Modern B2B Payment Platform: Boost Cash Flow & Cut DSO

Discover how a modern B2B payment platform reduces DSO & improves cash flow. A guide for CFOs on evaluation, KPIs, & AR automation.

Monday starts with the aging report. A partner asks why a long-standing client hasn't paid. Someone on the finance team says the invoice was sent, the client says they never saw it, and the bank deposit that came in last week still hasn't been matched cleanly in QuickBooks. Nothing is broken enough to trigger a crisis. But the process keeps leaking time, confidence, and cash.

That's the reality in many professional services firms. Revenue is booked. Work is delivered. Yet collections still depend on spreadsheets, inbox searches, memory, and whoever feels comfortable sending the follow-up email. The result isn't just slower payment. It's less control over cash flow, weaker forecasting, and too much partner attention spent on issues that should be routine.

A modern B2B payment platform should fix that. Not by acting like a prettier checkout page, but by becoming part of the operating system for receivables. For firms trying to reduce DSO, improve cash flow, and tighten execution without adding friction to client relationships, that distinction matters.

Moving Beyond Payments The Real Job of a B2B Platform

In a services firm, collections friction rarely shows up as one dramatic failure. It shows up in quiet waste.

An invoice goes out late because billing needed one more approval. A client wants to pay by ACH, but the invoice only makes card payment obvious. A payment lands, but the remittance is incomplete, so someone has to guess which matter or engagement it belongs to. A reminder doesn't get sent because the account manager worries about tone.

Those are AR problems, but they're also control problems.

The old view of a B2B payment platform was simple. Accept payment digitally, shorten the trip from invoice to bank account, move on. That's too narrow now. As payment infrastructure has become more embedded in finance operations, the practical question has changed from “can this system collect money?” to “can this system help us run receivables with fewer surprises?”

That broader shift is part of a larger movement in financial infrastructure. Visbanking's insights on BaaP are useful here because they frame platforms as embedded financial layers, not isolated tools. Finance leaders should think about AR the same way. The strongest systems don't sit off to the side. They connect payment activity, workflow, and visibility inside the firm's daily operating process.

For a smaller firm, that might start with invoice delivery, reminders, and cleaner payment capture. For a larger professional services practice, it often means tighter sync between billing, collections, cash application, and reporting. The platform becomes less about acceptance and more about orchestration.

The firms that collect predictably usually haven't found magic clients. They've built a process clients can move through without confusion.

If you're still comparing vendors mainly on gateway features, it's worth stepping back and looking at how payment gateways for business fit inside the full invoice-to-cash workflow. Payment capture matters. But if acceptance improves while reconciliation, outreach, and forecasting stay manual, finance still carries the burden.

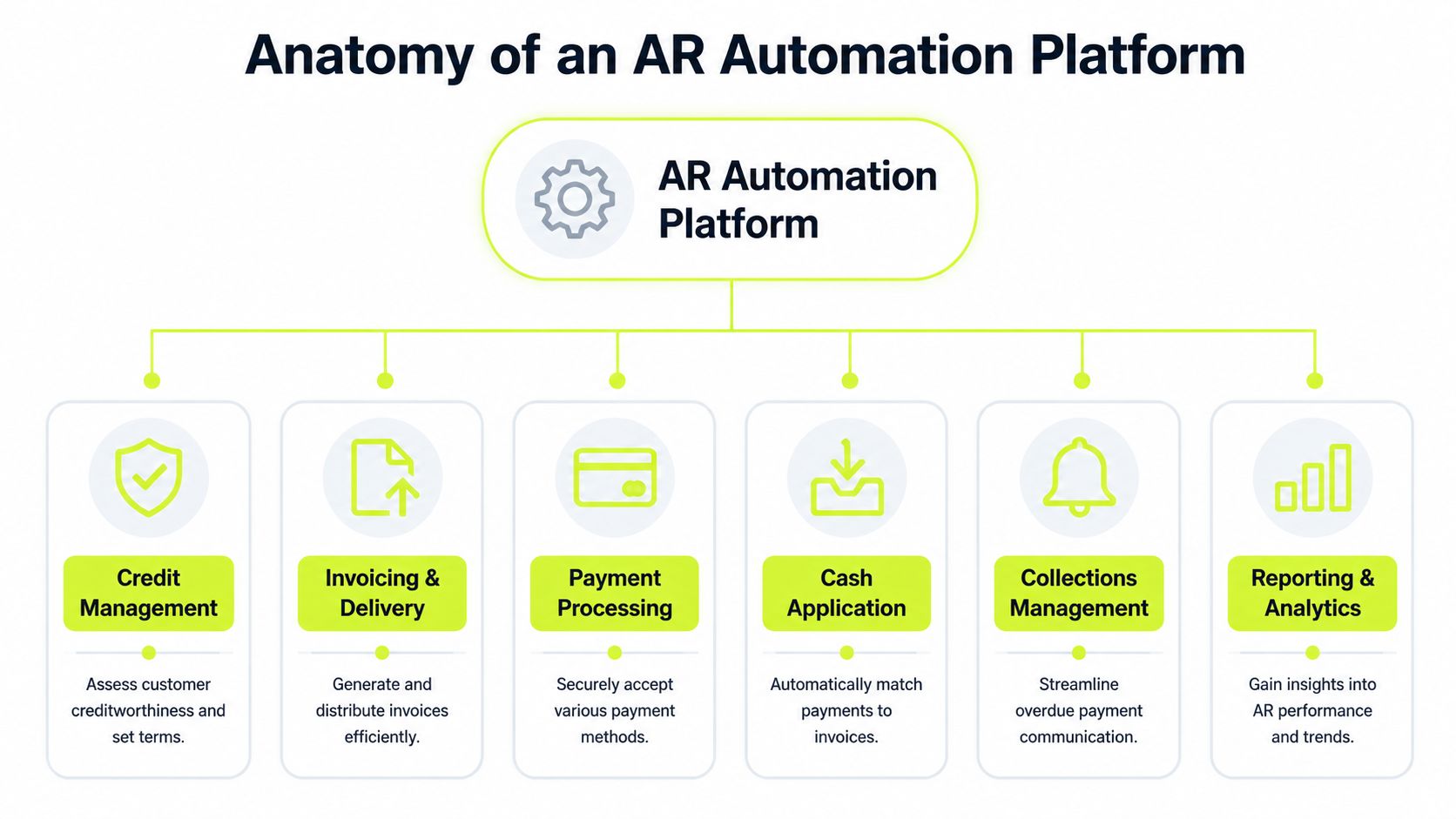

The Anatomy of an Accounts Receivable Automation Platform

A good AR stack doesn't behave like a pile of disconnected features. It behaves like a controlled sequence.

Invoice creation triggers delivery. Delivery drives payment action. Payment data flows into matching logic. Matching updates the ledger. The ledger updates the collections queue. Management gets a current view of exposure instead of a retrospective explanation.

That's what CFOs should expect from accounts receivable automation.

Core components that actually matter

At the front end, the platform should handle invoicing and delivery reliably. That includes generating invoices from the source system, sending them through consistent channels, and keeping a record of what was delivered and when. In professional services, this matters because billing often involves multiple approvers, adjusted time entries, and client-specific formats. If invoice delivery is inconsistent, every downstream metric gets noisier.

Then comes payment processing, though many evaluations stop too early at this point. A technically comprehensive B2B payment platform should support multiple rails in one portal, including ACH, wire, card, virtual card, and eChecks. For enterprise or global use, guidance from HighRadius on robust B2B payment platform requirements points to multi-currency processing with 150+ currencies, 100+ payment methods, and routing across 40+ card processors. The practical reason is straightforward. More rail coverage improves payment acceptance, while routing flexibility helps finance teams manage fees, authorization performance, and customer preferences.

That doesn't mean every professional services firm needs global complexity. It means even smaller firms should avoid platforms that force every client into one payment behavior.

Where the real leverage sits

The middle of the process is where the strongest systems separate themselves.

Cash application should match incoming payments to the right invoice with minimal manual review. If your team still opens bank reports, payment notices, and accounting records side by side to determine what got paid, the platform isn't doing enough.

Reconciliation and ERP sync should happen in a way that reduces lag between payment activity and financial visibility. That includes posting status updates back into accounting, keeping open balances current, and making exceptions visible quickly.

Practical rule: If a payment is received but your team still has to “figure out what happened,” you don't have automation. You have digital intake.

The control layer above the transaction layer

The best AR software for professional services adds orchestration on top of processing.

That includes:

- Credit management: Setting terms and evaluating client risk before balances age into a collections problem.

- Collections workflows: Triggering reminders based on invoice status, amount, client behavior, or aging band.

- Omnichannel outreach: Coordinating email, SMS, and call tasks so communication stays consistent without sounding robotic.

- Reporting and analytics: Showing which invoices are at risk, where payment friction appears, and how the queue is moving.

In a law firm, advisory firm, or agency, this matters for relationship reasons as much as efficiency. Collections can't feel random or aggressive. The outreach has to reflect the client relationship while still protecting the firm's position. A good platform helps finance maintain that balance with process, not improvisation.

If you're evaluating AI AR automation, this is the point to test. Ask whether the system only automates tasks, or whether it can prioritize work, escalate intelligently, and adapt to actual payment behavior. Rule-based automation can help. But orchestration is what turns AR from clerical work into managed financial control.

Translating Platform Features into Balance Sheet Improvements

Finance teams don't buy software because the portal looks cleaner. They buy it because receivables need to convert into cash with less delay, less labor, and fewer exceptions.

That's why the value of a B2B payment platform should be judged in balance sheet terms first.

Cash moves differently in B2B

B2B collections are operationally heavy because the payment amounts are larger and the workflows around them are more controlled. Paddle's overview of B2B payment complexity cites the average B2B ACH debit transaction at $41,118, compared with $44 for consumers. That gap explains why enterprise-grade payment systems emphasize approvals, reconciliation, and auditability instead of simple checkout design.

In a professional services firm, one delayed payment can affect payroll timing, partner distributions, hiring plans, or tax reserves. The issue isn't transaction volume alone. It's the weight each receivable carries.

What changes on the balance sheet

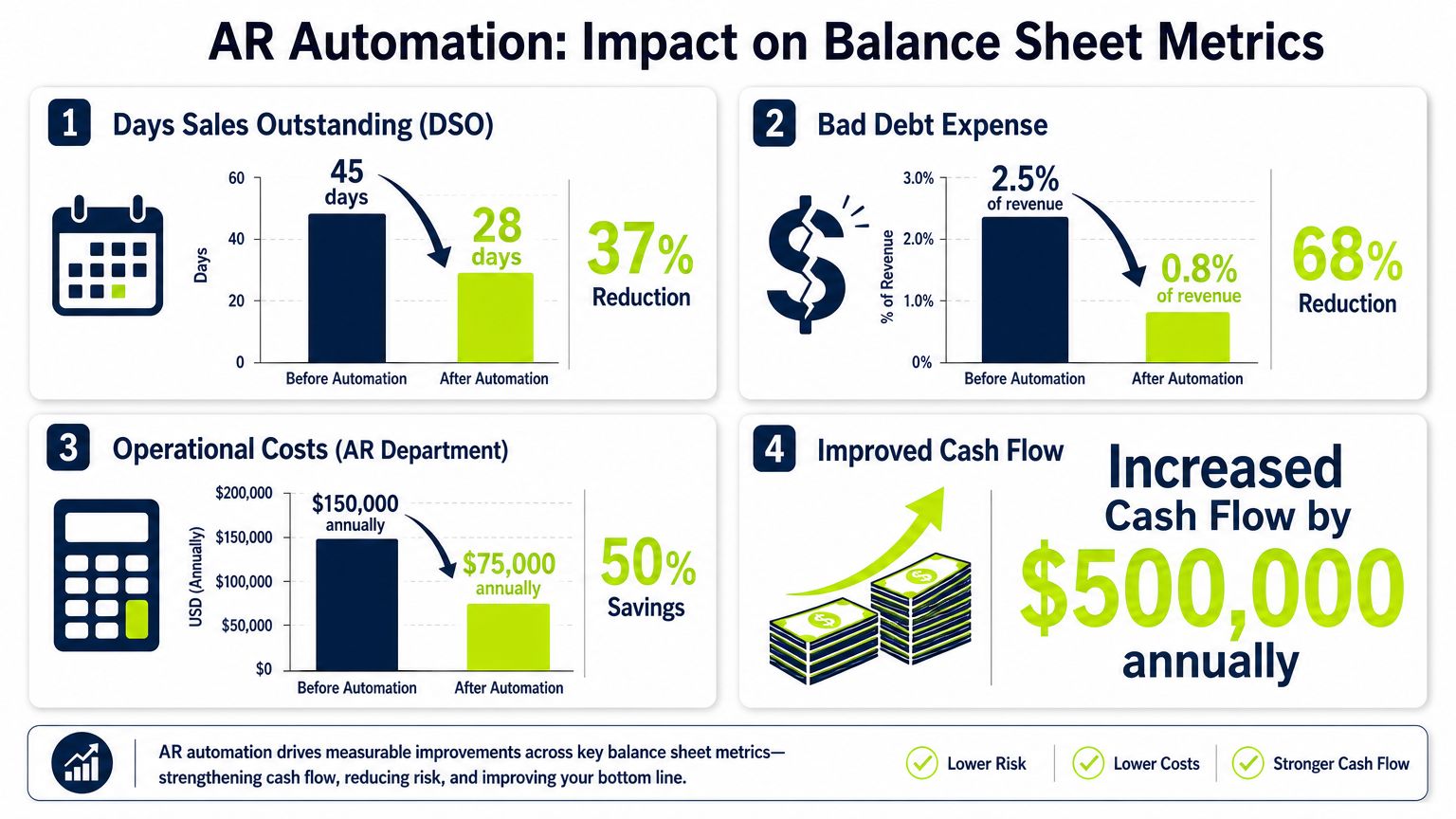

When invoice delivery becomes timely, payment options broaden, and reminders go out consistently, DSO usually comes under pressure for the right reasons. Clients pay sooner because there's less friction. Your team follows up earlier because the system exposes aging quickly. Exceptions don't sit unseen in email threads.

That directly improves cash flow predictability. Forecasting gets tighter when invoice status, payment activity, and unapplied cash are visible in one operating view. You don't need perfect certainty. You need fewer blind spots.

The second balance sheet effect is on accounts receivable quality. Cleaner collections workflows usually surface disputes, missing approvals, and client-side payment blockers earlier. That gives the team more time to resolve issues before balances age into something harder to collect.

For firms that want a sharper baseline on this metric, a working definition of what DSO means in practice helps anchor the conversation beyond the formula.

The quiet savings matter too

Most finance leaders focus first on speed to cash. They should. But operating cost matters almost as much.

A platform that cuts down manual matching, duplicate follow-ups, and status-check meetings reduces the hidden cost of collections. It also reduces the amount of senior time spent chasing what should already be known.

Here's the practical translation:

Platform capability | Operational change | Financial effect |

|---|---|---|

Faster invoice delivery | Clients see accurate invoices earlier | Less unnecessary delay in payment timing |

More payment methods | Clients can pay the way their AP process prefers | Fewer avoidable stalls at the payment step |

Automated cash application | Payments post faster and with fewer exceptions | Better visibility into true open AR |

Structured reminders | Follow-up happens on schedule, not by memory | More predictable collections performance |

When AR improves, the balance sheet usually looks better before the P&L tells the story. Cash shows up first.

The client experience improves too. Not because collections become softer, but because they become clearer. Clients receive accurate invoices, simple payment choices, and consistent communication. That tends to preserve relationships better than ad hoc outreach from whichever partner happens to be most frustrated.

How to Evaluate AR Software for Professional Services

Most vendor demos are designed to make payment acceptance look easy. That isn't the hard part.

The hard part is choosing software that reduces friction without shifting cost and complexity somewhere else. Many platforms can take a payment. Fewer can reduce DSO without adding reconciliation work, increasing processing expense, or weakening control.

A useful framing comes from The Takeoff's analysis of how finance leaders should evaluate B2B payment platforms. It highlights an issue many buyers miss. B2B payments are still highly manual, with one source citing 80% of SMB invoices as still manual and paid by check, while another notes 50% of B2B payments still happen by check and estimates a $200T digital opportunity over the next decade. The important point for a buyer isn't just that digitalization is growing. It's whether the platform lowers total AR friction, or merely moves cost from back-office labor to processing fees and exception handling.

What to ask before you ask about features

Start with integration depth.

If your firm runs on QuickBooks, the question isn't “does it integrate?” Nearly every vendor says yes. The question is whether QuickBooks AR automation is two-way, reliable, and timely enough to keep invoice status, payment posting, and collections actions aligned. If staff still need to export, clean, and rekey data, the integration isn't deep enough.

Then test workflow control. Good AR systems should let finance define contact sequences, escalation timing, dispute handling, and role-specific permissions without engineering support. Professional services firms need this because not every client should receive the same outreach, and not every collector should have the same authority.

A practical vendor scorecard

Use a short list that reflects operating reality:

- Integration quality: Can the system sync invoices, payments, notes, and status changes cleanly with your accounting stack?

- Cash application strength: Does it reduce manual matching, or does your team still resolve most receipts by hand?

- Collections configurability: Can you tailor cadence, language, and escalation by client type, partner, office, or service line?

- Portal experience: Is it simple for clients, or does it create one more login and one more excuse not to pay?

- Fee visibility: Can you see the trade-offs by payment method, including how card usage affects margins?

- Risk and exception handling: Does the platform help identify troubled accounts early, or only tell you balances are overdue?

If you're comparing systems broadly, reviewing a market view of accounts receivable software options can help sharpen the shortlist. But the decision still comes down to operational fit.

What good AI looks like

A lot of products now use the term AI AR automation loosely. In practice, finance teams should separate cosmetic AI from useful AI.

Useful AI helps prioritize who needs outreach, flags unusual payment patterns, routes exceptions faster, and supports collector judgment with better timing and context. Cosmetic AI writes reminder text but leaves the core workflow unchanged.

Don't ask whether the platform has AI. Ask which manual decisions your team will stop making every week.

This short walkthrough is worth using as a sanity check during evaluation:

In professional services, the right system should feel less like a payment app and more like disciplined receivables infrastructure. If the demo centers on convenience but avoids discussions about fees, matching, workflow exceptions, and forecast visibility, you're looking at an incomplete solution.

From Vendor Selection to First Value

The fastest way to create implementation pain is to roll out new AR software across every client, entity, and partner workflow at once.

A phased start works better. Pick one segment where friction is visible and the process is reasonably consistent. That could be recurring retainer invoices, one office location, or a client group with a history of delayed payment and heavy manual follow-up. The point is to create a contained operating environment where finance can see what changes.

Start with a pilot that finance can measure

Define success before configuration starts.

Use practical measures, not vanity metrics. Ask whether invoices are going out on time, whether payment options are being used, whether unapplied cash is dropping, whether collectors spend less time on manual reminders, and whether partner interruptions are decreasing. If the pilot improves those areas, you have evidence that the process is strengthening.

A good pilot also exposes workflow gaps early. You'll find the unusual approval path, the client who insists on a specific remittance format, the engagement partner who wants to review every message, and the accounting field that wasn't mapped correctly. That's useful. Better to discover those issues in a narrow lane than across the whole firm.

Get the right people involved early

AR automation is never only a finance project.

Partners influence client communication. Account managers often know where relationships are fragile. IT or outsourced support may own the accounting connection. Whoever manages QuickBooks, billing, and collections policy needs to agree on what the system should do by default and where human approval still matters.

A simple rollout sequence usually works best:

- Stabilize invoice and customer data so the system starts with clean records.

- Turn on payment capture and sync for the pilot group first.

- Layer in reminders and escalation rules after the base workflow proves reliable.

- Review exceptions weekly and update the playbook before expanding.

Aim for confidence, not spectacle

The first value usually comes from fewer manual touches and better visibility, not from a dramatic transformation story.

If the team can trust invoice status, see what's overdue without assembling it manually, and spend less time figuring out where cash belongs, adoption tends to follow. That's especially true in firms where collections has historically depended on personality and persistence more than process.

The best implementations don't feel flashy. They feel calmer. Finance has cleaner data. Partners get fewer surprises. Clients get a more consistent experience. That's what good change management looks like in AR.

Defining and Measuring Accounts Receivable Automation ROI

Once the platform is live, ROI needs to move out of the sales deck and into the monthly operating review.

The strongest case for AR software isn't abstract efficiency. It's whether the firm collects more predictably, spends less effort per dollar collected, and gets a clearer view of risk in the receivables book.

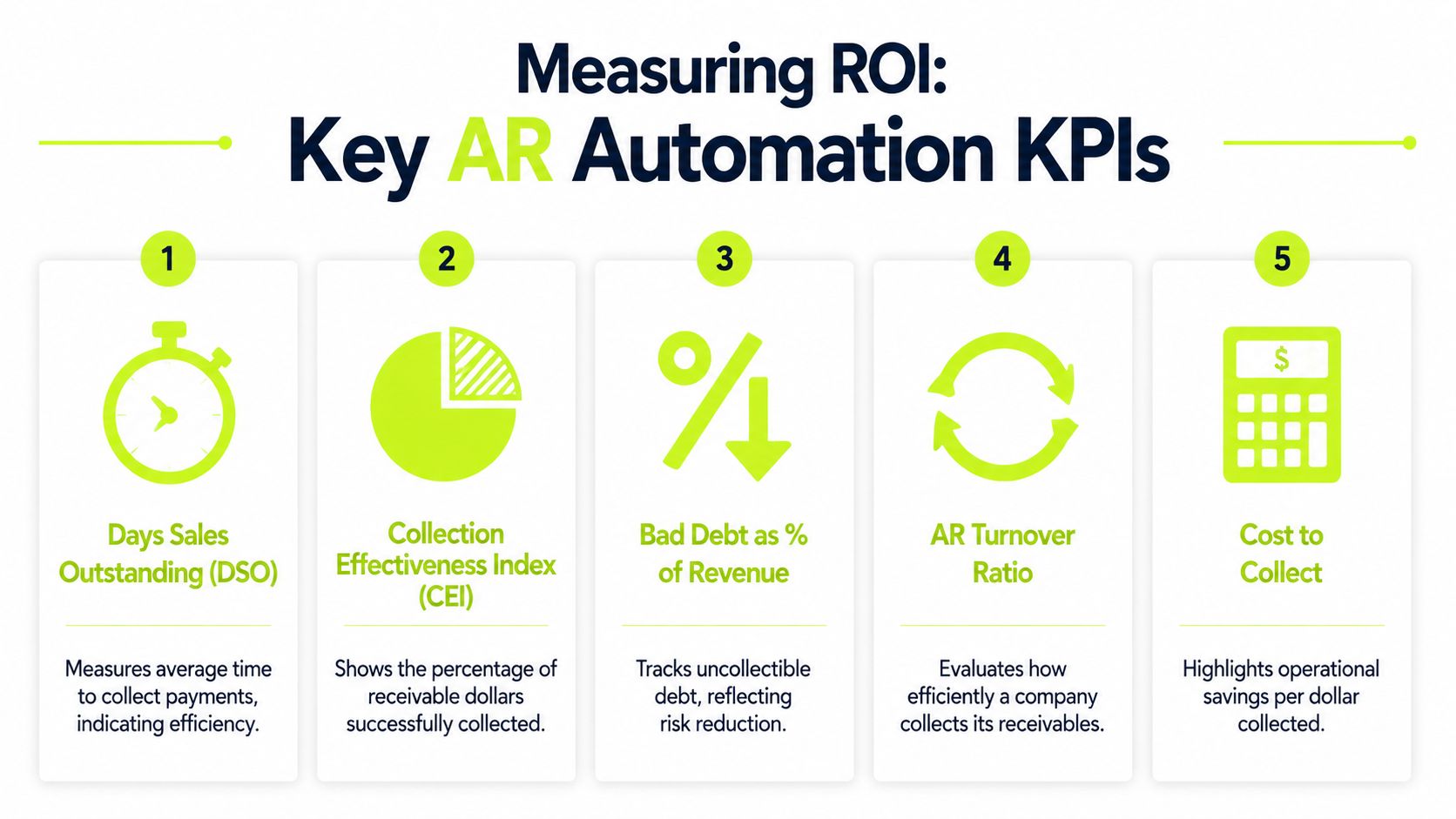

The KPI set worth tracking

A practical dashboard should include a mix of speed, quality, and efficiency measures.

- DSO: This remains the headline measure for how quickly receivables convert to cash.

- CEI: Collection Effectiveness Index helps show how much of available receivables the team is collecting.

- ADD: Average Days Delinquent gives a cleaner read on lateness beyond overall DSO.

- AR turnover ratio: Useful for understanding collection efficiency over time.

- Cost to collect: Tracks labor, tool spend, and process overhead relative to the receivables operation.

Not every firm needs every metric in the first month. But if you only track DSO, you can miss whether improvement came from healthier process or from short-term pressure tactics that create other problems later.

How to model ROI without overstating it

Keep the math conservative.

Start with working capital release from any DSO improvement. Then add identifiable labor savings from tasks the platform removes or compresses. Then consider softer but still real gains such as fewer write-offs, better visibility, and stronger client payment experience. Don't force precision where you don't have it. Finance teams trust models that leave room for judgment.

A simple framework looks like this:

ROI component | What to calculate |

|---|---|

Working capital effect | Average daily revenue multiplied by DSO improvement |

Labor efficiency | Hours removed from invoicing, follow-up, matching, and reporting |

Collections quality | Changes in delinquency, dispute aging, and exception backlog |

Forecast value | Improvement in confidence around expected cash timing |

Good ROI models don't try to prove perfection. They show that the current manual process already has a cost, and that cost is avoidable.

Why this matters now

The market isn't moving toward less payment complexity. It's moving toward more embedded, more connected infrastructure. Resolve's reporting on B2B payments market growth says the global B2B payments market was valued at $1.355 trillion in 2024 and is projected to reach $2.943 trillion by 2033. That scale points to structural demand for systems that reduce manual invoicing, speed settlement, and improve working-capital efficiency.

For a professional services firm, the takeaway is practical. As clients expect cleaner digital payment experiences and internal finance teams are asked to do more with tighter headcount, accounts receivable automation stops being a convenience project. It becomes part of how the firm protects liquidity.

The useful discipline is to review ROI in layers. First, has the team reduced manual work? Second, is cash arriving with fewer surprises? Third, is leadership getting a better view of receivables risk before it becomes a collections problem? If the answer to those questions is yes, the platform is doing its job.

Taking Control of Your Firm's Cash Flow

The old model treated a B2B payment platform as a transaction utility. Accept the payment, post the cash, move on. That model is too limited for firms that care about control.

The newer model is more valuable. Payment infrastructure now feeds collections, forecasting, and risk decisions. KPMG's view, summarized in its report on connected B2B payment data, is that combining payment, AP automation, and AR automation data can help identify delays and discrepancies, assess financial health, and support better credit evaluation. That marks a significant shift. The platform becomes part of the firm's control layer, not just its payment layer.

For most firms, the next steps are simple:

- Calculate the current cost of collections: Include staff time, partner interruptions, and rework around unapplied cash.

- List the top friction points: Late invoice delivery, weak follow-up discipline, limited payment options, poor QuickBooks sync, or unclear ownership.

- Pressure-test your process design: If you need a practical outside reference on collections workflow, this guide to dunning management software is a useful lens on structured follow-up and escalation.

The firms that improve cash flow most reliably aren't always the most aggressive. They're usually the most consistent.

Resolut automates AR for professional services. It helps firms run collections with more consistency, better accuracy, and the right amount of human judgment. If you want tighter control over receivables without turning client relationships into a collections battle, Resolut is built for that.