GDPR Compliance: A CFO's Guide to Risk & Cash Flow

Master GDPR compliance for finance & AR teams in 2026. This guide for CFOs covers data rights, breach response, & a checklist to boost cash flow.

A client asks to be erased from your systems. Their invoice is still unpaid. Your team has sent reminders from Outlook, logged notes in the CRM, issued the invoice from QuickBooks, and stored the engagement letter in a shared drive. Nobody is trying to mishandle data, but nobody can say with confidence where that client's information lives or what must be retained.

That's where GDPR compliance stops being a legal memo and becomes a finance operations problem.

For firms in the $3M to $50M range, this usually shows up inside ordinary work. A partner forwards an email thread to collections. A controller exports an aging report with contact names. An outsourced bookkeeper keeps copies of invoices longer than anyone intended. If you're using accounts receivable automation, AI AR automation, or even basic QuickBooks AR automation, the issue isn't just whether the tool works. It's whether your process is controlled.

Finance leaders already know how to build controls around approvals, cash application, and write-offs. GDPR asks for the same discipline around personal data. If you manage it well, you can reduce DSO, improve cash flow, and keep client communication efficient without turning AR into a compliance bottleneck.

Why GDPR Is a Finance and AR Issue

Consider a common tension. A former client disputes a fee, stops responding, and then submits a request tied to their personal data. Finance wants the receivable collected. Operations wants the file closed. Legal wants caution. Most firms discover, at that moment, that invoice data is spread across too many systems to act quickly.

That delay has a cost. Collections slow down. Staff spend time searching inboxes and shared folders. People improvise. Improvisation is what breaks controls.

Where finance gets exposed

In professional services, AR holds more personal data than many finance teams realize. Names, email addresses, job titles, payment contacts, billing notes, dispute comments, and bank-related correspondence all move through the receivables process. Even if your firm isn't selling consumer products, your AR workflow may still process personal data.

The practical issue isn't abstract privacy theory. It's operational reliability.

- Outstanding invoices: Teams need a clear basis for what billing data must stay accessible while an account is open.

- Follow-up activity: Reminder emails, call logs, and ticket notes often sit outside the accounting system.

- Retention decisions: Staff may delete too much, or keep too much, because nobody has defined the rule.

A strong AR control environment helps here. If your team already reviews segregation of duties, approval paths, and exception handling, this is a natural extension of that discipline. A useful starting point is a finance-focused review of accounts receivable internal controls.

Practical rule: If finance can't explain where client billing data sits, who can access it, and why it's being retained, GDPR compliance is already weaker than it looks.

There's also a physical layer that finance teams often miss. Old laptops, retired drives, and replaced office hardware can still contain invoice history, contact details, and exported reports. For firms that need a sensible operational reference, Handling retired IT assets securely is worth reviewing.

The broader point is simple. GDPR compliance in AR isn't about making collections softer. It's about making collections more controlled.

GDPR Fundamentals for Financial Leaders

Month-end close is two days away. A client disputes an invoice, asks what personal data you hold, and your collections notes sit across the ERP, shared inboxes, and a payment portal. Finance now has two jobs at once. Protect cash flow and prove the process around that data is under control.

CFOs do not need to become privacy specialists. They do need a workable operating model for how AR data is collected, used, retained, and shared.

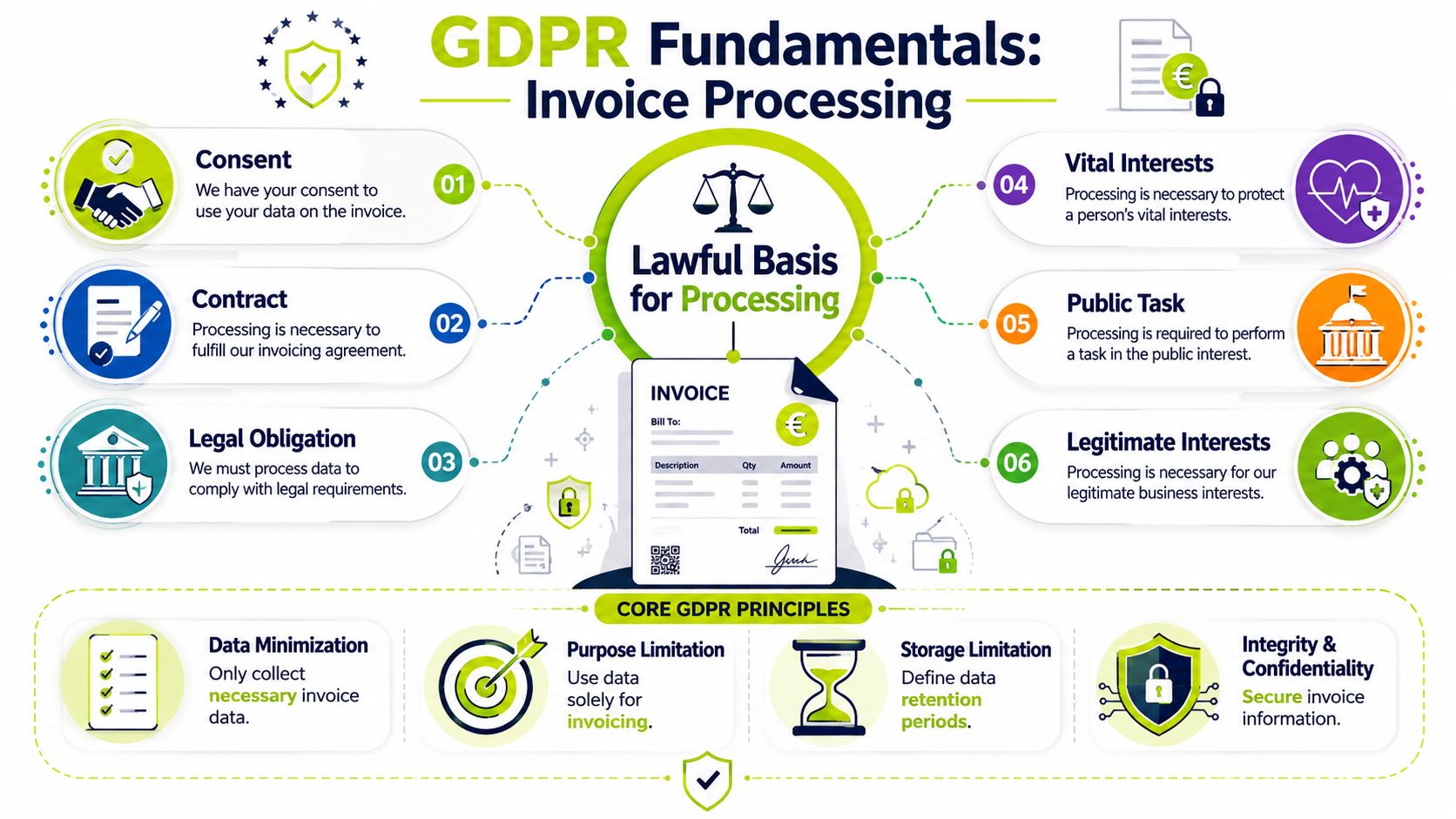

At the center is lawful basis. In AR, teams often reach for consent because it sounds safe. In practice, billing, cash application, collections activity, and recordkeeping usually rest on the underlying client relationship and related obligations. That distinction matters because consent can be withdrawn, while invoice processing still has to continue if there is a valid business and legal reason to keep going.

The two concepts finance teams need most

Your firm acts as the controller. It decides why invoice data is collected, how it is used, how long it is kept, and which systems touch it. Your software vendors are usually processors. They handle data on your behalf, but they do not take over your responsibility for policy, oversight, or response when something goes wrong.

The practical comparison is straightforward. The controller role works like a general contractor managing the job. Processors do pieces of the work. If a subcontractor makes a mess, the client still expects the general contractor to fix it.

That is why vendor adoption is never the end of the discussion for finance. An AR platform may improve collections cadence. A payment tool may reduce manual handling. An outsourced support team may extend coverage hours. None of that transfers accountability for how personal data is processed inside the workflow.

Why this belongs on the finance risk register

The financial exposure is large enough to merit CFO attention. GDPR allows for significant penalties, and certain personal-data breaches must be reported within 72 hours of awareness. That reporting clock is an operating requirement, not a legal footnote.

Early enforcement activity also showed that regulators were dealing with high volumes of complaints and breach notifications soon after the regulation took effect on 25 May 2018, according to Varonis' GDPR first-year review. For finance leaders, the lesson is simple. Weak data discipline in AR can become a regulatory issue fast, especially when teams rely on side spreadsheets, inbox rules, and undocumented retention habits.

Finance question | GDPR lens | Practical meaning in AR |

|---|---|---|

Why are we storing this contact? | Lawful basis | Tie the data to billing, service delivery, collections, or a defined obligation |

Who sets the workflow rules? | Controller role | Your firm owns the decision-making and oversight |

What does the vendor actually do? | Processor role | The tool helps process data, but accountability stays in-house |

How fast must we react to a breach? | Reporting obligation | Incident response needs ownership, escalation paths, and a clock that starts immediately |

Good GDPR compliance looks a lot like good controllership. Purpose is defined. Decisions are documented. Access is limited. Exceptions are visible.

That framing helps finance make better trade-offs. AR teams still need effective reminder sequences, usable contact records, and enough history to resolve disputes. The goal is not to strip friction out of collections by keeping everything forever. The goal is to keep the data that supports cash collection, remove what no longer has a justified purpose, and document the rule so staff can follow it consistently.

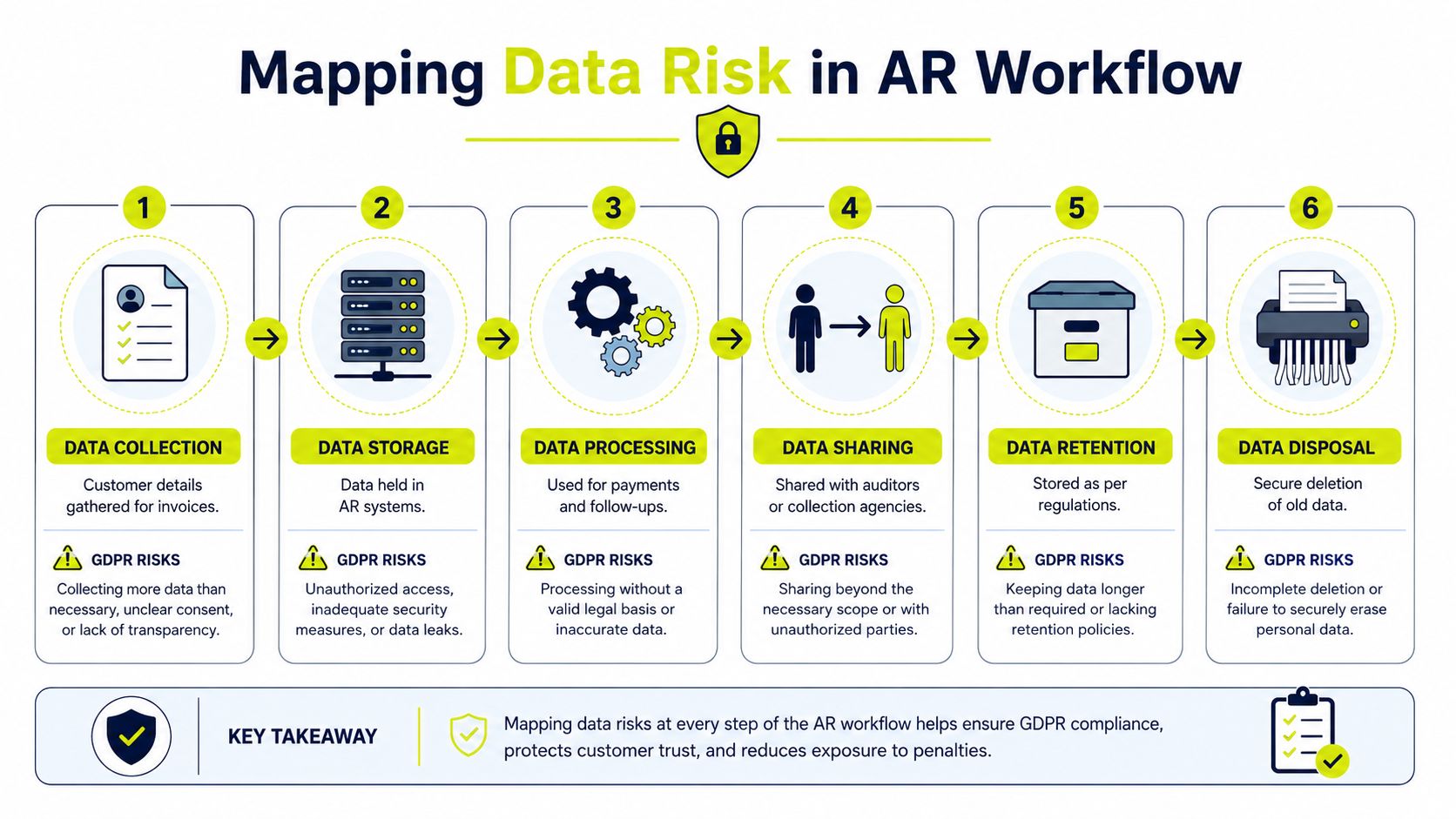

Mapping Data Risk in Your AR Workflow

Most finance teams can't fix what they haven't mapped.

GDPR compliance is heavily driven by data mapping and lawful-basis tracing. Organizations should inventory what personal data they collect, where it flows, who can access it, which third parties receive it, and when it's erased, according to BitSight's GDPR compliance checklist. In AR, that means following the entire invoice lifecycle, not just the accounting entry.

The AR data trail

A typical professional services workflow starts clean and gets messy fast.

Client onboarding may begin with an engagement letter, intake form, W-9 request, or billing setup email. Then the data branches out. Contact details move into QuickBooks, a PSA platform, a CRM, shared inboxes, and perhaps a hosted payment page. As invoices age, collections notes appear in email threads, call logs, spreadsheets, and support systems.

By the time someone asks, "Where do we have this person's data?" finance often has five partial answers and no complete one.

A practical map by workflow stage

Use the AR process itself as the mapping structure.

- Client setup Capture what personal data enters the firm first. Usually that's billing contacts, signatories, and communication preferences.

- Invoice creation Identify what data appears on invoices, statements, and attachments. Many firms include more identifying detail than necessary.

- Collections activity Review reminders, dispute notes, call summaries, and escalation records. Shadow data tends to grow in these areas.

- Payment processing Document what sits in the accounting platform versus the payment gateway. Finance teams should know whether they are storing sensitive payment-related information locally or passing it through.

- Reporting and analysis Aging reports, cash forecasts, and partner dashboards often include named contact data. Ask whether those reports need it.

- Archiving and disposal Define where closed-account records move and how deletion is triggered.

A short working table helps teams spot risk quickly:

AR stage | Where data usually sits | Common control gap |

|---|---|---|

Onboarding | Email, CRM, file storage | Duplicate records with no owner |

Billing | ERP or QuickBooks | Extra personal detail on invoice fields |

Follow-up | Inbox, AR software, spreadsheets | Notes stored outside governed systems |

Payment | Gateway, bank reports, accounting system | Unclear boundary between processor and firm records |

Reporting | BI exports, PDFs, board packs | Broad internal access |

Retention | Archives, local drives, old hardware | No defined deletion trigger |

The point of this exercise isn't paperwork. It's architecture.

Once the map is clear, privacy by design becomes practical. You can limit data collection, tighten access, define retention, and structure accounts receivable automation so it reduces manual chasing without multiplying unmanaged copies of client data. That's where GDPR compliance starts helping operations instead of slowing them down.

Handling Key GDPR Obligations in Practice

A payment reminder goes to the wrong contact on a Friday afternoon. By Monday, finance is sorting through mailbox threads, exported reports, and AR notes to work out what was sent, who saw it, and whether the issue needs escalation. That is what GDPR looks like in practice for an AR team. It is an execution problem inside a cash collection process.

The operational question is simple. Can the team respond to requests, incidents, and process changes without slowing collections or creating more data sprawl? Strong GDPR handling in finance protects cash flow because it reduces rework, cuts avoidable escalation, and keeps customer communications controlled.

DSARs are an operations test

Data subject access requests expose process weakness fast. In AR, customer data rarely sits in one place. It shows up in invoice PDFs, collections notes, shared inboxes, support tickets, call summaries, and reporting exports. Guidance from DataGuard's DSAR guidance explains the obligation well. The hard part for finance is running the same search and review process every time.

Ad hoc responses fail for a predictable reason. Each person searches their own tools, applies their own judgment, and misses records stored outside the core system. That creates delay, inconsistency, and unnecessary risk.

A finance-ready DSAR process should include:

- Central intake: Send requests into one monitored queue with an owner and backup cover.

- Identity verification: Confirm the requester before releasing, correcting, or deleting anything.

- System inventory: Keep a standing list of every system AR uses, including inboxes, archives, and exports.

- Review and redaction: Remove third-party information before producing records.

- Decision log: Record what was disclosed, what was withheld, and the basis for each decision.

For finance leaders, the control point is repeatability. If the team cannot execute the workflow during month-end or while chasing overdue balances, the process is too fragile.

Breach response needs a finance clock, not a month-end clock

Finance teams are built around close cycles, approvals, and reconciliations. Breach response runs on a much shorter timeline. As noted earlier, GDPR expects prompt assessment and, where required, notification within a defined window. Waiting for the next scheduled review is not a workable approach.

Keep the response protocol short enough to use under pressure:

- Contain the issue: Stop the mistaken send, revoke access, or pause the sync.

- Escalate quickly: Finance, IT, security, and legal should know who gets the first call.

- Preserve evidence: Save the email chain, audit log, export file, or ticket history.

- Assess impact: Identify what personal data was involved, whose data it was, and whether the exposure is likely to create harm.

- Document timing: Record when the team became aware and what happened next.

This matters in ordinary AR work. Misaddressed statements, exposed spreadsheet exports, and overbroad access to aged debt reports are more common than dramatic cyber events. The firms that handle these well usually have a short incident playbook, named owners, and audit trails that finance can access without waiting on three other teams.

Physical records and retired devices belong in the same control set. Old laptops, archived drives, and office equipment can still hold customer and payment data. Standards-based references such as Beyond Surplus data destruction standards give teams a practical benchmark for disposal procedures.

A clear public notice supports this work because it sets expectations about data use, retention, and individual rights. It also gives finance a simple way to check whether internal practice matches external commitments. A well-structured privacy policy example for AI and finance operations shows how those commitments can be presented plainly.

A short explainer can help teams socialize the workflow internally:

DPIAs for finance projects

A Data Protection Impact Assessment is a pre-launch risk review for higher-risk processing. Finance teams do not need to treat it as a legal memo. They need to use it before new AR automation changes how customer data is collected, combined, scored, or routed.

That includes projects such as AI-driven collections workflows, centralized debtor communication tools, or integrations that pull invoice and contact data across multiple systems. The useful questions are operational:

Question | Why finance should care |

|---|---|

What new data is being collected or inferred? | Extra fields and derived signals create retention and access problems later |

Who can see it? | Permissions tend to widen after launch |

Can the workflow be explained clearly? | Opaque automation is harder to review, challenge, and defend |

Can the process be limited by design? | Tighter scope reduces both risk and admin effort |

A good DPIA saves time. It forces the team to catch scope creep, permission issues, and vendor dependencies before they hit collections, customer service, and audit.

Vetting Your AR and Finance Software Vendors

Finance leaders sign the contracts, approve the spend, and inherit the consequences. Vendor diligence for GDPR compliance shouldn't sit off to the side as a legal appendix. It belongs in software procurement.

This matters even more when a firm is adding accounts receivable automation to reduce DSO and improve cash flow. Speed is useful. Unexamined data handling is not.

What to ask before you buy

Under GDPR Article 32, controllers and processors must implement appropriate technical and organisational measures matched to risk, and the regulation explicitly names controls such as pseudonymization, encryption, and the ability to restore availability and access to personal data after an incident, according to GDPR Article 32.

That gives finance teams a practical lens for vendor review. Ask direct questions:

- Security design: How is personal data encrypted, segmented, and protected in transit and at rest?

- Access control: Which roles can see contact details, notes, and payment information?

- Resilience: How does the vendor restore availability after an incident?

- Sub-processors: Which downstream providers touch your data?

- Notification process: How quickly will the vendor alert you to an incident?

- Deletion support: Can they support retention schedules and deletion requests in a controlled way?

The procurement view that works

Too many software reviews focus on features first and data handling second. For AR software for professional services, reverse that order.

A useful comparison looks like this:

Vendor question | Weak answer | Strong answer |

|---|---|---|

Where does our data go? | "It's in the cloud" | Clear system architecture and processor list |

How do you handle incidents? | "We take security seriously" | Defined notification path and response process |

Can we manage retention? | "You can export data" | Documented retention and deletion controls |

Who can access what? | "Admins control permissions" | Granular, role-based access with auditability |

Vendor rule: If a provider can't explain its processor chain, incident workflow, and deletion controls in plain language, finance should assume the operational burden will fall back on the firm.

A formal data processing agreement matters, but don't stop there. Review whether the contract matches the actual workflow. If the product sends payment reminders, stores communication history, and syncs with your ledger, the paper has to reflect that reality.

Payment flow is especially important. Hosted payment architecture can reduce risk when it keeps sensitive actions inside a controlled environment rather than scattering payment details across emails and attachments. This is one reason many firms prefer a hosted payment gateway approach over improvised payment collection methods.

The finance takeaway is simple. Your vendor stack is part of your control environment. Treat it that way.

A Practical GDPR Compliance Checklist for AR Teams

AR teams don't need another abstract framework. They need a working checklist that fits billing, follow-up, and payment operations.

Use this as a live control list, not a one-time exercise.

Daily controls inside the workflow

- During client onboarding, limit fields. Collect what's needed for invoicing, service delivery, and collections. Don't ask for extra personal details because a form builder made the fields available.

- For lawful basis, tie each workflow to a reason. Billing records, reminder activity, and payment reconciliation should map to a defined business purpose. If a field or process has no clear basis, remove it.

- In invoice design, keep it lean. Many firms place too much identifying detail on invoices and attachments. Include what the client needs to process the bill, not every internal note tied to the account.

- For email collections, standardize templates. Free-form follow-up creates inconsistent disclosures, uneven tone, and unnecessary data exposure.

Team controls that reduce friction

Some controls live in behavior, not software.

- Use one system of record for collection notes. If staff keep separate spreadsheets or inbox folders, DSAR handling and internal review become harder.

- Restrict report access. Aging reports, dispute logs, and cash forecasting packs often circulate widely. Limit named client data to the people who need it.

- Set retention rules for closed matters. AR teams are good at keeping records. They're often less disciplined about ending retention at the right point.

- Train staff on exceptions. The risky moments are unusual ones. Wrong recipient, duplicate contact, former client dispute, partner override, manual export.

Clean AR processes usually improve both compliance and collections. Teams chase faster when they aren't hunting across inboxes, drives, and side spreadsheets.

A CFO review list each quarter

A short quarterly review keeps GDPR compliance tied to operating control.

Review item | What to check |

|---|---|

Data map | New systems, new exports, new payment flows |

Access rights | Former staff, temporary roles, outsourced users |

Templates | Reminder content, privacy language, escalation wording |

Retention | Whether deletion or archiving rules actually ran |

Vendors | Contract changes, sub-processor updates, workflow drift |

If you're using QuickBooks AR automation or layering new AI AR automation on top of existing accounting tools, run the same checklist against the whole stack. The common failure isn't bad intent. It's process drift. A manual exception becomes a habit, then a hidden system.

For finance leaders, the aim isn't maximal restriction. It's proportionate control. Enough structure to protect client data and support GDPR compliance, without making it harder to improve cash flow.

Compliance as a Competitive Advantage

Well-run firms make back-office discipline visible. Clients notice when billing is clear, reminders are professional, payment steps are straightforward, and data handling feels controlled.

That doesn't happen by accident. It comes from governance that is proportionate to the business. Not performative. Not bloated.

There's also a real strategic upside. Firms that treat GDPR compliance as an operating system tend to make better software choices, cleaner handoffs, and faster decisions. They avoid the trap of over-implementing controls that create unnecessary drag, a concern raised in work on the unintended consequences of GDPR from the GWU Regulatory Studies Center. In practice, that means fewer awkward workarounds and less friction in receivables.

For teams that want a broader operational reference point, a checklist-style view of unified GDPR compliance management can help frame the work across systems instead of treating each request or incident as a one-off.

The best finance organizations don't separate compliance from cash flow. They build AR processes that support both.

Resolut automates AR for professional services, helping firms reduce DSO and improve cash flow with workflows that stay consistent, accurate, and human. If you're looking for accounts receivable automation, AI AR automation, or QuickBooks AR automation that supports disciplined operations without making client communication colder, learn more at Resolut.