Cash Flow to Creditors Formula: A CFO's Guide

Master the cash flow to creditors formula. Learn to calculate, interpret, and use this key metric to monitor liquidity and manage debt servicing effectively.

Your firm closes the month with a healthy profit. Partners feel good about the pipeline. Then payroll hits, a lender payment clears, and the bank balance looks tighter than it should.

That disconnect is common in professional services. Revenue can be earned long before cash arrives. Large invoices sit in review. Retainers get consumed faster than they're replenished. Debt service keeps moving on schedule whether clients pay on time or not.

That's where the cash flow to creditors formula becomes useful. It tells you something the P&L cannot. It shows the net cash moving between your firm and its lenders, and that answer changes how you should think about billing cadence, collections pressure, and whether debt is helping or hurting your position.

Beyond Profitability The Real Story of Your Cash

A consulting, legal, accounting, or agency firm can post solid margins and still feel squeezed. The usual culprit isn't poor work. It's timing.

You deliver work in one month, invoice in the next, and collect later. Meanwhile, your line of credit, term debt, and interest payments run on a different clock. If you only watch net income, you miss the financing reality underneath the business.

That's why I treat cash flow metrics as operating tools, not academic ratios. A firm owner doesn't need another elegant formula. They need to know whether the business is generating enough internal cash to cover lender obligations, or whether lenders are carrying the business for another period.

Profit answers whether the work was priced and delivered well. Cash answers whether the firm stays in control.

For professional services firms, that distinction matters more than it does in many product businesses. Your largest asset is often accounts receivable, not inventory. If receivables drift, borrowing creeps up. Then leadership starts making financing decisions that are really collections problems in disguise.

A good starting point is understanding how net cash flows differ from accounting results. Once you look at the movement of cash instead of reported earnings alone, debt service becomes easier to interpret.

What this looks like in practice

A firm may say, “We paid interest this quarter, so creditors took cash out of the business.”

Maybe. Maybe not.

If the same firm also drew additional debt during the period, creditors may have provided more cash than they received. That changes the conversation. You're no longer just servicing debt. You're using debt to bridge operating timing, fund hiring, or smooth uneven client payments.

That's not automatically bad. But it should be deliberate.

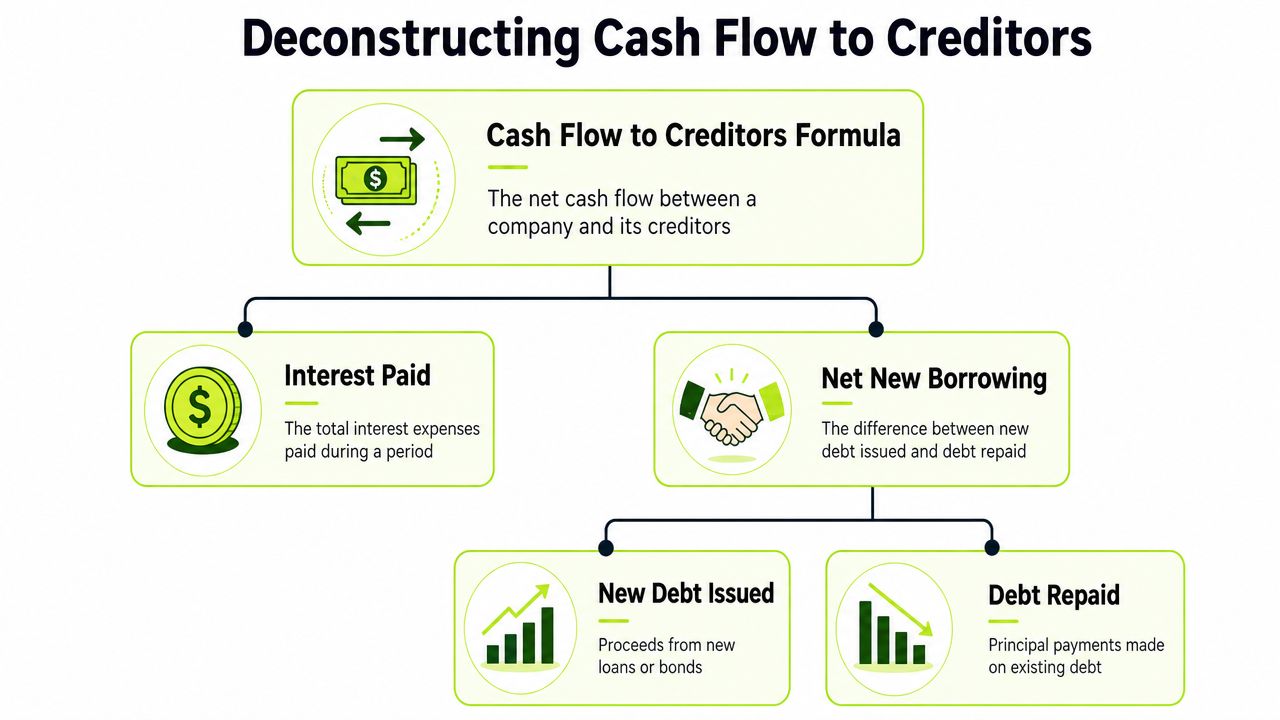

Deconstructing the Cash Flow to Creditors Formula

The formula is simple:

Cash flow to creditors = interest paid minus net new borrowing

That definition matters because it captures the net cash transferred from a firm to its lenders, not just interest expense alone, as outlined in this cash flow to creditors method definition.

The first component is interest paid

This is the straightforward part. It reflects the cash cost of borrowing during the period.

For an operator, interest paid tells you the carrying cost of your debt structure. If that number is manageable and supports growth, fine. If it keeps rising while receivables age and collections slip, the debt is becoming a patch over an operating issue.

The second component is net new borrowing

The metric is often misread at this stage.

Net new borrowing is the change created by new debt issued and debt repaid. If you borrow more than you repay, net new borrowing is positive. If you repay more than you add, net new borrowing turns the other direction.

Think about a personal line of credit. If you pay the bank interest this month but also draw more cash from the line than you repaid in principal, the bank still sent net cash your way. The same logic applies here.

Why the subtraction matters

Because the formula subtracts net new borrowing, the result tells you whether lenders received net cash from the business or supplied it.

A few practical interpretations help:

- Positive result: your firm sent net cash to creditors. You paid them more than they provided.

- Negative result: creditors supplied net cash to the business. Borrowing exceeded interest paid.

- Near zero result: financing was relatively balanced for the period, though the underlying mix still matters.

Practical rule: Never review interest expense by itself when you're deciding whether debt is under control. Pair it with debt movement, or you'll draw the wrong conclusion.

For professional services firms, this matters because debt often compensates for client payment timing. If your AR software for professional services isn't giving you clean visibility into invoice aging, you can mistake a billing-cycle problem for a capital-structure decision.

Calculating and Interpreting the Results

The mechanics are simple, but the interpretation needs discipline.

A video walkthrough can help if you want to see the logic in motion.

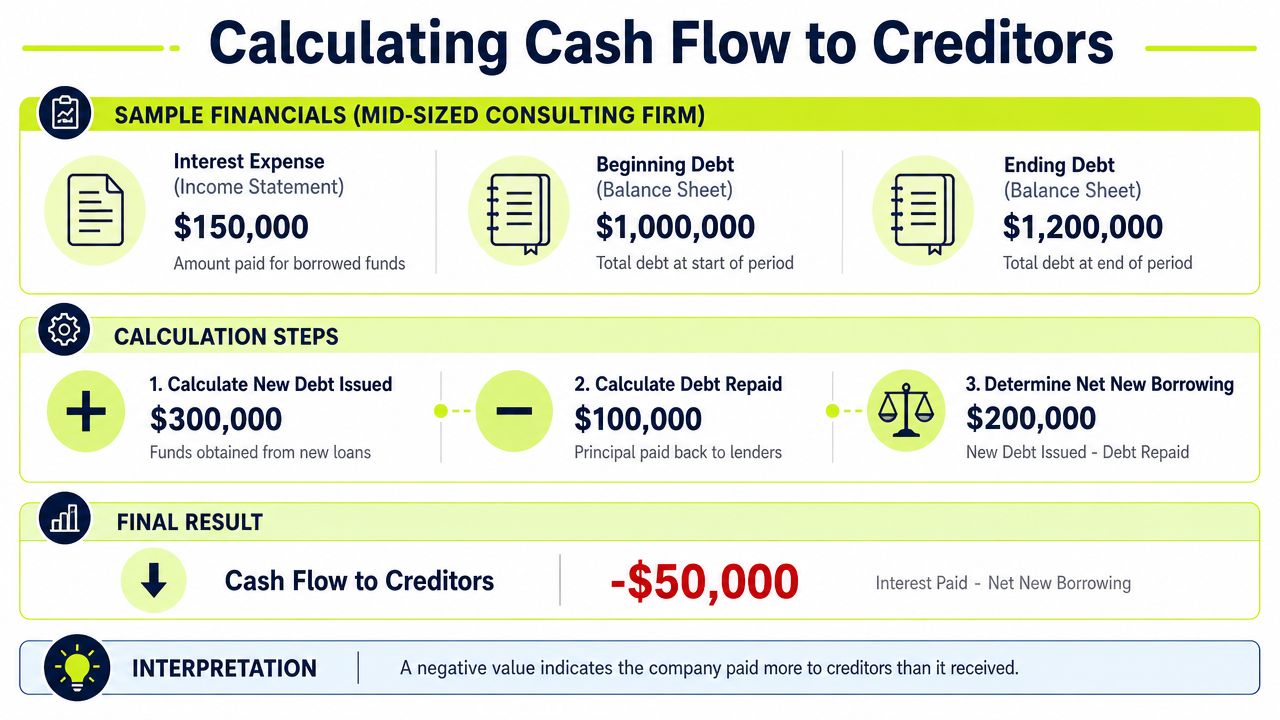

A clean worked example

One instructional example shows $18,600 in interest expense and $27,800 in net new borrowing, producing -$9,200 of cash flow to creditors using the formula Interest Paid minus Net New Borrowing, which indicates a net cash inflow from creditors. The same example shows why a modest change in debt balances can dominate the final number, as explained in this instructional finance video on cash flow to creditors.

That's the key lesson. The debt movement often matters more than the interest line.

How to calculate it inside your firm

Use a simple sequence:

- Pull interest paid for the period.

- Review debt balances from the beginning and end of the same period.

- Determine whether the firm took on more debt than it repaid.

- Subtract net new borrowing from interest paid.

If your accounting stack includes QuickBooks, teams often run into a practical limitation. The raw data exists, but it may not be organized for decision-making. You still need someone to distinguish normal debt service from refinancing activity, partner distributions funded by debt, or temporary working capital draws.

What the sign tells you

A positive result means cash moved out to creditors on a net basis. In plain English, the business paid lenders more than it raised from them during the period.

A negative result means lenders effectively financed part of the business during that period. That can be sensible if you used debt to fund a deliberate expansion, smooth seasonal cash timing, or bridge long enterprise billing cycles.

What doesn't work is treating a negative result as harmless when the underlying issue is weak invoicing discipline, slow follow-up, or poor cash application. If collections are inconsistent, debt starts masking operational drag.

A negative number isn't automatically a warning sign. It becomes one when borrowing is covering avoidable delays in billing and payment collection.

A fast interpretation grid

Result | What it means | CFO question |

|---|---|---|

Positive | Net cash went to lenders | Are we paying debt down at the right pace? |

Negative | Lenders supplied net cash | Is this strategic borrowing or a workaround for slow collections? |

Volatile | Debt movement is driving swings | What changed in financing policy or payment timing? |

For firms trying to reduce DSO, improve cash flow, or evaluate AI AR automation, this metric is a useful pressure test. If debt use rises while receivables age, the finance issue probably starts upstream in billing and collections.

A Key Piece of the Full Cash Flow Picture

Cash flow to creditors only becomes fully useful when you place it next to the rest of the financing picture.

The core identity in financial statement analysis is cash flow from assets = cash flow to creditors + cash flow to stockholders, as shown in this finance teaching reference on cash flow identities. That identity helps isolate financing decisions from operating performance.

Why this matters for a services firm

In a professional services business, leaders often blur three separate questions:

- Are we producing cash from operations?

- Are we sending cash to lenders and owners?

- Are we relying on financing to offset weak working capital control?

Those are different issues. The identity forces you to separate them.

If operations are solid but cash is still tight, look at financing flows and owner distributions. If operations are weak, then debt and equity decisions may only be delaying a fundamental fix. That usually means billing speed, collection consistency, and better oversight of receivables.

A useful companion lens is working capital management for finance leaders. For most firms in the professional services range, that's where the day-to-day cash pressure shows up.

A better management conversation

When I review this with owners, I want one clear answer: did the business generate enough cash on its own, or did financing choices carry the period?

That framing improves decision quality. It stops teams from celebrating profitability while ignoring liquidity. It also stops them from blaming debt when the actual issue is that invoices went out late, disputes sat unresolved, or collectors lacked a consistent process.

Common Pitfalls and Strategic Adjustments

The formula is clean. Real books usually aren't.

Where teams get the answer wrong

The first problem is mixing unlike debt items. A revolving line used for short-term working capital behaves differently from a longer-term expansion loan. If you lump everything together without context, the number may be technically correct but strategically useless.

The second problem is using accrual figures when the question is about cash movement. Interest expense on the income statement isn't always the same as cash interest paid in the period. If the books include timing differences, the metric needs judgment.

The third problem is ignoring why debt changed. A debt increase tied to a controlled office build-out is different from a debt increase caused by slow-paying clients and uneven follow-up.

Practical adjustments that help

- Separate debt by purpose: Keep working capital lines apart from term loans. You'll get a sharper read on whether borrowing supports operations or growth.

- Check the cash reality: Reconcile book interest to cash interest paid when timing is messy.

- Review billing and AR before blaming debt levels: In many firms, debt pressure starts with delayed invoices, weak collections notes, or unresolved client deductions.

- Clean up reporting cadence: Monthly review is usually more useful than waiting for quarterly surprises.

If your systems are fragmented, modern cloud accounting design can make this analysis much easier. This strategic guide to cloud accounting is a practical resource for finance teams trying to tighten reporting visibility without adding unnecessary complexity.

The formula doesn't fail in the real world. Reporting discipline does.

What doesn't work

What doesn't work is treating debt as a permanent substitute for operating cash control. It also doesn't work to push principal down aggressively just because the firm had one strong month. In professional services, collections timing can change quickly if a few major invoices stall.

The better move is to pair debt analysis with client billing cycles, retention terms, payment methods, and follow-up workflows. That gives you a financing strategy grounded in reality.

Putting This Metric to Work in Your Firm

Use the cash flow to creditors formula as a decision signal, not just a report line.

If the result is consistently positive, ask whether you're pushing too much cash toward debt while starving the business of flexibility. You may want to revisit repayment pace, refinance terms, or hold more cash during periods of long client approval cycles.

If the result is consistently negative, don't panic. Ask whether the borrowing is supporting deliberate growth or compensating for avoidable friction in receivables. That's a very different management problem.

Where operations change the answer

For professional services firms, the fastest path to more financing control usually isn't another loan. It's better AR execution.

That means:

- Faster invoice release: Don't let completed work wait for administrative cleanup.

- Consistent follow-up: Collections should run on process, not memory.

- Cleaner cash application: Unapplied cash hides the true receivables picture.

- Better client payment options: Friction at payment time slows everything downstream.

Here, accounts receivable automation, AI AR automation, and QuickBooks AR automation start to matter. Better AR software for professional services can help reduce DSO, improve cash flow, and give you more internally generated cash to service debt on your terms.

A stronger forecasting rhythm also helps. If you want to connect debt decisions to upcoming cash needs, this guide to cash flow forecasting for finance teams is worth reviewing.

The goal isn't zero debt. It's optionality. When receivables move cleanly and cash arrives predictably, you can decide when to borrow, when to pay down debt, and when to keep liquidity on hand.

Resolut automates AR for professional services, helping finance teams stay consistent, accurate, and human. If you want tighter collections workflows, faster payment visibility, and better control over cash timing, Resolut is built for that job.