Credit Risk Management Solutions A CFO's Guide

Learn how credit risk management solutions reduce DSO and bad debt for professional services firms. A guide for CFOs on evaluation, implementation, and ROI.

Credit risk management usually gets treated like a banking topic. For a professional services firm, that framing misses the actual exposure.

If you send invoices and wait to get paid, you're already in the credit business. The risk doesn't sit in a loan book. It sits in work completed, revenue recognized, and cash that hasn't arrived yet.

That matters because enterprises waste $200B annually on uncollected AR, and 1 in 10 invoices goes unpaid, while the integration of AI-driven AR automation with invoice-level risk orchestration remains underexplored in B2B finance operations, according to Intellify's analysis of lending analytics and AR risk workflows. For a services firm, that's not abstract market risk. It's payroll, partner draws, hiring plans, and tax payments.

The Real Cost of Unmanaged Credit Risk

Most firm owners think credit risk starts when they extend unusual payment terms. It starts earlier than that. The moment you deliver work before cash is collected, you've extended credit.

In a professional services firm, unmanaged credit risk rarely shows up as a dramatic default at first. It shows up as aging receivables, uneven collections, disputed invoices that linger too long, and finance teams manually chasing clients without a system. By the time leadership calls it a “collections issue,” margin has already eroded.

What the loss looks like in practice

The direct cost is obvious. Slow-paying clients stretch cash conversion, increase borrowing pressure, and force owners to fund operations with retained earnings that should've been reinvested.

The hidden cost is operational. Your controller spends time reviewing account histories. Project leads get pulled into payment conversations late. Partners make exceptions without clear thresholds. Nobody has a clean view of which invoices are just late and which are becoming doubtful.

Practical rule: Treat every open invoice as a live credit exposure, not a bookkeeping entry.

A lot of firms try to solve this with policy alone. Tighter terms help, but they don't solve timing, prioritization, or consistency. A written collections policy doesn't tell your team which client needs a call today, which invoice should move to a firmer tone, or which account deserves a payment plan before the relationship deteriorates.

Why the old mental model falls short

Traditional credit controls focus on customer onboarding and broad credit approval. That's too static for firms billing monthly retainers, milestone fees, pass-through costs, or time-and-materials work.

What works better is a continuous model. Assess risk before invoicing, at invoice release, after due date, and as payment behavior changes. If you're reviewing reserves for doubtful accounts, it helps to connect that accounting judgment with actual invoice behavior. A practical resource on allowance for uncollectible accounts then becomes useful for aligning AR operations with the balance sheet.

For firms exploring payment structure changes, it's also worth looking at Comfi's risk-free payment solutions as an example of how payment design can reduce customer friction while containing exposure.

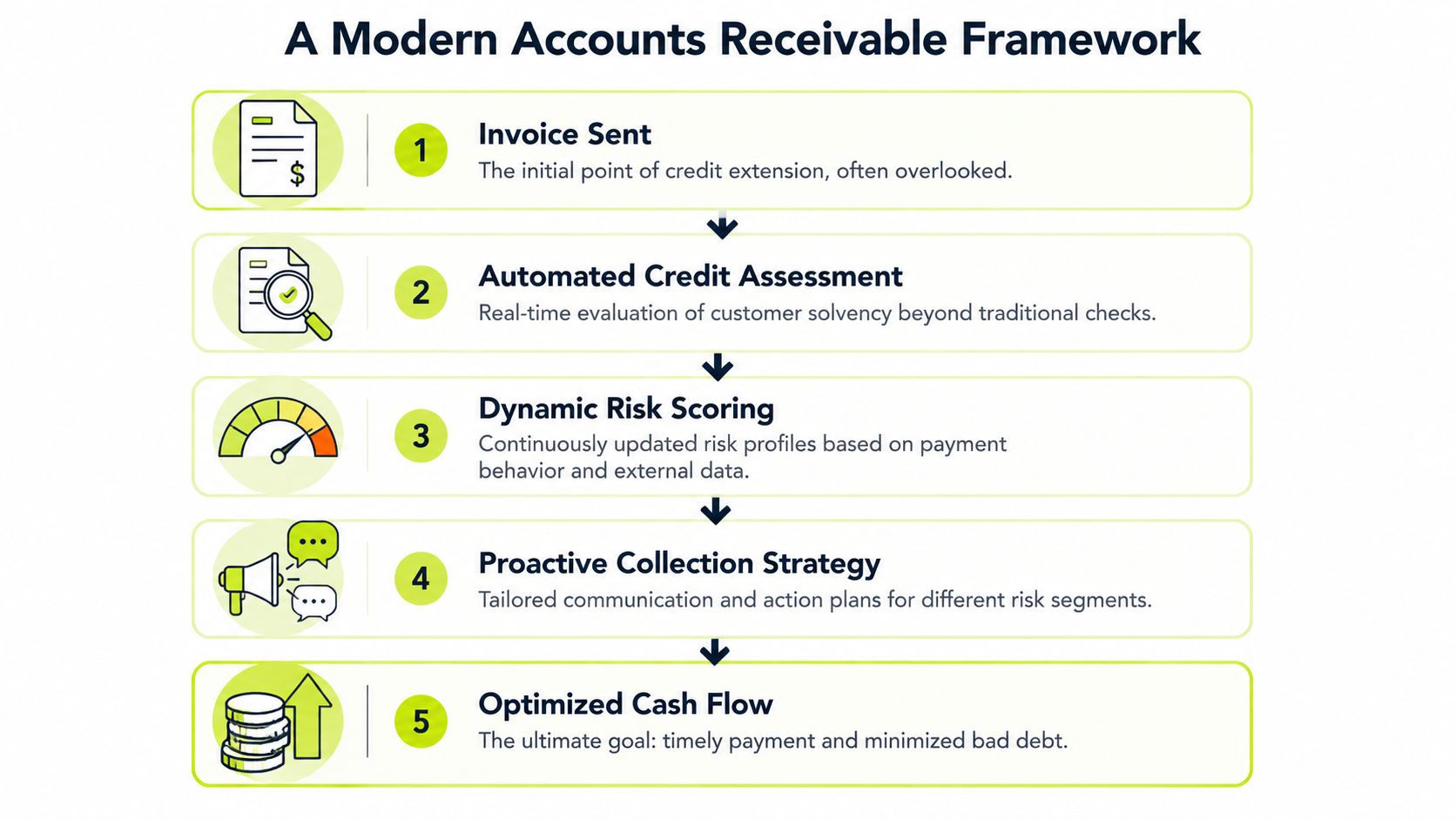

Beyond Traditional Credit A Modern AR Framework

The market is moving in this direction. The global credit risk solutions market was valued at $12.8 billion in 2025 and is projected to reach $28.6 billion by 2034, with a 9.3% CAGR, according to Capgemini's credit risk management analysis. That growth started in bank-grade risk controls, but the operating logic now applies directly to firms that need tighter control over receivables.

A modern AR framework treats invoicing, collections, payment acceptance, and reconciliation as one control system. Not four separate tools. Not one spreadsheet plus a few reminders from accounting.

Every invoice is a credit decision

Professional services firms often miss this because they don't think of themselves as lenders. But if a client receives deliverables now and pays later, you've made a credit decision whether you documented it or not.

The stronger approach is to build a framework around the full invoice-to-cash cycle:

- At invoice creation: confirm that billing accuracy, contact data, approvers, and payment instructions are right

- At release: assess whether the client's recent payment behavior suggests normal follow-up or closer monitoring

- After due date: shift outreach based on risk, relationship value, and dispute signals

- At payment: reduce friction with simple, secure options and clear remittance capture

- At reconciliation: close the loop quickly so finance can trust AR aging and cash position

What unified control looks like

Credit risk management solutions become practical for a services CFO. The useful systems don't just score accounts. They connect scoring to action.

A modern platform should give finance one operating view of exposure, outreach, payment status, and exceptions. That's very different from a legacy setup where your ERP holds invoice data, a collector sends emails manually, and someone else posts cash later.

The best AR process is boring. Invoices go out on time, follow-up happens consistently, clients have easy ways to pay, and exceptions surface early.

If you're comparing operating models, firms that need broader finance workflow support may also review providers focused on end-to-end AP/AR for small businesses. The key question is whether the system can orchestrate receivable risk, not just record transactions.

For firms trying to define the software category more clearly, this overview of a receivable management system is a useful reference point.

The shift that matters

The old model asked, “Should we extend terms?”

The modern model asks, “How do we continuously manage exposure after work is delivered?”

That shift changes behavior. It moves AR from reactive chasing to controlled execution.

Key Capabilities That Drive Cash Flow

Most finance teams don't need more dashboards first. They need a system that makes the next right action obvious.

That starts with risk scoring tied directly to receivables. Integrated quantitative models can reduce loan losses, which is analogous to bad debt in AR, by 20-30%, and machine learning applied to invoice-level Probability of Default can help cut DSO by 10-15 days in B2B invoicing, according to SAS on credit risk management and real-time scoring.

Proactive risk scoring

The practical value of scoring isn't the score itself. It's what the score changes.

If a client that normally pays in thirty days begins paying in forty-five, opens fewer emails, and starts disputing line items after approval, the system should move that account into a different workflow. That might mean earlier outreach, a call from the account owner, or a pause before more work gets released.

A useful score updates as behavior changes. A useless score gets reviewed once a quarter and filed away.

Automated collections that still feel human

Finance teams often make one of two mistakes. They either over-automate with generic reminders that irritate good clients, or they under-automate and depend on heroic manual follow-up.

The middle path works better. Use automation for timing, sequencing, and channel coordination. Keep judgment for exceptions, strategic accounts, and disputed invoices.

Good workflows usually include:

- Segmented outreach: Low-risk accounts get polite reminders. Higher-risk accounts get firmer messaging and faster follow-up.

- Channel coordination: Email alone isn't enough for every client. Some pay after an SMS prompt. Others respond only when a project lead calls.

- Escalation rules: The team should know when an invoice moves from reminder to intervention.

One reason firms look outside their own industry for ideas is that banks have spent years refining signal detection and workflow analytics. This background piece on banking industry analytics is helpful for understanding how behavior-based monitoring can inform AR decisions, even though the operating context is different.

Payment orchestration matters more than most firms expect

If paying you is inconvenient, collections performance suffers even when the client intends to pay.

That means your AR software for professional services should support a client-friendly payment experience with clear invoice links, accurate balances, and straightforward options. Clients shouldn't have to ask where to remit, whether partial payment is acceptable, or how to apply payment to multiple invoices.

A surprising amount of “credit risk” is really payment friction plus slow follow-up.

Automated cash application and QuickBooks AR automation

Many firms experience a subtle loss of control. Collections may improve, but if cash posting lags, the aging report becomes unreliable and collectors chase invoices that have already been paid.

For firms running QuickBooks, QuickBooks AR automation should do more than trigger reminders. It should reduce the manual handoff from payment receipt to reconciliation, so the controller can trust the subledger and close faster.

That's especially important in professional services, where one client payment may cover several invoices, retainers, or project phases. If your team still matches remittances by hand, scale will create noise before it creates advantage.

Intelligent escalation without damaging the relationship

Escalation should be part of the operating model, not an emotional decision made after frustration builds.

Some accounts need a firmer voice. Others need a reset with the client sponsor because the issue isn't unwillingness to pay but internal approval delay. The right platform supports graduated escalation, including legal-style language when appropriate, while keeping a human reviewer in the loop.

This is one reason firms evaluate tools like NetSuite AR modules, Billtrust, HighRadius, and specialized platforms such as Resolut, which combines risk identification, omnichannel collections, payment workflows, and automated cash application in one operating layer. Ultimately, the question isn't feature count. It's whether the system helps your team reduce DSO, improve cash flow, and stay consistent under pressure.

If you want a sharper operating definition for the risk side of the equation, this guide to what credit worthiness means in practice helps frame how customer quality should influence AR actions.

Measuring the Impact on Your Firm

A finance system earns its place when it changes core metrics you already review in the monthly packet. For AR, that means speed, loss rate, and predictability.

Advanced solutions that use AI-driven portfolio monitoring can achieve 25-40% improvements in risk-adjusted returns, and in a B2B context that translates to keeping non-performing invoice rates below 2% versus industry averages of 4-5% by using early warning signals to trigger intervention, according to Credit Benchmark's credit risk monitoring framework.

Reduce DSO without turning collections into a blunt instrument

DSO falls when three things happen reliably. Invoices go out correctly. Follow-up happens on time. Paying is easy.

Many firms focus only on the third reminder. The stronger move is earlier intervention. If a system identifies payment drift before an invoice becomes severely overdue, your team can act while the relationship is still cooperative.

A practical dashboard should show more than total overdue AR. It should surface behavioral changes by client, invoice cohort, collector queue, and dispute status.

When DSO improves, the real benefit isn't just speed. It's optionality. You gain room to hire, invest, and absorb surprises without forcing decisions.

Lower write-offs by catching deterioration early

Bad debt often looks inevitable only in hindsight. Usually the warning signs were there. Slower payment cadence. More exceptions. Delayed responses. Repeated promises without follow-through.

A modern monitoring setup lets finance separate temporary delay from actual deterioration. That distinction matters. You don't want to overreact with strong-arm tactics on a valuable client who has an internal approval bottleneck. You also don't want to keep extending soft treatment to an account that's degrading.

Here's a useful walkthrough on what modern monitoring can look like in practice:

Improve cash flow forecasting

Forecasting gets cleaner when AR data is trustworthy.

If collections activity, promises to pay, disputes, and unapplied cash all sit in different places, your weekly cash forecast turns into informed guesswork. Once those signals live in one workflow, the forecast improves because finance can distinguish booked receivables from likely cash.

A simple measurement set works well:

KPI | What to watch | Why it matters |

|---|---|---|

DSO trend | Direction and consistency over time | Shows whether billing and follow-up are improving |

Non-performing invoices | Which accounts stall repeatedly | Highlights write-off risk early |

Promise-to-pay conversion | Commitments kept versus missed | Tests the quality of collections activity |

Cash application lag | Time from payment to posting | Protects reporting accuracy |

Dispute resolution cycle | Aging of invoice exceptions | Prevents collectible balances from going stale |

For most firms, the operational efficiency gains are meaningful too. When accounting stops spending hours assembling status updates by hand, that time goes back into analysis, client coordination, and exception handling.

How to Evaluate the Right Solution

A good demo can hide a weak operating fit. The right way to evaluate credit risk management solutions is to test whether the tool matches how your firm bills, follows up, reconciles, and escalates.

Start with your current state. If your firm runs on QuickBooks, a polished enterprise platform may still fail if QuickBooks AR automation is shallow, delayed, or dependent on exports. The same is true if your team relies on project managers for dispute resolution and the software can't route issues cleanly.

What separates useful systems from expensive noise

Look for evidence of workflow depth, not feature sprawl.

A vendor may show scoring, reminders, and dashboards. That's not enough. Ask how risk signals trigger different actions. Ask how unapplied cash gets resolved. Ask what the client experience looks like when paying multiple invoices or asking for clarification.

Don't buy AR software for professional services based on reminder templates. Buy it based on control.

A strong evaluation usually comes down to five questions:

- Does it integrate cleanly with your accounting stack? You want dependable synchronization of invoices, credits, payments, and customer records.

- Can workflows adapt by client type? Your largest strategic client shouldn't receive the same sequence as a chronically slow small account.

- Is the AI predictive or just rule-based? Vendors should explain what changes when payment behavior shifts.

- How strong is the client payment experience? Simplicity affects collections outcomes.

- Can finance stay in control? Human review should be available where judgment matters.

Vendor Evaluation Checklist

Evaluation Criterion | What to Ask | Why It Matters |

|---|---|---|

Accounting integration | How does the system sync with QuickBooks or your ERP, and how are sync failures handled? | AR control fails if invoice and payment data drift |

Workflow flexibility | Can we set different paths by client segment, invoice age, dispute status, and owner? | Services firms need nuance, not one-size-fits-all chasing |

Risk modeling | What inputs affect risk scoring, and how often do scores update? | Static scoring won't catch deteriorating payment behavior |

Collections orchestration | Which channels are supported, and how do reminders, calls, and escalations coordinate? | Consistency improves collections without creating chaos |

Cash application | How are remittances matched, exceptions flagged, and unapplied cash resolved? | Clean reconciliation supports reporting and trust in AR aging |

Payment portal quality | What does the payer experience look like on desktop and mobile? | Friction at payment stage slows collections |

Security and controls | How are permissions, approvals, audit trails, and sensitive payment data handled? | Finance needs defensible controls, not just convenience |

Implementation support | Who owns onboarding, training, and process design? | Weak rollout can sink a good tool |

Run your evaluation with real invoices, real client scenarios, and real exceptions. If a vendor only looks strong in a clean demo environment, keep looking.

Implementation A People Process Tech Roadmap

Implementation goes better when you treat it as an operating change, not a software install.

The common failure pattern is simple. Leadership buys a tool to reduce DSO. Accounting gets limited training. Old exceptions remain undocumented. Project leaders keep sending ad hoc payment emails. Six months later, the firm says the software didn't work.

People

Assign clear ownership early.

Finance should own policy, segmentation, and escalation rules. Operations or project leadership should help define client communication boundaries. Someone needs authority to decide when the system follows standard workflow and when an exception is justified.

Training should focus on judgment, not just clicks. Your team needs to know when to pause automation, when to involve account leaders, and when to move an issue into dispute management rather than collections.

Process

Map the current state before you configure anything.

Review how invoices are created, approved, delivered, followed up, disputed, paid, and posted. Most firms find the same weaknesses quickly: inconsistent invoice timing, unclear ownership, no standard escalation path, and too much dependence on individual relationships.

A tighter process usually includes:

- Invoice discipline: send accurate invoices on schedule, with clear support detail

- Risk-based follow-up: route outreach by client behavior, not collector preference

- Exception handling: separate disputes, short pays, and true delinquency

- Escalation governance: define who steps in and when

- Close-loop posting: make sure payment status updates fast enough to support daily action

Implementation succeeds when finance, operations, and client-facing leaders agree on what the system should do automatically and what still needs human judgment.

Technology

The technology work is more straightforward than many organizations expect. The challenge isn't connecting systems. It's configuring them around the right process.

Test integrations with live edge cases. Partial payments. Credits. Multi-invoice remittances. Client-specific terms. Historical notes. Promise-to-pay dates. If those scenarios break, the team will revert to spreadsheets.

There's another issue that deserves attention during rollout. The OCC's fall 2024 risk perspective highlights the intersection of operational risk and credit fraud, with rising external fraud targeting payment systems. That's why implementation should include secure, consumer-grade AR portals with flexible payment options and strong controls, as noted in the OCC's Fall 2024 Semiannual Risk Perspective.

That's not a side concern. If you accelerate collections while creating new payment risk, you haven't improved control. You've just moved the problem.

Your Path to Financial Control

For a professional services firm, credit risk management solutions aren't about behaving like a bank. They're about running receivables with discipline.

The firms that stay in control usually do three things well. They treat every invoice as a live exposure. They connect risk signals to action. They make it easy for clients to pay without letting standards slide.

That combination changes the finance posture of the business. Collections become more consistent. Forecasts get cleaner. Exceptions surface earlier. Client relationships improve because the process is clear and predictable, not improvised when balances age badly.

This also changes how owners make decisions. When AR is stable, growth plans aren't built on hope. Hiring, compensation, partner distributions, and tax planning all become easier because cash timing is less volatile.

The primary benefit isn't just lower DSO, though that matters. It's control. Calm, operational control.

If your current process still relies on spreadsheets, inbox reminders, and team memory, start with the basics. Tighten invoice accuracy. Standardize follow-up. Improve payment options. Then add intelligence where it changes behavior, not where it only adds another dashboard.

That's what modern credit risk management looks like in a services environment. Not theory. Daily execution that protects cash flow without alienating good clients.

Resolut automates AR for professional services, bringing together risk identification, collections workflows, payment orchestration, and cash application in a way that stays consistent, accurate, and human. If you're looking to reduce DSO and improve cash flow without turning client relationships into a collections battle, Resolut is worth a look.