Factoring Accounts Receivable Company: A CFO's Guide

A CFO's guide to evaluating a factoring accounts receivable company. Understand costs, risks, and when AR automation is a better choice to improve cash flow.

Revenue is up. Utilization is solid. The pipeline looks healthy.

But cash is tight because clients are taking their time to pay, and your payroll, partner draws, software spend, and tax obligations won't wait. That gap is where many firm owners start asking about a factoring accounts receivable company.

My view is simple. Factoring can solve a real problem, but it's usually a blunt instrument. If you run a professional services firm, you should treat it as a tactical decision, not a default operating model.

The Cash Flow Operator's Dilemma

You deliver the work in March. The client approves the invoice in April. AP says the payment run is in May. The cash lands in June.

That sequence is normal in professional services, and it creates a false picture of financial health. On paper, you're profitable. In practice, you're funding client payment delays out of your own operating cash.

I see this pattern most often in firms between early scale and mid-market maturity. Revenue grows faster than collections discipline. A few enterprise clients push terms out. One disputed invoice stalls. Suddenly the controller is moving money between accounts just to keep timing clean.

Cash flow strain in a profitable firm usually isn't a revenue problem. It's a working capital problem with a collections layer on top.

A factoring accounts receivable company enters the conversation at that point because it offers speed. Instead of waiting through standard payment cycles, you sell eligible invoices and pull cash forward. That can protect payroll, smooth vendor payments, or bridge a concentrated client delay.

But don't confuse urgency with strategy.

Before you hand over invoices, you need to know whether the issue is temporary timing, weak billing discipline, or a structural gap in how your firm manages receivables. If your process is loose on invoice approval, follow-up cadence, and escalation, financing the receivable won't fix the root cause.

If you're tightening policy first, it helps to review practical guidance on understanding late payment rules. Not because legal pressure solves everything, but because collections gets easier when your team understands what recourse exists and when to use it.

What usually drives the factoring question

- Large clients set the tempo: Your team may finish work quickly, but enterprise procurement and AP teams still move slowly.

- Payroll hits before collections: Service firms carry labor cost first and recover cash later.

- Growth absorbs liquidity: More revenue can tighten cash when invoices age out.

- The founder wants certainty: Predictable cash matters more than maximizing every basis point of margin when the business is under timing pressure.

That's the dilemma. You're not choosing between good and bad. You're choosing between expensive speed and operational repair.

How a Factoring Accounts Receivable Company Operates

A factoring accounts receivable company buys your invoices. It doesn't make a standard term loan against them.

That distinction matters. The transaction is typically structured as a sale of receivables, which means the invoice becomes the asset that generates immediate liquidity. According to the IRS overview of receivables factoring, businesses usually receive cash within about 24 hours, rather than waiting the usual 30, 60, or 90 days for customer payment, with advance rates commonly around 70% to 95% and fees often around 1% to 5% of invoice value, depending on risk and collection effort (IRS factoring overview).

Here's the process visually.

The mechanics in plain English

There are three parties:

- Your firm issues the invoice.

- Your client owes the payment.

- The factor buys the invoice and advances cash.

The flow is straightforward.

You complete work and issue an invoice. The factor reviews that invoice, along with the client's credit quality and payment history. If it accepts the invoice, it advances most of the value upfront. Later, once the client pays, the factor releases the reserve minus its fee.

A simple example makes this easier to see. If you factor a $100,000 invoice, firms often receive $80,000 to $95,000 quickly, with the factor holding back roughly 5% to 20% as a reserve until the customer pays (Versapay explanation of AR factoring structure).

Practical rule: The factor is underwriting your client's ability to pay, not just your need for cash.

Why the reserve matters

Most finance leaders focus on the upfront advance. That's only half the economics.

The reserve is the held-back portion of the invoice. It protects the factor while the receivable is outstanding. Once your client pays, the factor returns that reserve after deducting the agreed fee.

That means your actual cash timing depends on two things:

- How fast your client pays

- How the fee accrues over time

For a clean explainer on the transaction structure, this overview of what invoice factoring is is useful if you want your operating team to understand the mechanics before you evaluate providers.

A short walkthrough can help if you need to brief a founder or partner group.

What changes operationally after you sign

Many professional services firms hesitate at this point, correctly.

In the traditional model, the factor often takes over collections on the factored invoices. Your client may now be instructed to pay the factor directly. That can be fine in industries where factoring is common. In advisory, agency, consulting, legal support, engineering, or other relationship-driven firms, it can feel intrusive.

You also won't be able to factor every invoice. Eligibility often depends on invoice age, client credit quality, and documentation quality. If your billing support is messy, approvals are disputed, or time entries don't reconcile cleanly, the factor will either decline the invoice or price the risk accordingly.

Visual ideas for your finance team

- Cash conversion timeline chart: Work delivered, invoice issued, factor advance received, client payment collected, reserve released.

- Cinematic image: A controller at month-end with a billing queue on one screen and payroll calendar on another, showing the timing tension behind the financing decision.

Calculating the True Cost and Risk of Factoring

The advertised fee is never the full story.

A factor may quote what sounds like a manageable charge, but the effective cost depends on collection speed. Factoring is commonly priced as a time-based fee, and that changes the economics fast. Wise explains that factors often advance about 75% to 95% of face value and charge around 1% to 5% per month, with slower collections pushing the effective cost higher because the fee is tied to time outstanding (Wise guide to accounts receivable factoring).

Stop looking only at the headline fee

If the fee accrues by month, your client's payment behavior becomes a pricing variable.

That means a slow-paying but creditworthy client can still turn a supposedly simple working-capital tool into an expensive one. For a professional services firm, that's dangerous because many large clients pay slowly as a matter of policy, not distress.

Use this table to pressure-test a proposal. The scenarios below are illustrative calculations based on the plan's stated fee structure.

Scenario | Factor Fee (2% per 30 days) | Days to Collect | Total Cost | Effective APR |

|---|---|---|---|---|

Fast-paying client | 2% per 30 days | 30 | 2% of invoice value | About 24% annualized |

Standard corporate cycle | 2% per 30 days | 60 | 4% of invoice value | About 24% annualized |

Slow enterprise payer | 2% per 30 days | 90 | 6% of invoice value | About 24% annualized |

That annualized view isn't perfect, because factoring is a sale structure rather than a loan. But it's still the right discipline. If you don't convert the fee into a comparable annual cost, you'll understate what you're paying for speed.

If you wouldn't accept the implied annual cost on a credit facility, don't wave it through just because the contract labels it a receivables sale.

The risk split matters more than the marketing

Two contracts can look similar and behave very differently.

With recourse factoring, your firm remains economically exposed if the client doesn't pay under the agreement terms. With non-recourse factoring, the factor assumes more of that non-payment risk, usually at a higher price and with tighter conditions. The phrase sounds simple, but the details aren't.

Read the triggers carefully. Some “non-recourse” structures only protect against narrow credit events and not billing disputes, offsets, or documentation problems. In professional services, disputes are often the main issue.

What to review in the agreement

Don't just ask for the fee schedule. Ask for the full operating burden.

- Minimum volume requirements: Some providers want a steady flow of invoices, not occasional use.

- Term commitments: A short cash need can get wrapped into a longer contract.

- Termination provisions: Exiting may be harder than getting in.

- Lien language: A broad claim on receivables can complicate other banking relationships.

- Concentration limits: Heavy reliance on one client may reduce what the factor will buy.

- Dispute definitions: Service firms need precision here because scope disagreements happen.

My recommendation on cost analysis

Model factoring the same way you'd model any external capital source.

Build a simple sheet with invoice amount, advance rate, reserve, estimated collection date, fee cadence, expected net proceeds, and downside cases if the client pays late or disputes. Then compare that against the cost of fixing the underlying AR process.

If the process fix costs less over a reasonable operating horizon, choose the process fix.

A Decision Framework for Evaluating Factoring Companies

A partner closes a large project. Payroll hits next week. The client pays on 60-day terms and usually drifts past that. A factoring proposal shows up promising fast cash.

At that point, the decision is not whether factoring exists. The decision is whether this provider solves a timing problem at an acceptable cost, or whether it creates a control problem you will spend the next year cleaning up.

Start with fit, not rate

A factoring company is only a good fit if your cash issue is mainly timing. If your real problem is weak billing discipline, slow dispute resolution, poor follow-up, or inconsistent collections, factoring will mask the issue and add expense.

Before you compare providers, answer three operating questions:

- Are invoices clean and approved before they go out?

- Do clients pay late because of process friction or because they are stretching vendors?

- Is this a temporary working-capital gap or a recurring pattern?

If the problem is operational, fix AR first. These accounts receivable management tips are a better starting point than a term sheet.

Evaluate the cash release mechanics

Now look at structure.

You need to know how much cash you receive immediately, what gets held in reserve, how deductions are calculated, and what has to happen before the reserve is released. Do not accept a blended headline advance rate without client-level detail. Your largest client, your slowest payer, and your most dispute-prone account may all be priced differently.

Ask for a sample funding calculation using your actual invoice mix. Then stress-test it against slow payment, partial payment, and a billing dispute.

Use these questions:

- What advance rate applies by client and invoice type?

- What events reduce the advance or delay funding?

- How often are reserves reconciled and paid out?

- Which invoices are excluded because of age, concentration, contract terms, or client credit profile?

Judge the provider by its effect on your client relationships

In professional services, collections behavior matters as much as price.

If the factor touches your clients, it becomes part of your delivery model. An aggressive collector can damage an account partner faster than a high fee will damage margin. I would treat client communication standards as a board-level risk item, not a back-office detail.

Review actual notices, email templates, call workflows, and dispute escalation paths. Ask who owns the relationship when a client says the invoice is wrong. If the answer is vague, walk away.

Review the contract for operating traps

The contract decides whether factoring stays a tool or turns into a dependency.

Have finance and counsel review the same document at the same time. This guide to a factoring contract agreement is a useful primer before that review.

Focus on the clauses that change your freedom to operate:

- Exclusivity: Can you factor selectively, or are you committing a broad pool of receivables?

- Term length: Does a short-term cash need come with an annual commitment?

- Termination rights: What notice, fees, or payoff conditions apply if you exit early?

- Cross-default and lien language: Will this conflict with your bank covenant package or future financing?

- Servicing and incidental fees: Are there wire fees, due diligence charges, minimums, or inactivity penalties?

- Dispute and chargeback treatment: Who absorbs the loss, and when?

Score each provider the way a CFO would

Do not pick a factor on rate alone. Score each option across four areas and weight them based on your actual risk.

Dimension | What good looks like |

|---|---|

Economics | Clear pricing, predictable reserve release, no hidden servicing charges |

Client impact | Professional communication, controlled collections process, credible dispute handling |

Flexibility | Selective invoice use, reasonable term, clean exit path |

Control and reporting | Timely reports, clean reconciliation, visibility for controller and CFO |

My rule is simple. If a provider weakens client control or restricts your financing flexibility, the deal has to be exceptional elsewhere to survive review. In many firms, it still should not pass.

That is the core decision framework. Compare the provider not only to another factor or a bank line, but also to the cost of fixing AR operations so you collect faster without selling the receivable.

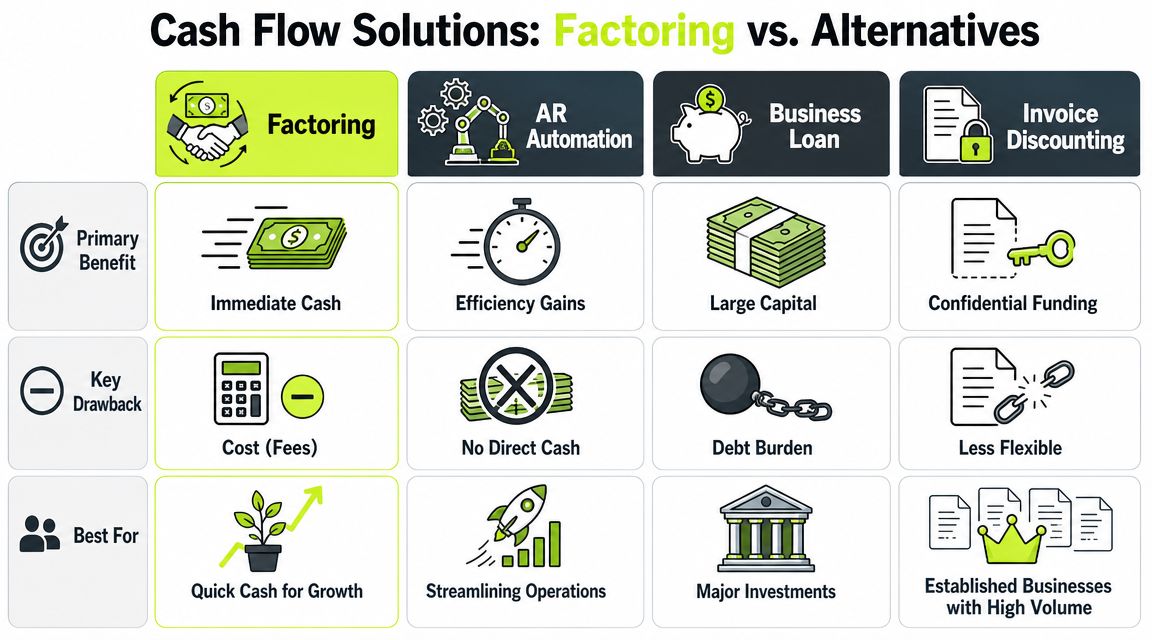

Factoring vs AR Automation and Other Alternatives

Most firms ask the wrong question.

They ask, “Should we factor?” The better question is, “What is the cheapest and cleanest way to convert earned revenue into collected cash without damaging control?”

Factoring is only one answer.

Where factoring fits

Factoring is a cash acceleration tool. It's useful when timing is the problem and speed matters more than cost.

That can make sense if you're carrying a temporary working-capital squeeze, funding a sharp growth period, or covering a concentrated client delay. It's less appealing when your problem is recurring weak billing operations, poor collections cadence, fragmented cash application, or inconsistent partner enforcement.

Invoice financing is similar, but not identical

Teams often mix up factoring and receivables financing.

The key difference is control. In traditional factoring, the provider often takes over collection on the sold invoices. In other receivables financing structures, your firm may retain more control over customer communication while still borrowing or advancing against invoice value. If your team is comparing structures, this explanation of receivables financing is a useful contrast point.

That distinction matters because client experience matters.

If you're a consulting firm, agency, architecture practice, engineering firm, or outsourced finance provider, collections is not a back-office side note. It's part of account management.

AR automation addresses the root cause

In my view, for most professional services firms, accounts receivable automation is the better strategic move.

Paystand notes an important market shift. Technology, automation, and changing payment behavior are reshaping when factoring is needed at all, and businesses are increasingly using tools to decide when to factor selectively rather than by default. It also points to questions around omnichannel collections, automated cash application, and dynamic billing that can reduce dependence on selling receivables in the first place (analysis of automation and the changing factoring landscape).

That's the comparison.

If your team can invoice cleanly, send the right follow-up at the right time, route disputes quickly, offer digital payment paths, and reconcile cash without manual lag, you can often reduce DSO, improve cash flow, and keep control of the client relationship without paying a factor to stand in the middle.

What modern AR software changes

For a professional services firm, strong AR software for professional services should improve execution in a few specific areas:

- Billing consistency: Invoices go out on time with accurate support.

- Collections orchestration: Reminders, escalation, and follow-up happen on schedule instead of relying on memory.

- Payment convenience: Clients can pay through cleaner digital workflows.

- Cash application: Your team closes the loop faster once money lands.

- Risk visibility: Finance sees which accounts need attention before they age badly.

That's where AI AR automation becomes practical instead of theoretical. It helps teams prioritize outreach, segment accounts, and maintain a reliable cadence without adding headcount just to chase invoices.

If you're still running collections out of inboxes, shared spreadsheets, and ad hoc reminders from account leads, your issue isn't a lack of financing products. It's process fragmentation.

What about QuickBooks shops

A lot of firms in the $3M to $50M range still anchor finance operations in QuickBooks.

That's fine, until AR complexity starts outrunning the bookkeeping stack. QuickBooks AR automation can improve follow-ups and visibility, but the true value comes when the workflow around billing, reminder timing, dispute tracking, and payment capture is managed as an operating system rather than a series of manual tasks.

For firms evaluating process upgrades, these accounts receivable management tips are a solid external reference point. They're especially useful if you're trying to tighten internal discipline before reaching for outside financing.

A blunt comparison

Option | Best use case | Main trade-off |

|---|---|---|

Factoring | Immediate cash need tied to specific invoices | Higher cost and less control over collections |

Invoice financing | Need liquidity while preserving more customer control | Still adds financing complexity |

Business loan or line | Broader capital need not tied to invoices | Debt burden and underwriting friction |

AR automation | Ongoing effort to improve cash conversion operationally | Doesn't create instant cash on day one |

If your firm is healthy but slow to collect, operational repair usually beats financial engineering.

One factual example of a platform in this category is Resolut, which combines credit risk assessment, collections workflows, dynamic billing, payment options, and automated cash application in one AR operating layer for B2B teams.

Visual ideas for leadership review

- Comparison matrix slide: Cost, control, client experience, implementation speed, and long-term scalability across factoring, loan, and AR automation.

- Cinematic image: Partner meeting with aging report on screen, showing the shift from reactive financing to controlled collections operations.

Making the Right Choice for Your Firm's Financial Health

A factoring accounts receivable company can be the right move. But only in the right situation.

Use it when speed is essential, the invoices are clean, the clients are creditworthy, and the cash need is specific. Don't use it to hide weak billing discipline, delayed invoicing, soft collections, or poor payment workflows. That just turns an operating problem into a recurring financing expense.

My recommendation for professional services firms

If you're in a short-term pinch, evaluate factoring with rigor and assume the client experience matters as much as the fee.

If your receivables issues show up month after month, skip the financial workaround and fix the system. Tighten invoice timing. Standardize follow-up. make escalation rules explicit. Give clients easier payment paths. Clean up dispute handling. Build a process that lets finance lead collections without burning relationship capital.

That's how you improve cash flow with control.

A practical decision rule

Choose factoring if all three are true:

- You need cash now

- The invoices are collectible

- The situation is temporary

Choose AR process redesign if any of these are true:

- Invoices go out late

- Collectors rely on manual reminders

- Partners escalate inconsistently

- Cash application and dispute tracking are slow

- Client payment behavior is visible only after the invoice is already old

The best finance operators don't just ask how to get paid. They build systems that help the firm get paid faster, with less friction, and with better data.

That's the standard to hold.

If your firm wants to improve collections without outsourcing the client relationship, Resolut is built for that operating model. It automates AR for professional services with structured workflows across billing, follow-up, payment capture, and cash application, while keeping the process consistent, accurate, and human.