How to Send a Certified Mail USPS: A CFO's Guide

Learn how to send a Certified Mail USPS as a strategic tool. This guide for finance leaders covers costs, online options, and AR integration to reduce DSO.

An invoice crosses 90 days. Your team has already sent the reminder cadence, escalated the tone, called the client, and documented every promise to pay. Then the replies stop.

That's the point where many firms drift into improvisation. Someone drafts a tougher email. Someone else suggests legal. Days pass. Cash sits in limbo.

A better approach is to treat escalation as a controlled finance process. If you're figuring out how to send a certified mail USPS item, the question isn't really about mail. It's about proof, timing, and influence inside a modern collections system.

When Digital AR Automation Needs a Physical Backstop

Digital workflows should handle most collections activity. Email, payment links, SMS, call tasks, and workflow rules belong inside accounts receivable automation. If you need a refresher on where that discipline fits, this overview of AR automation is useful.

But automation has a limit. A client who ignores six emails may still react to a formal envelope that requires attention. That's not old-fashioned. That's signal control.

Use Certified Mail as an escalation trigger

I wouldn't use Certified Mail for routine invoice reminders. That's expensive in labor and too blunt for normal AR. I would use it when a receivable has moved from “slow payer” to “documentation risk.”

That usually means one of these conditions is true:

- The balance is disputed and you need a clear record of what was sent.

- The client has gone silent after repeated digital outreach.

- Your firm is approaching legal escalation and wants a defensible communication trail.

- A contract notice matters and ordinary email no longer feels sufficient.

Practical rule: Certified Mail is strongest when it marks a deliberate stage change in your collections workflow.

USPS frames Certified Mail as an extra service used when evidence of mailing matters, not as a universal add-on for every mailing class, as outlined in the USPS Certified Mail basics. That matters for finance leaders. You're not buying postage. You're buying documented escalation.

Don't confuse formality with strategy

Most firms overuse either informality or force. They either keep nudging by email long after the debtor has disengaged, or they jump too quickly to attorney language that damages the client relationship.

Certified Mail sits in the middle. It creates a harder edge without immediately handing the file to counsel.

That's why I see it as part of a larger control framework alongside AI AR automation. Your digital system should decide when a client account graduates to formal notice. The mailing itself is just the execution layer.

If your current approval flow for formal notices still runs through PDFs, attachments, and manual signatures, it's worth reviewing tools that modernize that part of the stack. This roundup of SignWith offers Adobe Sign alternatives is useful if your team is standardizing signature workflows around notices, acknowledgments, and payment plans.

The best answer is sometimes not Certified Mail

Finance judgment matters here. The best certified-mail answer is sometimes not to send certified mail at all. If your legal or audit requirement can be satisfied by a lower-friction proof method, use that instead.

For high-volume disputes, billing notices, and collections workflows, manual post-office steps can become operationally expensive. CFOs should reserve Certified Mail for the moments when physical, trackable delivery changes the risk profile.

That discipline improves cash flow more than theatrics do.

Choosing Your Proof Certified Mail Service Options

The right service level depends on what you need to prove. Don't let staff decide that ad hoc. Set a policy.

The basic economics are clear. As of January 2024, the Certified Mail fee was $4.40 on top of postage, and adding a physical Return Receipt cost $3.65, bringing a single letter to nearly $9 all-in in a common example, according to Quadient's Certified Mail guide.

Match the proof to the risk

For finance teams, there are three practical buckets.

- Standard Certified Mail Use this when proof of mailing and traceability are enough. Final reminders, contract notices, and documented demand letters often fit here.

- Certified Mail with Return Receipt Use this when signature evidence matters more than simple tracking. This is the stronger choice for disputes likely to become legal exhibits.

- Restricted Delivery Use this when you need tighter control over who may accept the item. This is narrower and should be reserved for specific risk cases, not everyday collections.

If the notice will end up in a file reviewed by outside counsel, choose the proof level before you send it. Retrofitting evidence later usually fails.

USPS Certified Mail Service Comparison

Service Level | Added Cost (Approx.) | Proof Provided | Best For |

|---|---|---|---|

Standard Certified Mail | $4.40 plus postage | Mailing receipt and tracking history | Final reminders, standard formal notices |

Certified Mail with physical Return Receipt | $4.40 plus postage and $3.65 for paper Return Receipt | Mailing proof plus physical signature record | Higher-risk disputes, stronger evidentiary files |

Restricted Delivery | Higher than standard options | Tighter delivery control | Sensitive notices where recipient control matters |

The table isn't about mailroom preferences. It's about evidence sufficiency.

My recommendation for policy design

Most professional services firms should keep it simple:

- Standard Certified Mail for late-stage demand notices where you need a documented escalation step.

- Return Receipt only when legal, contractual, or internal counsel standards justify the extra cost and handling.

- Restricted Delivery only by exception, with controller or CFO approval.

That policy protects margin. It also keeps your team from treating every difficult invoice like a courtroom drama.

A common mistake is paying for maximum proof on low-risk files and then skipping it on the accounts that threaten collections, write-offs, or partner disputes.

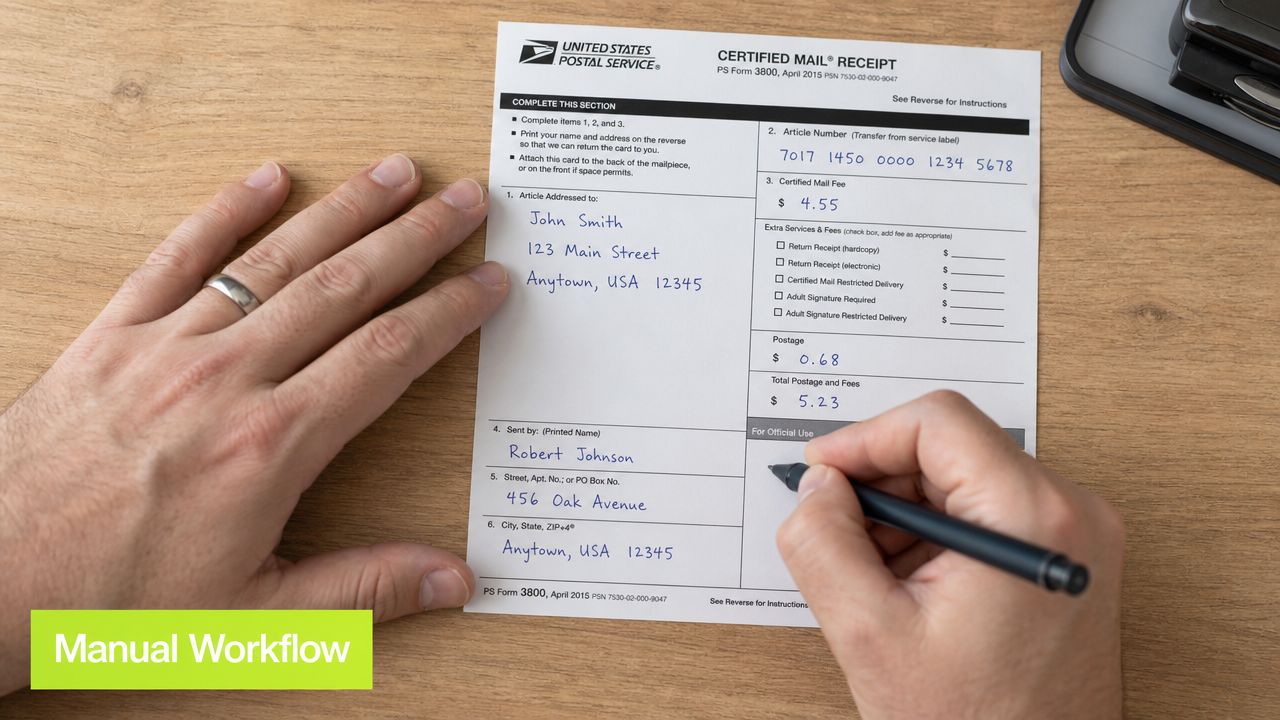

Executing the In-Person Workflow for Maximum Control

If you're sending Certified Mail manually, build it like an internal control. Don't let it become an office errand.

USPS structures the process around Form 3800. The sender addresses the mailpiece, attaches the form to a First-Class Mail or Priority Mail item, pays postage plus the Certified Mail fee, and receives a mailing receipt with a unique tracking number, as described in the USPS PostalPro Certified Mail guidebook.

Build the SOP, not just the envelope

Your finance team needs a repeatable checklist. I'd require these steps every time:

- Confirm legal name and address. Pull them from the signed contract, approved customer master, or counsel instruction. Don't trust an email signature block.

- Print the final notice from the controlled template. No ad hoc edits after approval.

- Complete Form 3800 carefully. The value is in the documentation trail, so sloppiness defeats the point.

- Use the correct underlying class. Certified Mail works with First-Class Mail or Priority Mail.

- Hand it to a postal clerk. Don't shortcut the acceptance step.

- Retain the receipt immediately. This is evidence, not scrap paper.

What the receipt means operationally

The stamped mailing receipt is the trigger artifact. Once the clerk accepts the item and you have the tracking number, your team should log the event in the client record.

At minimum, store:

- the letter PDF

- approval record

- mailing date

- USPS tracking number

- who sent it

- any follow-up task tied to delivery status

That's what turns mailing into a controllable event inside your AR software for professional services.

A quick visual walkthrough helps if you're training staff across offices:

Where teams usually lose control

The common failure isn't filling out Form 3800. It's everything around it.

One staff member uses the wrong address. Another forgets to upload the receipt. A partner asks for status two weeks later and nobody can locate the tracking record. At that point, the firm has spent money and time without improving its legal posture.

Treat every Certified Mail item like a mini closing document. If the evidence isn't filed, the step didn't happen.

If you want to know how to send a certified mail USPS item correctly, that's the answer. Follow the USPS procedure, then wrap it in finance-grade documentation discipline.

Scaling the Process with Online Certified Mail Services

Manual Certified Mail works. It doesn't scale well.

If your firm sends occasional formal notices, the post office workflow is fine. If you manage recurring disputes, multi-office approvals, or a growing collections queue, manual handling becomes expensive in the worst way. Not because of postage, but because skilled staff are doing low-value administrative work.

What online services actually change

Online Certified Mail providers replace the physical trip with a digital workflow. Your team uploads the document, enters recipient details, selects service options, and the provider handles print, fold, stuffing, postage, and mailing.

That matters because it moves formal notice activity back into the same control environment as your other finance systems. The event becomes searchable, timestamped, and easier to supervise.

For firms already pursuing QuickBooks AR automation, this is the missing bridge. You can automate the trigger logic digitally, then execute the physical notice without asking a collections manager to leave the office.

Why this is better for CFOs

The gain isn't novelty. It's operational consistency.

An online workflow usually gives you:

- Centralized records so mailed notices don't live in desk drawers

- Cleaner approvals because templates and service levels can be standardized

- Faster execution when a file needs same-day escalation

- Better auditability because the proof stays in a digital system

That's exactly how AI AR automation should work in practice. Let the system manage timing, segmentation, and escalation rules. Let human staff review exceptions. Let the mailing process execute as a documented service, not a manual expedition.

My policy view on online versus manual

For a small number of sensitive notices, in-person mailing still has value. It forces deliberate handling, and some firms prefer that tactile control.

For any firm sending formal notices with frequency, online execution is the better operating model. It shortens cycle time, reduces staff interruption, and makes oversight easier.

Certified Mail should feel as operationally clean as sending an approved invoice batch. If it doesn't, your process is too manual.

This is the broader lesson for collections leaders trying to improve cash flow. Don't isolate formal notice activity from your AR system. Integrate it. The stronger your orchestration, the easier it becomes to escalate a stubborn account without losing documentation, consistency, or management visibility.

Common Mistakes and Recordkeeping for the Audit Trail

Most firms don't fail at sending the letter. They fail at proving what happened afterward.

The first misconception is the biggest one. Certified Mail doesn't guarantee receipt by a specific person. USPS documentation supports a delivery attempt or delivery verification, not a universal promise that the intended individual personally received it. It also doesn't speed delivery on its own. The underlying mail class controls transport, commonly 2 to 5 business days for First-Class Mail in business guidance, as noted in Quadient Direct's step-by-step guide.

Four mistakes I see repeatedly

- Mistaking mailing proof for legal certainty A tracking number helps. It doesn't cure a weak process, a bad address, or an unclear letter.

- Failing to preserve the original receipt If the stamped acceptance receipt disappears, your evidence file is weaker than it should be.

- Using inconsistent service choices One collector uses standard Certified Mail, another orders extra services, and nobody can explain why.

- Keeping records outside the client file Screenshots in email inboxes and paper receipts in desk folders won't survive turnover or audit review.

Build a real audit file

Finance leaders should require a standard package for every formal notice:

Required Record | Why It Matters |

|---|---|

Approved letter PDF | Shows exactly what was sent |

Mailing receipt | Proves USPS acceptance |

Tracking number log | Connects the event to delivery status |

Delivery confirmation or return receipt | Strengthens the timeline |

Internal approval note | Shows authorized escalation |

A file like that stands up much better in disputes, audits, and partner reviews.

If your team also handles litigation support, contract exhibits, or large notice sets, document control becomes even more important. This practical Adobe Bates numbering guide is useful when you need consistent pagination and reference logic across formal records.

Recordkeeping should live inside controls

If your collections team can send a formal notice without creating a permanent digital record, the control environment is incomplete. That's why I'd tie Certified Mail procedures to your broader accounts receivable internal controls.

Here's the standard I'd hold:

- One system of record for the client communication file

- One naming convention for mailed notices and proofs

- One owner responsible for confirming documentation is complete

- One review point before legal escalation

That discipline does more to reduce DSO than dramatic collection language ever will. Clients pay faster when they know your process is organized, consistent, and serious.

Integrating Formal Notices into Your Financial Operations

Certified Mail belongs in the escalation ladder, not in the administrative basement.

The sequence should be deliberate. Start with digital reminders and payment enablement. Escalate with stronger written communication. Use Certified Mail when the account requires formal proof and a documented pivot in posture. If the matter continues, your file is already organized for counsel or executive review.

Treat escalation as a finance system

A mature collections operation doesn't ask, “Can someone run this to the post office?” It asks:

- What event triggered formal notice?

- What level of proof does this file require?

- Where is the evidence stored?

- What happens next if the client still doesn't respond?

That's the difference between ad hoc collections and controlled financial operations.

For firms dealing with disputes and tougher past-due files, a formal notice often sits one step before legal demand. This guide to a legal demand letter for payment is a useful reference when you need to distinguish ordinary escalation from a more serious legal communication.

My closing view

If you're searching for how to send a certified mail USPS notice, learn the mechanics once and codify them. Then stop thinking of it as a mailing task.

Think of it as a financial instrument. It creates evidence. It signals seriousness. It supports collections discipline. And when it's integrated into your operating rhythm, it helps protect revenue without turning every late invoice into a legal event.

That's what modern AR should do. Use automation where speed matters. Use formal notice where proof matters. Control both.

Resolut automates AR for professional services. It helps finance teams run consistent collections, orchestrate escalations, and keep the record clean from first reminder to final notice. If you want a more controlled way to improve cash flow without sacrificing the human side of client relationships, Resolut is built for that.