B2B Online Payment Methods: A CFO's Guide to Control

Explore B2B online payment methods like ACH, cards, and wires. This guide helps CFOs and controllers reduce DSO, cut costs, and improve cash flow.

Month end usually exposes the problem.

A client mails a check because that's how they've always paid. Another sends an ACH with no invoice number in the remittance. A third pays by card through a portal, and your team has to sort out fees, match the net deposit, and clear the open invoice in QuickBooks. None of those payments are bad. The problem is that each one creates a different administrative path.

That's why a discussion about b2b online payment methods can't stop at “offer ACH” or “accept cards.” For a finance leader, the essential question is simpler and more operational. Which methods help you get paid faster without creating more reconciliation work, more exceptions, and more control gaps?

Beyond the Invoice The Growing Complexity of B2B Payments

For most professional services firms, payment complexity shows up long before anyone labels it a systems issue. It starts as small friction. A payment lands, but the backup is missing. An invoice is technically paid, but not applied. A partner asks for a cash forecast, and the AR aging looks clean on paper while unapplied cash sits in the bank.

That strain gets harder to manage as payment options expand. The global B2B payments market is projected to grow from $1,355.09 billion in 2024 to $2,943.11 billion by 2033, and real-time B2B payments recently grew 63% year over year, according to Straits Research's B2B payments market analysis. More rails should make collections easier. In practice, they often create more operational variance unless the finance stack is designed to absorb it.

Where finance teams lose control

The issue usually isn't acceptance. Most firms can technically take payment in several ways.

The issue is what happens after acceptance:

- Bank payments arrive without context: Treasury sees the deposit, but AR still has to determine which invoice or matter it belongs to.

- Card payments create convenience but not always clean accounting: Net settlements, fees, and processor timing can complicate cash application.

- Legacy methods linger: A client may prefer the old process even after you've introduced digital options.

Offer more ways to pay if you want. Just don't confuse more options with a better receivables process.

The operator's lens

A CFO shouldn't evaluate payment methods as isolated features. The better lens is control.

Ask four practical questions:

- Will this method help reduce DSO or just change how money arrives?

- How much staff time does it create after the payment is sent?

- How clearly can we reconcile it back to invoice, client, and general ledger?

- What approval and fraud risks does it introduce?

That's the shift. Payment choice is no longer a front-end client experience issue alone. It's part of an accounts receivable automation strategy that affects cash flow, staff load, and management visibility.

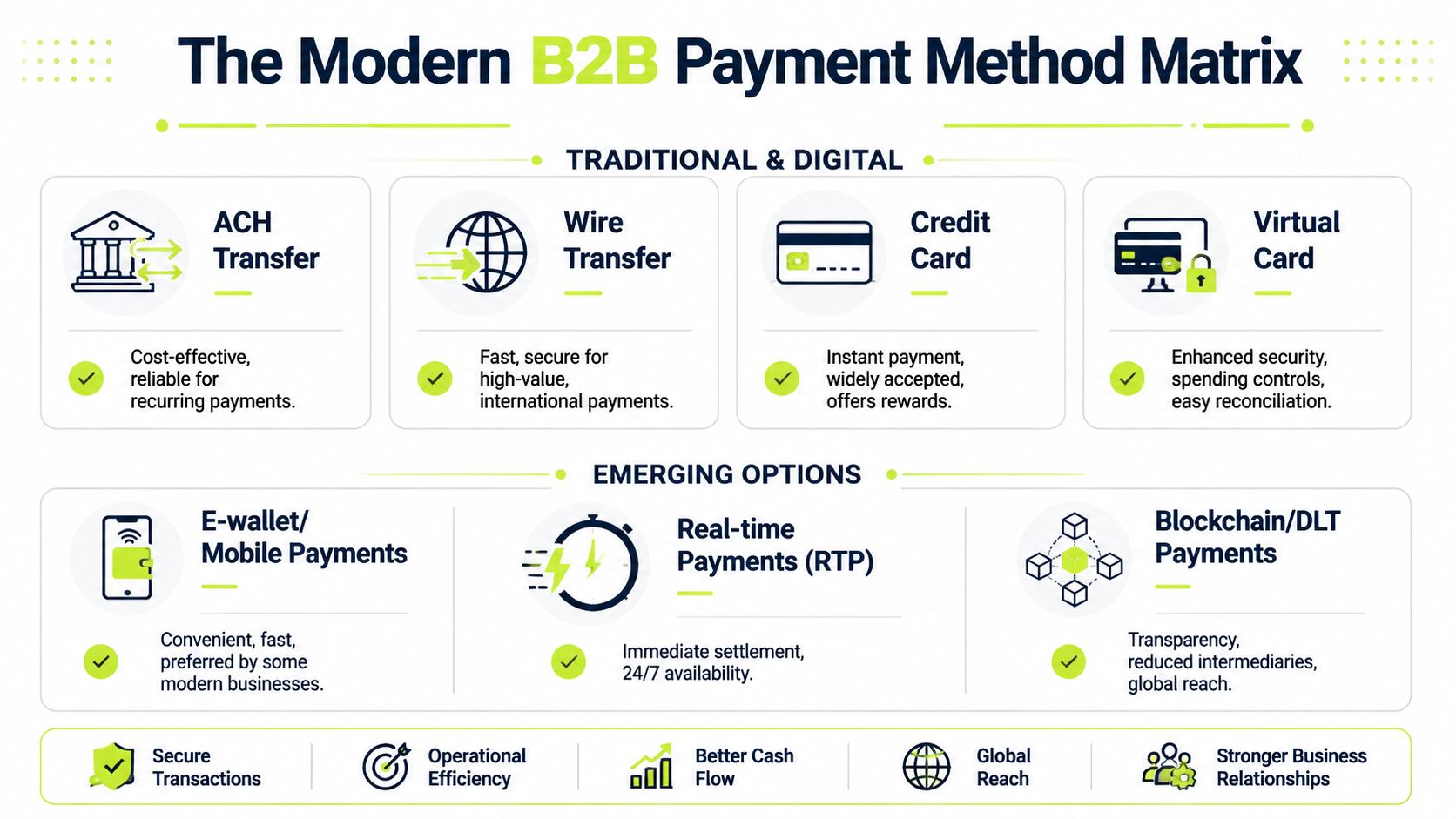

The Modern B2B Payment Method Matrix

Most firms don't need every payment rail. They need the right mix.

For a professional services business, the practical menu usually falls into three groups. Bank-to-bank transfers handle larger invoices and repeat billing. Card networks solve for convenience and urgency. Digital platforms sit on top and determine how cleanly the payment moves into your books.

The categories that matter

Bank transfers usually offer the strongest fit for invoice-based collections. ACH works well for domestic recurring payments. Wires fit high-value or time-sensitive transactions where certainty matters more than cost.

Card payments reduce payer friction. They're useful when you want a client to resolve a balance immediately, especially on smaller invoices, deposits, or one-off project work.

Digital options like hosted portals, e-invoicing flows, digital wallets, and emerging real-time rails shape the payment experience. They matter less as standalone methods than as part of a system that captures remittance details and closes the loop back to AR.

B2B Online Payment Method Comparison

Payment Method | Typical Cost | Settlement Speed | Reconciliation Effort | Best For |

|---|---|---|---|---|

ACH transfer | Lower than cards in most cases | Slower than cards or wires | Moderate, unless remittance is structured | Retainers, recurring invoices, larger domestic payments |

Wire transfer | Higher than ACH | Fast | Low to moderate if payment detail is clear | Large invoices, urgent payments, cross-border situations |

Credit card | Higher due to processing fees | Fast authorization and funding flow | Moderate because of fees and batch settlement handling | Smaller invoices, urgent catch-up payments, client convenience |

Virtual card | Similar card economics, with stronger controls | Fast | Lower than standard card use when controls are built in | Controlled supplier or client payment flows, tighter oversight |

Digital wallet | Convenience-led | Fast from the payer side | Varies by platform | Select clients that prefer modern checkout behavior |

Real-time payment options | Speed-focused | Immediate or near immediate where available | Depends on portal and accounting integration | Time-sensitive collections |

Check | Manual and operationally heavy | Slow | High | Legacy clients and exceptions only |

What works in practice

A common mistake is choosing one preferred rail and pushing every customer into it. That rarely holds.

A more durable model looks like this:

- Default to ACH for standard invoicing

- Keep wires available for large or urgent matters

- Use cards selectively where speed outweighs margin loss

- Put all of it behind one payment experience with accounting logic attached

If you're evaluating portal design and acceptance flow, this guide to payment gateways for business is useful because the gateway decision affects more than checkout. It affects reconciliation discipline and how much manual work your AR team inherits.

The best payment mix isn't the one with the most options. It's the one your team can operate cleanly.

Bank Transfers ACH and Wires Explained

If you invoice business clients regularly, bank transfers should sit at the center of your payment stack.

That isn't theory. In North America, ACH credits account for 37% of B2B transactions, and the average company processes 1,000 to 1,999 ACH credit transfers monthly, according to Zomentum's analysis of AFP payment data. For finance teams, that confirms what most controllers already see in practice. ACH is still the workhorse.

Where ACH fits best

ACH works when the relationship is established and the payment pattern is predictable.

Think monthly retainers, milestone billing, recurring managed services, and project invoices with standard terms. It's familiar to buyers, usually less expensive than card acceptance, and operationally stable when your invoicing process captures the right remittance details up front.

The weakness isn't the rail itself. It's the handoff. If the client sends an ACH without clear reference data, your team still has to identify and apply the cash.

A strong ACH process usually includes:

- Clear invoice references: Put invoice numbers and payer instructions directly in the billing communication.

- Standardized remittance collection: Train clients to reply to a dedicated payment inbox or use a portal that attaches payment context automatically.

- ERP or accounting sync: If you're running QuickBooks AR automation, the value comes from linking inbound payment data to the open invoice list without rekeying.

For a deeper primer on the mechanics, what ACH credit means in practice is worth reviewing with your finance team.

When a wire is the right answer

Wires solve a different problem.

Use them when the amount is large, the timing is sensitive, or the payment risk justifies tighter certainty. In professional services, that can mean a litigation retainer, a closing-related payment, or any invoice where waiting through standard bank timing creates unnecessary exposure.

The real trade-off

ACH is efficient at scale. Wires are decisive.

If a firm treats wires as routine, costs and client friction rise. If it forces ACH into every scenario, collections can slow where urgency matters. The right policy is usually simple: ACH by default, wire by exception, and a documented rule set so AR staff doesn't have to improvise under pressure.

Card Payments Virtual Cards and Digital Wallets

Cards do one thing very well. They remove excuses.

When a client receives an invoice and can pay immediately with a stored card or a simple portal flow, you eliminate bank setup delays, approval lag, and the vague “we'll process it this week” response. That's why many firms use cards to accelerate smaller balances, initial deposits, and overdue catch-up payments.

Convenience has a margin cost

The trade-off is direct and obvious. Card acceptance improves ease, but the fee comes off your economics immediately.

For a professional services firm with healthy gross margins, that may be acceptable on a small invoice or when the alternative is waiting. On a large project bill, it can be harder to justify. That's why many finance teams separate client convenience from default payment policy. They accept cards, but they don't steer large recurring invoices toward them.

If you're evaluating whether to pass some of that cost through, this breakdown of a convenience fee on credit card payments is a practical place to start.

Why virtual cards deserve a closer look

Virtual cards are more interesting from a control standpoint than a standard card-on-file setup.

They let teams define tighter parameters around amount, use, and timing. That makes them useful when you want card speed without the looseness that often comes with broad card credentials. In a B2B setting, that can improve auditability and reduce confusion around who approved what.

A card program only helps AR if the payment record is clean enough to post without detective work.

Security still belongs in the decision

Card acceptance isn't just a payments conversation. It's a data handling conversation.

If your firm stores, touches, or transmits card information directly, the process needs tighter discipline than many mid-market teams realize. For anyone reviewing processor setup, hosted fields, or portal design, this overview of securing customer card data is a useful operational reference.

Where digital wallets fit

Digital wallets can help at the edge. They're useful when clients expect a modern checkout experience, or when a mobile-friendly payment step reduces friction.

I wouldn't build a B2B collections strategy around wallets alone. For most professional services firms, they're an accessory layer. The core still comes back to bank rails, cards, and how the payment data flows into AR software for professional services.

The True Cost of Payment Acceptance

Most payment conversations get stuck on transaction fees. That's too narrow.

The larger cost often sits in the back office. A payment method that looks cheap on paper can be expensive once your team spends time chasing remittance, clearing unapplied cash, handling exceptions, and answering internal questions about what's been paid.

The hidden labor inside a “paid” invoice

A payment isn't done when the client sends it. It's done when your books reflect it accurately.

That gap matters. If your controller still has to match a deposit to an invoice from an email thread, review card settlements manually, or ask account managers which entity paid, then your process is carrying hidden cost. It also slows reporting. Cash may be in the bank, but the aging won't clear until someone finishes the work.

Common sources of drag include:

- Unstructured remittance: The money arrives, but invoice references don't.

- Multiple acceptance points: Payments come from bank transfer, processor dashboard, mailed checks, and ad hoc links.

- Accounting lag: The ledger update depends on manual intervention rather than rules-based posting.

- Exception handling: Credits, short pays, partial payments, and fee deductions get pushed into someone's inbox.

Fraud and control aren't separate issues

The same fragmented process that creates reconciliation work also weakens control.

B2B payments suffer from low authorization controls and high fraud vulnerability due to a historical focus on B2C security, and mismatches between buyer payment preferences and supplier acceptance methods complicate automation and add risk, as outlined in Seeed's analysis of unmet B2B payment needs. In practice, that means manual workarounds become control gaps. Staff starts accepting payment evidence by email, forwarding banking details, or making judgment calls outside the system.

A useful reset is to review payment acceptance as part of your internal control environment, not just as a treasury function.

This short video is a good prompt for that review:

What finance teams should measure

If you want to improve cash flow and reduce DSO, don't just ask what a payment method costs. Ask what the full workflow costs.

Track the items below over a quarter:

Operating question | Why it matters |

|---|---|

Time from payment receipt to invoice application | Shows whether cash posting is clean or delayed |

Number of unapplied cash items | Reveals remittance and matching problems |

Volume of payment-related inbox traffic | Signals how much work happens outside the system |

Frequency of exception handling | Exposes where process design is weak |

Approvals occurring outside policy | Points to fraud and audit risk |

The firms that tighten these basics usually see cleaner aging reports, faster collections follow-up, and less noise at month end. That's where AI AR automation starts to matter. Not as a buzzword, but as a way to route exceptions, match payments, and keep staff focused on the small set of items that need judgment.

Integrating a Smarter B2B Payment Strategy

By this point, the pattern is clear. The problem isn't whether ACH, wires, or cards exist. The problem is what happens when each one lives in its own silo.

That's especially common in firms between $3 million and $50 million in revenue. The accounting system is one place. The payment processor is somewhere else. Bank reporting lives in a portal. Collections activity happens in email. Then leadership asks for a clean view of receivables and cash timing, and finance has to assemble it manually.

A better operating model

The more durable approach is a blended payment strategy with one orchestration layer behind it.

Use different methods for different situations, but force the data into one governed workflow. That means your payment portal, invoice records, collections activity, and accounting system should all point back to the same receivable.

A practical model for professional services usually looks like this:

- ACH as the default for standard invoices because it fits recurring and higher-value billing.

- Card acceptance for convenience-driven use cases such as deposits, smaller invoices, or fast resolution of past due balances.

- Wire instructions reserved for urgency or large transfers where timing certainty matters.

- A single payment experience for the client so your team isn't managing separate reconciliation paths.

Why integration changes the economics

Sixty-four percent of companies use electronic methods for over half of B2B payments, yet lack of integration between payment gateways and AR systems still creates fragmented workflows. That gap contributes to $200B wasted annually on AR administration, according to Digital Commerce 360's reporting on digital payment adoption and AR friction.

That's the part many firms underestimate. Digital acceptance alone doesn't solve the back office problem. Integration does.

If your team still exports data from one system and re-enters it into another, you haven't modernized AR. You've just digitized one step.

What to look for in the stack

For firms using QuickBooks, the standard is straightforward. Your payment workflow should support invoice-level matching, status updates, and clear exception handling without requiring spreadsheet cleanup at close.

When assessing AR software for professional services, look for these operational traits:

- Invoice-linked payment options: Clients should pay against a specific open item, not a generic account.

- Automatic cash application: The system should match and post routine receipts with minimal intervention.

- Collections visibility: Promises to pay, disputes, and follow-ups should sit near the receivable record.

- Accounting sync: QuickBooks AR automation should reduce duplicate entry, not create another admin console.

- Role-based controls: Staff should work within approvals and audit trails.

If your client base is becoming more international, payment mix gets more nuanced. This guide on how to expand internationally is helpful for thinking through cross-border payment considerations before you add more complexity than your current AR process can handle.

One practical option in this category is Resolut, which combines payment portal functionality, automated cash application, collections workflows, and accounting connectivity in one AR process. That matters less as a product feature list and more as an operating principle. One payment stack should create one source of truth.

From Payments to Orchestration The Final Layer

Most firms don't need another disconnected payment option. They need a system that coordinates the options they already have.

That final layer is orchestration. In AR, orchestration means the software and process discipline that connect invoice delivery, customer outreach, payment acceptance, cash application, exception handling, and escalation into one controlled flow. The payment method still matters. But it matters as an input into a larger process, not as the process itself.

What orchestration changes day to day

For a controller, it means fewer unapplied receipts and fewer end-of-month surprises.

For a CFO, it means more confidence in cash forecasting, cleaner aging, and less dependence on tribal knowledge inside the AR team. For firm owners, it means clients still get flexibility, but the finance function keeps control.

A real orchestration layer should handle work such as:

- Route the client to the right payment option based on invoice size, urgency, or policy

- Attach remittance and invoice context automatically so payments post cleanly

- Trigger follow-up workflows when invoices age or promises break

- Surface exceptions early instead of letting them sit in inboxes

- Support human review where judgment matters and automate the routine items

Keep the strategy practical

Not every firm needs cutting-edge rails. Some do. If you're tracking where payment infrastructure may go next, especially in cross-border or programmable finance environments, it can help to watch builders in adjacent spaces such as a web3 fintech development company. The immediate lesson for most finance teams isn't to adopt every new rail. It's to build an AR system flexible enough to absorb change without adding chaos.

Better b2b online payment methods help. Better orchestration is what turns them into reliable cash flow.

That's the shift worth making. Accept the payment methods your clients need. Standardize the controls your finance team needs. Then connect both inside a process that supports accounts receivable automation, clearer reporting, and calmer closes.

If your firm wants that kind of control, Resolut automates AR for professional services with a focus on consistency, accuracy, and human oversight.