Credit Risk Assessment Tools for B2B Service Firms

Move beyond gut feelings. Learn to use modern credit risk assessment tools to protect cash flow, reduce DSO, and make smarter credit decisions for your firm.

A client looked solid when you signed the engagement letter. The work was profitable, the team was busy, and the receivable sat in aging just long enough to feel annoying, not dangerous. Then the excuses changed tone. AP turnover. A funding delay. A dispute that surfaced after the work was already delivered.

That's the quarter when many finance leaders realize they don't have a credit process. They have a collections process.

For professional services firms, that distinction matters. You're often extending credit to private companies with limited public financial information, uneven payment discipline, and projects that keep expanding before old invoices are cleared. By the time a serious hold is discussed, the exposure is already on the books. If that sounds familiar, small business credit risk management is less about avoiding every bad account and more about building a framework that catches deterioration early enough to act.

Moving Beyond the Surprise Write-Off

The surprise write-off rarely starts as a dramatic event. It usually starts with tolerance.

A project manager asks for one more exception because the client is strategic. Sales says the renewal is close. Finance sees a few late invoices, but the relationship has been good, so nobody wants to escalate. Then one account consumes more attention than ten healthy ones, and cash flow planning turns into guesswork.

Why reactive credit control fails in service firms

Service businesses don't hold inventory they can reclaim. Once the work is delivered, recovery options narrow fast.

That's why old habits break down. A spreadsheet review once a month won't help if a client's payment behavior worsens mid-project. Gut feel won't help if the partner team keeps staffing work while receivables age. A bureau score alone won't help if the customer is privately held and the most useful signal is your own payment history.

Practical rule: If your first serious credit conversation happens after invoices are already overdue, you're managing consequences, not risk.

A better approach treats credit risk assessment tools as part of operating discipline. They're not there to replace judgment. They're there to tell your team when judgment needs to be applied sooner.

What proactive control looks like

In practice, proactive control is simple to describe and harder to execute consistently:

- Review exposure before more work is released: Don't wait for a formal default event. Review what's open, what's unbilled, and what's likely to be invoiced next.

- Use payment behavior as a live signal: A client who starts stretching terms is telling you something. Finance should treat that as decision input, not background noise.

- Tie risk to action: A deteriorating account should trigger a changed response. That might mean revised terms, executive review, tighter milestone billing, or a pause on new work.

The payoff is control. Not theater. Not a prettier dashboard.

When a firm moves from reactive credit holds to a data-driven framework, collections become calmer, forecasting improves, and client exceptions stop being made in the dark.

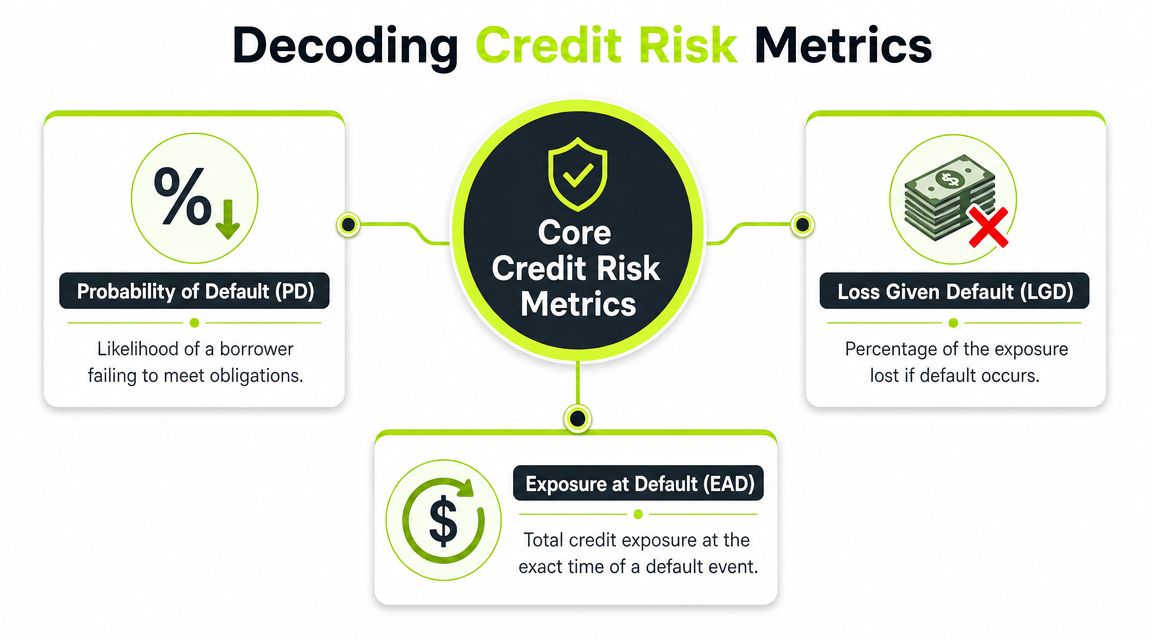

Decoding the Core Metrics of Credit Risk

Most credit risk assessment tools dress up basic concepts in technical language. The core math is simpler than it sounds.

Take a consulting contract worth $100,000 annually. The client is active, the invoices go out monthly, and several months of work are in motion. You need a clear way to judge how risky that account is before approving more exposure.

PD is the chance the client stops paying

Probability of Default (PD) answers one question. How likely is it that this client won't meet its payment obligations?

For a service firm, PD is rarely inferred from one source alone. You look at aging trends, broken promises, dispute frequency, executive turnover on the client side, and whether payment timing is getting worse invoice by invoice. If your team is also working on better reporting and streamlining data with AI insights, the useful lesson is the same. Risk decisions improve when operational signals are organized into something visible and current.

LGD is what you likely won't recover

Loss Given Default (LGD) is the portion of the balance you expect to lose if default happens.

It is vital for service firms to maintain a realistic outlook. If the work is already delivered and there's no hard collateral, the amount you recover may depend on bargaining power, legal costs, and whether there's enough commercial value left in the relationship to negotiate a settlement. That's very different from a secured lending situation.

A practical way to think about LGD is this. If a client fails, how much of the open balance is collectible after disputes, delays, and legal friction?

EAD is your real exposure today

Exposure at Default (EAD) is the amount at risk if the client defaults now.

That number usually exceeds the single overdue invoice everyone is staring at. It includes open receivables, approved work in progress that's about to bill, and sometimes contractual commitments that your delivery team is still honoring. If finance only watches past-due balances, it can miss the full exposure building behind the scenes.

The best credit review often starts with a plain question: “If this client stopped paying today, how much value is already exposed?”

If you want a more grounded definition of the underlying credit concept before evaluating software, credit worthiness in practical terms is a useful starting point.

Why these three metrics matter together

A tool that shows only a score doesn't help much. A finance leader needs to know what is likely to happen, what the loss could look like, and how much is currently at stake.

That combination turns a vague risk discussion into an operating decision. Do you keep terms as they are, tighten approvals, change billing cadence, or escalate before more work ships? That's where these metrics earn their keep.

Comparing Credit Risk Assessment Models

Not all credit risk assessment tools solve the same problem. Some help with public-company screening. Some automate rule enforcement. Some promise AI-driven prediction. Very few handle the complex mix that professional services firms face.

The issue is straightforward. Many of your clients are private, unrated, and operationally healthy until they aren't. CreditBenchmark notes that consensus data aggregators address the “unrated entity problem” by pooling anonymized internal credit views from banks with actual exposure to middle-market, private, and fund counterparties that traditional agencies do not cover, which is directly relevant when a service firm is trying to assess a client with little public data available (CreditBenchmark on the unrated entity problem).

Where each model fits

Some models are useful for screening. Some are useful for control. The strongest setups usually combine external context with your own receivables data.

Model Type | Primary Data Source | Best For | Key Limitation for Service Firms |

|---|---|---|---|

Traditional credit bureau data | Agency files, public records, external ratings | Initial screening of larger or publicly visible counterparties | Weak coverage for private, unrated clients |

Static rule-based engines | Internal policy rules, aging thresholds, credit limits | Consistent policy enforcement and fast exception handling | Rigid logic can miss changing behavior patterns |

Dynamic machine learning models | Internal payments data, behavioral signals, alternative data | Detecting subtle deterioration earlier | Hard to trust if the model is opaque or poorly governed |

Hybrid systems | External data plus internal AR, billing, dispute, and workflow signals | B2B firms with mixed client quality and limited public data | Requires clean integration and stronger operating discipline |

Traditional bureau-driven models

These are familiar and often useful at the front end. If a prospect has a meaningful public file, external credit data can provide a decent baseline.

The problem is coverage. In professional services, many clients won't have the depth of public information needed to support a reliable decision. Even when a file exists, it may lag current conditions. A client can look stable externally while your own AR team is already seeing slower approvals and longer payment cycles.

Static rules are dependable, but narrow

Rule-based systems still matter. A rule like “no new work if invoices exceed approved terms and there is no documented payment plan” is operationally valuable because it's clear and enforceable.

What static rules don't do well is context. They can tell you that a threshold has been crossed. They usually can't tell you whether the client is trending toward trouble before the threshold is breached.

Rules are strong at consistency. They're weak at early pattern recognition.

Dynamic AI and machine learning models

Many vendors overpromise in this area. The true benefit isn't magic prediction. It's better pattern detection across payment timing, disputes, invoice acceptance, project expansion, and changes in customer behavior.

For service firms, that can be useful because the strongest signal is often internal. Your own history may say more about client risk than any bureau file. But if the model can't explain what it's seeing, finance teams struggle to trust it, audit it, or defend its decisions.

Why hybrid systems usually win

A hybrid setup tends to fit the operating reality of a mid-market service business. It uses external data when available, but it doesn't collapse when a client has no public rating. It gives weight to internal payment behavior, open exposure, and recent account activity.

That matters because the practical question isn't whether a model can score risk in theory. It's whether it can score the specific clients you invoice.

Essential Tool Features for Modern AR Teams

A credit score sitting in a portal doesn't change cash flow. What matters is whether the tool changes behavior inside finance, sales, and delivery.

For AR teams, the best credit risk assessment tools don't just evaluate risk. They turn risk into workflow.

Real-time scoring tied to account activity

A static review at onboarding isn't enough. Client risk changes while work is active.

A useful platform updates risk when new invoices are issued, promises are broken, disputes increase, or payment timing slips. That gives the finance team a reason to act before the next month-end review. In a services environment, timing matters because exposure grows as labor is delivered, not just when invoices become overdue.

Integration with AR aging and billing systems

If the tool can't see your live receivables, it's mostly an advisory layer.

For firms using QuickBooks or another accounting system, the practical requirement is simple. The tool should pull in aging, invoice status, unapplied cash context, and client-level payment patterns without forcing the AR team to maintain duplicate records. That's where QuickBooks AR automation becomes relevant. Credit decisions should sit next to the same data your collectors and controllers use every day.

A disconnected model creates two versions of the truth. Finance starts trusting the ledger. Operations starts trusting the dashboard. Nobody moves quickly because nobody is looking at the same account picture.

Alerts that arrive before a hold is necessary

Good alerts aren't just notifications. They're operational prompts.

The best ones tell your team what changed and what should happen next. If a client has begun paying later, a strong alert might recommend revised outreach, executive review, or tighter approval on new project work. If a billing dispute appears on a previously clean account, that signal should go to both AR and client service leadership.

Useful alerts usually have three traits:

- Specific trigger logic: The team knows why the alert fired.

- Clear owner: Someone is accountable for the next step.

- Embedded response path: The alert connects to a task, queue, or approval workflow.

APIs and workflow orchestration

APIs matter less for technical elegance than for control. If your credit tool can push risk changes into proposal approval, billing cadence, collections sequencing, and customer communication, then the score becomes operational.

Accounts receivable automation and AI AR automation come into play. The point isn't to automate everything. The point is to automate the routine response while keeping judgment for exceptions. For example, a moderate risk change might alter reminder timing automatically, while a severe deterioration routes the account for controller review.

Auditability and human override

Finance leaders need to defend decisions. That means the tool should show which inputs shaped the score, what changed over time, and who approved any override.

That matters for internal control, but it also matters for relationships. Sometimes you'll keep a client on flexible terms for strategic reasons. Fine. Just make sure the exception is visible, documented, and revisited.

A tool earns trust when it makes decisions easier to review, not harder to explain.

The firms that reduce DSO and improve cash flow with software usually aren't buying flashy analytics. They're buying systems that close the gap between risk insight and daily AR execution.

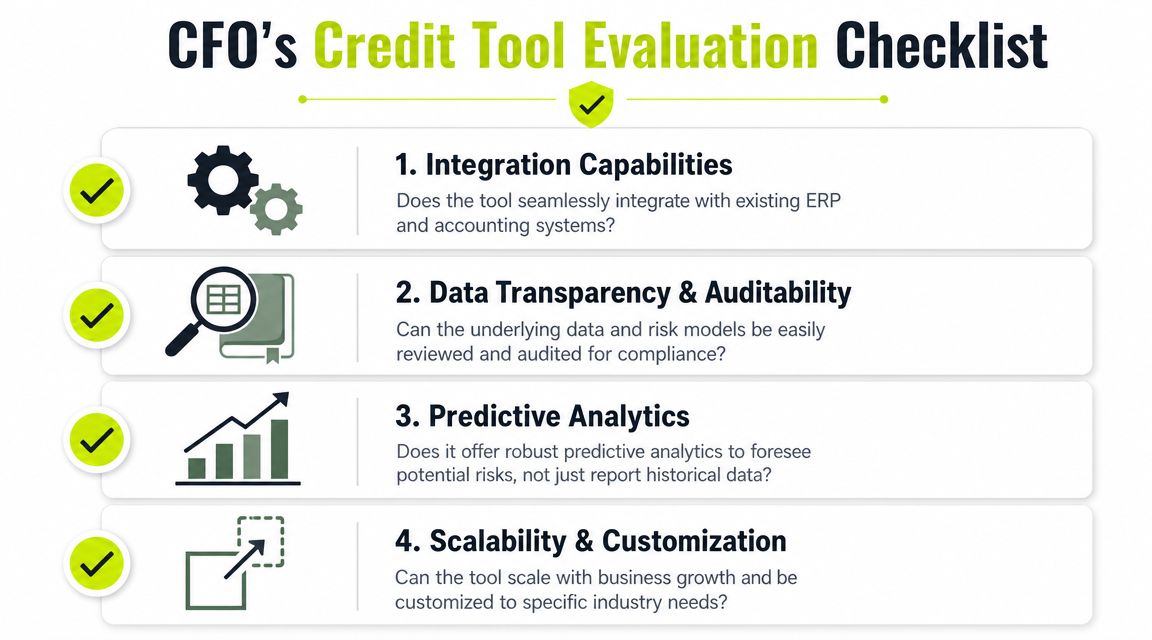

A CFOs Checklist for Vendor Evaluation

Vendor demos usually look polished. The hard part is getting past polished.

A CFO or controller should evaluate credit risk assessment tools by asking what happens in messy accounts, not ideal ones. You want to know how the system behaves when a new client has little history, when a partner pushes for an exception, or when the model's recommendation conflicts with commercial pressure.

Ask what the model actually uses

Vendors love broad phrases like AI-driven scoring and alternative data. Ask for specifics.

The World Bank reports that using alternative data in credit models can yield predictive gains of 5% to 20% versus traditional-data-only models, while also noting inputs such as digital invoices, payment gateways, and e-commerce data across underwriting, monitoring, and collections (World Bank guidance on alternative data in credit models). That's useful, but it doesn't mean every vendor using “alternative data” is improving decisions in your environment.

Ask these questions directly:

- Which signals matter most in your model: If they can't name the drivers, they probably can't validate them.

- How do you separate useful signal from noise: More data isn't automatically better control.

- How often is the model recalibrated: A stale model can be as misleading as no model.

Test the system on unrated and thin-file clients

At this point, many demos get uncomfortable.

Professional services firms often serve private companies with limited public data. Ask the vendor to show how the tool handles a client with no external rating, no deep bureau file, and only a short payment history. If the answer boils down to “we need more data,” you've found the limitation.

A good evaluation question is simple: what does your tool do when internal receivables behavior is the strongest signal available?

Push on integration, not just analytics

If you're evaluating AR software for professional services, integration should be treated as a control issue, not a convenience feature.

Ask the vendor to demonstrate:

- QuickBooks workflow fit: Show exactly how new invoices, aging buckets, and payment updates are reflected.

- Task routing: Who gets notified when risk changes, and where do they act?

- Collections linkage: Can outreach cadence change automatically based on risk movement?

For firms tightening front-end controls as well as back-end collections, the same discipline often improves onboarding quality. Teams looking at approvals, documentation, and account setup can borrow useful ideas from optimizing supplier onboarding, especially around consistency and handoff design.

Require proof on your own history

Don't settle for benchmark claims from a generic customer segment. Ask the vendor to test against your data.

That doesn't need to become a science project. It does need to answer practical questions:

- Did the system identify accounts your current process missed?

- Did it create useful prioritization, or just more alerts?

- Could your AR team act on the output without adding manual work?

If a vendor can't show how the tool performs on your historical receivables, you're buying a promise, not a control system.

Review governance before you review design

A sharp interface is nice. Governance is what keeps the tool from becoming shelfware.

Look for:

- Transparent override controls: You need to know who changed a recommendation and why.

- Audit trail quality: Model inputs, score changes, and workflow actions should be reviewable.

- Role clarity: Finance, sales, and delivery shouldn't each invent their own exception path.

The right vendor won't resist these questions. They'll welcome them, because serious buyers care about operational control more than visual polish.

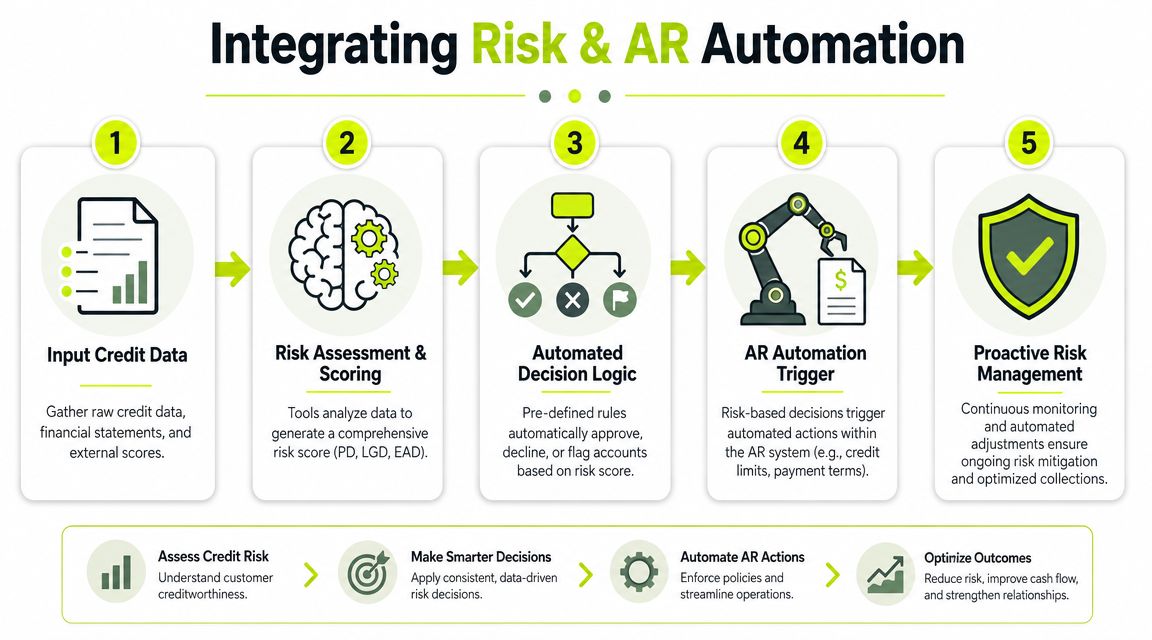

Integrating Risk Tools with AR Automation

A risk score on its own is just a label. The return comes when that label changes the next action automatically and visibly.

That's why credit risk assessment tools matter most when they're embedded inside the AR workflow, not parked in a separate analyst portal.

Before integration

In many firms, the process still looks like this. A credit review happens manually. Someone exports an aging report. A note gets emailed to collections. Sales may or may not be copied. Delivery keeps moving because no formal hold has been entered.

Nothing is technically broken, but the response is slow and uneven. High-risk accounts stay in motion because the information reaches people as commentary, not as a trigger.

After integration

An integrated setup works differently. Risk changes feed directly into collections logic, billing controls, and account review queues. When an account weakens, the system can change reminder tone, increase follow-up urgency, or route the client for approval before additional work is released.

That's where accounts receivable automation software stops being a back-office efficiency project and becomes a cash-control system.

Here's the difference in practical terms:

- Before: AR identifies trouble after invoices age.

- After: Finance responds when payment behavior first shifts.

- Before: Team members interpret risk manually.

- After: Predefined logic applies a consistent first response.

- Before: Exceptions live in email threads.

- After: Exceptions are visible, tracked, and reviewable.

A short walkthrough can help make that operating model concrete:

Where one platform can fit

This is the point where platform design matters. For example, Resolut combines AR automation with risk identification, collections workflows, billing orchestration, and cash application in one operating layer. That matters if your team wants risk signals to affect outreach, escalation, and payment follow-up without stitching together multiple disconnected tools.

A score becomes valuable when it changes behavior the same day, not when it gets mentioned in the next finance meeting.

For firms trying to improve cash discipline without becoming rigid with clients, that combination of automation and human review is usually the most workable model.

Maximizing ROI and Avoiding Common Pitfalls

The return on credit risk assessment tools doesn't come from owning the software. It comes from changing when and how your team acts.

In a professional services firm, the clearest gains usually show up as fewer ugly surprises, tighter forecasting, more disciplined client exceptions, and a stronger path to improve cash flow. If the tool is integrated well, it also supports accounts receivable automation, helps reduce DSO, and gives finance a better basis for deciding when to slow exposure before a client becomes a collections problem.

Three mistakes undermine that return more than anything else:

- Relying on one data source: Bureau data alone misses too much in private-company portfolios.

- Treating the tool as separate from AR execution: If risk insight doesn't change billing, collections, or approvals, the value stays theoretical.

- Failing to recalibrate: Client behavior changes. Your model and thresholds need review, too.

The firms that get this right don't chase perfect prediction. They build a process that catches deterioration early, responds consistently, and leaves room for human judgment where it matters most.

Resolut automates AR for professional services with a practical mix of risk signals, workflow control, and human oversight. If you're trying to build a steadier process around collections, billing, and client credit decisions, Resolut is built to keep that work consistent, accurate, and human.