What is a credit sale? A CFO's Guide to Cash Flow and DSO

Discover what is a credit sale and how it shapes cash flow and DSO for CFOs in 2026. Practical insights for receivables management.

In professional services, nearly every transaction is a credit sale. We deliver our expertise, issue an invoice, and get paid at a later date. This is standard operating procedure.

This creates an account receivable. Unlike a cash sale, where payment is immediate, this model introduces a time gap between recognizing revenue and realizing cash. For finance operators, managing this gap is a primary function.

Understanding the Operational Impact of a Credit Sale

A credit sale is the trigger for the cash conversion cycle. When an invoice is issued, revenue is recognized on the income statement, but simultaneously, a current asset—accounts receivable—is created on the balance sheet.

This asset represents a promise of future cash. Until that promise is fulfilled, the funds are not liquid, tying up the firm's working capital.

Every credit sale is an extension of trust, which inherently involves risk. The longer it takes a client to pay, the higher the Days Sales Outstanding (DSO), creating a direct strain on cash flow. Clear terms, defined in service contracts, are non-negotiable. A Free AI Contract Generator can help structure these agreements.

A credit sale transforms billable hours into a financial asset. The efficiency of converting that asset back into cash defines the financial health of the firm.

The table below provides a straightforward comparison of how credit and cash sales impact firm financials.

Credit Sale vs Cash Sale At a Glance

Attribute | Credit Sale | Cash Sale |

|---|---|---|

Timing of Payment | Payment is received after service delivery (e.g., Net 30, Net 60). | Payment is received at the time of service delivery. |

Initial Impact | Increases Accounts Receivable (asset) and Revenue. | Increases Cash (asset) and Revenue. |

Cash Flow Impact | Delayed positive cash flow; cash is not realized until payment. | Immediate positive cash flow. |

Risk Involved | Introduces credit risk and the potential for bad debt. | No credit risk; payment is guaranteed. |

While extending credit is necessary to compete in professional services, mastering its mechanics is essential for financial stability. It is a matter of ensuring liquidity keeps pace with profitability.

The Accounting Mechanics of a Credit Sale

Understanding the concept of a credit sale is simple. Translating it correctly onto the firm's books is what matters. Every credit sale initiates a two-part accounting entry impacting both the income statement and the balance sheet.

Imagine a consulting firm completes a $50,000 project. The moment the invoice is sent, the revenue is earned, even though no cash has been received. This triggers the first journal entry.

The Initial Journal Entry: Recognizing Revenue

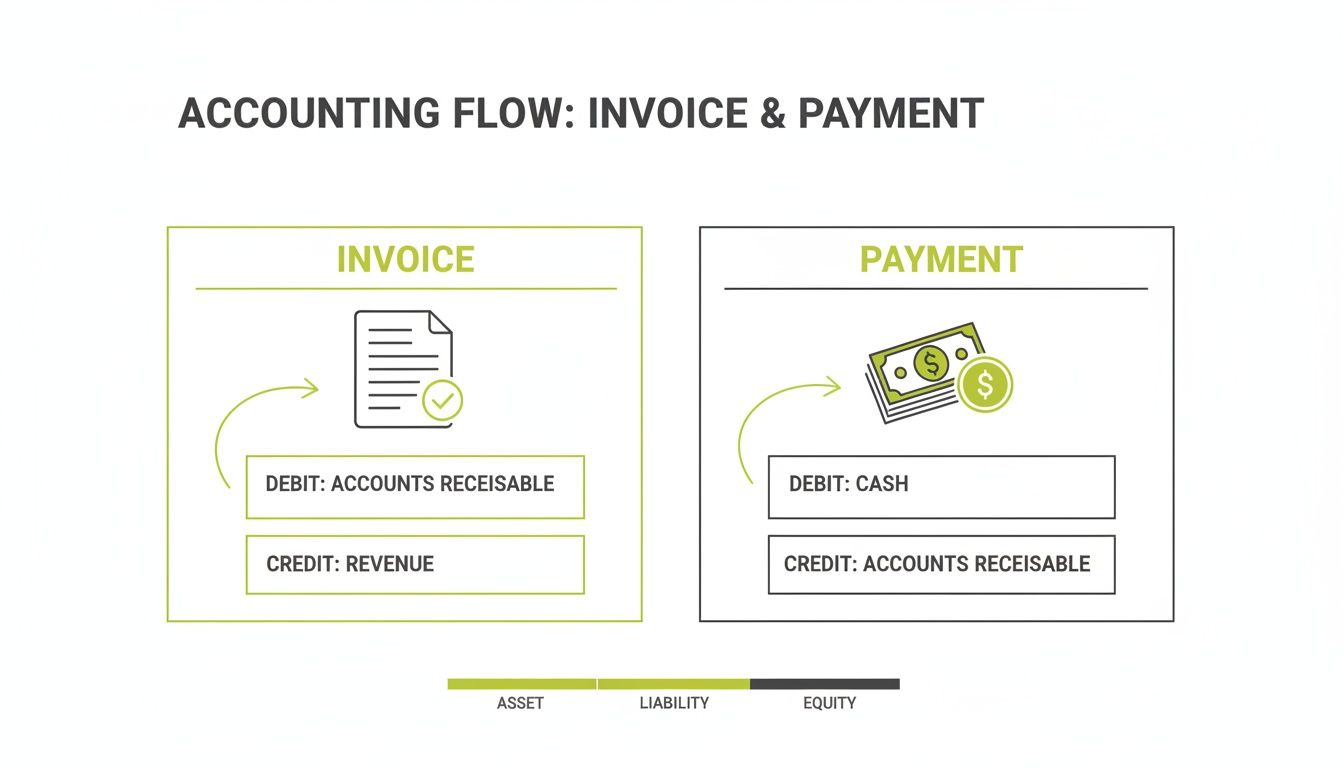

When the invoice is issued, the books must reflect the value delivered. A journal entry is made to debit Accounts Receivable and credit Service Revenue. This increases an asset (the promise of future cash) while boosting top-line revenue.

Journal Entry: At Time of Invoice >* Debit: Accounts Receivable $50,000* Credit: Service Revenue $50,000

This entry starts the clock. That $50,000 is now a receivable awaiting collection. Correctly calculating earned revenue is a cornerstone of financial reporting; our guide on how to find net credit sales offers more detail.

The Second Journal Entry: Realizing Cash

The cycle completes when cash is received. The second transaction settles the account and converts the receivable into working capital. The Cash account is debited, and Accounts Receivable is credited.

Journal Entry: Upon Receipt of Payment >* Debit: Cash $50,000* Credit: Accounts Receivable $50,000

With this, the receivable is cleared. The cash has moved from the client's balance sheet to yours.

These two events—recognizing revenue and realizing cash—are the foundation of accrual accounting. The shorter the time between these two entries, the healthier the firm's liquidity. This is where tools from QuickBooks AR automation to specialized AR software for professional services can reduce DSO and accelerate that critical second step.

The True Cost of Credit on Cash Flow and DSO

A credit sale means revenue is earned, but cash is not yet in hand. This is a fundamental tension. Every invoice represents money that is rightfully yours, yet it sits on the balance sheet as an account receivable. The operational question is not just "what is a credit sale?" but "what is this sale costing us until it’s paid?"

This delay is measured by a critical metric: Days Sales Outstanding (DSO). DSO represents the average number of days it takes to convert an invoice into cash. A high DSO is a clear indicator that cash is tied up, squeezing liquidity.

Calculating and Interpreting DSO

Calculating DSO is straightforward. It requires looking at receivables relative to sales over a specific period.

DSO Formula: (Total Accounts Receivable / Total Credit Sales) x Number of Days in Period

If a firm has $500,000 in AR and generated $1.5 million in credit sales during a 90-day quarter, its DSO would be 30 days. This means an average one-month wait for payment. This is where profitable firms encounter cash flow problems. Profitability on paper does not cover payroll. We cover this in more detail in our guide on what is DSO.

This diagram breaks down the two distinct events in a credit sale—invoicing and payment—and shows how they hit your books at different times.

The sale boosts revenue immediately, but the cash does not arrive until later. DSO measures that critical delay.

Why DSO Is a Competitive Lever

Monitoring DSO is a strategic discipline, not just an accounting task. Business runs on credit. For example, European credit markets saw issuance levels hit roughly €140.9 billion in high-yield bonds and €306 billion in leveraged loans in a recent year, while U.S. figures were $352.6 billion and $828.9 billion, respectively. These figures, from a report on 2026 leading credit trends at Octus.com, show the scale of corporate reliance on credit. In such an environment, efficient cash collection provides a distinct competitive advantage.

For a professional services firm, a lower DSO translates into measurable outcomes:

- Improved Cash Flow: More working capital is available for operations, investment, or a larger cash reserve.

- Reduced Financing Costs: Greater liquidity reduces reliance on expensive lines of credit to cover operational expenses.

- Stronger Financial Health: A predictable, rapid cash cycle creates stability and gives leadership greater control.

The objective is to reduce DSO without damaging client relationships. This requires a systematic approach to accounts receivable, moving from reactive collections to proactive cash flow management. This is where modern AI AR automation delivers significant operational lift.

Managing Credit Risk and Collections Systematically

Extending credit introduces risk. For professional services firms, managing that risk is a balancing act. Overly aggressive collections can damage the client relationships that are the firm's core asset. The goal is to move from reactive problem-solving to a systematic, controlled process.

Effective risk management begins with a documented credit policy that defines payment terms, credit limits, and delinquency protocols. This document is the operational playbook for every credit sale.

Building a Structured Credit and Collections Process

Applying the same generic reminder to a high-value, long-term client and a new account is poor practice. A structured process allows for a tailored, more effective approach.

This is achieved through two key activities:

- Pragmatic Client Assessment: Before extending significant credit, conduct due diligence. This can be as simple as reviewing payment history, requesting references for new clients, or setting a credit limit appropriate for the engagement's scope.

- Systematic Collections Cadence: Design a collections workflow that is persistent and professional. It should be a sequence of escalations, beginning with automated reminders and progressing to direct, personal follow-ups as an invoice ages.

Data shows that roughly 10% of invoices may go unpaid. A passive "wait and see" approach is not a viable strategy. A proactive plan is necessary to protect cash flow.

Effective risk management is not about aggressive tactics. It is about control through informed, systematic processes that preserve client trust while ensuring timely payment.

From Manual Effort to Automated Oversight

Manually tracking reminders, follow-up calls, and escalating accounts is a significant operational drag. This administrative burden is a classic bottleneck. This is where accounts receivable automation fundamentally changes the dynamic.

Instead of teams spending hours on collections, platforms using AI AR automation can segment clients based on payment behavior and risk. The system then executes personalized outreach campaigns autonomously. This frees up finance professionals to focus on the exceptions—high-risk accounts that require a human-to-human conversation. This is a critical step to improve cash flow and maintain control.

Ultimately, managing the risk of a credit sale requires the right systems. Whether built through internal policies or implemented with dedicated AR software for professional services, the objective is a predictable, controlled process that converts receivables into cash.

How AR Automation Restores Control Over Cash Flow

Managing the inherent risk of every credit sale is an operational imperative, but manual execution is inefficient. It consumes valuable time and delays cash realization. Chasing payments is not a high-leverage use of a finance professional's skill set. The solution is not to chase harder, but to build a more intelligent, controlled process.

This is where accounts receivable automation provides a step-change in capability. By implementing an intelligent system, you shift from reactive firefighting to proactive cash flow management. The outcome is restored control and predictability over a core financial function.

From Manual Workflows to Intelligent Orchestration

For many professional services firms, AR management is a disjointed process of spreadsheets, emails, and calendar reminders. It is inefficient by design. AI AR automation replaces this manual effort with a coordinated system engineered to reduce DSO and accelerate cash flow.

An automated system can sort clients by payment history, invoice age, and contract terms. This risk-profiling enables personalized communication plans that are both persistent and professional.

An automated AR system ensures the right message reaches the right client at the right time—without requiring manual intervention for routine follow-ups. This consistency accelerates payments while preserving client relationships.

The impact on cash flow is direct and measurable. Firms adopting AR automation frequently reduce Days Sales Outstanding by 20-30% within a few quarters. For a firm with $5 million in annual revenue, reducing DSO by just 15 days frees up over $200,000 in working capital. Further gains can be found with tools like automated invoice processing software.

This shift toward structured finance is a broad trend. The global private credit market, for instance, saw funds close with $224.25 billion in 2025 as corporations opted for private credit over traditional loans. For finance leaders, this highlights the rising importance of disciplined internal credit management. More details are available on these global private credit fundraising trends at S&P Global.

Unlocking Strategic Value from Your Finance Team

When the finance team is freed from the daily administrative burden of collections, they can focus on higher-value analysis. The core question shifts from "Who do I need to chase today?" to "Which clients pose a growing credit risk?" and "How can we adjust payment terms to improve cash flow?"

AR platforms provide the data to answer these strategic questions. With clear visibility into payment trends and at-risk accounts, you gain true operational control. While basic QuickBooks AR automation is a starting point, dedicated AR software for professional services provides the capabilities needed for a $3M–$50M firm. You can explore these concepts further in our guide on how to automate accounts receivable.

The Resolut Approach to Intelligent Receivables

Understanding credit sale theory is one thing. Managing the receivables lifecycle day-to-day is another operational challenge entirely. Professional services firms must move beyond manual processes that consume expert time and delay cash flow.

Resolut is designed to provide this operational layer, giving finance leaders the tools to control their cash cycle. It replaces the ad-hoc mix of spreadsheets and email reminders with a single, clear system built to shorten the time between invoice and payment.

From Reactive Collections to Proactive Cash Flow

The approach is built around a single, measurable goal: to reduce DSO and improve cash flow. This is achieved by connecting specific capabilities to the most common pain points in accounts receivable management.

In practice, this includes:

- Smart Client Communication: We help configure automated, yet personalized, outreach via email and SMS. The messaging remains on-brand and consistent, ensuring the right reminder reaches the right client at the right time.

- A Frictionless Payment Portal: We provide a clean, simple payment portal for clients. By offering flexible payment options, we remove common roadblocks that delay payment.

- Automated Cash Application: Incoming payments are automatically matched and reconciled. This alone saves hours of manual work and provides a real-time, accurate view of your cash position.

This level of AI AR automation helps the system identify at-risk accounts early. It frees your team to focus their expertise on complex situations and client relationships that require a human touch. Your AR function shifts from a reactive cost center to a strategic component of the firm's financial health.

With Resolut, you gain the visibility and control needed to manage every credit sale, from invoice to cash, with confidence and predictability.

Common Questions from Finance Leaders

In managing receivables, the same operational questions tend to surface. Here are my thoughts on a few common ones from fellow finance leaders.

What Is a Good DSO for a Professional Services Firm?

While firm-specific factors matter, a healthy DSO for a professional services firm generally falls between 30 and 45 days. This serves as a solid benchmark.

A DSO consistently above 60 days is a red flag. It indicates that cash is trapped in receivables, straining working capital. More important than hitting a single number is achieving a steady downward trend. That is the true indicator that process improvements are working to improve cash flow.

How Can We Implement AR Automation Without Disrupting Our Team or Clients?

The prospect of a large tech implementation can be daunting. Modern AR software for professional services is designed for integration, not disruption. A "co-pilot" approach works well: the system handles repetitive tasks like reminders, freeing your team to manage the high-value client relationships.

A phased rollout is the best practice. Start with a small client segment to test and refine the workflow. This ensures automated communications feel personal and align with your brand voice before a full-scale deployment.

This strategy allows your team to acclimate to the new tools and see the direct benefits of accounts receivable automation firsthand.

Does Automating Accounts Receivable Mean We Lose Control?

This is a common concern, but the reality is the opposite. Automation provides a level of visibility and control that is impossible to achieve with manual processes. Instead of information scattered across spreadsheets and email, you gain a single, unified dashboard.

This central hub shows the status of every invoice and flags at-risk accounts instantly. Your team can then manage by exception, applying their expertise where it is most needed. This data-driven oversight allows you to reduce DSO by making informed, strategic decisions, whether using basic QuickBooks AR automation or more advanced AI AR automation platforms.

--- Resolut automates AR for professional services—consistent, accurate, and human. Learn more at https://www.resolutai.com.