Bad Debt Reduction: A CFO's Playbook for 2026

A practical bad debt reduction playbook for CFOs. Learn to design credit policies, automate collections, and improve cash flow with actionable strategies.

Aging receivables usually don't arrive as a crisis. They show up as a few invoices slipping past terms, a partner asking for patience on a client relationship, and a controller carrying too much of the process in their head.

Then cash gets tighter than revenue suggests it should be.

That's the moment many professional services firms realize they don't have an accounts receivable process. They have habits. Some are good. Some are expensive. Bad debt reduction starts when finance stops treating overdue invoices as isolated exceptions and starts treating them as a managed operating system.

The True Cost of Unmanaged Receivables

Most CFOs have had the same month-end experience. Revenue looks acceptable. Pipeline looks active. But the aging report tells a different story. Current invoices are thinning out, older balances are stacking up, and the cash forecast is starting to rely on hope.

In professional services, this gets missed because the work is already delivered. The team feels productive. The client relationship may still look healthy. But an unpaid invoice is no longer a sales success. It's an unsecured loan.

The broader B2B picture makes the risk hard to ignore. In 2023, approximately 9% of all credit-based B2B sales resulted in uncollectible losses, and businesses wasted an estimated $200 billion annually on unpaid invoices, according to commercial debt statistics compiled here. The same source notes that only 10% of invoices over 12 months old are likely to be collected.

That last point matters more than is commonly acknowledged.

Practical rule: If an invoice becomes “old news” internally, it usually becomes “low priority” externally.

What this looks like inside a firm

A common pattern goes like this:

- Project teams finish strong. The client is happy with delivery.

- Billing goes out late. Time entries lag, approvals sit, or the invoice misses the best payment window.

- Collections start softly. The first follow-up is polite but delayed.

- Disputes surface late. Nobody knew the client wanted a PO, revised narrative, or split billing.

- Finance inherits a relationship problem. By then, the invoice is old and the advantage is lost.

None of this looks dramatic in isolation. Combined, it creates a quiet leak in working capital.

Why finance has to own the system

Bad debt is often framed as a sales issue, a client issue, or an economic issue. In practice, it's usually a systems issue. Terms weren't clear. Invoices weren't sent on time. Follow-up lacked cadence. Nobody had a trigger for escalation.

That's why I view bad debt reduction as a control discipline, not a collections tactic. If your current process depends on who remembers to send the reminder, it isn't a process.

For firms that want a clearer picture of how operational friction in billing and follow-up translates into cash drag, this breakdown of the true cost of AR inefficiency in professional services is worth reviewing.

Designing Your Proactive Defense System

A client signs the engagement letter on Friday. Work starts Monday. Nobody confirms billing contacts, PO requirements, or who can approve invoices. Sixty days later, finance is chasing a balance that was hard to collect from the start.

That failure starts upstream.

Start at onboarding, not at delinquency

The first defense against bad debt is policy. Good firms treat onboarding as the point where credit, billing, and delivery rules are set together. If those controls are vague at the start, collections gets harder with every week of work performed.

A workable policy usually includes four things:

- Defined payment terms in the engagement letter Terms need to be specific and visible. If billing is milestone-based, name the trigger for each invoice. If a retainer must be replenished, state the threshold and timing.

- A repeatable credit review for new clients Review risk before exposure builds, then review it again if the account changes. The credit management guidance from Dun & Bradstreet on assessing and monitoring customer credit risk supports using current financial information, payment behavior, and ongoing monitoring rather than relying on a one-time check. For a professional services firm, that means spotting strain early, before unbilled time and open AR pile up.

- Internal exposure limits Set a ceiling for unbilled work and open receivables by client. Once that limit is hit, finance reviews the account before more work goes out the door.

- Retainers or deposits for higher-risk work Front-loaded labor needs protection. If the client is new, the project is large, or payment history is uneven, collect cash before the exposure grows.

Terms only work when partners follow them.

What good policy actually says

Weak policies fail because they leave room for improvisation. “Bill promptly” is too vague. “Accounting handles collections” is not an operating standard.

A useful policy answers the questions people face in real time:

Question | Policy standard |

|---|---|

Who approves credit exceptions | CFO or controller, not the delivery lead alone |

When billing must go out | Immediately after a milestone, time period, or deliverable approval |

When work pauses | After defined nonpayment or threshold breach |

Which clients require retainers | New, high-risk, cross-border, or unusually large engagements |

Who owns disputes | Delivery lead resolves service issue, finance owns payment timing |

Firms usually lose control as follows: Sales agrees to custom terms. Delivery keeps working to protect the relationship. Finance sees the risk only after the balance is already old.

Cross-border work adds another layer. Currency, banking rails, tax forms, and transfer timing all affect whether an invoice is easy to collect or easy to delay. This guide on navigating cross-border payment challenges for exporters is useful because it treats payment design as a control issue from the start.

Build flexibility without losing control

Policy should adapt to client risk, but the rules need to stay disciplined. I would not give a long-standing client with a clean payment record the same structure I would give a new client asking for extended terms on a large project. That is not inconsistency. That is risk pricing.

Use clear tiers:

- Low-risk clients get standard terms and fast approval.

- Established but inconsistent clients get shorter billing intervals and tighter account review.

- Higher-risk clients move to deposits, staged invoices, or lower exposure caps.

The point is simple. Payment behavior should shape billing design before a receivable becomes a collection problem. That is how bad debt reduction becomes a financial system with measurable return, not a monthly cleanup exercise.

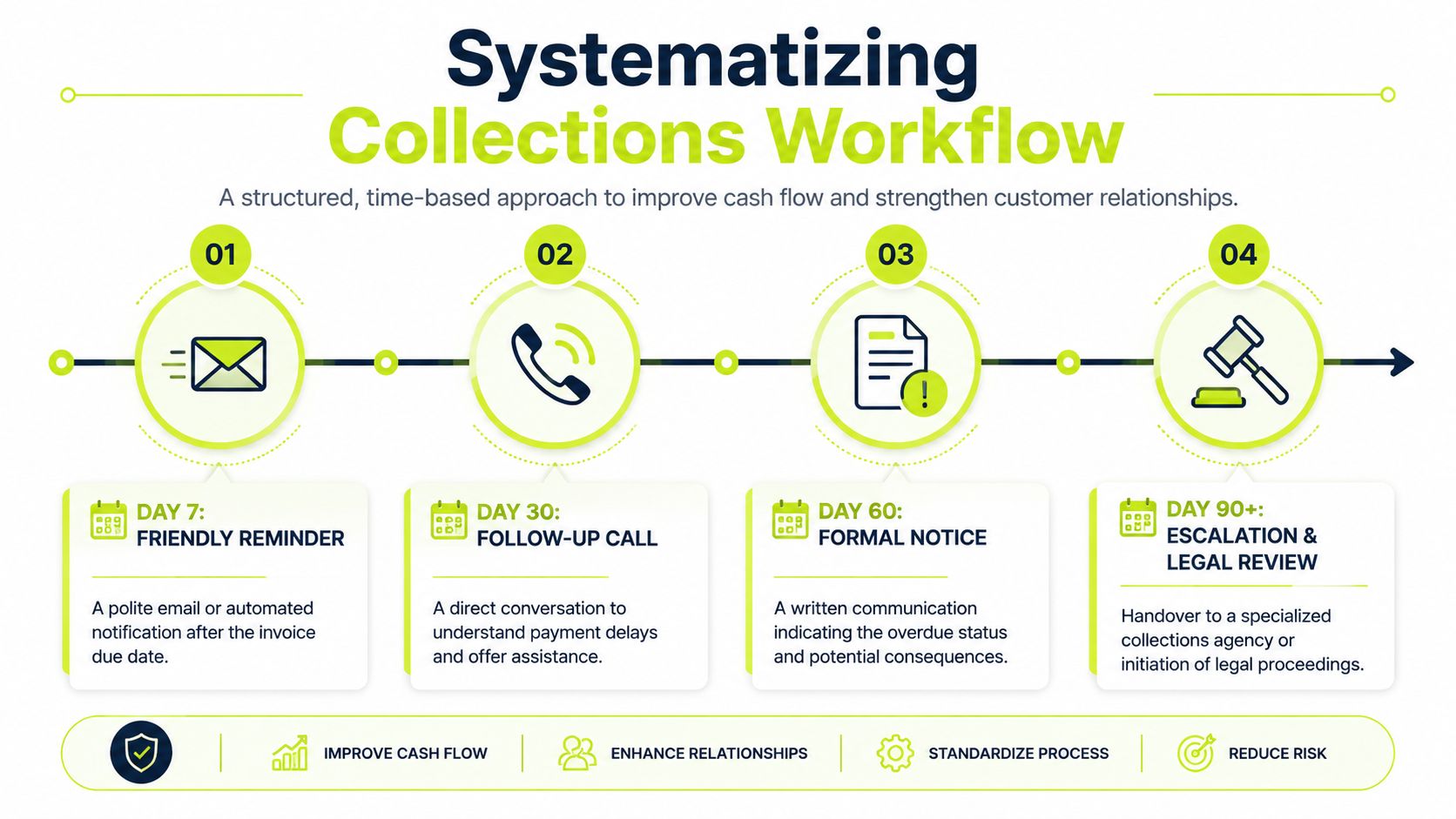

Systematizing the Collections Workflow

On Monday, AR says a client promised payment last week. By Wednesday, the delivery partner says the work is still moving because no one wants to strain the relationship. By Friday, the invoice is 45 days past due and nobody can say who owns the next step. That is not a collections problem. It is a workflow failure.

Collections performance improves when timing, ownership, and escalation are defined before an invoice goes overdue. Firms that rely on memory and individual style get inconsistent results. Clients notice that quickly. They learn who can be delayed, which excuses buy time, and how long they can sit on a balance before anyone acts.

Use time-based stages with clear ownership

A disciplined workflow assigns a deadline, a channel, and a named owner at each stage. It also changes the objective as the invoice ages.

Stage | Channel | Tone | Owner | Objective |

|---|---|---|---|---|

Pre-due reminder | Helpful | AR specialist | Confirm receipt and remove admin friction | |

Early overdue | Email plus call if needed | Direct and professional | AR specialist | Get payment date |

Mid-stage overdue | Phone call and written recap | Firm | Controller | Resolve blockers and test seriousness |

Late-stage overdue | Formal notice | Controlled escalation | Controller or CFO | Protect recoverability and trigger next action |

That clarity matters because delay usually starts with confusion, not refusal.

The cadence I'd put in place

A sound workflow follows a simple sequence, but the discipline is in doing it every time.

- Before due date Send a reminder with the invoice, payment instructions, and a billing contact. The job is to remove preventable friction before the due date passes.

- Just after due date Send a short note that confirms the balance and asks whether payment is already in process. Keep it factual. Long emails invite delay.

- If the client stays silent Call. Silence usually means one of three things: the invoice is stuck in approval, someone is disputing it informally, or it has dropped in priority.

- If explanations keep changing Move the account into tighter review. Ask for a specific payment date, then confirm the conversation in writing.

- If the account reaches late stage Escalate according to policy. Repeating the same reminder does not improve recoverability.

A collections process should answer one question at every step: what happens next if the client does nothing?

Speed beats clever wording

Older receivables are harder to collect. Any controller who has worked an aging report knows that. Early action matters because once an invoice loses urgency inside the client's organization, recovery depends less on message quality and more on whether your team can reach the right decision-maker and force a clear commitment.

That is why I prefer a documented service standard over improvised outreach. If day 3, day 15, and day 30 each have a defined action, the team stops debating tone and starts reducing risk. Firms building that discipline often benefit from a clear accounts receivable automation framework, especially when volume makes manual follow-up inconsistent.

Standardize scripts, not judgment

Good collections teams do not freelance the process. They use standard templates, call notes, and escalation triggers. Judgment still matters, but it should be reserved for the accounts that warrant it.

For example, a billing dispute needs coordination with delivery. A strategic client asking for a short extension may justify a controlled exception. A client who keeps missing promised dates needs tighter terms and senior involvement. Those are different cases. They should not be handled with the same script or by the same person.

Useful references can help refine that late-stage playbook. This overview of effective strategies for debt recovery is a practical example because it separates routine follow-up from formal escalation.

A mature collections workflow improves more than cash timing. It reduces avoidable write-offs, shortens the path from invoice to action, and gives leadership a clear view of where accounts stall and why.

Leveraging Intelligent AR Automation

Manual AR breaks first in the same places every time. Follow-ups go out late. Notes live in too many systems. Promises to pay are captured inconsistently. The finance team spends more time administering outreach than deciding what action makes sense.

That's where accounts receivable automation starts to matter.

Basic automation is useful. QuickBooks AR automation rules, scheduled reminders, and payment links can clean up the obvious gaps. But basic automation usually acts like a timer. It sends the same message to everyone at the same stage.

Intelligent AR automation does more than that. It coordinates invoice delivery, reminders, payment behavior, dispute tracking, and risk changes across the whole client base.

Where basic automation helps

For smaller firms, simple automation can deliver immediate control.

- Invoice triggers keep billing from drifting past the service date.

- Reminder schedules stop the team from relying on memory.

- Payment links and portals remove friction for clients who are willing to pay.

- Shared activity logs reduce the “I thought someone else handled it” problem.

That alone can make AR software for professional services worthwhile. It creates consistency. It also gives leadership a cleaner view of whether delays come from client behavior or internal slippage.

Where AI AR automation changes the game

The bigger improvement comes when the system starts adapting to client behavior. In a volatile economy, customers' creditworthiness can change rapidly, and modern AR systems address that with dynamic reviews rather than one-time checks, as discussed in this CBO budget options reference on bad-debt reimbursement and risk conditions.

That matters because many professional services firms still treat onboarding as the final risk decision. It isn't. A client who paid reliably last year may pay very differently after budget cuts, financing pressure, leadership turnover, or reimbursement changes in their own market.

Operating principle: Review risk as a moving condition, not a fixed label assigned at onboarding.

Intelligent systems can surface patterns a busy finance team may miss:

- Payment drift on accounts that used to pay predictably

- Repeated partial payments that signal stress or internal approval issues

- Channel response patterns that show which clients react to email, phone, or portal prompts

- Dispute clustering tied to a billing lead, service line, or client group

For readers looking at the category more broadly, this explanation of what AR automation is is a useful foundation.

Orchestration matters more than reminders

The phrase “AI AR automation” gets overused. Its value isn't novelty. It's orchestration.

A good system should help finance do four things at once:

- Prioritize accounts by risk and collectability

- Route outreach by stage, amount, and history

- Keep every touch documented in one place

- Support human intervention when the account needs judgment

That's how a small team starts operating like a much larger one. The software handles sequence and signal. Finance handles exceptions and decisions.

A short walkthrough makes the distinction clearer:

The practical test is simple. If your team still exports aging into a spreadsheet, rewrites follow-ups manually, and checks client risk only when something goes wrong, the process is too dependent on labor. Automation should reduce administrative effort and increase control at the same time.

Managing Late-Stage Receivables and Escalation

Some invoices won't respond to standard collections. At that point, many firms make one of two mistakes. They either become overly accommodating and let the balance age indefinitely, or they escalate emotionally and damage the chance of recovery.

Neither approach is disciplined.

Late-stage receivables need a decision framework. Once an account reaches that stage, the question isn't whether the client relationship matters. It's how to maximize recovery while controlling further exposure.

When a payment plan makes sense

A payment plan is useful when the client still communicates, acknowledges the debt, and has a realistic path to paying over time. It's less useful when the plan is just a polite delay mechanism.

I'd look for three conditions before offering one:

- Acknowledgment of the balance in writing

- Specific payment dates, not vague intent

- Protection against new exposure, such as pausing additional work or requiring prepayment going forward

If those conditions aren't present, a payment plan often extends risk instead of reducing it.

Late-stage AR should be managed like a workout process. Every concession should buy clarity, commitment, or security.

When to stop extending courtesy

Professional services firms are especially vulnerable here because delivery teams want to preserve the client relationship. That instinct is understandable. It's also expensive when finance keeps hearing, “They've always paid eventually.”

Eventually is not a control.

A useful internal test is whether the account has become decisionless. If weeks pass without a confirmed payment date, documented dispute resolution, or signed plan, the firm is no longer managing the receivable. It's carrying it.

Agency, legal, or write-off

The escalation path should depend on facts, not frustration.

Situation | Likely best next step |

|---|---|

Client is responsive but strained | Structured payment plan with tight monitoring |

Client ignores repeated outreach | Formal demand letter |

Debt is valid but collection is stalled | External collections agency may be efficient |

Contract is strong and amount is material | Legal review may be justified |

Documentation is weak or dispute is real | Settle, revise, or reserve appropriately |

This is a cost-benefit decision. Some debts are too small or too ambiguous to litigate. Others justify formal action because the amount, precedent, or client behavior creates broader risk.

The key is to separate emotion from economics. A demand letter is not a personal statement. It's a business signal. Agency placement is not failure. It's an external tool. Legal action is not toughness. It's one option in a recovery portfolio.

Firms with strong bad debt reduction discipline make these choices earlier and more calmly because the file is already documented. Terms are clear. Follow-ups are logged. Disputes were surfaced before the account became stale. That preparation matters as much as the final escalation step.

Measuring Your Bad Debt Reduction ROI

If bad debt reduction isn't measured, it gets recategorized as “finance overhead.” That's the wrong view. A controlled AR process protects cash, preserves margin, and gives leadership a cleaner forecast.

The scorecard doesn't need to be complicated. It needs to be used.

The core KPIs

I'd track at least these:

- Days Sales Outstanding (DSO) Formula: Accounts Receivable / Average Daily Credit Sales This shows how long receivables remain outstanding on average.

- Collection Effectiveness Index (CEI) Formula: Cash Collected / Collectible Receivables for the period This shows how effectively the team converts available receivables into cash during the measurement window.

- Bad Debt to Sales Ratio Formula: Uncollectible balances / Revenue This shows how much revenue is ultimately lost to nonpayment.

- Average Days Delinquent Formula: DSO minus best possible DSO This helps separate billing-cycle reality from true lateness.

How to tie process changes to financial return

The ROI calculation should be practical. Compare the cost of software, implementation time, and internal process changes against the value created through lower write-offs, faster collections, and less manual effort.

A basic approach looks like this:

- Estimate current loss and delay Include write-offs, time spent chasing invoices, and the cost of carrying slow-paying balances.

- Measure post-change performance Look at trend movement in DSO, delinquency aging, and collection consistency.

- Assign value to the change Faster cash improves flexibility. Lower write-offs protect margin. Less manual effort lets finance spend more time on analysis and control.

For firms refining reserves and policy around collectability, this guide to the allowance for uncollectible accounts is a useful companion to the KPI work.

Good AR measurement changes the conversation with partners. It turns “collections feels better” into “cash is arriving earlier and losses are lower.”

Bad debt reduction works best when policy, workflow, and measurement reinforce each other. That's how you reduce DSO, improve cash flow, and make the receivables function more predictable month after month.

Resolut automates AR for professional services with a system built for consistent follow-up, accurate execution, and human control where it matters. If you're tightening credit policy, improving collections discipline, or looking for AI-driven orchestration beyond basic reminders, Resolut is designed to help finance teams get paid faster without turning client communication into chaos.