A CFO's Guide to Payment Terms and Conditions in 2026

Master payment terms and conditions to improve cash flow and reduce DSO. A definitive guide for CFOs on drafting, enforcing, and automating AR processes.

Your payment terms are not administrative details. They are the operational controls that govern your firm’s cash flow. For professional services firms, vague or poorly enforced terms lead directly to higher Days Sales Outstanding (DSO) and strained client relationships.

This guide moves beyond reactive collections into a proactive strategy. Clear terms set clear expectations from day one, giving you control over your firm’s financial health.

Why Your Payment Terms Are a Financial Control System

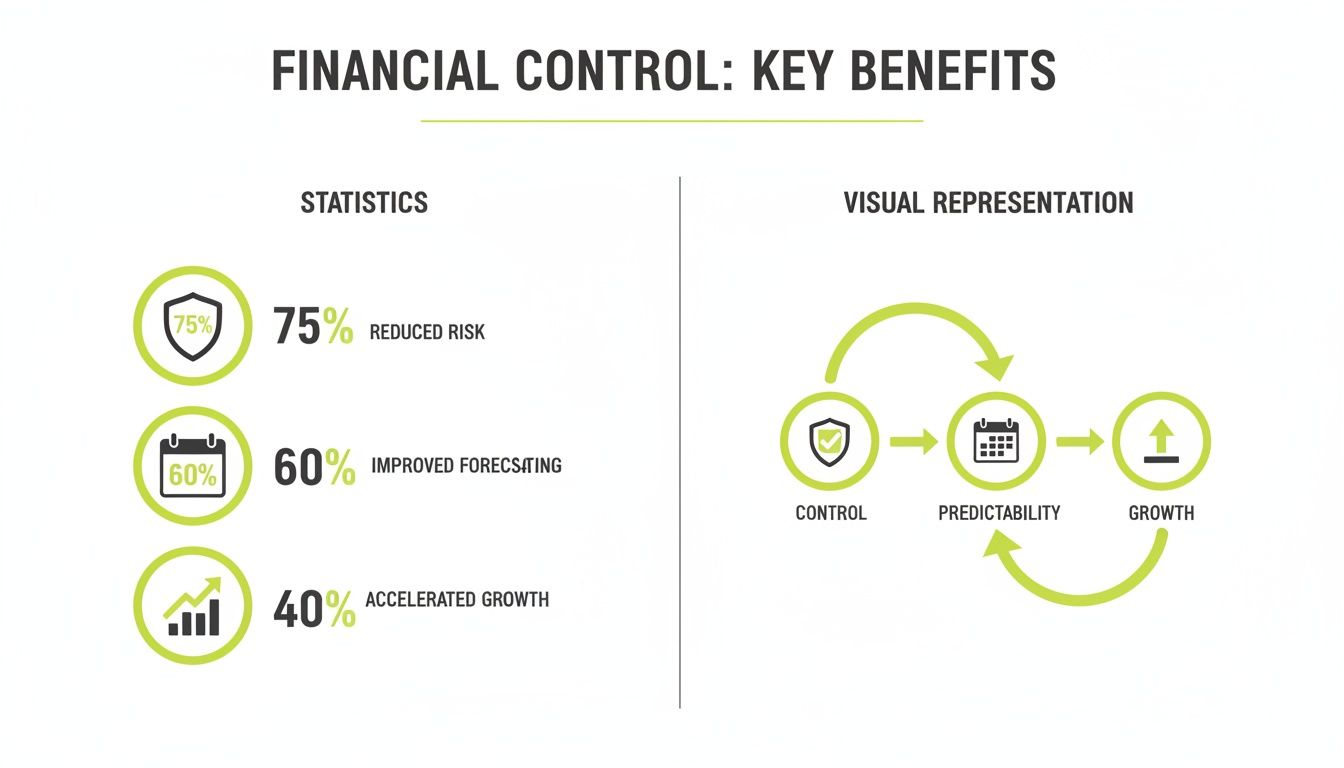

Think of your payment terms and conditions as the financial control system for your client engagements. This isn't about boilerplate text; it's about engineering predictable cash flow.

The objective is to reclaim control. Despite digital invoicing, payment cycles are extending. Well-defined, enforceable terms are your primary defense against the cash flow gaps created by late payments.

The True Cost of Ambiguous Terms

For a professional services firm in the $3M–$50M revenue bracket, ambiguous payment terms have a measurable impact on liquidity. When terms are open to interpretation, clients will interpret them in their favor. A standard Net 30 quietly becomes a 45- or 60-day reality.

Let’s quantify the impact. For a $10M firm, a 15-day increase in DSO ties up an additional $410,000 in accounts receivable. This is not an abstract number; it is working capital that could be funding growth, talent acquisition, or technology investment.

Vague payment terms are an open invitation for clients to manage their cash flow at your expense. Precision isn’t about being difficult—it's about setting the financial foundation for a healthy partnership.

From Administrative Task to Strategic Control

The core problem is treating payment terms as a perfunctory administrative task. Delegating this to non-financial staff who copy and paste from a template cedes control of your most critical asset: cash.

A robust payment terms framework is an operational tool designed to:

- Improve Cash Flow: Firm deadlines and clear consequences build predictable revenue streams.

- Reduce DSO: Clear terms are easier to enforce, directly lowering Days Sales Outstanding.

- Strengthen Client Relationships: Addressing payment logistics upfront with total transparency prevents future disputes and collections calls.

This approach transforms your terms from a passive document into an active component of your financial strategy. It protects your liquidity and ensures you are paid on time for the value you deliver.

The Paradox of Modern Payment Timelines

Historically, terms like ‘Net 30’ were a practical response to physical logistics. Invoicing involved printing, mailing, and waiting for a paper check to return. A 30-day window was logical.

The paradox for finance leaders today is that while digital invoicing has reduced administrative work to minutes, payment timelines have stretched to 45, 60, or even 90 days.

What was an operational necessity has become a drain on liquidity. By extending terms, your clients are using your accounts receivable as an involuntary, zero-interest credit line. This directly inflates your DSO.

The Real Cost of Extended Timelines

The ‘Net 30’ standard is eroding. Recent data shows only 36% of B2B firms hold to 30-day terms. A larger portion, 38%, now operates on 45-day cycles, while 11% have pushed terms to 90 days. This trend is a primary driver of inflated DSO.

Compounding this, 60% of B2B invoices in the U.S. are paid late, adding an average of 7 days to the collection cycle. The industry-wide DSO now hovers around 50 days, creating a systemic squeeze on working capital. For more on these numbers, NetSuite provides a breakdown of modern payment term trends.

Reclaiming Financial Control

This slow extension of payment timelines is a strategic threat. The widening gap between work delivery and payment receipt creates unpredictability, making accurate forecasting and confident investment nearly impossible.

The lengthening of payment cycles is a quiet but persistent erosion of financial stability. It transforms your working capital into your client's and forces you to operate with less predictability and higher risk.

This is why modern finance leaders are implementing accounts receivable automation. By using technology to enforce the payment terms and condition you set, you can systematically reduce DSO and improve cash flow.

Tools like AI AR automation and QuickBooks AR automation provide the leverage to turn a historical disadvantage into a competitive edge. They systematize collections, ensuring consistent follow-up and transforming your AR function from a reactive cost center into a proactive, strategic asset.

How to Draft Payment Terms That Protect Your Cash Flow

With payment terms, clarity is your first line of defense for a healthy cash flow. Your terms are the rulebook for the financial relationship with a client. If the rules are fuzzy, you invite late payments and disputes.

This is not about using a generic template. It is about constructing precise, enforceable clauses that are legally sound and operationally practical. Ambiguity creates loopholes that lead directly to aging receivables.

The goal is to create a transparent, professional framework that leaves no room for misinterpretation. Every clause must have a clear purpose tied to a specific financial outcome.

Core Payment Obligations

The foundation of any solid agreement specifies exactly when and how you expect to be paid. Vague language like "payment upon project completion" invites delays. Be specific.

These are the non-negotiables to define:

- Precise Due Dates: State the exact terms, whether “Net 30,” “Net 15,” or “Due on Receipt.” For large projects, link payments to milestones: “50% due upon project kickoff, 50% due upon final deliverable approval.”

- Accepted Payment Methods: List every method a client can use, such as ACH, credit card, or corporate check. This prevents the "I tried to pay but..." excuse. Our guide on the legal invoice format covers this structure.

- Currency Specification: If you serve international clients, this is essential. Explicitly state the payment currency (e.g., "All payments must be made in USD"). This removes currency fluctuation from the equation.

Defining these details upfront removes friction and establishes a firm, professional tone.

A Table of Essential Clauses

To make your terms airtight, you need additional clauses that prevent scope creep, manage disputes, and protect revenue.

Essential Clauses for Your Payment Terms

Clause | Purpose | Example Phrasing |

|---|---|---|

Late Payment Penalty | Discourage overdue payments and compensate for delayed cash flow. | "A late fee of 1.5% per month will be applied to all outstanding balances not paid within the agreed-upon terms." |

Dispute Resolution | Create a formal, time-bound process for handling invoice disagreements. | "Clients must submit any invoice disputes in writing within 10 business days of receipt. Failure to do so constitutes acceptance of the invoice." |

Service Suspension | Provide leverage to pause work if a client is not paying. | "We reserve the right to suspend all services if an invoice remains unpaid for more than 15 days past its due date." |

Partial Payment Policy | Clarify that partial payment does not create a new payment plan or waive late fees. | "Partial payments will be applied to the outstanding balance but do not constitute an agreement to new terms. The remaining balance is subject to late fees." |

These clauses are operational tools, not just legal jargon. They set clear expectations and provide mechanisms for enforcement.

Using Incentives and Penalties Strategically

Your payment terms can actively encourage desired behavior. You can guide clients toward on-time—or even early—payment while establishing firm consequences for late payment.

A small incentive can have a significant impact.

An early payment discount like 2/10 Net 30 isn't a gesture; it’s a strategic lever. Offering a 2% discount for payment in 10 days accelerates cash collection, directly shrinking DSO and boosting working capital.

Conversely, the late payment clause is your primary tool against aging receivables. It is not punitive; it is compensation for the cost of carrying that debt. For a penalty to be a deterrent, it must be enforced consistently. This is where accounts receivable automation provides critical value.

For a real-world example of how these elements are structured, review a set of comprehensive terms and conditions. By codifying these rules, you build a self-enforcing system that protects your cash.

Tailoring Terms to Client Risk and Industry Norms

A one-size-fits-all payment term policy for every client is a strategic failure. For professional services firms in the $3M–$50M range, defaulting to Net 30 for every engagement is a missed opportunity to manage risk.

Payment terms should be a flexible tool, adjusted based on industry standards and individual client risk. This strategic segmentation protects your financial position without damaging strong client relationships.

Segmenting Clients by Risk Profile

Begin by categorizing clients into risk tiers based on objective data. This is not a personal judgment but a prudent financial control.

A practical structure includes:

- New or High-Risk Clients: Require an upfront deposit of 25-50% to confirm commitment and lower your initial risk. Use shorter payment cycles like Net 15 or Due on Receipt for the first few invoices.

- Established but Inconsistent Clients: Offer standard Net 30 terms but be disciplined in enforcing late fee clauses. This signals that you value the business but expect adherence to the agreed payment terms and condition.

- Long-Term, Reliable Partners: For trusted clients, extending more flexible terms like Net 45 can reinforce the partnership. This demonstrates you see them as more than just another account.

This approach transforms your payment terms from a rigid document into a dynamic risk management tool, aligning financial exposure with earned trust.

Static payment terms ignore the most critical variable in any B2B transaction: client-specific risk. Dynamic, tiered terms allow you to align financial exposure with the strength and history of the relationship, protecting cash flow where you need it most.

Aligning with Industry Benchmarks

Client risk is only half of the equation. Your terms must also align with industry norms. Being an outlier can make you appear difficult to work with. While Net 30 is common, many professional services firms must accommodate 30- to 60-day terms. In manufacturing, the trend is toward 45 days, with 11% pushing to 90. You can find more data on industry-specific payment terms to benchmark your position.

Controllers must balance being competitive with protecting the firm’s own cash flow.

Using Payment History to Drive Dynamic Adjustments

The most reliable data for refining your terms resides in your own accounts receivable ledger. A client's payment history is the single best predictor of future behavior. Analyzing this data reveals patterns that should inform your strategy. If a client consistently pays 5-10 days late, their next contract should reflect that reality—perhaps by shortening terms from Net 30 to Net 20.

This is where AI AR automation delivers a significant advantage. Manual analysis is inefficient and prone to error. An AR software for professional services, especially one with QuickBooks AR automation, can continuously analyze payment data to flag risks and suggest term adjustments. This helps you understand client credit worthiness and adjust your strategy proactively.

This data-driven approach enables you to systematically reduce DSO and improve cash flow while enforcing financial discipline in a way that preserves client relationships.

Enforcing Terms with Intelligent Automation

Having solid payment terms and condition is one thing; enforcing them is another. For most finance teams, enforcement is a manual process: run an aging report, sift through it, write reminder emails, and make follow-up calls.

This system is flawed. Manual enforcement is inconsistent. You chase the largest or loudest accounts, which teaches clients that your deadlines are flexible. This operational drag directly harms your financial health by increasing DSO and making cash flow unpredictable.

The solution is not more manual effort. It is moving from manual firefighting to intelligent automation. Accounts receivable automation transforms enforcement from a reactive task into a proactive, consistent system.

From Manual Chasing to Automated Workflows

An automated collections system operates without error or emotion. It never misses a due date or lets an invoice fall through the cracks. This is the value of AI AR automation. It does not replace finance professionals; it equips them with a system that executes your collections playbook flawlessly.

An automated workflow follows your communication rules without fail:

- Pre-Due Date Reminders: An automated reminder is sent 7 days before an invoice is due.

- Due-Date Notifications: On the due date, a clear notification is sent with a direct payment link.

- Systematic Escalations: After the due date, a sequence of professional messages is triggered at set intervals, such as 7, 15, and 30 days past due.

Achieving this level of consistency manually is impossible at scale. Automation establishes a firm cadence that conditions clients to pay on time. Firms using this approach often reduce their DSO by 10-25% within the first two quarters.

Using AI for Smarter Collections

Modern AR software for professional services does more than send timed reminders. AI optimizes the what, when, and how of each communication.

AI-driven systems analyze historical payment data to identify behavioral patterns. The system might learn one client is 30% more likely to pay after an afternoon SMS reminder, while another responds to an early morning email. To build such a responsive system, it's worth exploring the capabilities of **AI workflow automation**.

AI in AR isn't about sci-fi robots. It's about practical intelligence—using data to figure out the best message, timing, and channel for each client, making your collection efforts ridiculously effective.

This intelligence enables personalized outreach at scale. The system can automatically adjust the tone from collaborative to firm based on payment history and invoice age. The result is a collections process that feels both fair and effective. For more detail, see our guide on how to automate accounts receivable.

Measurable Results and Financial Control

Automating enforcement delivers measurable improvements in key financial metrics. The consistency of an automated system creates predictable cash flow and a stronger balance sheet—a clear benefit for firms using tools like QuickBooks AR automation.

A $20 million professional services firm with a 60-day DSO can unlock over $547,000 in working capital by reducing DSO by just 10 days. That is cash for investment, debt reduction, or shareholder returns.

When you automate enforcement of your payment terms and condition, you build a more resilient financial operation that reduces risk, improves client communication, and provides the control needed to guide the firm’s growth.

From Polite Reminders to Legal Escalation

Realistically, some invoices will become overdue even with the clearest payment terms and condition. This is not a failure; it is a business reality. The key is having a structured, unemotional escalation path that protects you from the 1 in 10 invoices at risk of becoming bad debt.

The foundation of this plan is consistency. Manual follow-up is often inconsistent and emotional. Accounts receivable automation eliminates this variability. It establishes a predictable series of reminders, and every action is documented.

This automated cadence resolves most overdue accounts, freeing up your team and creating a time-stamped paper trail for any invoices that require further action.

Human Intervention for High-Value Accounts

For high-value or severely late invoices, automation is not enough. This is where AI AR automation provides alerts based on rules you set—such as invoice amount or days past due—notifying the right person on your finance team to intervene.

The goal is a direct, professional conversation. You are not calling to argue. You are calling to get information, referencing the automated reminders and the terms they agreed to.

The point of a human call isn't to confront, but to understand and solve the problem. Is there a dispute you don't know about? A simple processing error on their end? Or are they facing a genuine cash flow crunch? The answer tells you exactly what to do next.

This conversation provides the intelligence needed to decide on next steps, preventing further delays.

The Voice of the Lawyer

When your own collection efforts stall, the next step does not have to be calling a lawyer. A better intermediate step is an automated "voice of the lawyer"—a formal demand letter drafted by legal counsel and sent from your collections platform.

This action signals that the matter is now serious and serves as a final warning before legal proceedings. For many debtors, this shift in authority is the catalyst needed to remit payment, improving recovery rates without the high cost of litigation.

A structured escalation path provides a scalable way to manage collections that protects cash flow without destroying client relationships.

Achieving Proactive Financial Management

Optimizing your firm's payment terms and conditions is the final step in moving from a reactive financial posture to a proactive one. It is a fundamental shift from chasing late payments to building a system that delivers consistency, accuracy, and predictability to your cash flow.

Pairing well-crafted terms with smart accounts receivable automation produces tangible results. The operational drag of collections is replaced by a systematic process that lowers DSO and stops revenue leakage. For a $20M firm, reducing DSO by just 5 days can free up nearly $275,000 in working capital.

Enhancing Human Oversight with Technology

The right technology does not replace your finance team; it enhances their capabilities. AI AR automation provides the data and tools for smarter, faster decisions on client risk and collections strategy.

Technology should serve as an operational amplifier, handling the repetitive, low-value tasks of collections so that your finance team can focus on high-value strategic initiatives like forecasting, risk analysis, and capital allocation.

This creates an AR software for professional services that is both disciplined and flexible. The collections process is consistent yet feels human. For firms using QuickBooks AR automation, data flows seamlessly from invoice creation to final reconciliation.

The New Standard for Financial Operations

This approach transforms your AR function from a cost center into a strategic asset. You are no longer just collecting cash; you are actively managing and optimizing it. This proactive posture makes your firm more financially resilient and positions it for sustainable growth.

Resolut automates AR for professional services—consistent, accurate, and human. Learn more at Resolut.