What Is Day Sales Outstanding? a Guide for Firm Owners

Learn what is Day Sales Outstanding (DSO), how to calculate it, and how to reduce DSO to improve cash flow. A guide for CFOs and professional services firms.

Revenue can look healthy while cash feels tight. A professional services firm closes projects, sends invoices, books income, and still finds itself watching payroll timing, partner draws, and vendor payments more closely than it wants to.

That gap is where most owners start asking a practical question: what is Day Sales Outstanding, and why does it matter so much to cash flow?

The short answer is simple. Day Sales Outstanding, or DSO, tells you how long it takes to turn credit sales into cash. For a firm that bills after work is performed, that number says a lot about operational discipline. It tells you whether billing is prompt, whether clients understand your terms, whether follow-up is happening on time, and whether cash is getting stuck between “earned” and “collected.”

In a services business, DSO isn't just an accounting metric. It's a control metric. If it drifts up, working capital gets trapped in receivables. If it comes down in a sustainable way, you gain room to hire, invest, and operate without constant pressure.

Beyond the Balance Sheet What Day Sales Outstanding Reveals

A firm can finish a strong month, post solid revenue, and still hesitate on hiring because cash has not arrived. That tension is common in professional services, where labor is paid now and collections happen later.

DSO helps explain that gap.

Used well, it gives owners and finance leaders an early read on whether cash will keep pace with delivery. It shows how much money is tied up after the work is done, the invoice is sent, and the firm is waiting to get paid. In that sense, DSO is less about reporting the past and more about judging how reliably the business converts completed work into operating cash.

What DSO is really telling you

Days Sales Outstanding measures the average time it takes to collect on credit sales. The basic math comes later. Here, the practical point is what the number exposes inside the business.

A rising DSO usually means cash is slowing somewhere between project delivery and payment receipt. Sometimes the issue starts before the invoice ever goes out. Time approval drags, project managers hold billing, or billing data arrives incomplete. In other cases, the invoice is correct but the client payment process is slow, the follow-up cadence is inconsistent, or payment terms are looser in practice than they looked in the contract.

That is why finance teams often pair DSO with related views such as a days sales uncollected formula, especially when they want a closer look at what remains outstanding over a defined period.

In plain terms, DSO answers a question owners care about: how long does earned revenue stay unavailable for payroll, taxes, partner distributions, and growth spending?

A profitable services firm can still feel squeezed if cash conversion lags behind delivery.

Why owners should care before month-end

DSO also surfaces trade-offs. Pushing invoices out faster usually improves cash timing, but billing too early or without clean support can create disputes that slow payment even more. Tightening collections can shorten the cycle, but a poor approach can strain a client relationship that still matters commercially. Good operators manage both sides. Speed and accuracy. Discipline and context.

A rising number usually points to one of a few operating issues:

- Billing delay: Time capture, approvals, or closeout steps are holding invoices back.

- Term slippage: Agreed payment terms are not matching actual client behavior.

- Collections inconsistency: Follow-up depends on individual effort instead of a set process.

- Payment friction: The client is willing to pay, but the payment path is harder than it should be.

A controller sees those issues in receivables aging and weekly cash forecasts. An owner feels them in tighter decision-making, less room for error, and more time spent managing timing instead of running the firm.

That is what DSO reveals beyond the balance sheet. It shows whether your operating model is helping cash arrive on time, or letting receivables absorb it.

Calculating and Decoding Your Day Sales Outstanding

A DSO calculation takes a minute. Reading it well is what improves cash control.

The standard formula

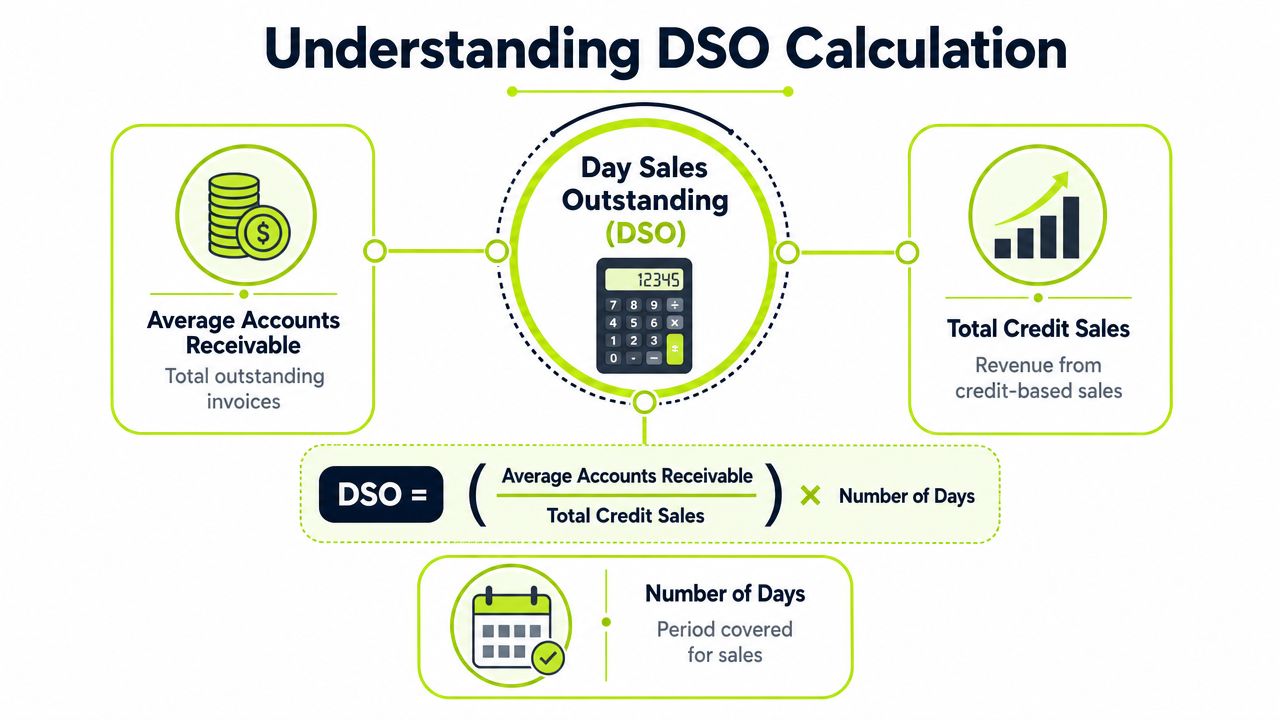

DSO = (Average Accounts Receivable / Net Credit Sales) × Number of Days

The formula shows how many days, on average, receivables stay outstanding before they turn into cash. Use net credit sales, not total sales, because cash sales do not create a collection cycle. That keeps the metric focused on billing, collections, and payment timing.

If you want a closely related framing, this guide to the Days Sales Uncollected formula is useful because many finance teams use the terms interchangeably in practice.

A simple worked example

Use a 30-day period. If average accounts receivable are $1,000,000 and net credit sales are $2,000,000, DSO is 15 days.

That result gives management a practical read on cash timing. On average, the firm collects its credit sales in 15 days during that period.

For an owner, that number matters because it sets the pace of available cash. A 15-day DSO supports faster reinvestment, more room in the forecast, and less reliance on a line of credit. A 45-day DSO creates a different operating posture, even if revenue looks strong on paper.

How to read the number

For a professional services firm, DSO should translate into a plain operating conclusion:

DSO reading | What it means in practice |

|---|---|

Lower DSO | Cash is arriving faster, which gives the firm more flexibility on payroll, hiring, and vendor payments |

Higher DSO | More cash is sitting in receivables, which tightens liquidity and reduces room for error |

Stable but elevated DSO | The issue may be built into client terms, billing cadence, approval steps, or client mix |

Volatile DSO | Timing effects, uneven project billing, or dependence on a few large invoices may be distorting the picture |

The key is to ask why the number moved. A lower DSO is usually a sign of cleaner invoicing, tighter follow-up, or easier payment execution. A higher DSO can point to delayed billing, weak collection discipline, or clients stretching terms beyond what was agreed.

That is why I treat DSO as a control metric, not just a scorecard. If it rises, the cash forecast gets weaker. If it improves for the right reasons, the business gets more optionality.

When the simple formula isn't enough

The standard formula works well when billing is steady. It gets less reliable when a services firm has lumpy project work, milestone invoices, or sharp swings at quarter end.

In those cases, finance teams often use a countback approach to get a clearer view of actual collection speed across uneven billing periods. The benefit is a more realistic reading of cash conversion. The trade-off is added complexity, which means the metric can be harder for non-finance leaders to calculate quickly and explain consistently.

For professional services, that trade-off is usually worth managing. A cleaner measure helps separate a true collections problem from a billing pattern issue, and that leads to better decisions on staffing, client terms, and short-term cash planning.

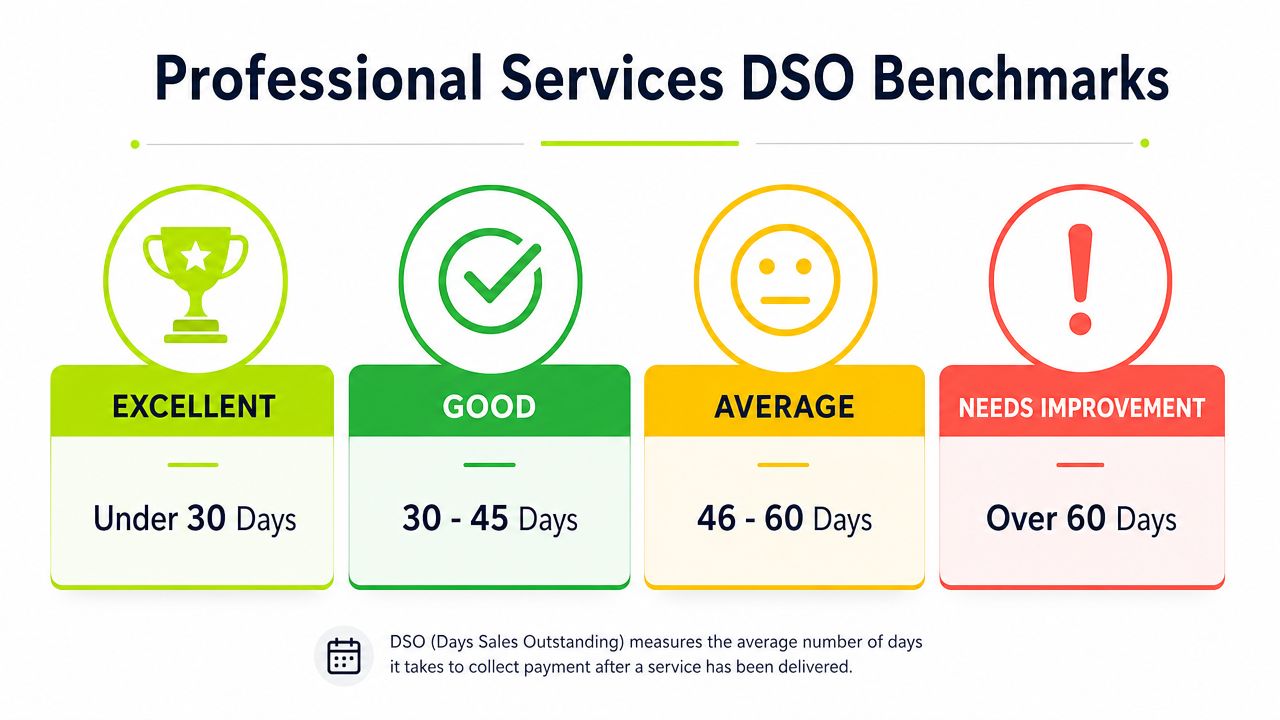

What Is a Good DSO for Professional Services

A services firm can look profitable on paper and still feel cash pressure every month. The usual reason is not revenue. It is the gap between finishing the work, sending the invoice, and getting paid.

That is why a good DSO matters. It does more than describe receivables performance. It shows how much control the firm has over its cash conversion cycle.

What “good” actually means

For professional services, a good DSO is one that fits your billing model, client base, and payment terms, while still giving the business enough cash predictability to operate without strain.

A firm billing fixed monthly retainers can usually hold a lower DSO than a firm billing large project milestones with complex client approvals. A boutique advisory practice serving founder-led companies may collect faster than an enterprise-focused consultancy that has procurement steps, legal review, and multiple approvers. The number has to be judged in context.

I do not treat “good” as a generic benchmark to chase. I treat it as a target range the firm can defend. If collections slow, leadership should know whether the cause is client mix, billing design, approval friction, or follow-up discipline.

If you want a second way to evaluate collection speed, how to find average collection period gives a related lens that can help validate what DSO is showing.

A practical standard for services firms

The better question is not, “Is our DSO low enough?” It is, “Does our DSO support payroll, tax obligations, partner draws, and hiring plans without constant cash management?”

That shifts the conversation from reporting to control.

A good DSO in professional services usually has three characteristics:

- It is predictable: Finance can forecast receipts with reasonable confidence.

- It reflects disciplined execution: Invoices go out on time, with the right detail, to the right approver.

- It does not depend on damaging concessions: The firm is not accelerating cash by discounting away margin or training clients to pay only after repeated escalation.

Those trade-offs matter. I would rather see a slightly higher DSO with firm pricing and orderly collections than a lower DSO achieved through fee write-downs, awkward exceptions, or partner-by-partner improvisation.

What pushes “good” out of reach

In services businesses, DSO often rises because operations and billing are out of sync.

Common examples show up fast:

Operational issue | Cash flow effect |

|---|---|

Time entry or project sign-off is late | Invoices go out days or weeks after work is complete |

Billing support is inconsistent across partners or managers | Collection timing becomes uneven and hard to forecast |

The client contact is not the actual approver | Invoices sit untouched while teams sort out ownership |

Invoice detail does not match client requirements | Disputes slow payment and increase follow-up work |

None of those problems starts in collections. They start upstream. That is why DSO is useful as a forward-looking operating signal. When it drifts up, future cash gets tighter, and finance loses room to plan.

The target is control, not optics

A firm with a stable, explainable DSO usually has tighter billing habits and fewer surprises in the cash forecast. A firm with a “good-looking” number that no one can explain is harder to manage.

The strongest standard is simple. Good DSO gives the business room to invest, confidence in near-term cash, and fewer collection emergencies. In professional services, that comes from coordinated billing and follow-up, not from watching a benchmark in isolation.

The Limitations of Relying on DSO Alone

DSO is useful. It isn't complete.

Averages hide structure. One large overdue invoice can pull the number up and make a decent portfolio look worse than it is. The opposite can also happen. A few large current invoices can make the average look fine while a long tail of neglected smaller balances keeps aging in the background.

Where DSO can mislead

A low DSO can look healthy while masking margin leakage. If the firm relies on aggressive concessions, awkward exceptions, or reactive discounts just to accelerate payment, collections may improve while economics worsen.

A stable DSO can also hide operational drag. If one group bills early and another bills late, the average may look acceptable even though parts of the business are routinely slowing cash conversion.

DSO should start the conversation, not end it.

What to review alongside it

If I'm evaluating receivables quality, I don't stop at DSO. I also want to see:

- AR aging: Which balances are current, drifting, or already problematic

- Cash flow forecast: Whether projected receipts line up with obligations

- Invoice dispute patterns: Whether payment delays start with billing accuracy

- Client concentration: Whether a small number of accounts dominate collection risk

That combination tells a much better story than a single metric.

The trade-off leaders often miss

The pitfall is trying to force DSO down in a way that distorts the business. Tightening too hard can strain client relationships. Staying too loose can starve the firm of working capital. Good finance leadership is balancing those two pressures without losing control of either one.

In that sense, DSO is less like a final answer and more like an instrument reading. It tells you where to investigate.

Four Levers to Reduce DSO and Improve Cash Flow

A services firm can finish the work, send the invoice, and still miss payroll timing because cash lands two or three weeks later than expected. That gap usually comes from process drift across delivery, billing, collections, and payment, not from one isolated AR mistake.

The firms that bring DSO down consistently treat it as an operating discipline. Atradius makes a similar point in its discussion of the hidden cost of DSO, tying results to timely invoicing, credit control, collection workflows, and the trade-off between cash protection and customer experience. In professional services, that trade-off matters. Push too hard and you create friction with good clients. Stay too loose and working capital disappears into receivables.

If you want a related view of collection timing, this guide on days in accounts receivable is a useful companion.

Lever one Invoice integrity and timing

The first lever is simple. Bill fast, and bill correctly.

In services businesses, the invoice often arrives after weeks of work that the client experienced through calls, deliverables, and emails, not through formal billing checkpoints. If the invoice shows up late or lands with missing support, the client has a reason to pause, reroute, or dispute it. Cash slows immediately.

Two controls make the biggest difference:

- Send invoices as close as possible to service delivery or milestone completion: Delay between work and billing weakens urgency and creates room for internal approval lag on the client side.

- Check every submission detail before release: Billing entity, approver, PO number, scope references, tax treatment, and backup documents need to be right the first time.

I have seen many firms call it a collections issue when the primary failure happened upstream in billing.

Lever two Contract and term clarity

Terms on paper do not guarantee payment speed. Operational clarity does.

A strong engagement letter should define more than due dates. It should spell out billing triggers, who approves invoices, where invoices must be submitted, what documentation is required, and how disputes get resolved. Without that detail, the finance team ends up negotiating process after the invoice is already outstanding.

A short pre-engagement review helps prevent that drift. It gives delivery, finance, and the client a shared picture of how work converts to cash.

Control point | Why it reduces DSO |

|---|---|

Clear billing milestones | Limits surprise and invoice pushback |

Named invoice approver | Reduces routing delays inside the client account |

Defined submission method | Cuts avoidable admin back-and-forth |

Confirmed payment expectations | Keeps delivery and finance aligned |

This is also where system fit matters. As firms grow, weak handoffs between project delivery and accounting create billing lag. Teams that need tighter control often choose ERP accounting software when spreadsheets and disconnected tools stop supporting consistent execution.

Lever three Systematic collections cadence

Collections need a defined rhythm. Otherwise follow-up depends on who remembers, who is busiest, or which client speaks up first.

A good cadence starts before the due date, continues on the due date, and escalates in a controlled way after the due date. That structure protects cash flow because it catches issues while the invoice is still recoverable without drama. It also gives account leaders clear rules for when to step in.

The right cadence is not identical for every client. Strategic accounts may require partner involvement and more customized communication. Smaller recurring accounts often respond well to precise, professional reminders sent on schedule.

Consistency usually outperforms intensity.

Lever four Frictionless payment experience

Payment delay is often administrative, not intentional. A client may approve the invoice and still pay late because the payment path is clumsy.

Reduce that friction wherever possible. Make invoices easy to read. Include correct remittance details. Offer practical digital payment options. Give clients a clear route for questions before they become excuses for delay.

That is why accounts receivable automation, AI AR automation, and better AR software for professional services matter in practice. They improve payment speed by reducing handoff errors, missed reminders, and avoidable effort across the invoice-to-cash cycle.

The payoff is broader than a lower DSO figure. You get more predictable cash receipts, less staff time spent chasing status, and fewer client conversations that start with preventable billing confusion.

Automating AR to Systematically Lower Your DSO

Once the process is defined, automation is what makes it reliable. Without it, even strong policies decay under workload, staff changes, and month-end pressure.

Here's what good AR orchestration looks like in practice.

What automation should actually handle

The best systems don't just send reminders. They support the full collection sequence:

- Invoice delivery: Sending invoices on time, to the right contact, with the right attachments

- Follow-up cadence: Triggering reminders and escalations consistently

- Payment capture: Giving clients a simple path to pay

- Visibility: Showing finance leaders which invoices are drifting and why

For firms already running their books in QuickBooks, QuickBooks AR automation is often the practical entry point because it reduces manual chasing without forcing a full finance system overhaul.

Where AI helps and where it doesn't

I'm cautious about overpromising on AI in finance operations. The useful application is not “replace judgment.” It's prioritize effort and keep communication consistent.

That means AI AR automation can help identify which invoices need attention, which accounts may require escalation, and which communication style fits the account history. Human review still matters, especially with strategic clients, disputed work, or unusual approvals.

Used properly, automation protects relationships because the system handles routine follow-up while the finance team focuses on exceptions that need judgment.

For firms evaluating their wider back-office stack, it also helps to review how billing and finance systems connect upstream. This overview of how to choose ERP accounting software is a useful reference if you're thinking beyond point solutions and looking at process integration across accounting and operations.

Orchestration matters more than isolated tools

A disconnected stack creates its own delay. One tool generates invoices, another sends reminders, a third records payment status, and someone in finance manually updates the rest. That setup usually creates lag, duplicate effort, and inconsistent client communication.

An orchestration platform brings those actions into sequence. In that context, Resolut is one example of a system built for AR automation across credit workflows, billing, outreach, payment options, and cash application. That matters because reducing DSO usually requires coordination, not just reminder emails.

A short product walkthrough gives a clearer sense of that operating model:

For a services firm, the goal isn't to sound more forceful. It's to make the process more dependable. That's how automation improves cash flow without turning collections into a client-service problem.

From Metric to Mandate Gaining Control Over Cash Flow

If you're asking what is Day Sales Outstanding, you're really asking how much control your firm has over turning work delivered into cash received.

That's why DSO matters. It shows whether billing, terms, follow-up, and payment experience are supporting liquidity or weakening it. Used well, it becomes a forward-looking operating lever, not just a retrospective KPI.

Firms that manage DSO well don't just collect faster. They plan better, operate with less strain, and protect client relationships while doing it.

Resolut automates AR for professional services, consistent, accurate, and human.