Statute of Limitations on Debt in Arizona: A CFO's Guide

Understand the statute of limitations on debt in Arizona for contracts, credit cards, and judgments. A guide for CFOs on managing AR and collection risk.

Your aged receivables report usually tells the truth faster than the income statement does.

If you run a professional services firm in Arizona, you've probably stared at a 90+ day bucket and asked the same questions every controller asks. Is this still collectible? Should we keep calling? Is legal review worth it? Or are we burning staff time on balances that won't convert to cash?

That's where the statute of limitations on debt in Arizona stops being a legal footnote and becomes a finance control. The rule affects when a creditor can still sue, when an account should move to legal review, and when your team needs to stop treating an old balance like an active recovery target. If your process doesn't reflect those timelines, your AR team can chase the wrong accounts, miss recoverable ones, and distort cash flow forecasting.

For firms trying to improve cash flow, reduce DSO, and put structure around collections, this is an operational issue first. The legal rule is just the boundary line. The actual work is turning that boundary into clean account classification, better escalation, and tighter accounts receivable automation.

The Financial Impact of Arizona's Debt Timelines

Aged AR isn't just an accounting report. It's a queue of decisions.

Every delinquent balance forces a choice. You can continue internal follow-up, escalate to counsel, negotiate, or write it off. In Arizona, that decision has to line up with the debt's legal timeline. Once the applicable period expires, a creditor generally loses the right to sue in court, even though collection efforts may continue outside litigation under the rules that apply to the situation.

For a CFO or firm owner, that changes how you look at old receivables. A balance that appears collectible from a relationship standpoint may be much weaker from a legal recovery standpoint. Another balance that the team assumes is stale may still be well within the window. That gap is where write-off errors and wasted labor show up.

What this changes in practice

The first operational mistake is treating all past-due balances as if they age the same way. They don't.

The second mistake is relying on “last activity” instead of the legally relevant event. In many firms, AR notes are inconsistent, collection history lives in email, and no one can quickly confirm the date that matters for escalation.

Practical rule: If your AR system can't show debt type and the event that starts the legal clock, you don't have a collections process. You have a memory problem.

That's why finance leaders should treat debt aging and legal aging as separate fields. Standard aging tells you how late the invoice is. Legal aging tells you how much runway is left for stronger enforcement options.

For multi-state firms, this gets more important. Arizona's rules don't line up neatly with neighboring states, which is one reason a state-specific collections playbook matters. If you manage receivables across jurisdictions, it helps to compare how timelines differ, such as in this discussion of Colorado debt limitation rules.

The measurable outcome that matters

You don't need another abstract compliance memo. You need cleaner prioritization.

When legal timing is built into AR workflow, teams spend more time on recoverable balances, less time on dead-end escalation, and more accurately reserve against doubtful accounts. That supports better forecasting, tighter write-off discipline, and a more credible cash flow plan.

Arizona's Debt Limitation Periods by Debt Type

A Phoenix consulting firm has two $18,000 balances that are both 14 months old. One sits under a signed MSA. The other came from extra work approved on calls and billed later. Same aging bucket. Different recovery profile.

That is the operating point in Arizona. Debt type determines the limitation period, and the classification decision affects reserves, escalation timing, and whether outside counsel gets a clean file or a fact dispute.

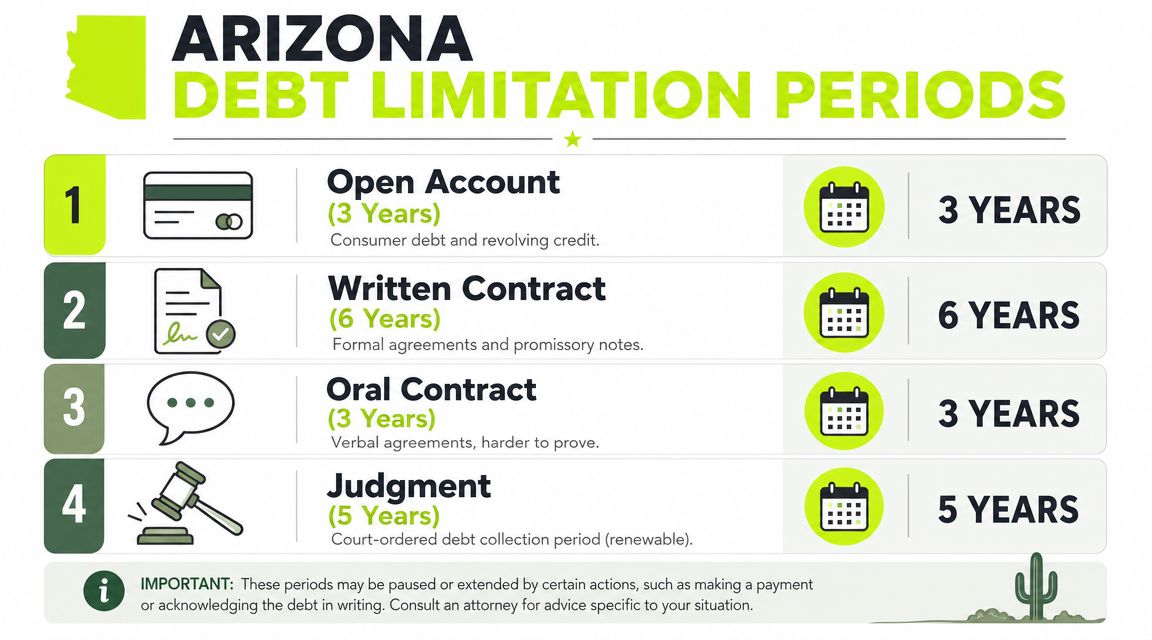

The core Arizona timelines

Arizona Judicial Branch guidance identifies these baseline periods: medical debt at 6 years, written contracts including most credit card debt at 6 years, oral debts at 3 years, auto loan debt with repossession at 4 years, and state tax debt at 10 years, as shown in the Arizona Judicial Branch debt limitation guidance.

For a professional services firm, the useful question is not "what is the rule in general?" It is "how should this account be tagged, routed, and worked this quarter?"

Debt type | Arizona timeline | Why the tag matters operationally |

|---|---|---|

Written contracts | 6 years | Usually the strongest category for firms with signed engagement letters, MSAs, SOWs, and fee agreements |

Most credit card debt | 6 years | Matters if the balance includes card-based obligations or reimbursements documented that way |

Medical debt | 6 years | Relevant for firms in healthcare and healthcare-adjacent billing environments |

Oral debt | 3 years | Shorter runway, weaker documentation, and faster need for review |

Auto loan debt with repossession | 4 years | A reminder that secured obligations follow different timelines than ordinary service AR |

State tax debt | 10 years | Outside normal client AR, but still relevant to enterprise risk tracking |

Judgment renewal | 5 years from entry, and renewal is required to keep the judgment enforceable under Arizona Judicial Branch debt limitation guidance | Post-judgment accounts need a separate control calendar, not standard invoice follow-up |

Written contracts usually deserve the most attention

For most firms, written contract receivables are the center of gravity. If engagement documents are signed, stored, and tied to the invoice record, the file is easier to place, easier to defend, and easier to value.

Arizona sets a 6-year period for actions for debt founded on a written contract, including most credit card debt. Keep the legal citation in your policy manual or counsel memo, then make the operational rule simple for staff: if the signed contract is missing from the account record, treat the file as higher risk until someone fixes it.

That trade-off matters. Teams often assume a client relationship is enough. It is not enough if the invoice references work that drifted beyond the signed scope, the renewal was never executed, or approvals happened informally. In those files, collection slows because AR, operations, and counsel spend time reconstructing the deal instead of enforcing it.

Common failure points include:

- Unsigned renewals. The original agreement exists, but later terms were extended casually.

- Scope drift. The invoice includes work that is only partly covered by the written terms.

- Hybrid billing structures. Retainer, hourly fees, and pass-through expenses sit in one balance with inconsistent support.

Each of those issues lowers confidence in recoverability. That should change how you score the account internally.

Oral agreements compress the window and raise proof risk

Arizona treats oral debt claims more narrowly, with a 3-year period under the same Judicial Branch guidance.

For a firm owner, that is a controls problem before it becomes a legal problem. A partner starts work before the paperwork is signed. A client adds a small project on a call. The invoice goes out, but the file does not contain a signed amendment or clear written acceptance.

Now the team has less time and a weaker record.

If your firm regularly bills work that begins before the contract is complete, set a rule. Either convert that work to a signed writing within a fixed number of days, or flag the account for earlier review at the 60-day or 90-day delinquency mark. That is how you prevent a documentation gap from becoming a write-off.

Judgment tracking needs its own calendar

Once an account becomes a judgment, standard AR aging stops being the main control. The key date is the judgment timeline itself.

Arizona judgments must be renewed within five years of entry to remain enforceable, according to the Arizona Judicial Branch debt limitation guidance.

I have seen firms win the case and then lose control of the asset. The judgment sits in a spreadsheet, ownership is unclear, and no one calendars the renewal deadline. From a finance standpoint, that is the same as letting collateral expire. The receivable may still appear collectible in theory while the enforcement path weakens in practice.

What to build into your AR system

A workable setup is straightforward if the policy is clear and the fields are mandatory.

- Tag debt type at intake. Written contract, oral agreement, judgment, secured claim, or another defined class.

- Store the legal trigger date. Do not rely on generic "last activity" fields.

- Separate invoice age from legal age. A 240-day invoice under a clean written contract should not be prioritized the same way as a 240-day invoice built on disputed verbal approvals.

- Require the agreement file. If staff cannot pull the signed contract in under a minute, the account is not ready for efficient escalation.

- Route by risk. If the debt type is unclear, move the account to review before it ages deeper into the queue.

AR software for professional services and QuickBooks AR automation can help only if your chart of accounts, client records, and document controls are consistent. Automation speeds up a good process. It also speeds up bad classification.

Restarting the Clock Tolling and Revival Rules

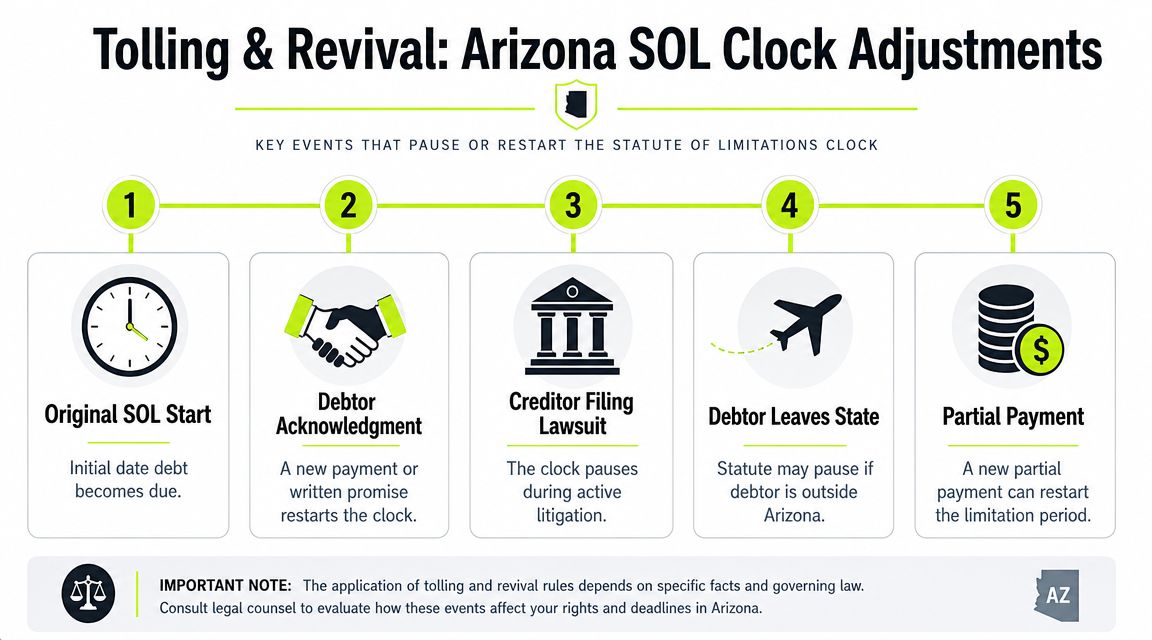

Arizona collection timing gets misunderstood when teams assume the clock is a simple countdown from invoice date. It isn't.

What matters is the legal trigger, and for some debts, later account events don't move the start date the way collectors expect. In such cases, old habits from charge-off logic or generic collection playbooks can lead finance teams in the wrong direction.

The credit card rule Arizona clarified

A major turning point came in 2018, when the Arizona Supreme Court decided Mertola, LLC v. Santos. The court clarified that for credit-card debt, the 6-year period starts at the first uncured missed minimum payment, not when the account is later charged off, as summarized in this explanation of Arizona debt limitation timing and Mertola.

For operators, the lesson is broader than credit cards. Don't build your workflow around accounting treatment if the legal trigger is different. Charge-off, write-down, or internal status changes may matter for reporting, but they don't automatically define the litigation window.

Partial payment is not a cure-all

This is another place teams get sloppy. Some collectors assume any payment restarts the clock.

Under the Mertola framework summarized in the same source above, a partial payment does not restart the clock unless it brings the account fully current, while a full cure can reset it. That's an important distinction because many firms note “client paid something” and mentally treat the account as refreshed.

It may not be.

A small payment can improve cash position without improving legal position. Your notes should reflect both.

What to track inside the file

You need a file history that supports decision-making, not just activity logging.

A useful record includes:

- The first missed required payment or default event tied to the governing agreement.

- Whether later payments cured the delinquency fully or were only partial.

- Whether the team is using accounting dates instead of legal dates in status reporting.

That sounds basic, but it's often where recoverability analysis breaks down. A collector sees recent communication and assumes the matter is “active.” Counsel sees the default history and recognizes the legal window is much tighter.

What doesn't work

The weak approach is relying on one of these shortcuts:

- Last invoice date

- Last email reply

- Charge-off date

- Last partial payment without cure analysis

Those are useful context fields. They are not reliable substitutes for the legally relevant starting point.

For firms using accounts receivable automation or AI AR automation, this is exactly the kind of rule that should sit inside the workflow engine. The system should flag accounts based on the event that matters, prompt staff to verify whether a payment cured the account, and prevent casual assumptions from steering legal escalation.

Operationalizing Collection Timelines in Your AR Workflow

Most firms don't struggle because they lack legal concepts. They struggle because the concepts never make it into daily process.

The cure is operational design. If Arizona timelines matter, your AR system should reflect them in routing, reminders, escalation, and review thresholds. Otherwise, your team is depending on spreadsheet memory and inbox archaeology.

Build the file once, use it many times

At minimum, each receivable should carry these fields inside QuickBooks, your PSA, or your AR layer:

Field | Why it matters |

|---|---|

Contract type | Determines the likely legal bucket |

Signed agreement on file | Supports enforceability and faster escalation |

Default or missed-payment date | Anchors legal aging |

Current collection stage | Aligns outreach with risk |

Assigned owner | Prevents orphaned balances |

Legal review flag | Separates ordinary dunning from counsel-ready files |

QuickBooks AR automation can do useful work when the source fields are clean. An automated workflow can't classify what no one captured.

Use stage-based workflows instead of generic reminders

A disciplined process changes tone and effort as the account ages.

For example:

- Early stage accounts: Standard reminders, payment links, confirmation of invoice receipt.

- Middle stage accounts: More direct outreach, dispute identification, senior contact involvement.

- Later stage accounts: File review, contract validation, legal-readiness check, reserve discussion.

That's the practical side of protecting revenue through dunning. The point isn't to send more emails. It's to send the right message, at the right point, with the right escalation path.

What finance leaders should automate

The highest-value automation is not flashy. It's controlled.

- Date-based flags: Alert the team when an account is approaching an internal legal review threshold.

- Document checks: Require the agreement, statement history, and contact log before escalation.

- Priority queues: Push recoverable, well-documented balances ahead of low-quality files.

- Exception handling: Stop routine cadence when a dispute, payment plan, or counsel review is active.

Operator note: Good automation reduces hesitation. When the system shows contract type, age, and next action clearly, collectors spend less time debating and more time executing.

A solid workflow also improves forecasting. When your team can separate “late but routine” from “aging toward legal risk,” expected collections become more credible. That helps controllers explain cash flow variance with more confidence.

If you need a baseline process map before layering in software, this guide to accounts receivable procedures for finance teams is a useful starting point.

What to avoid

Don't automate a weak policy.

If your current process treats every old balance the same, AR software for professional services won't magically reduce DSO. It will just send faster reminders to the wrong cohorts. First define the rules. Then automate the rules.

Compliance Pitfalls and Your Legal Escalation Strategy

A partner wants legal action on a client that is 14 months past due. The balance is large, the relationship is deteriorating, and the AR team is under pressure to "do something." If the file is missing the signed agreement, the aging trigger is wrong, or the account has drifted into a legally weak position, that push for escalation creates risk instead of recovery.

This section is where Arizona timing rules become operating controls for professional services firms. The question is not whether the invoice is still unpaid. The question is whether the account is documented well enough, classified correctly enough, and timed early enough to justify legal spend.

Where firms lose money and create exposure

The common failure is poor escalation discipline.

A collector uses lawsuit language before anyone confirms the debt category. A billing manager keeps an old account in the standard reminder sequence because no one changed its status. A partner promises hard action on a call, but finance has not reviewed the file for collectibility, dispute history, or legal age. Each of those mistakes increases compliance risk and wastes staff time on balances that may not support a strong legal path.

For firm owners, the trade-off is straightforward. Early review takes more effort up front. Late review raises the odds of bad messaging, weak files, and legal referrals with a low chance of recovery.

For broader context on consumer-facing collection boundaries and timing issues, even outside Arizona, this overview of Morgan & Morgan on debt collection rights is a useful reminder that collection rights narrow as debts age.

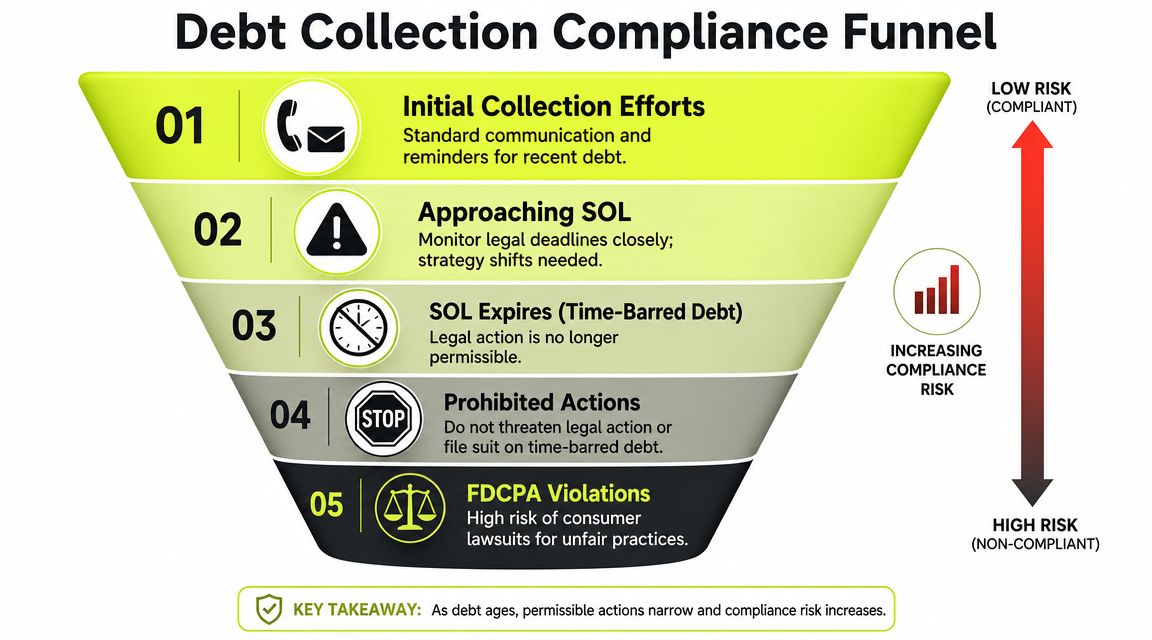

A practical escalation model for AR teams

Use a staged process that ties account age to control requirements, not emotion.

Stage | Finance action | Main control objective |

|---|---|---|

Early delinquency | Standard billing follow-up and client contact | Collect routine late payments at low cost |

Repeated delinquency | Confirm dispute status, decision-maker, and service acceptance | Avoid chasing the wrong issue |

Late-stage delinquency | Review contract, statements, notes, and prior promises | Build a file that can survive scrutiny |

Pre-legal review | Check legal timing, recovery likelihood, and approval authority | Keep weak accounts out of legal spend |

Near-barred or stale account | Restrict legal-threat language and route to exception handling | Reduce compliance exposure |

This model improves two measurable outcomes. It reduces avoidable counsel referrals, and it raises the share of legal placements that have complete documentation on day one.

If-then rules that hold up under pressure

Broad principles fail in collections. Teams need rules they can execute.

- If the signed agreement is missing, then stop legal escalation and assign a documentation task with an owner and due date.

- If the debt type is unclear, then freeze automated progression until a manager classifies the account.

- If the client has raised a service dispute, then move the account out of routine collections and into management review.

- If the balance is old enough to require legal-age review under your policy, then send it to counsel screening or internal legal review before any threat language is used.

- If the account is outside the litigation window or too close to justify filing costs, then remove lawsuit references from scripts, emails, and call notes.

Older accounts need tighter permissions. They also need better file quality.

Set authority limits before a partner tests them

In many firms, the actual compliance problem is not the collector. It is informal authority.

Relationship partners, practice leaders, and office managers often speak to clients before finance can review the account. If those employees can imply legal action without a file review, the firm loses control of both message and timing. Set a simple rule. Only designated finance leaders or counsel-approved staff can approve legal-threat language, and only after the account clears a checklist.

That checklist should include the governing agreement, statement history, dispute status, contact log, and a current assessment of whether legal escalation is commercially sensible. A $12,000 balance with clean documentation may justify fast review. A $12,000 balance with missing terms, disputed scope, and scattered notes often does not.

The role of specialized support

Outside help works best when the handoff is structured.

Use external recovery support when the file is complete, the client history is clear, and internal follow-up has hit its limit. If your team wants a reference point for how specialized firms structure handoffs, scoring, and escalation paths, this overview of a nationwide debt collection company for structured recovery workflows is useful.

What works in practice

What works:

- Restricted approval authority for legal-threat language

- File checklists before counsel review

- Status codes that separate disputed, legally reviewed, and stale accounts

- Queue logic that prioritizes recoverable balances over poorly documented ones

What fails:

- Open-ended chasing with no status change

- Verbal promises from partners that bypass finance controls

- Identical templates for fresh and old debt

- Legal escalation based on balance size alone

The firms that handle this well treat legal timing as part of AR operations. That keeps effort focused on collectible accounts, protects the client communication record, and improves cash flow by sending the right files to the right path at the right time.

A Disciplined Approach to Managing Aged Receivables

The statute of limitations on debt in Arizona matters most when it changes behavior inside finance.

For professional services firms, the practical playbook is straightforward. Classify the debt correctly. Capture the default-related event that matters. Keep the contract attached to the file. Route old balances through different workflows based on legal age, not just invoice age. That's how you improve cash flow without creating unnecessary compliance exposure.

A short operating checklist

- Know the bucket: Written contract, oral agreement, judgment, or another category.

- Track the right date: Not every recent payment or status change affects legal timing.

- Set escalation rules: Internal collections, manager review, counsel review, or write-off.

- Use automation carefully: Good accounts receivable automation supports policy. It doesn't replace it.

- Review old balances with discipline: The point is to reduce DSO and recover cash where recovery is still realistic.

Finance teams usually don't need more activity. They need better sequencing.

When your workflow reflects Arizona's legal timelines, your team stops reacting and starts managing. You get cleaner prioritization, stronger controls, and a better link between AR effort and actual recoverability.

Resolut helps professional services firms automate AR with consistency, accuracy, and a human touch. If you want a tighter process for follow-up, escalation, and cash collection, it's built to support the kind of disciplined workflow described above.