NSF Banking Meaning: A Guide for Finance Leaders

Understand the NSF banking meaning for B2B finance. Learn how to handle returned payments, reduce DSO, and improve cash flow with strategic AR automation.

A client payment was supposed to settle today. Cash was already mentally allocated. Payroll, partner draws, software renewals, and that month-end transfer all assumed the deposit would clear.

Then the remittance fails.

In most firms, that moment gets treated as a banking nuisance. It isn't. For a controller or CFO, nsf banking meaning has less to do with a bank fee and more to do with operational control. A payment didn’t just bounce. Forecast accuracy weakened, collections work expanded, and a client relationship just entered a more delicate phase.

That matters even more in professional services. We’ve already delivered time, advice, or project work. There’s no inventory to pull back. Once the payment fails, finance has to recover cash without turning a good client into a bad conversation.

An NSF Is More Than a Fee It's a Cash Flow Disruption

A practical example makes the point faster than a textbook definition.

A law firm sends a monthly invoice to a long-standing client. The client pays by ACH. The payment shows as initiated, so the AR team clears part of the follow-up queue and assumes the account is moving toward current status. A day later, the bank return comes through. Non-sufficient funds.

Now three things happen at once.

The cash forecast is wrong. The invoice stays open. Someone on the team has to unwind the posting, notify the account owner, and start collection activity again. That’s a lot of process friction from one failed payment.

Why B2B teams feel this more sharply

Consumer articles usually stop at “your bank declined the transaction.” That definition is accurate, but incomplete for an operating finance team.

In a professional services firm, an NSF event can affect:

- Liquidity planning: The receipt we expected today may now arrive much later, or through another payment method.

- Partner confidence: Leadership asks why cash came in light against forecast.

- Client handling: We need to collect firmly without embarrassing a client contact who may not control treasury.

- DSO discipline: One failed payment can keep an otherwise current account aging longer than it should.

Experian’s context for AR teams is useful here. It notes that 1 in 10 invoices go unpaid and ties unpaid invoices to $200B in annual enterprise waste, while also noting that a bounced check can extend DSO by weeks for businesses waiting on payment (Experian on nonsufficient funds and unpaid invoices).

The operating lesson

An NSF isn’t just “client didn’t have enough money.”

Sometimes it is. Sometimes it’s timing, account selection, treasury sloppiness, or an autopay setup that failed at the wrong moment. Finance teams get into trouble when they treat every NSF as the same type of risk.

Practical rule: Record the event as a payment failure first, not as a client character judgment.

That mindset leads to better next actions. We preserve cash discipline and relationship discipline at the same time.

What Is an NSF in Banking and Payments

At the banking level, NSF means non-sufficient funds. The payer’s bank declines the transaction because the account doesn’t have enough available funds to cover it.

For the business receiving payment, the key point is simple. The payment does not go through. You don’t have cash. Your invoice remains unpaid.

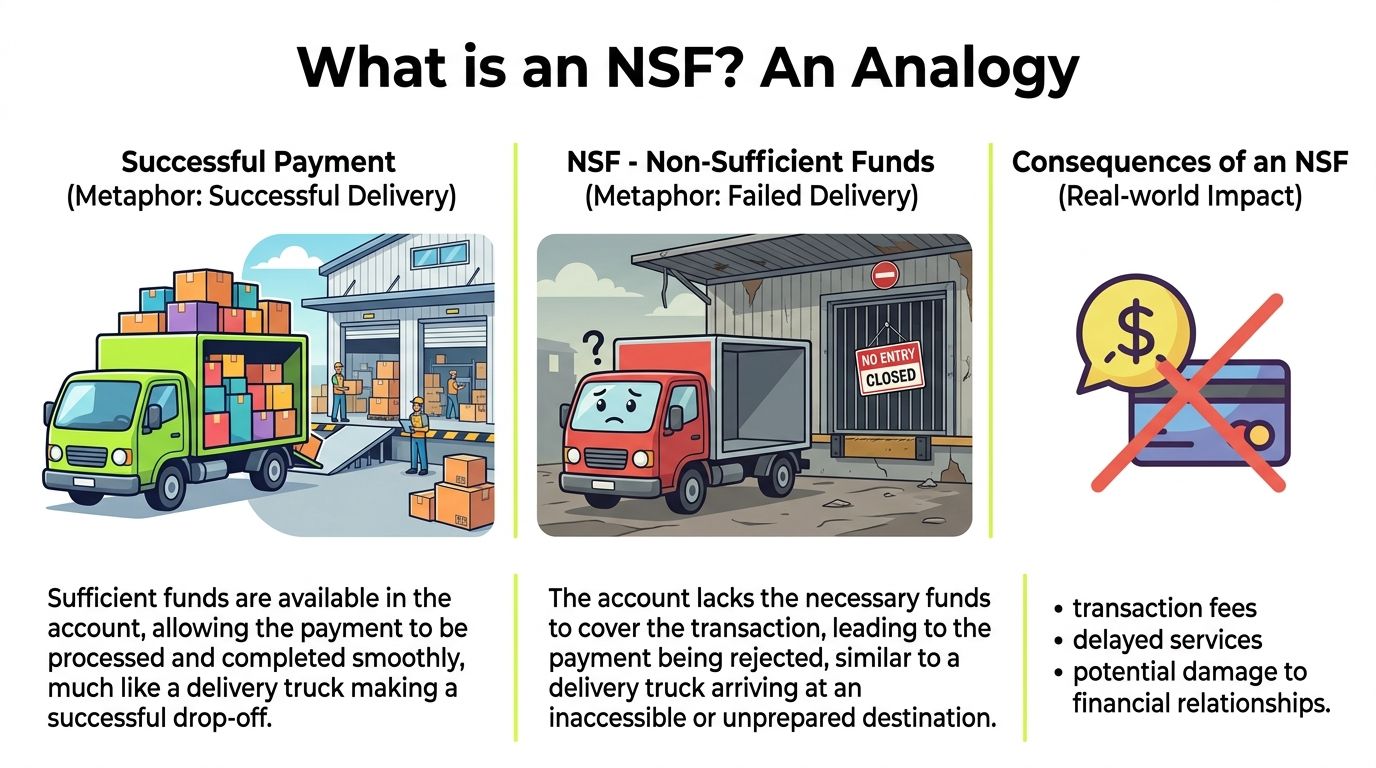

A simple analogy that fits finance operations

Think of a payment like a delivery truck arriving at a warehouse.

If the warehouse is open and staffed, the delivery is accepted. Payment settles.

If the truck arrives and the warehouse is empty or closed, delivery fails. That’s an NSF. The bank attempted the handoff and rejected it because the funds weren’t available.

That’s different from an overdraft. In an overdraft, the bank accepts the delivery anyway and lets the account go negative.

It’s also different from a payment that first settles and is later reversed for another reason. AR teams need separate workflows for those cases. If you want a clean primer on ACH movement itself before building those workflows, this overview of what ACH credit means is worth keeping in your team’s process notes.

What changed on the banking side

The fee story has shifted a lot.

The average NSF fee in 2024 was $17.72, and recent averages have ranged from $16.82 to $19.94 across institutions. At the same time, the CFPB reports that among banks with more than $10 billion in assets, 97% of NSF fee revenue has been eliminated, and consumers are saving nearly $2 billion annually on a going-forward basis. All banks with more than $75 billion in assets have stopped charging NSF fees, according to the Remitly summary of CFPB findings (Remitly on NSF charge meaning).

For businesses, that creates a subtle shift. Banks may be collecting less fee revenue, but the payee still deals with the failed payment.

NSF vs Overdraft vs Returned Payment

Failure Type | What Happens to the Payment | Who is Primarily Penalized | Impact on Your Business (The Payee) |

|---|---|---|---|

NSF | The bank declines it before completion | Usually the payer, and sometimes the payee through return-related bank charges | Invoice stays open, cash doesn’t arrive, AR follow-up restarts |

Overdraft | The bank covers it and the payer account goes negative | Primarily the payer | You usually still receive funds, so AR impact is much lower |

Returned payment | Payment may have appeared successful, then is reversed or returned later | Depends on cause and payment rail | Reconciliation gets harder, and root-cause analysis matters before outreach |

If the transaction was declined outright, treat it as a collection event. If it settled and then reversed, treat it as a reconciliation and dispute event until proven otherwise.

That distinction saves time and prevents sloppy follow-up.

The Ripple Effect of a Single Failed Payment

One failed payment rarely stays contained to one line on a bank statement.

The visible part is the return. The expensive part is the cleanup around it.

What breaks first

Start with the ledger.

Cash was expected. The receipt may have been posted. Now AR has to reverse the payment application, reopen the invoice if necessary, and confirm the aging is accurate. If the client has multiple open matters or projects, misapplication risk goes up quickly.

Then comes communication. Someone has to contact the client, explain the issue, ask for replacement payment, and decide whether future terms need to change.

Sage notes that when a customer payment results in an NSF, it directly extends DSO and delays cash flow. It also notes that 39% of checking accounts no longer charge NSF fees, but businesses receiving declined payments still face returned item fees, late fees, and administrative costs that often exceed the initial bank penalty (Sage on NSF checks and business impact).

Why the soft costs matter more than the bank fee

A firm can absorb a modest returned-item charge. What hurts is the chain of manual work:

- Reconciliation effort: AR and accounting need to correct the cash posting and invoice status.

- Collection time: Follow-up starts again, often with more urgency and more internal visibility.

- Forecast distortion: Near-term cash assumptions have to be revised.

- Client friction: The account manager may now need to step in.

A good reference point is this discussion of cash flow problems in business. An NSF is a small event on paper, but it behaves like a larger cash-flow problem because timing gets disrupted at exactly the wrong moment.

A controller’s view of true cost

If a meaningful client invoice fails, we don’t just lose time. We lose confidence in the reliability of expected cash.

That changes decisions. We may hold discretionary spending. We may delay a vendor payment. We may push harder on another customer because the first receipt didn’t land.

The bank event is brief. The operating consequences can last for the rest of the month.

That’s why mature AR teams track failed payments as a process issue, not just a collections annoyance.

An Action Plan for Your AR Team After an NSF

The best response to an NSF is calm, scripted, and fast. Not aggressive. Not passive.

When teams improvise, they either overreact and strain the client relationship, or they underreact and let the receivable age.

Step one is internal triage

Before contacting the client, get the accounting right.

- Reverse the payment cleanly. Reopen the invoice or remove the receipt application so the AR aging is accurate.

- Tag the failure reason. Don’t use a generic “payment failed” note if the bank return identifies NSF. The reason affects your next step.

- Check account history. Is this a first-time timing issue or part of a pattern? Your tone and escalation should reflect that.

- Alert the right internal owner. For professional services firms, that may be the partner, engagement manager, or account lead.

Step two is client outreach with the right tone

The first message should be factual and easy to act on.

Use language like this:

We attempted to process payment for invoice [number], and the transaction was returned by the bank for non-sufficient funds. We’ve reopened the balance. Please confirm the best date and method to resubmit payment. If helpful, we can provide an alternate payment option today.

That works because it doesn’t accuse anyone of bad faith. It states the issue and asks for a concrete next step.

For teams tightening their communication standards, this guide to managing customer communication is useful. NSF follow-up should sound controlled, not emotional.

Step three is deciding whether to retry

Automatic retry sounds efficient. It often isn’t.

Forte’s discussion of ACH NSF returns makes an important point. Some returns happen because of timing issues such as delayed deposits, pending transfers, or holiday clearing delays, and repeated re-presentment without better information can stack fees and damage the relationship.

Use a simple decision filter:

- Retry soon if the client confirms funds will be available on a specific date.

- Pause retry if the client is unclear, unresponsive, or already has multiple failed attempts.

- Switch methods if urgency matters more than convenience. Card, wire, or portal payment may be better than repeating the same failed path.

If your team handles more complex recovery scenarios, it’s worth reviewing practical payment representment strategies that explain when resubmission helps and when it just increases friction.

Step four is fee policy and terms enforcement

Many firms have the contractual right to pass through bank costs or returned-payment charges. Fewer firms apply that right consistently.

Use judgment.

If this is a first incident from a strong client and the payment is quickly corrected, waiving the internal hassle cost may be the right commercial call. If it’s recurring behavior, enforce the policy and move the client to stricter payment terms.

A workable policy often includes:

- First event: notify, recover payment, document.

- Repeat event: add fee recovery if contractually allowed.

- Chronic event: require alternative payment method or prepayment.

Step five is escalation

Not every NSF belongs in collections on day one.

Some belong with the relationship owner. Others need controller-to-controller contact. A few need legal review if the account is already strained and other balances are aging.

Escalate based on pattern, exposure, and client responsiveness.

Operating advice: Escalate when behavior repeats, not when emotions rise.

That keeps the process fair and easier to defend internally.

Shifting from Reactive Recovery to Proactive Prevention

Most firms don’t need a heroic collections team. They need fewer preventable payment failures.

That starts before the invoice goes out.

Consumer fee changes don't protect the payee

Capital One’s consumer-facing discussion highlights a useful B2B point. While major U.S. banks are increasingly waiving consumer NSF fees, the volume of returned ACH items in B2B has risen, and it notes that 20% of SMBs misjudge balances. That leaves AR teams carrying more of the operational burden when autopayments fail (Capital One on NSF fees).

So prevention can’t rely on the bank’s fee policy. It has to live in our AR process.

Four controls that reduce surprises

Clear payment terms at engagement start

Spell out due dates, accepted payment methods, retry authorization, and returned-payment handling in the engagement letter or MSA.

Don’t bury this in boilerplate. If a client pays by ACH, confirm who owns treasury approval and account funding.

Pre-due reminders that are operational, not promotional

A short reminder before debit date or due date prevents a lot of avoidable failures.

The message should be plain: invoice amount, due date, payment method on file, and who to contact if the account needs updating.

Backup payment options in the portal

When ACH fails, the fastest recovery often comes from offering another path immediately.

A client who can switch from bank transfer to card or another approved method on the same day is easier to recover than one who has to restart the process through email threads.

Light credit and payment behavior review

Professional services firms often skip this because the client relationship feels strong.

That’s understandable, but risky. If a client regularly pays at the edge of terms, changes banking details frequently, or asks for exceptions often, we should tighten monitoring before an NSF happens.

What doesn't work

Three habits create repeat failures:

- Blind autopay trust: Assuming a saved bank account means future payments are safe.

- Manual follow-up only after failure: By then, we’re already behind.

- One-size-fits-all treatment: A good client with a timing issue shouldn’t get the same workflow as a chronically unstable payer.

Prevention is mostly process discipline. The payoff is fewer awkward calls, steadier collections, and better cash predictability.

Using AR Automation to Control Payment Failures

Manual discipline helps. It doesn’t scale well.

Once a firm has enough invoices, enough client entities, and enough payment methods in play, spreadsheet tracking and inbox-based collections stop being reliable. That’s where accounts receivable automation becomes less of a convenience and more of a control layer.

The technical problem manual teams miss

NSF returns on ACH aren’t always signs of nonpayment risk.

Forte explains that they can result from timing issues like delayed deposits, pending bank transfers, or clearing delays. It also warns that naive retry logic can trigger repeated fees and create unnecessary client friction. Its conclusion is the one finance operators should care about most: intelligent retry scheduling and pre-payment verification are essential for separating timing issues from true credit risk (Forte on NSF re-presentment and ACH complexity).

That’s the heart of the problem. A human AR clerk may know a client is usually good for it. The system still needs to act correctly at scale.

What effective automation does

Good AI AR automation doesn’t just send reminders. It makes different decisions for different failure patterns.

Look for workflows that can:

- Flag at-risk invoices early: Prior payment behavior, broken promises to pay, and recent failed transactions should change outreach timing.

- Route retries intelligently: Don’t hit the same account again without a reason to believe funds are available.

- Offer alternate payment paths immediately: A self-service portal can shorten the gap between failure and recovery.

- Coordinate outreach across channels: Email may be enough for one client. Another may respond faster to SMS or a direct account-owner prompt.

- Sync with accounting records: If you’re using QuickBooks, clean status updates matter. QuickBooks AR automation is most valuable when it keeps the ledger and outreach workflow aligned.

For firms modernizing the full finance stack, it also helps to understand how AR tools fit into broader cloud accounting solutions. The point isn’t to add software for its own sake. It’s to remove manual gaps between invoice, payment, exception, and reconciliation.

Where this fits for professional services firms

The operational sweet spot is straightforward. Use policy to set the rules, then use software to enforce them consistently.

That’s where AR software for professional services earns its keep. It supports recurring retainers, milestone invoices, partner visibility, and client-specific workflows without forcing the team to remember every exception manually.

One option in that category is Resolut, which combines credit risk assessment, collections orchestration, omnichannel outreach, dynamic billing, and cash application in one system. For firms trying to reduce DSO and improve cash flow, that kind of platform helps standardize response to failed payments instead of leaving each collector or bookkeeper to handle NSF events ad hoc.

Automation should not make your collections voice harsher. It should make your process more consistent.

That’s the key control gain.

Taking Control of Your Cash Flow Certainty

The core nsf banking meaning for a finance leader is simple. A payment was attempted, the bank declined it, and now the firm has to recover cash without losing accuracy or trust.

Handled poorly, an NSF turns into forecast noise, extra admin work, and a strained client conversation. Handled well, it becomes a contained exception with a clear response, clean ledger treatment, and tighter prevention controls going forward.

That’s the bigger takeaway. NSF risk isn’t fully avoidable, but it is controllable.

The firms that manage it best don’t rely on heroic follow-up. They build policy, communication discipline, payment flexibility, and automation into the AR process so failed payments don’t keep dictating the month.

Resolut automates AR for professional services with a practical focus on consistency, accuracy, and human control. If your team wants a steadier way to reduce DSO, improve cash flow, and manage payment failures without adding collection chaos, you can learn more at Resolut.