Automatic Payment Pools: Boost Cash Flow & Automate AR

Unlock faster, more predictable cash flow with automatic payment pools. CFOs: Reduce DSO, automate AR, and optimize finance with this modern solution.

Revenue can look healthy on paper while cash stays stubbornly unpredictable.

If you run a professional services firm, you know the pattern. Invoices go out on time. Clients say they'll pay. Then the money lands in fragments, with vague remittance notes, partial payments, and just enough delay to distort your weekly cash view. Your controller spends hours matching receipts, your project leads keep asking whether a client is “current,” and your forecast keeps getting revised because collections are still too manual.

That isn't a sales problem. It's an operating model problem.

We should treat cash-in the way we treat payroll, close, and procurement. As a controlled process. Automatic payment pools are a practical way to do that. In a corporate AR context, they centralize incoming payments, apply rules to identify and post them, and remove as much human chasing and reconciliation work as possible. If we want to reduce DSO, improve cash flow, and stop relying on spreadsheet heroics, this is the right frame.

The Unpredictable Nature of Accounts Receivable

A familiar scenario: the firm finishes a strong month. Utilization is solid. New work is signed. Billing goes out. Yet cash still feels shaky because collections arrive unevenly and no one can tell, with confidence, which invoices will clear this week.

That instability creates second-order problems. Hiring decisions get delayed. Partner distributions get debated longer than they should. The finance team spends too much time answering basic questions that should already be visible in the system.

What chaos looks like in practice

In most firms, AR friction doesn't show up as one dramatic failure. It shows up as dozens of small, expensive misses:

- Payment follow-up happens inconsistently. One client gets three reminders. Another gets none because the account owner assumed finance had it covered.

- Cash application is too manual. A payment arrives through ACH, card, or wire, and someone still has to interpret memo lines and hunt through open invoices.

- Disputes surface late. The client didn't approve a time entry, wants a revised invoice, or routed the bill to the wrong AP contact. We find out only after the due date passes.

- Forecasting stays fuzzy. The pipeline may be healthy, but near-term cash remains a judgment call.

Professional services firms feel this more acutely because invoices often reflect retainers, milestone billing, recurring monthly work, pass-through expenses, and project overruns all at once. That mix creates a lot of room for payment friction.

Practical rule: If collections depend on people remembering who to nudge, when to nudge them, and how to post the payment after it arrives, the process isn't under control.

Why manual AR keeps costing more than it seems

Most leaders underestimate the burden because the work is distributed. A bookkeeper touches the payment. A controller reviews the exception. A partner sends the awkward follow-up email. An operations lead confirms whether the project should keep moving. No single step seems catastrophic. Together, they create drag across the firm.

Automatic payment pools become useful as an operating strategy. We're not talking about a new bank account or a speculative instrument. We're talking about a controlled intake and routing layer for receivables. Payments come into one orchestrated system, the system applies rules, and exceptions get surfaced instead of buried.

That's how we replace AR anxiety with cadence. Not by chasing harder, but by designing the flow better.

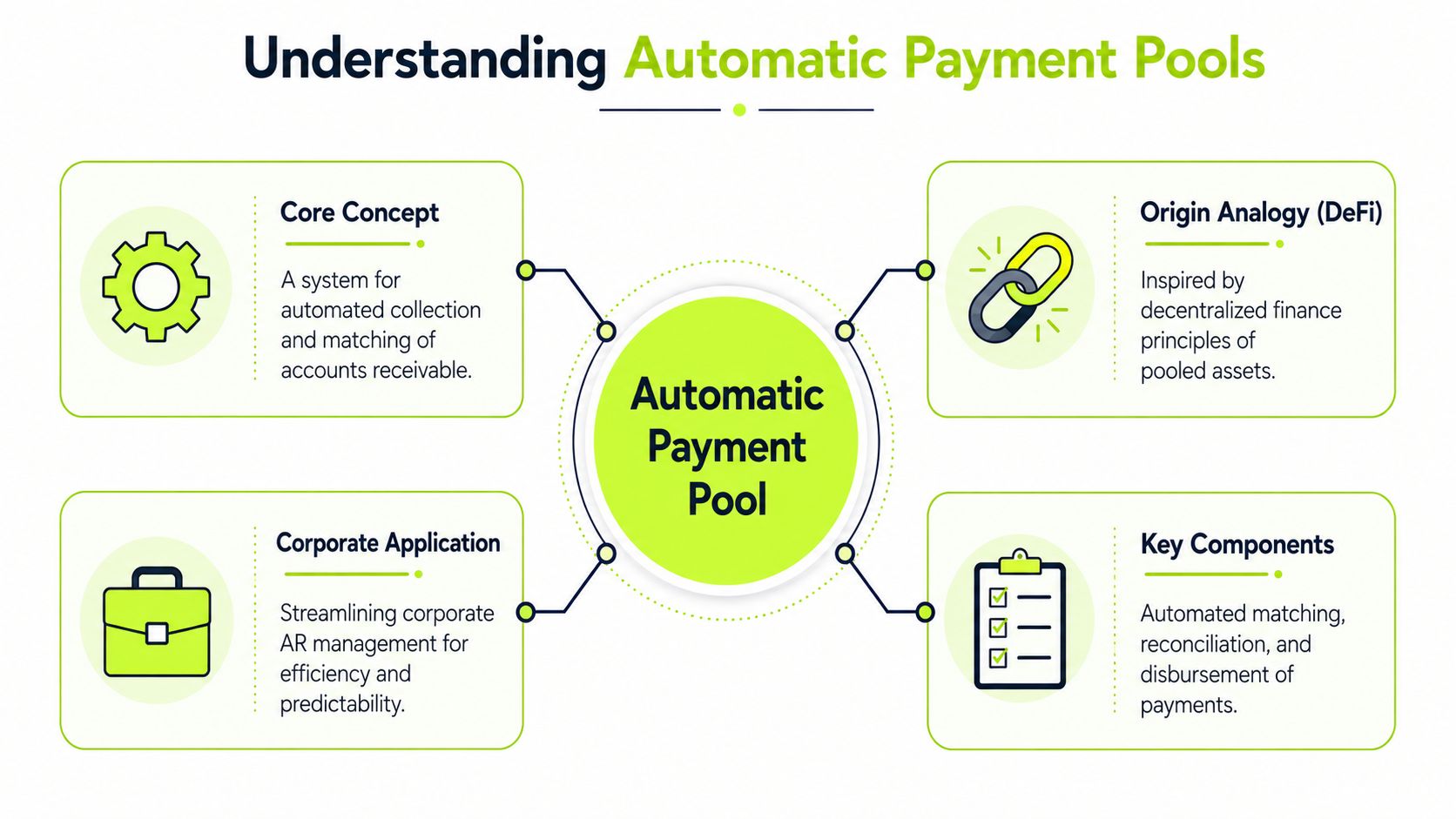

Defining Automatic Payment Pools in Corporate AR

The term comes from a different world, so let's clean it up.

In decentralized finance, a liquidity pool is a programmable reserve of digital assets locked in a smart contract, and automated market makers use that pool to set prices and execute trades without a traditional order book. Multiple sources describe that shift as a foundational move away from centralized intermediaries and toward algorithmic, 24/7 markets, as explained in BankingHub's overview of liquidity pools and automated market making.

That's the analogy. Not the model we should copy directly.

What the term should mean for finance leaders

In corporate AR, automatic payment pools should mean a software-defined cash collection layer where incoming client payments are aggregated, identified, matched to open invoices, and reconciled based on rules.

The point is operational control. We pool the payment intake logic, not the economic risk.

A standard operating account receives funds. An automatic payment pool adds intelligence on top of that flow:

Component | What it does in AR |

|---|---|

Centralized intake | Collects payments from card, ACH, wire, and digital channels into one governed workflow |

Matching logic | Uses invoice numbers, payer identity, amount, timing, and rules to apply cash automatically |

Exception handling | Routes short pays, overpays, unapplied cash, and split payments to the right person |

Reconciliation layer | Updates the accounting system and keeps subledger activity aligned |

Why this framing matters

Most firms already have pieces of this. They have QuickBooks, NetSuite, Stripe, or a bank portal. What they usually don't have is orchestration.

That's the gap. Without orchestration, teams still rely on inboxes, exported reports, and tribal knowledge. With orchestration, the system does the first pass on every payment and finance only handles the exceptions that require judgment.

The best AR process isn't the one with the most reminders. It's the one that makes paying easy, matching automatic, and exceptions visible.

This re-framing also helps separate corporate finance from crypto hype. The useful lesson from DeFi is automation through predefined logic. If you want a side example of how programmable payment behavior shows up in digital commerce, this guide to non-custodial crypto subscriptions is worth scanning for the recurring-payment mechanics, even if your firm operates entirely in B2B fiat workflows.

For CFOs and controllers, the decision is simpler than the terminology suggests. We either continue treating collections and cash application as a people-heavy back-office task, or we turn them into a rule-based system. I'd choose the system every time.

The Tangible Benefits for Your Firm's Bottom Line

The value of automatic payment pools isn't conceptual. It shows up in three places that matter to every finance leader: collection speed, reconciliation effort, and forecast confidence.

If a firm wants accounts receivable automation to do real work, those are the outcomes to judge it by. Not feature count. Not dashboard design. Not AI branding.

Faster cash conversion

When payment links are embedded in invoices, reminders follow a schedule, and clients can pay through the channel they prefer, the path from invoice to cash gets shorter. That matters more than almost any cosmetic AR improvement.

We should expect two changes. First, fewer invoices sit untouched because the client “never got around to it.” Second, fewer payments arrive without enough context to post them cleanly. That combination is how firms reduce DSO in practice.

The broader payment market already supports this shift. Digital wallets accounted for about 30% of global point-of-sale volume by 2024, cash fell to 46% of worldwide payments from 50% in 2023, and global payments revenue grew at an average of 7% annually from 2019 to 2024, according to McKinsey's global payments report. For us, the important point is simple: clients are increasingly comfortable with programmable payment rails.

Less manual work where it hurts most

Cash application is where many AR teams lose hours they never budgeted for.

A client pays three invoices in one transfer. Another pays one invoice short because of a dispute. A third pays from a parent entity name that doesn't match the billing record. In a manual environment, every one of those creates extra touchpoints. In a rule-based environment, many can be identified and routed automatically.

That changes how finance work gets staffed. The team spends less time posting receipts and more time managing exceptions, client communication, and root-cause fixes.

Consider the operational difference:

- Manual model Payments arrive, someone opens multiple systems, compares notes, posts entries, and follows up when data is incomplete.

- Automated model Payments enter a controlled flow, the system applies matching logic, routine items post automatically, and only exceptions require review.

Better forecasting and fewer surprises

Cash predictability improves when incoming payments are processed with the same logic every day. That doesn't eliminate late payers. It does eliminate a lot of preventable noise.

Professional services firms benefit here because labor, contractor payments, software subscriptions, and partner draws don't pause while AR catches up. The smoother the inflow, the more credible the forecast.

Operator's view: Clean reconciliation is a forecasting tool. If unapplied cash sits unresolved, your cash report is already less reliable than it looks.

A good automatic payment pool won't make every client pay early. It will make your cash process more consistent, your collections motion more disciplined, and your reporting more trustworthy. That's enough to move the bottom line in the right direction.

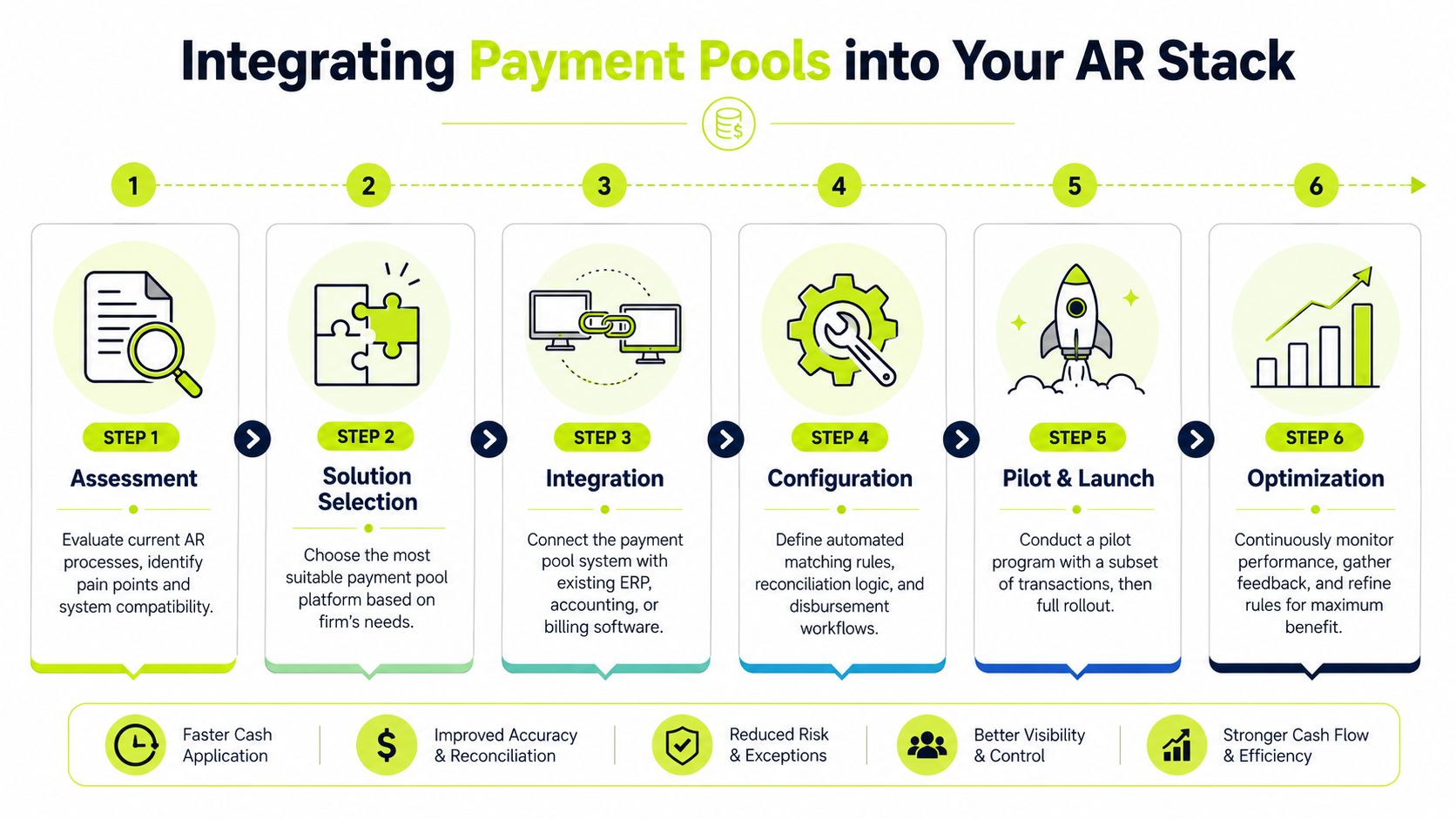

Integrating Payment Pools into Your AR Stack

Most firms don't need a rip-and-replace project. They need a control layer that connects the systems they already use.

That's good news for anyone running lean finance operations. Automatic payment pools work best as an orchestration layer between billing, payment processing, and accounting. Think of it as the logic engine that sits across your existing stack, not a total rebuild.

Start with the current flow

Before we pick software, we need a map of the current payment journey.

Where do invoices originate. Where do clients click to pay. Which payment methods are accepted. Where do remittance details land. Who posts cash. What happens when a payment doesn't match. If your team can't answer those questions in one meeting, your AR process already has too much hidden complexity.

A clean implementation starts with a short assessment:

- List every payment channel your clients use today, including ACH, card, wire, and any portal-based methods.

- Identify the source of invoice truth, whether that's QuickBooks, NetSuite, a PSA system, or billing software used by your operations team.

- Document exception patterns such as partial payments, client short pays, retainers, and parent-subsidiary remittances.

- Define approval boundaries so the system knows what it can auto-apply and what must be reviewed.

Connect the three systems that matter

Most AR software for professional services needs to align three layers.

The first is the billing and accounting layer. For many firms, that's QuickBooks or NetSuite. This layer contains invoice status, customer records, credit memos, and open balances. If you're exploring accounts receivable automation software, this system must stay clean.

The second is the payment layer. That may include Stripe, Adyen, bank transfer rails, or a payment portal tied to your invoice workflow. This layer captures the money and the transaction detail that helps identify it.

The third is the cash application and workflow layer. Automatic payment pool logic belongs in this layer. It receives invoice data, receives payment data, applies rules, and sends the result back to the accounting system.

What good implementation looks like

QuickBooks AR automation is a useful example because many small and midsize firms already have the accounting foundation in place. The mistake is expecting QuickBooks alone to solve workflow discipline. It won't. It records the result. It does not orchestrate the process around it.

A stronger setup usually includes:

- Invoice-triggered outreach tied to due dates and payment behavior

- Client-facing payment options that reduce friction at the point of collection

- Automated matching rules for common payer and invoice patterns

- Exception queues for anything the system shouldn't force through

- Posting controls that keep the ledger accurate

If implementation starts with software demos before process mapping, we're doing it backward.

Pilot first. Use one payment channel, a limited customer group, or one business unit. Watch where the exceptions cluster. Tighten the rules. Then expand. That sequence keeps the project practical and keeps finance in control.

Key Performance Indicators and Best Practices

Automatic payment pools only help if we manage them like an operating system, not a one-time software launch.

The finance team should own a short list of metrics that show whether the process is speeding collections, reducing manual work, and containing exceptions. If we can't see that clearly, then “automation” is just a label.

Best practices that prevent AR drift

Start with discipline, not sophistication.

- Standardize invoice data first. If client names, invoice numbers, and remittance instructions are inconsistent, matching logic will fail more often than it should.

- Keep payment options broad but controlled. ACH, card, wire, and digital wallets can all help, but each option needs clear routing and posting rules.

- Build explicit exception paths. Short pays, duplicate payments, unapplied cash, and disputed invoices should land in named queues with named owners.

- Automate reminders with judgment. Escalation timing should reflect account history, invoice age, and relationship sensitivity.

- Review rules monthly. Payment behavior changes. The logic should change with it.

For leaders focused on reduce DSO initiatives, there's a useful baseline in this guide to what DSO means and how finance teams use it. But DSO alone isn't enough. We need operating metrics underneath it.

The KPI table we should actually monitor

KPI | Definition | Industry Benchmark (Professional Services) |

|---|---|---|

Automated cash application rate | Share of incoming payments posted without manual intervention | Higher is better. Most firms should aim to increase this steadily over time |

Time to reconcile | Time from payment receipt to accurate posting in the ledger | Same day is the operational target |

Unapplied cash aging | How long unidentified or unmatched cash stays unresolved | Shorter is better. Exceptions shouldn't sit unattended |

Reminder completion rate | Share of scheduled reminders sent on time according to policy | Near-complete execution is the target |

Promise-to-pay conversion | Share of payment commitments that convert into actual receipts | Use trendline improvement by client segment |

Cost per payment processed | Internal effort required to collect, match, and post each payment | Lower is better, without increasing write-offs or disputes |

Dispute resolution cycle time | Time from dispute flag to invoice resolution and collection path reset | Short, visible, and owned by a named person |

Payment method mix | Distribution of receipts across ACH, card, wire, and wallet rails | Track by client segment and optimize for speed and cost |

Don't let the dashboard hide the real issues

Some firms watch top-level AR aging and think they have enough visibility. They don't.

If the automated cash application rate is low, the team is still doing clerical work at scale. If unapplied cash aging is creeping up, your cash report is less clean than it appears. If reminder completion is uneven, collections discipline is slipping even if overall DSO hasn't moved yet.

The best KPI set tells us where the process broke before month-end exposes it.

Run these metrics weekly. Review them with finance and operations together. In professional services, collections quality often depends on both.

Mitigating Risks and Ensuring Financial Compliance

This model is useful only if it improves control.

That means we should talk plainly about the risks. Not market risk in the crypto sense. Process risk, data risk, and compliance risk inside B2B receivables.

Where implementations usually go wrong

Most failures are self-inflicted.

The first is bad data mapping. Client records don't match across systems, invoice references are inconsistent, and payment descriptors are too messy to support clean rules. The second is overengineering. Teams try to automate every exception on day one and end up creating rules no one trusts. The third is weak ownership. Finance assumes IT owns the system, IT assumes accounting owns the exceptions, and no one governs the workflow.

The fix is boring and effective:

- Clean master data before launch

- Start with common payment scenarios

- Create approval thresholds for auto-posting

- Audit exception queues regularly

- Separate payment acceptance from posting authority

Compliance should be designed in, not added later

Corporate AR payment pools are not public DeFi pools. That distinction matters.

Public pool models come with undefined risk around regulation and impermanent loss. Corporate AR workflows operate inside established financial regulations, and trust-building financial guidance remains essential for users navigating financial products, as discussed by the New York Fed on serving underserved markets. In our world, that translates into controlled payment handling, clear internal policies, and auditable workflows.

At a minimum, finance leaders should expect attention to:

- PCI DSS considerations when card payments are involved

- SOC 2 expectations for platform security and vendor controls

- Role-based access for posting, refund, and write-off actions

- Audit trails for every rule, exception, and override

- Documented internal controls over cash application and account changes

If you work with law firms or legal-service clients, it also helps to understand the broader software environment they operate in. This roundup of top legal solutions for lawyers is a useful reference point for how technology decisions intersect with compliance-sensitive workflows.

For firms tightening governance, this checklist on accounts receivable internal controls is the right operational companion to any automation rollout.

Good AR automation doesn't reduce control. It moves control upstream, into rules, permissions, and visibility.

The right implementation gives us fewer surprises, faster closes, cleaner cash reporting, and a finance process we can defend in front of auditors, partners, and lenders.

Resolut helps professional services firms automate AR with the control finance leaders need. If you want a more consistent way to reduce manual follow-up, improve cash flow, and keep collections accurate without losing the human touch, Resolut is built for that.