Convenience Fee on Credit Card: Master 2026 Compliance

Master the convenience fee on credit card. This guide for CFOs covers rules, compliance, & AR automation to boost cash flow without alienating clients.

Card processing costs now show up as a recurring margin decision, not a minor admin expense. For a professional services firm, that means payment design belongs with AR policy, client experience, and cash management, not buried in merchant statements.

A convenience fee on credit card payments can be useful in a narrow set of cases. It is not a cure for weak billing operations. Used carelessly, it creates compliance exposure, client pushback, and reconciliation problems that cost more than the fee recovers.

The better question is operational. Which payment choices get cash in faster, protect client trust, and stand up in an audit?

That standard matters more in firms that bill retainers, milestones, monthly service fees, or past-due balances. A card option may speed up collection, but every faster payment has a cost attached. Finance leaders need to decide whether to absorb that cost, pass part of it through under the right rules, or shift clients toward lower-cost methods without adding friction to the collections process.

The strongest teams do not overbuild around fees. They use fees as a tactical tool while fixing the bigger issue: an AR process that still depends on manual follow-up, inconsistent payment terms, and limited payment routing. Once the workflow is tight, fee revenue matters less because collections improve upstream. If your team needs a technical refresher on the payment stack behind that workflow, this overview of what is payment gateway is a useful starting point.

The True Cost of Accepting Client Payments

For many professional services firms, every card payment trades speed for margin.

That trade-off deserves more attention than it usually gets. Merchant fees reduce net collections on invoices that often fund payroll, partner draws, software commitments, and tax reserves. On a large retainer or milestone bill, the cost is no longer a rounding error. It becomes an AR policy decision.

Convenience fees came out of a narrow use case. The point was to recover the cost of offering a separate payment channel, not to create a general markup on any client who pays by card. Finance teams lose control when they treat every processing expense as something that can be pushed back to the client.

Professional services firms feel this more sharply than many product businesses. Invoices are larger. Payment timing affects liquidity planning. Client relationships are longer and more sensitive to billing friction. A fee that looks minor in the portal can still create pushback, delay approval, or trigger write-off requests from a key account.

The practical question is not whether card acceptance costs money. It does. The question is whether the payment setup improves cash conversion enough to justify that cost, and whether any fee applied to offset it will hold up operationally.

That puts the focus on control.

A finance leader should be able to answer four points without ambiguity:

- What is the cost by payment type? Card, ACH, wire, and wallet payments carry different fee profiles, settlement timing, and reconciliation effort.

- Which clients pay faster when cards are available? Faster payment can justify higher acceptance cost if it reduces follow-up work and shortens collection cycles.

- How will the fee appear in the client experience and the ledger? If disclosure, invoice presentation, and accounting treatment are inconsistent, the policy will create cleanup work.

- Does the current stack support clean execution? Gateway logic, processor settings, and ERP mapping all affect whether fee rules can be applied consistently. If your team needs a technical refresher, this explanation of what is payment gateway is a useful baseline.

In practice, convenience fees work best as a tactical option inside a broader AR strategy. Firms that rely on them too heavily usually have a deeper issue, manual collections, weak payment routing, or too few low-cost digital options. The stronger long-term move is to tighten invoicing, simplify approvals, and make lower-cost payment methods easy enough that the fee matters less over time.

A useful standard is simple. If the fee logic cannot be explained clearly to a client, configured cleanly in the payment flow, and reconciled cleanly at month-end, it is not ready for production.

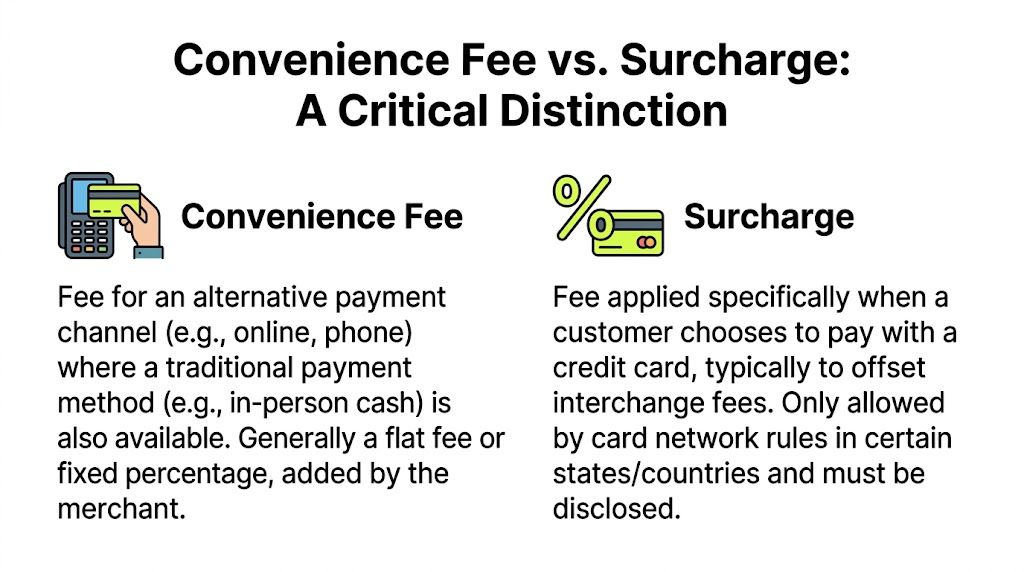

Convenience Fee vs Surcharge A Critical Distinction

Many finance teams use these terms interchangeably. That’s where trouble starts.

A convenience fee and a surcharge are different tools. They serve different purposes, trigger different rules, and create different client reactions. If your firm operates across multiple states or serves clients with varied payment habits, this distinction isn’t academic. It affects compliance, invoice language, and system setup.

Think of them as two different charges

A convenience fee is like a flat shipping charge for choosing a different delivery method. The charge is tied to the channel.

A surcharge is closer to a fuel surcharge. It’s tied to the payment method itself, usually as a percentage.

That difference seems small until you try to implement one inside a payment portal.

Side-by-side comparison

Feature | Convenience fee | Surcharge |

|---|---|---|

What triggers it | Use of an alternative payment channel | Use of a credit card |

Typical structure | Flat-rate charge | Percentage-based fee |

Legal status | Legal in all 50 states | Banned in some states |

Key cap | Rule-driven by network/channel requirements | Capped at 4% |

Primary risk | Misapplying channel logic | Violating state and network surcharge rules |

The clearest summary comes from Optimized Payments, which notes that convenience fees are flat-rate charges for using an alternative payment channel and are legal in all 50 states, whereas surcharges are percentage-based, capped at 4%, banned in states like Connecticut and Massachusetts, and come with stricter network disclosure rules.

Where firms get this wrong

The most common failure pattern looks like this:

- A firm wants to recover card cost.

- The processor offers “fee recovery.”

- The firm enables it.

- Nobody checks whether the fee is being applied as a convenience fee or a surcharge.

- Invoice language stays vague.

- Payment pages don’t clearly explain the client’s alternatives.

That setup may collect money in the short term, but it creates exposure.

A legitimate convenience fee on credit card payments depends on the existence of a valid alternative channel or method. A surcharge, by contrast, directly passes card cost through under a different legal framework. If your firm treats one as the other, the problem isn’t just terminology. The problem is that your client-facing process, card-brand compliance, and ledger treatment may all be wrong at once.

How to choose the right approach

For most professional services firms, the decision comes down to operating model.

A convenience fee fits better when:

- You want to preserve a fee-free payment path such as ACH.

- You’re charging for a non-standard or premium payment route.

- You need a cleaner, fixed-dollar approach rather than a percentage.

A surcharge fits better when:

- You’re explicitly recouping credit card processing cost.

- Your legal footprint allows it.

- Your systems can apply it correctly by payment type and jurisdiction.

A fee tied to convenience is easier to defend with clients than a fee that feels like punishment for using a card.

Why language matters

Clients don’t parse card-network terminology, but they do react to tone.

“Credit card processing fee” often sounds like the firm is passing along internal overhead. “Convenience fee” can work better only if the optionality is real. If there is no meaningful lower-cost alternative, the wording won’t rescue the experience.

That’s why finance and operations need to align before rollout. The legal label, the payment architecture, and the client message must match. If they don’t, your team will spend more time explaining fees than collecting invoices.

Navigating a Maze of Compliance and Card Network Rules

Payment rules break in the handoff between policy and system setup.

A convenience fee can look defensible in a policy memo and still fail at the point of payment, in the processor configuration, or in the way accounting records it. That is where finance teams get exposed. The issue is rarely intent. The issue is execution across card rules, disclosure requirements, jurisdictional limits, and ledger treatment.

What the card brands require

The practical rule set is fragmented. As Experian explains, Visa generally expects a flat fee tied to a non-standard payment channel, Mastercard limits convenience fees to certain merchant categories, American Express may permit percentage-based fees with separate authorization requirements, and Discover expects consistent treatment across payment methods within the same channel.

For finance leaders, those differences matter because fee policy is really a systems design question. If your payment stack cannot apply the right fee logic by brand, channel, and transaction type, you do not have a controlled program. You have a manual exception process waiting to happen.

Card brand | Practical implication for finance teams |

|---|---|

Visa | Fee structure is usually flat and tied to an alternative payment channel |

Mastercard | Eligibility is narrower, so not every business model fits |

American Express | Workflow may need distinct authorization handling for the fee |

Discover | Fee treatment has to stay consistent within the payment channel |

This is one reason gateway selection matters more than teams expect. A processor that can accept cards is not automatically a processor that can support compliant fee logic. When evaluating payment gateways for business, finance should ask how the system handles brand-specific rules, pre-payment disclosure, recurring billing restrictions, and separate fee posting to the GL.

The audit checklist that actually matters

I treat convenience fees the same way I treat sales tax setup or revenue recognition controls. They need documented ownership, repeatable testing, and evidence that the live workflow matches the written policy.

Use a checklist that focuses on failure points:

- Confirm the use case The fee should be tied to an allowable payment channel or optional method, not a broad effort to recover processing cost.

- Validate network-level configuration Processor and gateway settings need to match the card-brand rules that apply to your payment flow.

- Review recurring and stored-payment scenarios Retainers, installment plans, and autopay often create a separate compliance question. Test them separately.

- Test disclosure timing Clients should see the fee before authorization, with a clear opportunity to choose another payment route where required.

- Inspect posting logic Fee amounts should remain identifiable in the transaction record and map correctly into the accounting system.

- Check jurisdiction logic Multi-state firms need to verify that fee treatment changes when legal or network requirements differ by location or payment type.

Control point: If staff have to fix fee treatment by hand, the setup is not under control.

The state-level trap

The biggest practical mistake is assuming a national answer is enough.

State law can permit convenience fees in principle while still imposing narrower limits in practice. Those limits may affect debit card treatment, fee caps, disclosure language, or the conditions under which a fee can be charged. A firm with clients across multiple jurisdictions cannot rely on a generic summary and call the issue closed.

That is why over-reliance on fees is a strategic error. Every added rule increases configuration risk, exception handling, and client confusion. If a firm is using convenience fees as a primary AR strategy, the compliance burden rises faster than the cash benefit.

A safer operating view looks like this:

- State law may allow the fee concept

- Card-network rules still shape how the fee can be applied

- Processor capabilities determine whether the policy can be executed correctly

- Client location, payment type, and billing workflow can all change the answer

What works in practice

The firms that handle this well use a defined control structure.

Legal or outside counsel reviews the policy. Finance sets the operating rules and approves the economics. Operations translates those rules into the payment experience. Accounting verifies posting, refunds, and reconciliation. Someone owns periodic testing.

The firms that struggle usually delegate too much to the merchant processor. Processors can enable features. They do not own your disclosure language, your state-level exposure, your audit trail, or your GL accuracy.

That distinction matters. A convenience fee should be a tactical tool with tight guardrails, not a substitute for fixing AR friction at the source. The better long-term model is to reduce dependence on card fees by making lower-cost payment methods easy, fast, and visible enough that clients choose them without prompting.

Visual ideas for internal rollout

If you need approval from partners, legal, or operations, use materials that show how the policy will work in real transactions:

- A card-rule matrix with fee structure, disclosure requirements, and recurring-payment constraints by brand

- A payment-flow map showing invoice, payment page, fee presentation, authorization, posting, and refund handling

- A jurisdiction review sheet for the states where your clients are billed

- A control-owner chart that assigns testing, monitoring, and exception review

A convenience fee program can be run cleanly. It just takes more control than many firms expect.

Implementing Fees with Operational Precision

The policy decision is only half the work. The critical test is whether your accounting team, payment system, and client communications stay aligned after launch.

When they don’t, the result is familiar. Cash posts slowly, staff issue credits manually, clients ask why the amount changed, and the general ledger ends up with a bucket of unexplained payment adjustments.

Set up the accounting cleanly

A convenience fee should never disappear into gross service revenue.

It needs its own treatment in the transaction flow and, in most firms, its own reporting line so finance can see how often it’s used, how much cost it offsets, and whether it’s influencing payment behavior in the right direction.

A practical ledger setup usually includes:

- Separate fee mapping: Post the fee distinctly from earned service revenue.

- Clear invoice detail: Show the underlying invoice amount and the fee as separate transaction elements when the payment experience allows.

- Refund logic: Make sure any reversal process addresses the fee treatment consistently.

- QuickBooks discipline: If you’re using QuickBooks AR automation or adjacent tools, confirm the payment sync doesn’t collapse fee data into a generic payment adjustment.

Keep the payment page plain and direct

Language matters more than teams expect.

A fee that appears late in the payment flow feels deceptive even if it’s technically disclosed. A fee that appears early, with a clear no-fee alternative, is easier for clients to accept. That’s especially important because a 2024 J.D. Power survey found that merchants adding surcharges saw a 24-point drop in customer satisfaction, as reported by The Financial Brand.

That’s surcharge data, not a universal judgment on every fee type. Still, the lesson carries over. Surprises damage trust.

What to say to clients

Use simple language. Don’t hide behind processor jargon.

Good portal copy sounds like this:

Pay by bank transfer at no additional cost, or choose card for a faster digital checkout. A convenience fee applies to card payments where permitted.

That framing does three things well. It preserves choice, explains the fee, and points clients toward the lower-cost path without pressure.

Poor wording usually has one of these flaws:

- It sounds punitive.

- It appears only at checkout.

- It implies the fee is mandatory for everyone.

- It uses vague labels like “admin fee” or “processing charge” with no context.

Train the front line, not just finance

Partners, account managers, billing coordinators, and collections staff all need the same script.

If one person says “that’s just what the processor charges us” and another says “it’s required for card payments,” the firm loses credibility. A short internal FAQ is usually enough.

Include:

Scenario | Recommended response |

|---|---|

Client asks how to avoid the fee | Direct them to the fee-free payment option |

Client disputes the fee | Confirm whether the payment method and channel qualified under your policy |

Partner wants to waive it | Define who has approval authority and how waivers are recorded |

Client sends partial payment | Clarify how the payment is applied and whether any balance remains |

If your team is reevaluating payment infrastructure as part of this work, this guide to business payment gateways is a practical reference: https://www.resolutai.com/blog/payment-gateways-for-business

Implementation works when policy, technology, and client communication all say the same thing.

Quantifying the Impact on DSO and Cash Flow

A few days shaved off DSO can matter more to cash flow than recovering a small slice of card processing cost. That is why convenience fees deserve a working-capital lens, not just an expense-recovery lens.

The core question is simple. Does the fee structure change client behavior in a way that improves net cash performance after you account for payment timing, payment mix, exceptions, and staff time?

Measure the full economics, not just fee recovery

Controllers often start with the obvious metric: how much card cost did we offset?

That metric is too narrow. A better review looks at the operating result across the invoice-to-cash cycle:

- Payment mix shift. Did more clients move from card to ACH or bank transfer?

- Collection timing. Did invoices get paid faster, slower, or with no meaningful change?

- Exception volume. Did disputes, reversals, or fee questions increase?

- Staff effort. Did AR spend less time following up, explaining charges, or correcting postings?

- Cash application speed. Did payments post cleanly into the ledger, or did exceptions delay close?

Teams that want a clearer benchmark for this analysis should use a DSO framework for finance teams that ties payment design back to working capital.

The trade-off is operational, not theoretical

A convenience fee can improve margin on one set of payments and reduce card usage on another. That can be a good outcome if the lower-cost option is easy to use and still gets the invoice paid on time.

In practice, the best result is usually not higher card volume. It is a cleaner split in behavior. Clients who value speed or points still use card. Clients who are indifferent choose ACH. Finance gets lower processing expense and a more predictable payment pattern.

That predictability matters. A payment method mix you can forecast is easier to staff, easier to reconcile, and easier to model in weekly cash reporting.

Cash flow improves only if friction stays low

The fee model breaks down when it creates support work. A program that recovers processing cost but also creates more client questions, more manual reviews, and more exceptions can weaken cash performance overall.

I have seen this happen in firms with fragmented billing workflows. The posted fee is technically correct, but the client does not understand it, the payment posts to the wrong balance, or the team has to reverse and reapply cash manually. The processor economics look better on paper. The AR operation gets slower.

That is why the measurement model should include four layers, not one:

Layer | What finance should review |

|---|---|

Collection speed | How quickly can the client move from invoice receipt to completed payment? |

Payment cost | Which payment methods preserve margin after processing expense? |

Exception handling | How many disputes, reversals, fee questions, and manual interventions does the setup create? |

Ledger completion | How fast does the payment reconcile and close the invoice in the accounting system? |

Payment choice matters more than the fee itself

The firms that get the best result usually make the lower-cost rail obvious and easy, then leave card available as an option. If you need a broader comparison of client-facing rails, this guide to methods of electronic payment is a useful reference.

That approach improves behavior without turning every collection conversation into a pricing dispute.

It also supports the larger strategic point. Convenience fees are a tactical tool. They can shape payment behavior and recover part of the cost to accept cards, but they do not fix weak invoicing, inconsistent follow-up, or slow cash application. Firms that rely too heavily on fees usually end up treating a system problem as a pricing problem.

The stronger result comes from building an AR process that collects quickly with less intervention. When that system is in place, convenience fees become occasional and deliberate, not a core dependency.

The Strategic Alternative to Convenience Fees

The best long-term answer to rising payment cost isn’t to get better at charging fees. It’s to build an AR process that needs them less often.

That sounds counterintuitive until you look at where the primary cost sits. Processor expense matters, but so do late invoices, manual follow-up, fragmented payment options, delayed cash application, and partner time spent nudging clients to pay.

A convenience fee can offset one slice of that problem. It doesn’t solve the system.

Why over-relying on fees is a strategic error

Fees are reactive. They respond to cost after the invoice is already out, the payment method is already chosen, and the client is already in the payment flow.

A better system works earlier.

It shapes behavior before collection becomes awkward. It sends invoices promptly. It follows up consistently. It gives the client a clean self-service portal. It presents multiple digital options, including low-cost rails. If you want a broader overview of client-facing options, this summary of methods of electronic payment is a helpful comparison.

When firms improve those pieces, they often find that the need for a convenience fee on credit card transactions becomes narrower and more deliberate.

What a stronger AR system looks like

For professional services firms, the strongest design usually includes these elements:

- Fee-free ACH path: Make the lowest-cost option the easiest default.

- Card as an optional accelerator: Keep cards available for clients who value speed or simplicity.

- Automated reminders: Use accounts receivable automation so the payment request arrives before the relationship gets strained.

- Fast reconciliation: Cash should post without a team member chasing remittance details.

- Consistent policy enforcement: If a fee applies, the system handles it. Staff shouldn’t improvise.

The operational advantage

It is AR software for professional services that changes the conversation.

Instead of asking clients to absorb your processing cost, you redesign the payment journey so more clients pay faster through lower-cost methods. That’s a healthier outcome for both sides. The client keeps optionality. Finance gains predictability. Collections become less personal and more systematic.

A practical example is ACH. It often becomes far more attractive when the client can authorize payment through a modern portal instead of emailing forms or calling accounting. If your team is reviewing ACH cost structure as part of that redesign, this resource is worth bookmarking: https://www.resolutai.com/blog/ach-payment-processing-fees

What works and what doesn’t

What works

- Clear payment choices at invoice presentment

- Early, polite follow-up

- One portal for cards and bank transfer

- Policy-driven fee logic

- Fast posting back to the accounting system

What doesn’t

- Hiding the fee until checkout

- Offering cards but making ACH cumbersome

- Letting staff decide fee exceptions ad hoc

- Treating fee recovery as the main AR strategy

- Running payment collection separately from cash application

The firms with the best cash control don't depend on fees to protect margin. They remove friction so clients pay sooner through the right channel.

A better target for finance

The target isn’t “recover every penny of merchant expense.”

The target is a collection process that is predictable, low-friction, compliant, and scalable. Once you build that, fees become a selective tool. You use them where they fit, not as a blanket answer to weak process design.

That’s the more durable path to reduce DSO, improve cash flow, and give your team fewer exceptions to manage.

Achieving Total Control Over Your AR

Convenience fees sit at the intersection of margin, compliance, and client experience. That’s why they deserve more attention than a processor toggle and less faith than a silver bullet.

Used carefully, a convenience fee can support control. Used casually, it creates avoidable friction and messy exceptions. The difference comes down to discipline. Know whether you’re applying a convenience fee or a surcharge. Configure the payment flow to match the rule set. Keep disclosure plain. Record the fee cleanly. Measure whether the setup improves cash flow or just shifts cost around.

For most professional services firms, the larger opportunity is broader than fee recovery. It’s building an AR motion that combines accounts receivable automation, stronger payment options, cleaner posting, and fewer manual follow-ups. That’s how finance teams create lasting control.

Resolut automates AR for professional services with a practical focus on consistency, accuracy, and a human client experience. If your team wants to reduce DSO, improve cash flow, and bring billing, collections, payment options, and cash application into one operating rhythm, take a look at Resolut.