Bank Transfer Payments: A CFO's Guide to Cash Control

Master bank transfer payments (ACH, Wire, RTP) to reduce DSO and improve cash flow. A practical guide for CFOs on reconciliation, risk, and AR automation.

You know the pattern. Revenue is booked. The work is delivered. The client says payment has been sent. But your controller is still looking at an aging report, your cash forecast is soft around the edges, and your team is burning time matching deposits to invoices instead of closing the month cleanly.

For professional services firms, that gap between earned revenue and usable cash is where pressure builds. It affects payroll timing, partner distributions, hiring decisions, and how confidently you can invest. In that environment, bank transfer payments aren't just a payment option. They're part of your cash control system.

When firms get this right, they don't just collect faster. They tighten reconciliation, improve forecast reliability, and reduce the amount of receivables work that depends on tribal knowledge inside the finance team. That's where accounts receivable automation, AI AR automation, and better AR software for professional services start to matter.

Beyond Invoices The True Role of Bank Payments

A professional services CFO usually doesn't lose sleep over invoicing. The invoice went out. The work was approved. The client relationship is solid. The concern is whether cash will land when expected, whether it will be applied correctly, and whether the team will know that in time to act.

That's why bank transfer payments deserve more attention than they usually get. In most firms, they sit in the background as a treasury or billing detail. In practice, they shape three operating outcomes every finance leader cares about: DSO, reconciliation accuracy, and cash flow predictability.

The reason is simple. Bank transfers carry the bulk of serious business value across the system. In 2025, credit transfers accounted for 95.5% of the total transaction value processed by Irish resident payment service providers, amounting to €11.60 trillion according to the Central Bank of Ireland payments services statistics. That matters because it confirms what most operators already see firsthand. For high-value B2B settlement, bank transfers remain the backbone.

What this means in a services firm

If you run a firm in the $3M to $50M range, your exposure usually looks like this:

- Larger client invoices depend on transfer timing: A delayed transfer changes weekly cash positioning quickly.

- Application quality matters as much as collection speed: Cash in the bank doesn't help much if the team can't tie it to the right matter, engagement, or invoice.

- Client experience is part of collections performance: If payment instructions are unclear or references fail, a healthy client account can still age unnecessarily.

Operator view: The invoice is only the request. The payment rail is what determines when revenue becomes controllable cash.

Here, many firms stay too reactive. They focus on reminder cadence and collector effort, but not on the mechanics that govern how the client pays. If the transfer method creates ambiguity, delay, or reversibility, your AR team inherits that mess downstream.

A tighter payment design gives you fewer exceptions, cleaner posting, and better visibility into what's collectible now versus what's merely promised.

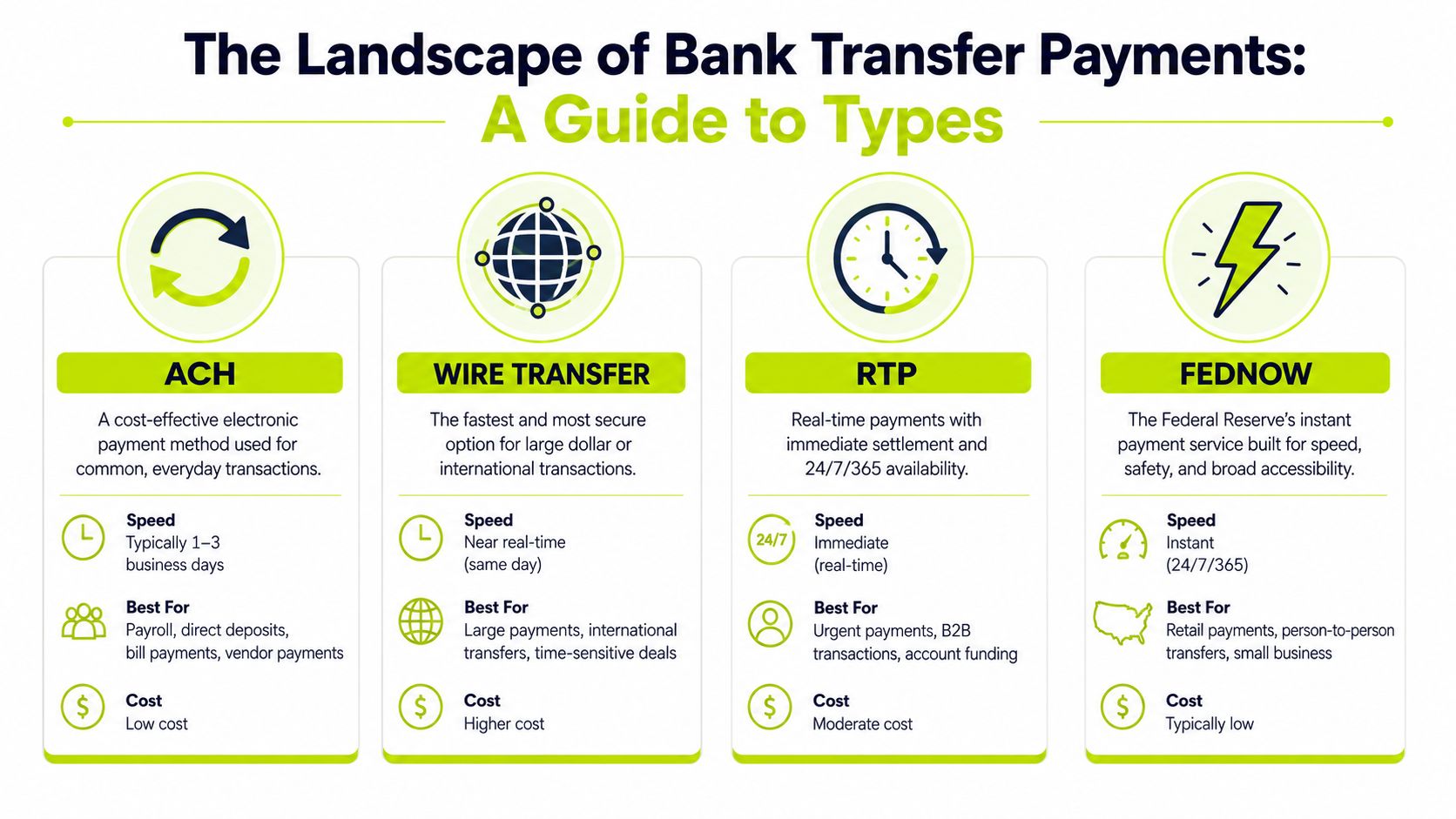

The Landscape of Bank Transfer Payments

Most finance teams use a mix of transfer types without a clear framework for when each one should be encouraged. That creates friction. The right question isn't which rail is “best.” It's which rail best fits the invoice, the client, and the cash control requirement.

In the U.S., the ACH network processes around 21 billion transactions annually, valued at $36.9 trillion, making it the dominant domestic bank transfer channel, according to this payments industry summary from Prove. The same source notes that this volume is over 10 times that of wire transfers, even though wires are used for larger-value wholesale payments.

A practical comparison

Payment type | Best fit | Strength | Trade-off |

|---|---|---|---|

ACH | Recurring domestic payments, lower-friction client remittance | Familiar and widely used | Slower settlement and less certainty |

Wire transfer | High-value invoices, urgent settlements, international payments | Fast movement and strong finality | Higher operational scrutiny and more input accuracy required |

SEPA credit transfer | Eurozone payments | Standardized regional transfer flow | Mainly relevant for firms with EU payment activity |

Real-time payments | Immediate domestic transfer needs | Instant confirmation and fast availability | Adoption and client readiness vary by bank and corridor |

How finance leaders should think about each rail

ACH works well when convenience matters more than immediacy. For retainers, recurring advisory fees, or predictable domestic payments, it often fits naturally. The weakness is operational certainty. You may see the payment in process before you can treat it as fully dependable cash.

Wire transfers belong in a different category. They are the right tool when invoice size, timing pressure, or settlement confidence matters more than convenience. Firms often underuse wires for large invoices because they focus on client effort instead of treasury outcome.

SEPA is useful if your clients operate in Europe and you want a cleaner euro transfer experience. The benefit is standardization. The challenge is that many U.S.-based services firms don't think about it until cross-border volume grows enough to expose process gaps.

RTP and FedNow are operationally attractive because they reduce the waiting game. If a client can pay instantly and your systems can ingest that data cleanly, forecasting gets sharper.

Don't optimize every invoice for the same payment rail. Optimize each invoice for certainty, cost, and collection effort.

A simple decision rule

For most firms, the decision logic should look like this:

- Use ACH when predictability is good enough and volume is high

- Use wire when invoice value or urgency raises the cost of delay

- Use real-time rails when the client can support them and speed matters

- Use regional rails like SEPA when they reduce cross-border friction

Visual idea: a one-page matrix mapping invoice size on one axis and settlement urgency on the other, with each transfer type placed where it belongs.

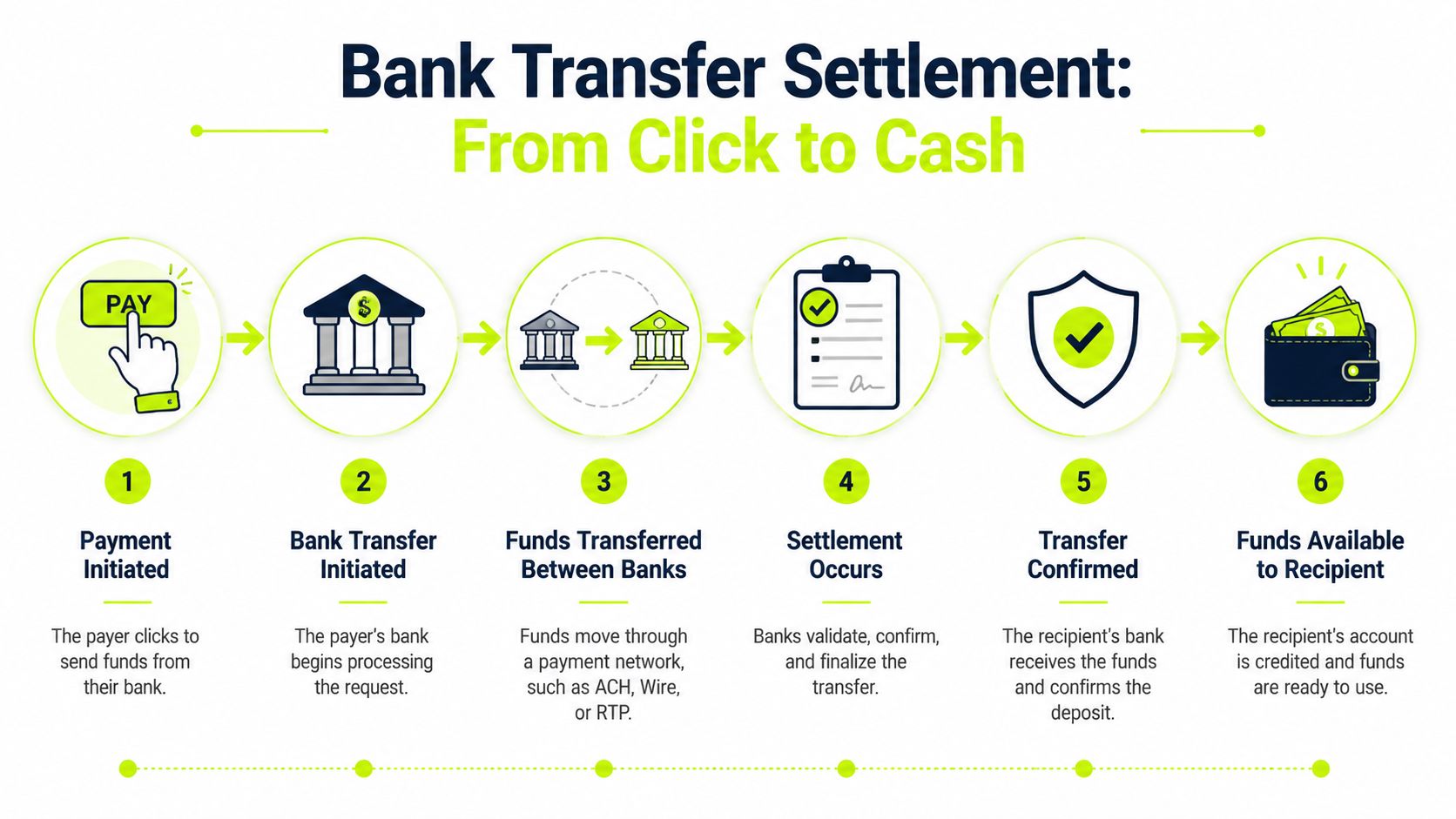

Understanding Settlement Mechanics and Timing

Most receivables problems blamed on “late payment” are a mix of timing, data quality, and settlement misunderstanding. If the finance team doesn't know where a transfer sits in the process, they can't forecast cash well or answer client questions with confidence.

A bank transfer moves through a few distinct steps. The client initiates the payment. The originating bank reviews and sends it through the relevant payment network. The network and participating banks clear and settle the transaction. Then the beneficiary bank credits your account.

Why wires feel different from ACH

For wholesale systems like Fedwire, the originating bank verifies the request before the operator settles the payment between banks and forwards the message to the beneficiary's bank, as described in JPMorgan's overview of how wire transfers work, including settlement mechanics. That individual handling is why wires are typically the cleaner option for high-value receivables.

ACH behaves differently. It's built around batch processing. That's fine when speed isn't the main issue. It's less helpful when your collections team is trying to answer a partner asking whether cash is available today.

What operators need to watch

Three timing issues show up repeatedly in professional services AR:

- Initiation isn't settlement A client saying payment was sent may only mean the file was submitted.

- Cutoff times change the day Domestic wires often settle the same business day if sent before the bank's cutoff, while international transfers typically take longer depending on destination and regulatory requirements, as outlined in the FFIEC discussion of wire transfer timing and funds availability.

- Intermediary steps create opacity Cross-border payments can route through intermediary banks, which makes status tracking harder and reconciliation slower.

If you manage service firms, Steingard Financial's piece on money in transit for service businesses is a useful reminder that timing gaps aren't just accounting nuisances. They affect how you judge liquidity in motion.

For teams refining ACH handling inside AR workflows, this explanation of what an ACH credit is is useful because it clarifies the operational distinction between initiated payments and settled funds.

A receivables forecast only gets better when the team treats payment status as a process state, not a yes-or-no event.

Visual idea

A cinematic dashboard image works well here. Show three columns labeled “initiated,” “settling,” and “applied,” with invoices moving between them. That conveys the full picture better than a simple paid/unpaid view.

Managing Risk Finality and Fraud

The biggest mistake I see in receivables operations is treating all bank transfer payments as equally safe once they appear on a remittance report. They aren't. Speed, reversibility, and compliance exposure vary by rail, and those differences affect cash decisions directly.

The sharpest divide is between final settlement and provisional cash.

Finality changes behavior

Wire transfers executed via Fedwire or CHIPS are irrevocable once the receiving bank credits the funds, while ACH transfers are reversible for up to 60 days, according to Resolut's discussion of how modern AR automation protects client relationships. The same source notes that prioritizing wires for invoices over $50k can reduce DSO by 2–4 days because the payment uncertainty disappears.

That's not a technical footnote. It changes what your team can safely do after payment arrives.

With a wire, treasury can treat the cash as final once credited. With ACH, the finance team needs more discipline. Booking the receipt is one thing. Treating it as fully cleared capital for planning purposes is another.

Where firms get exposed

A few patterns drive avoidable risk:

- Large invoices collected through the wrong rail: If a major payment lands through a reversible method, your forecast can look stronger than it is.

- Weak controls around payment instruction changes: Fraud often enters through updated banking details, rushed approvals, or email-based exception handling.

- Consumer payment overlap: If a firm accepts bank transfers from consumers, the Electronic Fund Transfer Act and Regulation E can apply to certain electronic fund transfers, as clarified in the CFPB's electronic fund transfers FAQs.

Practical rule: Match the payment rail to the risk profile of the invoice, not just to what's easiest for the payer.

Fraud control has to sit inside AR operations

Fraud prevention in receivables isn't only an IT concern. It sits in billing, master data, approval routing, and exception handling. If your team hasn't formalized those checks, this guide on why perform a fraud risk assessment is worth reading because it frames fraud work as an operating discipline rather than a periodic audit exercise.

A clean close also depends on disciplined matching between bank activity and ledger treatment. This overview of bank account reconciliation is a useful reference if your team still handles too many exceptions manually.

What works in practice

For professional services firms, the control framework is usually straightforward:

- Reserve wires for larger or more time-sensitive invoices

- Use ACH selectively where convenience outweighs finality risk

- Require structured approval for any bank detail changes

- Separate receipt recognition from final cash certainty in internal reporting

- Push exception handling out of email and into a controlled workflow

Visual idea: a split-screen chart showing “cash received” versus “cash final,” with the gap representing receivables risk that the GL alone doesn't reveal.

Automating Reconciliation for Flawless Cash Application

Most AR teams don't struggle because clients never pay. They struggle because the payment arrives with poor reference data, lands in a bank feed without enough context, and then sits in an exception queue while someone tries to decode it.

That's where DSO stretches. Not from collections effort alone, but from cash application failure.

A meaningful operational gap appears when customers use non-digital aliases or paper-based references for bank transfer payments. The Federal Reserve Bank of Kansas City research notes that 31% of underserved households still use such methods for a quarter of their transactions, and that this gap can increase DSO by 7–12 days because payments remain unreconciled, as described in the study on underserved households in digital payment services.

That matters even in B2B services environments. Clients don't always pay with the perfect invoice number in the memo field. Some send from a parent entity. Some use a shorthand name. Some submit a transfer after forwarding a PDF remittance that never reaches the right inbox. Manual teams can work through this, but they do it slowly and inconsistently.

Why manual matching breaks down

The old process usually looks like this:

- Bank feed arrives: Treasury or accounting sees deposits but not always the invoice context.

- Remittance arrives separately: It may come by email, portal upload, or not at all.

- Staff member investigates: They search QuickBooks, client history, and old email chains.

- Cash sits unapplied: Aging reports remain distorted until the match is resolved.

Accounts receivable automation starts paying for itself precisely in such situations. Good systems don't wait for perfect data. They use payer behavior, open invoice patterns, remittance text, amount matching, and client history to recommend or execute the match.

Unapplied cash is one of the easiest ways to make a healthy AR book look worse than it is.

What AI AR automation changes

AI AR automation improves the handoff between payment receipt and ledger accuracy. Instead of forcing staff to interpret every exception, it narrows the exception queue to the cases that require judgment.

That matters for firms using AR software for professional services, especially where invoices tie to matters, projects, retainers, or milestone billing. The cleaner the payment-to-invoice match, the cleaner your partner reporting and forecast.

If you want to see how teams approach this in practice, this resource on automated payment reconciliation is a helpful reference point.

A short walkthrough is often more useful than a feature list:

What better cash application looks like

The end state is straightforward:

- Payments are matched quickly even when references are imperfect

- Collectors see real open items, not noise created by unapplied cash

- Controllers trust AR aging reports

- Leaders get a better view of near-term liquidity

For firms trying to reduce DSO and improve cash flow, this is usually the most underappreciated strategic point.

Integrating Bank Transfers into Your AR Workflow

The strongest bank transfer process doesn't live in treasury alone. It sits inside the full AR workflow, from invoice delivery to payment option selection to posting in the ledger. If those steps are disconnected, finance teams create work for themselves every day.

The fix isn't complicated. It's mostly about system design and discipline.

Start with the client payment experience

If clients have to ask how to pay, search old emails for wiring instructions, or manually re-enter invoice details, your process is already leaking time.

A better setup gives clients one clear route to pay and one clear place to include remittance detail. For professional services firms, that usually means:

- A portal linked directly from the invoice

- Pre-filled payment references

- Bank transfer options presented alongside other accepted methods

- Clear routing for domestic versus international payment instructions

Here, QuickBooks AR automation becomes useful. When payment intent, payment data, and invoice data stay connected, your team stops rebuilding context manually after the fact.

Build around data flow, not staff heroics

The strongest workflows pass information automatically from payment initiation into receivables operations and then into accounting.

That means your system should support:

Workflow point | What to enforce |

|---|---|

Invoice delivery | Include structured payment instructions and a clear reference field |

Payment receipt | Capture payer name, amount, remittance detail, and invoice linkage |

Exception handling | Route only true mismatches to a human reviewer |

Ledger sync | Post matched payments cleanly into the accounting system |

For firms using AR software for professional services, the goal is to keep billing, payment, and posting in one operational loop. If bank transfers arrive in the bank but the invoice status in QuickBooks stays stale, the team loses confidence in the system fast.

What works and what doesn't

What works:

- Standardized payment instructions on every invoice

- Client-facing payment pages that reduce ambiguity

- Webhooks or direct integrations that update statuses quickly

- A small, well-defined exception queue

What doesn't:

- Shared inboxes as the primary remittance process

- Multiple versions of bank instructions in circulation

- Collectors updating notes manually across separate systems

- Waiting until month-end to clean up unapplied cash

If your AR process depends on one experienced staff member knowing how to decode every bank receipt, it isn't a process yet.

A practical visual here is a left-to-right workflow graphic showing invoice issuance, client portal payment, bank receipt, auto-match, and QuickBooks posting. That's the operational chain CFOs want to see.

Achieving Control Over Your Cash Flow

Bank transfer payments are easy to treat as plumbing. That's a mistake. In a professional services firm, they influence when cash becomes usable, how accurately receivables are reported, and how much avoidable work lands on the finance team.

The pattern is consistent. When firms choose the right payment rail for the invoice, understand settlement mechanics, protect against reversibility and fraud, and automate reconciliation, they gain control. Not theoretical control. Practical control you can see in cleaner aging, fewer exceptions, and better weekly forecasting.

This is also where the value of accounts receivable automation becomes concrete. It's not just about sending reminders faster. It's about making sure the payment method, the remittance data, the bank activity, and the ledger all line up with less manual effort. That's how firms reduce DSO and improve cash flow without turning collections into a client experience problem.

For CFOs, Controllers, and firm owners, the goal isn't to master every payment acronym. It's to build an AR operation that produces confidence. Confidence that large invoices are routed through the right rail. Confidence that incoming cash is applied correctly. Confidence that the number on the dashboard reflects reality.

That's the difference between watching receivables and controlling them.

Resolut automates AR for professional services with a focus on consistent follow-through, accurate cash application, and a human approach to client communication. If your team wants tighter control over bank transfer payments without adding more manual work, it's a practical place to start.