Optimizing AI for Debt Collection: A 2026 CFO Guide

Boost cash flow and reduce DSO with AI for debt collection. Learn how AR automation ensures compliance and drives ROI for professional services firms in 2026.

Enterprises lose $200B annually to unpaid invoices according to Interval AI’s analysis of AI-driven debt collection. That number should change how finance leaders think about ai for debt collection.

For a professional services firm, the issue isn’t “collections technology.” It’s control. It’s whether invoices move through a disciplined system, whether partners can forecast cash with confidence, and whether your finance team spends time collecting money or chasing administrative debris.

Most firms in the $3M to $50M range don’t have a debt problem in the classic consumer sense. They have an accounts receivable discipline problem. Follow-up happens too late. Message tone is inconsistent. Account managers override process. Controllers lack a clean view of risk. And cash flow suffers long before anyone writes off bad debt.

AI AR automation fixes that when it’s implemented as a finance operating layer, not a novelty feature.

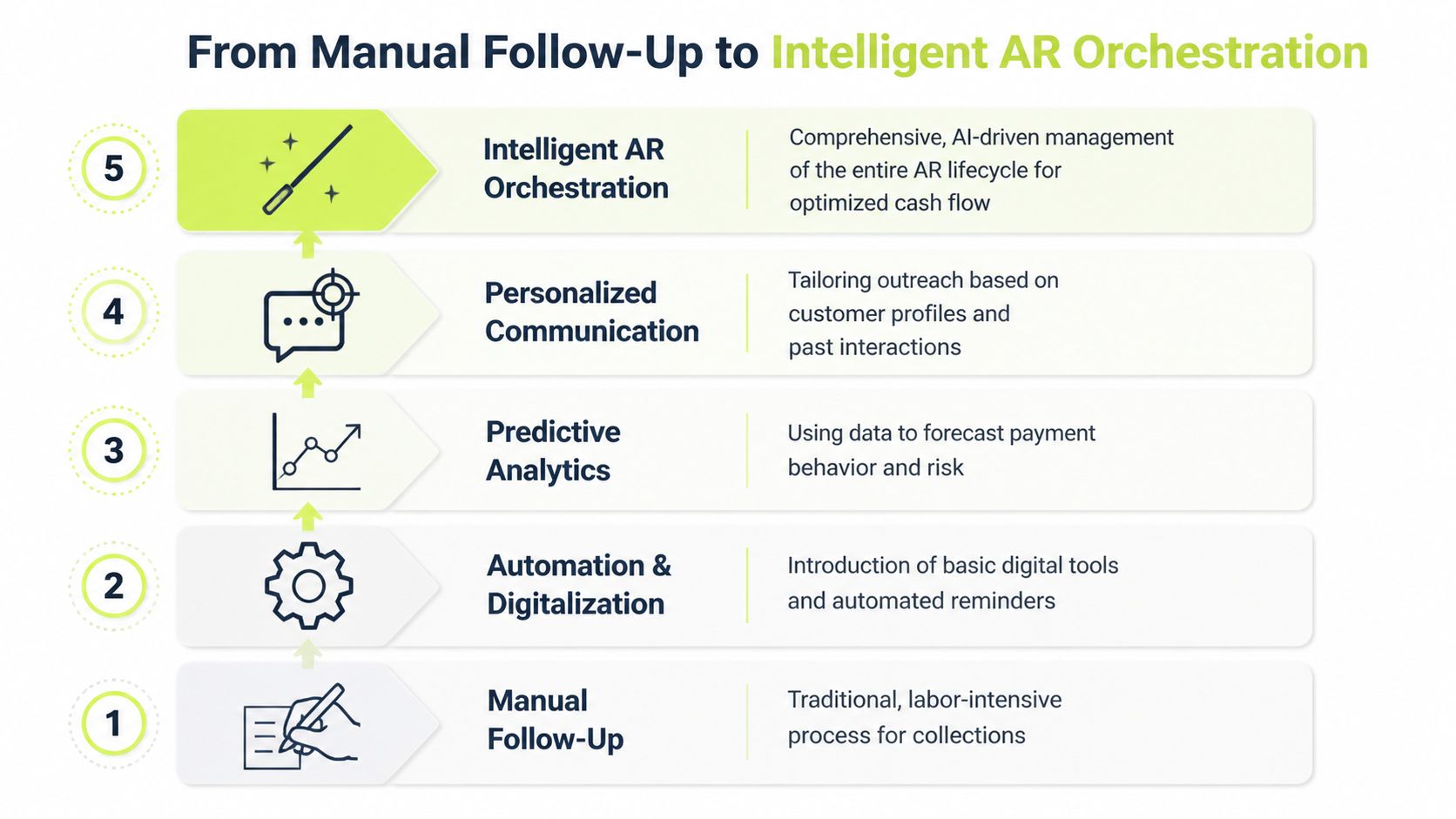

From Manual Follow-Up to Intelligent AR Orchestration

Manual collections break down in predictable ways. Your team sends reminders in batches, escalates based on who’s shouting loudest, and relies on memory to decide which client needs a soft touch and which one needs a firm notice. That isn’t a process. It’s improvisation.

A better frame is intelligent AR orchestration. That means one system coordinates timing, channel, tone, prioritization, escalation, and documentation across the full receivables cycle. The point isn’t to sound futuristic. The point is to make AR behave like a controlled financial process.

What changes when AI runs the workflow

The biggest shift is that follow-up stops being reactive.

Machine learning models can process hundreds of data points, including payment history and interaction sentiment, to prioritize outreach and tailor communication strategies. In that context, CR Software notes up to 30% higher recovery rates from predictive account scoring.

That matters in a professional services firm because not all overdue invoices mean the same thing. A strategic client with a temporary approval bottleneck shouldn’t get the same sequence as a chronically slow payer who only responds to firm escalation. AI AR automation helps your team distinguish between those cases early.

Here’s what intelligent orchestration usually includes:

- Risk-based prioritization: The system scores accounts based on payment behavior, aging, and engagement signals so your team works the highest-probability and highest-risk items first.

- Channel selection: It decides whether email, SMS, phone, or a self-service portal is most likely to move the invoice.

- Tone control: It supports softer language for relationship-sensitive accounts and stricter sequences when discipline matters more than diplomacy.

- Task reduction: It automates reminders, logs interactions, updates statuses, and keeps records current without constant manual entry.

Practical rule: If your collections process depends on individual memory, it’s already costing you cash.

Why finance should own the orchestration logic

Many firms falter at this specific point. They treat AR automation as an administrative tool instead of a finance control system. Consequently, they let messaging drift, exceptions pile up, and accountability disappear.

The finance leader should define the operating rules:

- Which invoices enter automated reminder flows.

- Which accounts require human review.

- When account managers are notified.

- When legal or executive escalation begins.

- How payment promises, disputes, and exceptions are documented.

If you’re assessing process maturity before selecting software, this dunning management software guide is a useful reference because it forces the right operational questions around sequencing, escalation, and policy design.

The firms that benefit most from ai for debt collection don’t “automate collections.” They build a repeatable AR system that behaves like a strong finance operator. It doesn’t sleep, it doesn’t forget, and it doesn’t improvise with your cash.

Quantifying the Financial Impact on Your P&L

A 10-day reduction in DSO can release a meaningful amount of cash from a services firm's balance sheet without adding a dollar of new revenue. That is the finance case for AI in receivables.

CFOs should evaluate AI AR on four outcomes. Faster cash conversion. Lower cost-to-collect. Tighter control over exception handling. Lower bad debt exposure.

The first metric is DSO. For professional services firms, high DSO usually points to weak post-invoice discipline, inconsistent follow-up, or poor escalation timing. AI improves that operating rhythm by pushing the right account into the right sequence sooner, documenting every touch, and reducing the lag between client behavior and finance response.

The P&L impact shows up quickly:

- Lower financing drag: Earlier collections reduce reliance on credit lines, partner distributions, or internal cash reserves.

- Stronger forecast accuracy: Cash receipts become easier to model when follow-up is scheduled and tracked instead of improvised.

- Lower labor cost per invoice: Finance teams spend less time chasing status updates and more time resolving disputes that put revenue at risk.

- Lower write-off risk: Faster intervention limits the number of accounts that drift from slow pay to bad debt.

The balance sheet improves first. The income statement follows.

A lot of leadership teams are disciplined about measuring sales and marketing spend, then become vague when they assess receivables operations. That is a mistake. This B2B RevOps guide to marketing ROI is useful because it reinforces the right habit. Tie operating spend to measurable return. AR software should face the same standard.

What to measure before you approve budget

Do not approve an AI AR platform on feature count. Build the case around baseline metrics and target movement over two quarters.

Track these five numbers before and after deployment:

- DSO

- Average days past due by client segment

- Cost-to-collect per invoice and per dollar collected

- Promise-to-pay kept rate

- Bad debt as a percentage of billings

If you want a tighter framework for defining those workflows and controls, this receivable management system guide is a useful reference.

The ROI logic is simple

If the platform shortens collection cycles, finance gets cash earlier. If it standardizes routine follow-up, labor cost drops. If it flags risk sooner, fewer accounts age into write-offs. Those three effects matter more than any claim about AI sophistication.

For a services firm, the biggest gain is usually not payroll reduction. It is better financial control. Account managers stop freelancing the collections process. Exceptions get surfaced earlier. Finance can see which invoices are at risk, which clients are slipping, and where policy is being ignored.

Measure AI AR against DSO improvement, cash flow timing, cost-to-collect, and bad debt reduction. If the vendor cannot show a path to those outcomes, the software does not belong in your finance stack.

A short explainer on the operating model is worth watching before you build your internal business case.

If your current process depends on individual judgment to decide who gets chased next, you do not have a scalable AR function. You have avoidable cash flow risk.

The Core Capabilities of an AI AR Platform

Not every platform that claims ai for debt collection manages receivables effectively. Some are reminder engines with a chatbot attached. A real AI AR platform should improve control across six operating areas.

Predictive scoring and workflow prioritization

The system should rank invoices by risk and likely response path, not just age them. In a services firm, that helps finance spot a client whose payment pattern is changing before the account becomes a write-off issue.

Personalized outreach across channels

Email alone is usually not enough. Strong AI AR automation adjusts message timing, tone, and channel based on account behavior, while keeping the communication history centralized so finance and client service aren’t working from different records.

Intelligent workflow orchestration

This is the layer that matters most. Rules should determine what happens when a client opens a reminder but doesn’t pay, misses a promise-to-pay date, disputes an invoice, or partially pays.

A mature receivables setup usually includes the same control logic described in a solid receivable management system: workflow ownership, status visibility, clean escalation paths, and measurable accountability.

Self-service payment options

Clients pay faster when friction is low. A good platform should route them directly from reminder to payment, not force them into an email thread with accounting just to resolve an invoice.

For professional services firms, this matters because partners often assume “relationship accounts” need white-glove handling when what they really need is a simple, clear payment path.

Conversational AI for call handling and documentation

Phone conversations still matter, especially for disputes and larger balances. But manual note-taking and after-call admin drain productivity.

According to CGI’s review of AI in debt collections, conversational AI with NLP-powered call summarization can reduce after-call work by 30% and shorten call times by more than a minute. That directly improves throughput for teams managing volume.

Escalation triggers and cash application support

The platform should know when to move from standard reminders to executive review, legal language, or outside escalation. It should also help reconcile incoming payments cleanly so unapplied cash doesn’t create false delinquency.

Here’s the test I use when evaluating capabilities:

- If it can send reminders but not control exceptions, it’s basic automation.

- If it can prioritize accounts but not document decisions, it creates risk.

- If it can automate outreach but not accelerate reconciliation, it only solves half the AR problem.

- If it can support both autopilot and human review, it’s closer to a real finance system.

A capable platform should make your team better at exceptions, not busier with routine follow-up.

Managing Compliance and Protecting Client Relationships

Most discussions of ai for debt collection focus on efficiency. That’s incomplete. The key question is whether automation improves discipline without creating legal exposure or damaging valuable client relationships.

Those are the two failure modes that matter in a professional services firm.

Compliance has to be designed into the process

A critical blind spot in AI adoption is the risk of scaling poor behavior faster. Experian’s discussion of AI in debt collection highlights the danger clearly: deploying AI at scale without audit trails, compliance infrastructure, and human oversight for edge cases can create legal and reputational liability.

That’s why finance should insist on a few baseline controls:

- Auditability: Every reminder, reply, promise-to-pay, dispute, and escalation should be logged.

- Rule enforcement: Contact timing, escalation language, and workflow triggers should follow policy, not employee discretion.

- Human review: Sensitive cases need a clear handoff point.

- Data controls: Payment behavior, contact records, and client financial details need appropriate protection.

If your team is tightening controls around customer data and process integrity, this practical overview of data security and compliance for SMBs is worth reviewing alongside your AR automation plans.

Relationship risk is real in B2B collections

Consumer-style collection logic doesn’t map neatly to professional services. Some overdue clients are also long-term revenue sources, referral channels, or strategically important accounts. Treating every delinquency the same is lazy finance.

Your workflow should separate accounts into relationship tiers. A high-value client with a temporary AP issue should trigger collaborative outreach. A chronically late, low-value client can move through a firmer sequence with less partner time involved.

Boardroom takeaway: Optimize for enterprise value, not just invoice recovery.

That’s where human-in-the-loop control matters. The system should surface risk, recommend next actions, and enforce documentation. But leadership should still decide when relationship preservation outweighs short-term pressure.

A structured communication framework also helps. If your team still relies on inconsistent ad hoc emails, use a tighter standard for notices and escalations. Even a simple reference point like this debt recovery letter template can improve consistency in tone and documentation.

What good governance looks like

The right setup is not “fully automated everything.” It’s controlled automation.

Use automation for routine reminders, status updates, payment links, and standard follow-up. Keep people involved for disputed invoices, high-value accounts, hardship cases, and any escalation that could affect the client relationship.

That balance gives you three advantages. You get consistency, you keep an audit trail, and you avoid letting software make judgment calls that belong to leadership.

Your Implementation Roadmap and Change Management Plan

Most AR automation projects fail for a simple reason. Leadership buys software before it defines operating rules.

The implementation plan should start with policy, ownership, and measurement. Then you layer in workflow automation. That sequence matters because your team needs to know what the system is supposed to enforce.

Start with a narrow pilot

Pick one segment of receivables. Good candidates include older invoices, a single business unit, or accounts with repetitive payment behavior. Don’t start with your most politically sensitive clients.

Before launch, establish a baseline for:

- DSO trend

- Collection effort by team

- Promise-to-pay follow-through

- Dispute frequency

- Bad debt or write-off pattern

- Time spent on manual reminders and status updates

Then define where automation runs on autopilot and where staff stay in control.

Build around roles, not features

Finance owns policy. Account managers protect relationships. Operations or IT supports integration. If those roles blur, exceptions pile up and no one knows who can override the workflow.

A practical rollout often looks like this:

- Phase one: Automate reminders, segmentation, and payment routing.

- Phase two: Add predictive prioritization and exception handling.

- Phase three: Introduce co-pilot support for calls, disputes, and escalations.

- Phase four: Standardize reporting so leadership can manage AR by exception instead of anecdote.

If you need a reference point for the broader operating model, this guide on how to automate accounts receivable is a helpful checklist for sequencing the work.

Expect adoption pressure to keep rising

This isn’t a niche category anymore. Technavio projects the global AI for debt collection market will grow by USD 2.77 billion from 2025 to 2029 at a CAGR of 15%, driven by operational efficiency and features that can improve customer satisfaction by 15%.

That projection matters less as a market headline and more as a signal. Your peers are looking for the same thing you are. Faster collections, lower manual effort, and better client experience under tighter financial control.

Don’t train your team to “use the tool.” Train them to manage exceptions, enforce policy, and escalate with judgment.

Change management is easier when the message is simple. You’re not replacing finance judgment. You’re removing avoidable manual work so the team can focus on the invoices and relationships that require attention.

Evaluating AI AR Platforms A Checklist for Leaders

Vendor demos usually overemphasize interface and underemphasize control. That’s backwards. The right platform should fit your finance process, your client profile, and your tolerance for risk.

In B2B settings, the system also needs to weigh recovery against relationship risk. Moveo’s discussion of AI use cases in debt collection makes that point well. Firms should triage outreach based on customer lifetime value, not just delinquency, to avoid damaging high-value relationships.

AI AR Platform Evaluation Checklist

Evaluation Criterion | What to Look For | Why It Matters |

|---|---|---|

Integration with accounting stack | Native or reliable integration with QuickBooks and adjacent finance systems | QuickBooks AR automation only works if invoice status, payments, and notes stay synchronized |

Workflow configurability | Custom reminder sequences, escalation rules, dispute handling, and approval paths | Professional services firms don’t all collect the same way |

Risk-based segmentation | Ability to prioritize by payment behavior, invoice risk, and client importance | You need discipline without treating every client identically |

Human-in-the-loop controls | Co-pilot options, approval checkpoints, manual override rights | Leadership should keep judgment on sensitive accounts |

Omnichannel communication | Email, SMS, phone support, and centralized conversation history | Clients respond on different channels, and finance needs one record |

Self-service payment experience | Clear invoice views, easy payment options, low-friction resolution paths | Faster payment often comes from less friction, not more pressure |

Compliance and audit trail | Logged interactions, policy enforcement, access controls, escalation history | This protects the firm if a process or communication is challenged |

Analytics and KPI reporting | DSO tracking, promise-to-pay reporting, recovery visibility, team activity insights | If you can’t measure improvement, you can’t manage ROI |

Cash application support | Reconciliation workflow, payment matching, unapplied cash visibility | Collections gains get diluted when cash posting lags |

Legal escalation readiness | Structured handoff, authoritative notices, documentation completeness | Some accounts need a firmer path without operational chaos |

Questions I’d ask in every demo

Ask vendors to show the workflow for an invoice that is overdue, disputed, partially paid, and owned by a strategic client. That exposes whether the platform handles real operating complexity or just standard reminders.

Also ask these directly:

- How does the system handle high-value relationship accounts?

- What can finance lock down by policy?

- Where does human approval sit in the workflow?

- How does it document disputes and promises-to-pay?

- What does QuickBooks AR automation sync, and how often?

- Can leadership see exception queues without asking staff for updates?

What good platform fit looks like

For a professional services firm, the best platform isn’t the one with the most AI language. It’s the one that gives finance tighter execution with less manual drag.

That usually means:

- Strong accounting integration

- Flexible communication logic

- Clear separation between autopilot tasks and human decisions

- Reliable audit trails

- Payment workflows that reduce friction

- Reporting that ties activity to cash outcomes

If a vendor can’t show those things live, assume the product is lighter than the pitch.

Conclusion The Path to Predictable Cash Flow

AI for debt collection is most useful when you stop thinking about it as collections software and start treating it as financial process control. The key payoff is better DSO management, steadier cash flow, lower collection cost, and fewer preventable write-offs.

For professional services firms, the winning approach is simple. Automate routine execution. Keep humans on exceptions. Protect compliance. Protect client value. Measure everything that affects cash.

Resolut automates AR for professional services with a focus on consistency, accuracy, and human control. If your firm wants tighter follow-up, better visibility, and a more disciplined path to cash, Resolut is built for that.