Colorado Statute of Limitations Debt: A CFO's 2026 Guide

Understand the Colorado statute of limitations debt for your firm. This 2026 guide covers key timelines, risks, & strategies for CFOs.

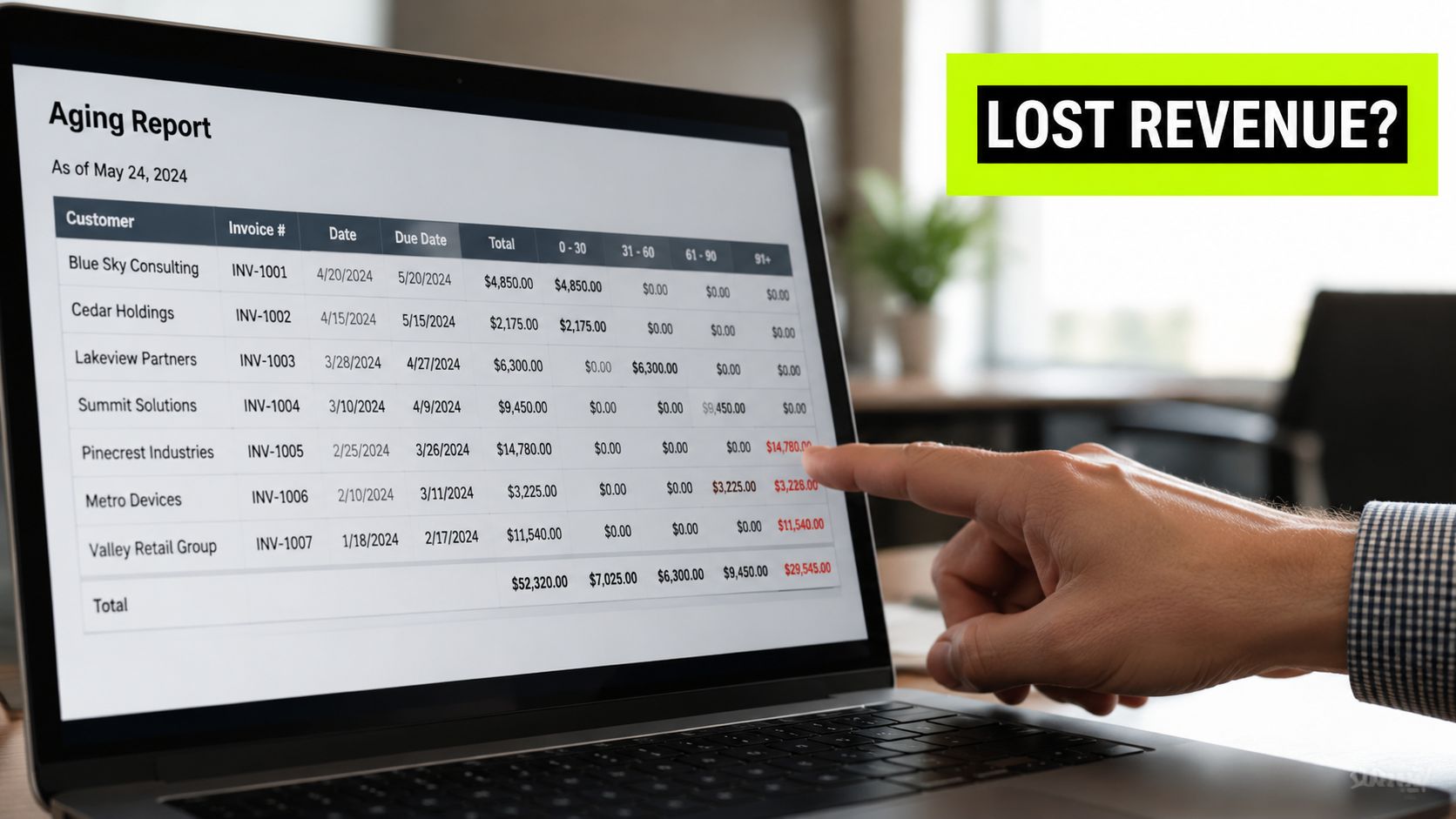

You review the aging report near quarter-end and one line item keeps pulling your eye back. It's a large invoice. It's been sitting far too long. The client hasn't disappeared, but momentum has. Your team has sent reminders, left messages, and logged follow-ups. Nothing has closed the gap.

That's where the Colorado statute of limitations debt issue stops being legal trivia and becomes a finance control problem.

For CFOs, controllers, and firm owners, the key question isn't just whether a receivable is old. It's whether your process still gives you options. If your team misreads the collection window, you can push a legally stale account too far or write off a balance that still had a path to recovery. Either mistake hurts cash flow, distorts the balance sheet, and weakens discipline across the entire AR function.

The Hidden Risk in Your Aging Report

An aging report doesn't just show late invoices. It shows where finance has lost timing, advantage, or both.

At professional services firms, that often happens unnoticed. A partner wants to preserve the client relationship. Billing went out late. A dispute sat in email instead of entering a structured workflow. Then the receivable turns from “slow” to “old,” and finance inherits a problem that should have been managed months earlier.

If your team still treats aging as a reporting exercise, you're already late. A strong aging report process should tell you which balances need immediate intervention, which ones need legal review, and which ones need a controlled exit from the books.

What finance leaders usually miss

The common mistake is assuming an old invoice is “harder to collect.” That framing is too soft. Old receivables create three separate risks:

- Cash risk: The longer an invoice sits, the less confidence you should have in timing and recoverability.

- Control risk: Teams start improvising. Notes are incomplete. Promises aren't documented. The file weakens.

- Legal risk: Once a debt approaches or crosses the enforceable window, the collections approach has to change.

Practical rule: Every materially aged balance should have both a collection status and a legal-timeline status.

That second status matters more than many firms realize. If you can't identify when the debt accrued, what type of obligation it is, and what event may have restarted the clock, then your aging report is incomplete. It may look precise, but it isn't decision-ready.

What good operators do differently

Strong controllers don't wait for year-end cleanup. They build a discipline around account age, documentation quality, and escalation timing.

A workable review cadence usually includes:

- Contract classification: Is the receivable tied to a written agreement, an oral arrangement, a note, or a judgment?

- Last-activity verification: Has there been a payment, acknowledgment, or settlement discussion that changes the timeline?

- Escalation ownership: Does AR own the next action, or does legal need to review before any further push?

The hidden risk in your aging report isn't only bad debt. It's false confidence.

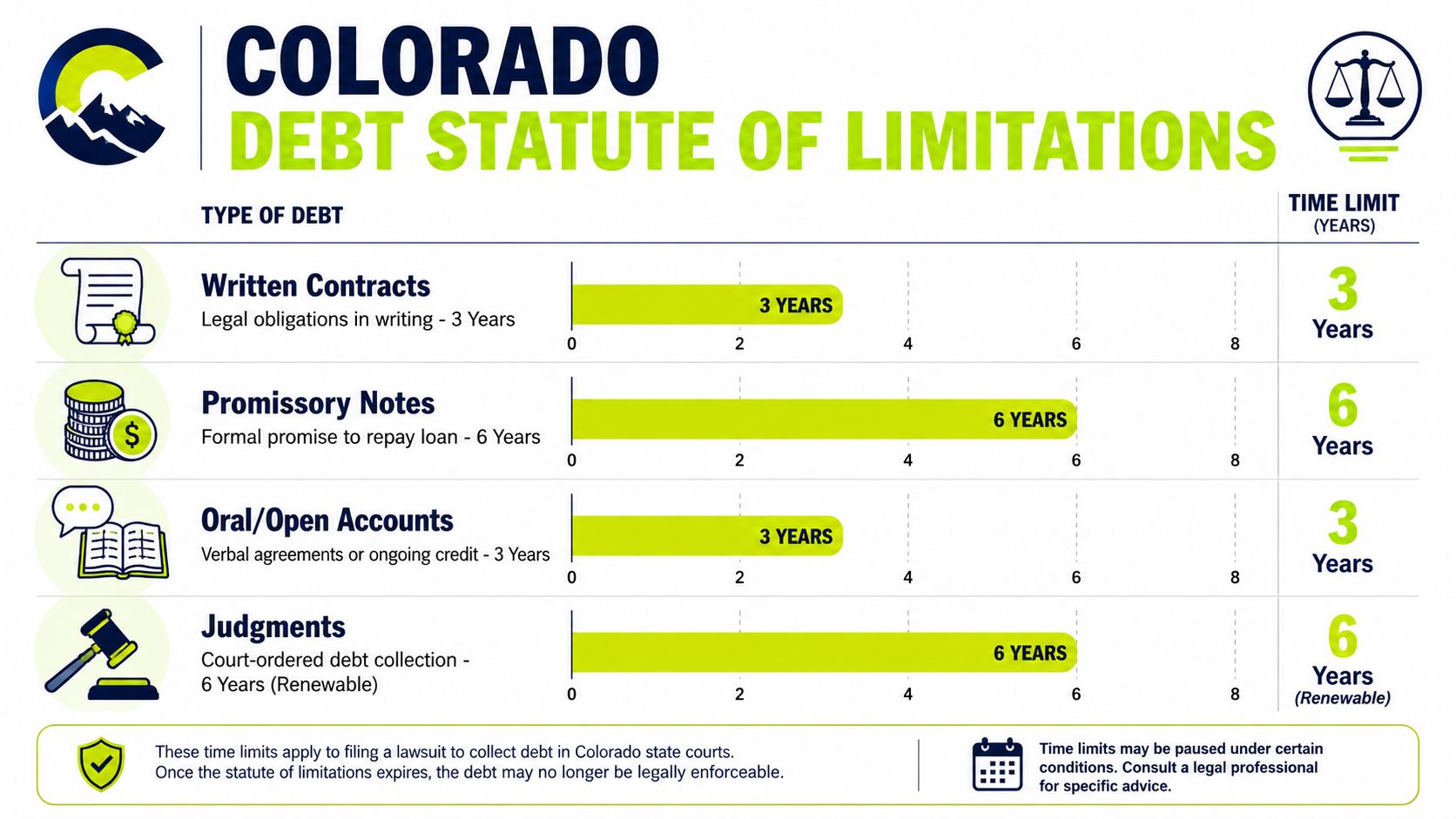

Understanding Colorado's Debt Collection Timelines

A partner asks why a six-figure balance is still sitting in AR after repeated follow-up. The account looks old, but the fundamental question is older than what. In Colorado, collectability depends on the legal category of the obligation, the accrual date, and whether the firm is trying to collect on an invoice, a note, or a judgment.

That distinction affects cash forecasting and escalation discipline. If the file is tagged incorrectly, AR may spend time pushing an account that should already be with counsel, or worse, send legal a claim with a weaker litigation path than the aging report suggests.

The baseline rule finance teams should know

For many actions in Colorado, the starting point is 6 years under Colorado Revised Statutes § 13-80-103.5. The statute says those actions must be brought within six years after the claim accrues.

For finance leaders, that is a filing window, not a reason to wait. A six-year period does not mean an account has six years of equal value. Recovery odds usually weaken much earlier because contacts change, documentation gets thinner, and staff memory disappears.

Where classification changes the answer

Colorado's judicial branch materials on civil statutes of limitation show why contract type matters operationally, not just legally (Colorado Judicial Branch reference chart). Some claims tied to oral agreements can carry a shorter timeline than claims tied to written contracts, and judgments follow a different enforcement framework altogether.

That is why a professional services firm should treat contract classification as an AR control, not a legal clean-up item. The invoice is only the billing artifact. The enforceable right usually comes from the agreement behind it.

Debt category | Operational takeaway |

|---|---|

Written contract | Store the signed engagement letter, amendments, invoices, and collection notes in one file |

Oral agreement | Escalate earlier and document the terms with more care because classification may be harder to prove |

Promissory note | Keep the note, maturity terms, and payment ledger attached to the customer record |

Judgment | Track it separately from trade receivables because enforcement and valuation work differently |

Multi-state firms should also avoid copying one state's rules into another state's process map. The timing logic differs by jurisdiction, which becomes obvious if you compare Virginia debt limitation periods for receivables and contracts with Colorado's framework.

What this means in day-to-day AR

In practice, the first control point is intake. If your firm opens a client matter without capturing whether the work is governed by a signed engagement letter, a modified SOW, or a loosely documented verbal approval, the collections problem starts before the invoice goes out.

A workable review sequence is straightforward:

- Identify what created the obligation. Engagement letter, oral modification, promissory note, or court judgment.

- Confirm when the claim accrued. Nonpayment, default, acceleration, or another trigger that counsel can validate.

- Match the supporting records to that theory. Billing history alone rarely carries the whole file.

- Assign the right path. Standard AR follow-up, management escalation, outside counsel review, or reserve analysis.

Later in the review, it helps to hear the categories explained visually.

The Colorado statute of limitations debt question for a controller is not just account age. It is whether the team can prove the type of obligation, the accrual date, and the records that support enforcement.

Where finance and legal should meet

Controllers do not need to brief the law from memory. They do need a file structure legal can trust. That means your ERP, AR platform, or QuickBooks automation layer should capture contract type, accrual trigger, and document location at the account level.

If those fields are missing, every later decision gets more expensive. The team wastes collector time, reserves become less reliable, and legal review starts with reconstruction instead of action.

When the Clock Stops Pauses or Resets

A controller pulls a 210-day invoice into the write-off review queue. The collector then mentions the client sent a partial payment two months ago and confirmed the balance by email during a payment plan discussion. That account may need a different legal and financial treatment than the aging report suggests.

That is the control problem in this section. The limitation period is not always measured from the original invoice date alone. Later events can matter, and if your team does not capture them in a reliable chronology, collections strategy, reserve analysis, and escalation decisions start from the wrong date.

Why an old invoice can become a current enforcement question

In practice, the risk is usually not ignorance of the rule. It is bad record flow.

A receivable can sit unchanged in the general ledger while the enforceability analysis changes underneath it. A partial payment, a written acknowledgment of the balance, or account-level correspondence about repayment can affect how counsel evaluates the file. If those events live in one employee's inbox or in free-form notes, finance reviews the account using stale assumptions.

The result is expensive in both directions. Teams write off accounts too early, or they spend staff time and legal budget on accounts they have not documented well enough to pursue with confidence.

Consider two files with the same invoice date:

- File A: No later payment, no written acknowledgment, and weak follow-up notes.

- File B: A later partial payment appears in the cash log, and the client later confirms the outstanding balance in writing.

Those files should not move through the same workflow. One may be nearing the end of its practical recovery window. The other may require a fresh legal review because later activity changed the timeline analysis.

What to capture every time the account changes

Collections notes are not enough. Your team needs an account history that counsel and auditors can follow without reconstruction.

Use a standard documentation checklist:

- Payment event: Record the exact date received, amount, payment method, and how cash was applied.

- Acknowledgment event: Save the email, letter, portal message, or signed communication in the account record.

- Promise-to-pay terms: Preserve any repayment language and the date it was sent or accepted.

- Reviewer assignment: Identify who assessed whether the event changed the limitation analysis.

- Workflow status: Update the ERP or AR system so the next collector, manager, or outside firm works from the same timeline.

A note in Outlook is not a control. A dated, searchable, account-level chronology is.

How finance should operationalize the reset question

Set a rule that any partial payment or written balance acknowledgment triggers exception handling. Do not leave that judgment to individual collectors. Route the account into a review queue, lock the key documents to the customer record, and require a manager or designated legal liaison to confirm the next action.

For multi-state firms, this matters even more. State rules are not uniform, and a single aging-based script creates avoidable compliance risk. Teams with clients across jurisdictions need state-specific workflow logic, reason codes, and document retention standards. A state comparison such as this guide to Virginia debt limitation timing shows why one national rule set usually fails in practice.

If payment activity or written acknowledgment can affect the clock, last invoice date cannot be your only decision field.

That one process change improves write-off timing, reduces wasted collection effort, and gives legal a file they can evaluate without rebuilding the account history from scratch.

The Financial Consequences of Pursuing Stale Debt

Finance teams usually feel the damage from stale debt before they label it correctly.

The first symptom is reporting distortion. Receivables stay on the books too long, DSO looks worse than it should, and reserves become a negotiation instead of an evidence-based estimate. The second symptom is wasted effort. AR staff spend time chasing balances that no longer support the same legal remedies.

The core distinction that changes strategy

A debt can be time-barred for suit and still generate collection activity. That's the source of much of the confusion.

A Colorado-focused summary highlights this mismatch clearly. While Colorado's general statute of limitations for many liquidated debts is six years, district court judgments can be enforced for up to 20 years in some cases, which means old debt and old judgments shouldn't be managed with the same assumptions (Colorado time-barred debt and judgment nuance).

For finance leaders, the takeaway is simple. “Old” is not a category. It's a prompt for analysis.

What gets more expensive when controls are weak

The direct cost isn't only the missed recovery. It's the process drag around it.

When teams pursue stale debt without a clear rule set, several things happen:

- AR effort gets misallocated: Collectors spend time on accounts with low legal enforceability while fresher balances wait.

- Forecasting degrades: Cash expectations remain inflated because account status is based on hope rather than enforceability.

- Write-offs get delayed: The balance sheet carries noise, and management discussion gets less reliable.

- Client communication worsens: Staff improvise language and create avoidable exposure.

Collections should become more disciplined as an account ages, not more emotional.

That's especially true in professional services, where the unpaid balance often sits next to an active relationship. Partners may still be selling work to the same client while finance is trying to close an old obligation. Without a formal policy, the firm sends mixed signals.

Why judgment debt needs separate handling

A judgment is not just an older receivable. It's a different stage of the asset.

That means your accounting treatment, review cadence, and recovery assumptions should change once an account moves from pre-judgment collections to post-judgment enforcement. Teams that lump those accounts together usually under-manage one side of the portfolio. They either give up too early on collectible judgments or overwork pre-judgment balances that have already lost practical value.

A short decision table helps:

Account status | Best finance posture |

|---|---|

Pre-limitations, documented | Active collection, structured escalation |

Near limitations deadline | Legal review, evidence check, decision point |

Time-barred for suit | Controlled voluntary-payment workflow only |

Judgment entered | Separate enforcement calendar and record set |

What works and what doesn't

What works is clean segmentation, disciplined reserves, and early legal review on borderline files.

What doesn't work is treating every overdue balance as a customer-service problem that can be solved by sending one more reminder. Once a receivable reaches late-stage aging, it becomes a finance and risk-management problem first.

If your team wants to reduce DSO and improve cash flow, stale debt can't stay buried inside a generic over-90 bucket. It needs its own operating logic.

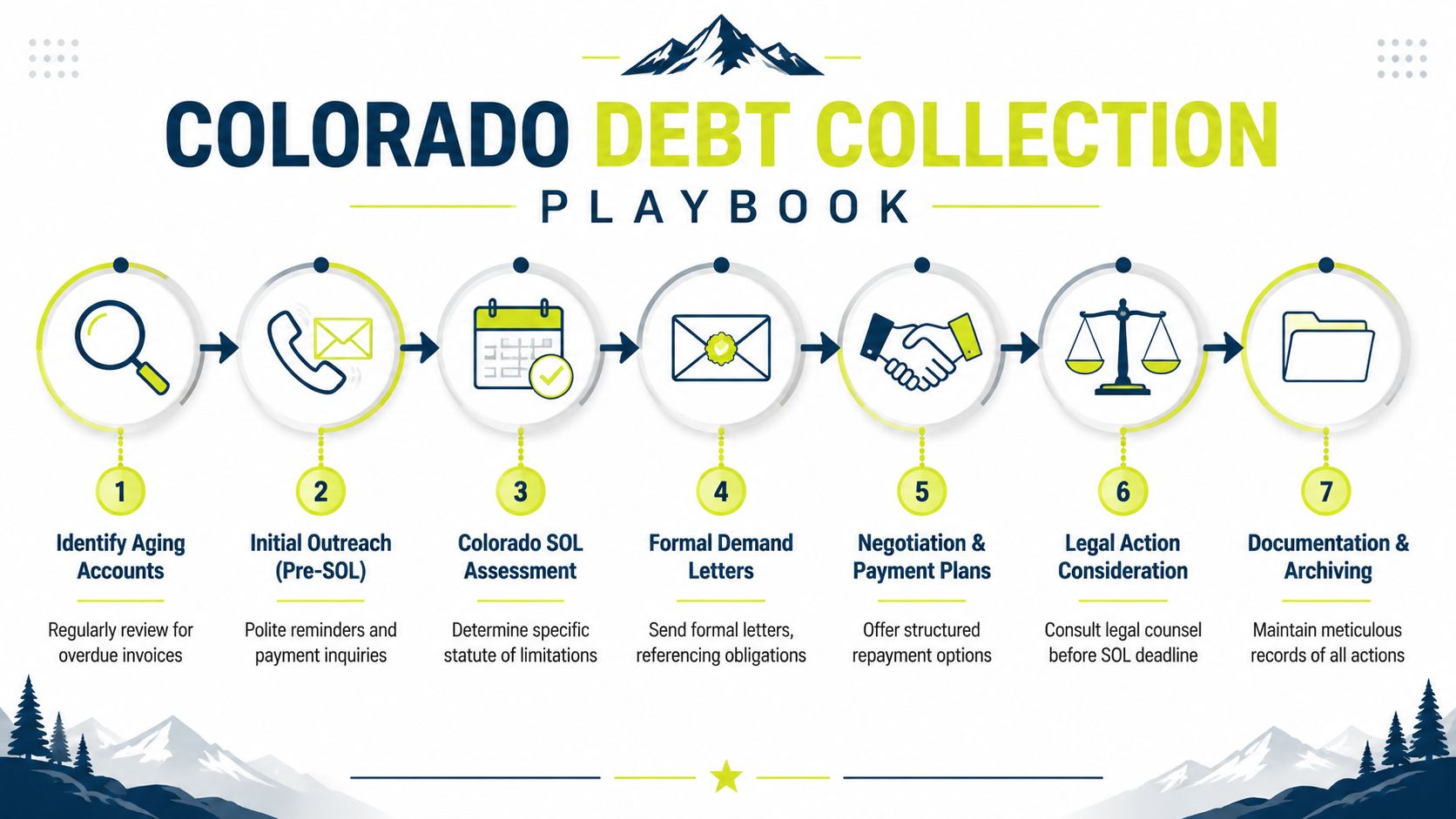

An Operational Playbook for Your Collections Team

A collections team performs best when it doesn't have to guess.

The strongest playbooks turn aging from a passive report into a sequence of controlled decisions. That matters in Colorado because the legal path depends on debt type, documentation, and timing. It also matters in professional services because relationship owners often pull AR in opposite directions unless finance sets the rules.

A workable control structure

Your team needs one owner for process, one owner for legal review, and one owner for client relationship decisions. In smaller firms, those roles may overlap. The responsibilities shouldn't.

Here's a practical operating model:

- Triage the aging report weekly Separate current disputes, payment-plan accounts, silent accounts, and legally sensitive accounts.

- Classify the debt before escalation Don't let staff send final demand language until the file shows whether the obligation is written, oral, note-based, or already reduced to judgment.

- Lock down the account file Contract, invoices, correspondence, payment history, dispute notes, and promises to pay should sit in one location.

- Use trigger-based action Escalation should happen because the file reached a condition, not because someone had free time that day.

The decision points that matter most

A useful playbook doesn't need legal language in every step. It needs clear thresholds for action.

Use decision criteria like these:

- If documentation is incomplete: Pause aggressive outreach and rebuild the file first.

- If there's recent payment activity: Review whether that activity affects the limitations analysis.

- If the account is approaching the legal edge: Route to counsel or designated internal reviewer before any litigation language appears.

- If the debt is time-barred for suit: Shift the script and approval process. Don't let collectors improvise.

Many firms also benefit when they automate collection workflows instead of relying on manual reminders and spreadsheet-based follow-up. The main benefit isn't speed alone. It's consistency. The same triggers fire every time, and exceptions become visible sooner.

Communication rules that protect the firm

Your staff should know which messages are courtesy reminders, which are formal demands, and which require review before sending.

That sounds basic, but it's where avoidable risk enters. Teams copy old templates, relationship managers send side emails, and no one can confirm which version of the story the client received.

Build message governance around three rules:

- One approved template set: No personal collection language from individual staff.

- One source of truth for account status: ERP, AR platform, or documented workflow system.

- One handoff path to legal or recovery specialists: No side escalation through private email threads.

If your current process is loose, formalizing it around a documented business debt recovery workflow is usually the fastest way to create consistency.

A strong collections playbook doesn't make your team harsher. It makes the firm more accurate.

Visual ideas for finance leaders

If you're socializing this internally, three visuals usually help:

- A heat-map aging dashboard showing invoice age against documentation quality.

- A decision tree for pre-limitations, near-limitations, time-barred, and judgment accounts.

- A partner-level scorecard that shows old AR by billing attorney, practice lead, or client owner.

Those visuals turn compliance into operating behavior.

Building a Resilient and Automated AR Process

A partner asks why a two-year-old balance is still open. AR says the client promised to pay. The collector who handled the file left six months ago, and the notes are split across email, the billing system, and a spreadsheet no one trusts. That is how firms end up debating legal timelines when the underlying failure happened much earlier in the process.

A controlled AR function keeps accounts from drifting into that zone. As noted earlier, Colorado limitation periods matter. But from an operating standpoint, the better goal is simple: identify risk early, document every step, and force escalation while the account is still collectible.

What modern AR should do by default

Manual AR fails in consistent ways. Payment promises stay informal. Disputes sit with the relationship owner. Follow-up timing depends on memory, workload, or who is willing to send another email. By the time finance reviews the account, the file is incomplete and the options are narrower.

Automation fixes that by turning collections into a managed workflow instead of a series of individual efforts. A sound setup should:

- Trigger reminders on schedule: Outreach goes out based on invoice age and account status, not staff memory.

- Flag collection risk early: Silence, repeated partial payments, recurring disputes, and broken promises should all push the account into review.

- Keep records in one place: Contracts, invoices, payment history, and collection notes need to stay tied to the account.

- Route exceptions fast: Disputed accounts, high-balance matters, and near-threshold aging should move to the right reviewer without delay.

Those controls reduce write-off risk. They also reduce the cost of collection, because staff spend less time reconstructing history and more time acting on current information.

Why this matters for professional services firms

Professional services firms have a predictable tension. Client relationships sit with partners or practice leaders, while cash discipline sits with finance. If ownership is unclear, both sides wait. The partner does not want to strain the client. AR does not want to escalate an account tied to a sensitive relationship. Aging keeps climbing.

The fix is not more pressure. It is better structure.

AI AR automation can standardize reminder timing, document account activity, and surface accounts that need human review before they become recovery problems. For firms already operating in QuickBooks, QuickBooks AR automation can also keep billing data and collection activity aligned, which matters because stale debt often starts as a recordkeeping gap rather than a legal dispute.

Controls that prevent stale debt

Teams usually focus on collection effort. Controllers should focus on collection controls.

Build the process so every invoice has a named owner, every contact attempt is logged, every payment promise gets a date, and every exception has a deadline for review. Near-limit aging should never sit in a general queue. It should trigger a specific decision: pursue, settle, send for legal review, or stop further collection activity based on policy.

That discipline changes the economics of receivables. Firms with clean documentation and timely escalation preserve more options. Firms with loose notes and delayed follow-up spend more time chasing balances that should have been resolved, reserved, or written off months earlier.

Resolut helps professional services firms automate AR with consistent workflows, accurate follow-up, and human oversight where it matters. If you're trying to reduce DSO, improve cash flow, and bring more control to collections without turning your finance team into a call center, Resolut is built for that.