges, overdue follow-up, documentation trails, payment promises, and cash application in one operating model. It should also support real-world tools already in use. For many firms, that means QuickBooks AR automation is part of the conversation because finance doesn't want another disconnected workflow.

The practical gain is control. Controllers can see which invoices are current but drifting. CFOs can forecast with more confidence because status is based on workflow evidence, not guesswork.

A short walkthrough helps make that concrete:

What works and what doesn't

Not every automation approach is useful. Basic reminder tools help, but they don't solve the full AR problem if they can't connect payment behavior, dispute handling, and reconciliation.

What tends to work:

- Rules tied to invoice state: Different workflows for current, near due, overdue, and disputed invoices.

- Human-in-the-loop escalation: Finance can step in when relationship context matters.

- Integrated cash application: Collected cash closes the loop quickly and accurately.

- System visibility for leadership: Dashboards show aging pressure before quarter end.

What usually disappoints:

- Email-only tools that don't track outcomes

- Separate collections and accounting systems that force duplicate work

- Automation with no policy logic beyond "send another reminder"

For firms evaluating options, platforms such as QuickBooks-connected workflows, ERP-linked collection tools, and systems like Resolut can help centralize outreach, payment status, and cash application without relying on manual chasing as the default model. The key isn't the label. It's whether the tool gives finance systemic control over the invoice lifecycle.

From Outstanding to Paid Gaining Systemic Control

The practical meaning of an outstanding invoice isn't "unpaid." It's "still in your control window."

That is the shift finance leaders need to make. Outstanding receivables are not just a normal byproduct of billing. They are the stage where invoice quality, client process, ownership discipline, and timing either protect cash flow or weaken it.

Professional services firms usually don't lose control all at once. They lose it through small delays. Late billing. Unclear approvals. Follow-ups that depend on memory. Cash application that trails collections. Each issue looks minor on its own. Together, they stretch DSO and tighten liquidity.

The firms that improve cash position most consistently are the ones that treat AR as an operating system. They define invoice status clearly. They diagnose aging before it hardens. They use manual discipline where it still makes sense, then automate the repeatable parts with precision.

If you're trying to reduce DSO, improve cash flow, and bring more predictability to receivables, start with the exact meaning of "outstanding." Then build the process that moves invoices from current to paid without drift.

Resolut automates AR for professional services. It gives finance teams a consistent, accurate, and human way to manage outreach, aging visibility, and cash application so outstanding invoices move to paid with more control.