Choosing a Nationwide Debt Collection Company: CFO Guide

CFO guide to choosing a nationwide debt collection company: covers legal risks, pricing, performance, & AR automation for cash flow.

Your aged receivables report usually tells the story before your bank balance does.

A professional services firm can tolerate a few slow-paying clients. It gets dangerous when one or two larger accounts move from “late” to “unlikely,” especially if the debtor sits in another state and your internal team has exhausted their options. At that point, the question isn't just collections. It's capital allocation.

Do you hand the account to a nationwide debt collection company and accept the economics of late-stage recovery? Or do you invest in accounts receivable automation, tighten first-party follow-up, and prevent more accounts from reaching that point in the first place?

For CFOs and controllers, this isn't a moral question and it isn't a branding exercise. It's a control question. You're deciding where to place effort, what kind of risk you'll carry, and how much of your cash conversion process you want to own.

When to Consider a Nationwide Debt Collection Company

The usual trigger is familiar. Your team has invoiced cleanly, followed up more than once, and escalated through the account lead. The client stops responding, disputes become vague, and the balance is now old enough that every week of delay makes recovery less likely.

If that client is local, you can sometimes lean on an existing relationship, outside counsel, or a regional collector. If the client is in another state, the problem changes. Collection becomes less about persistence and more about legal reach, licensing, and the ability to act without creating a compliance issue of your own.

The market itself reflects that pressure. IBISWorld projects the U.S. debt collection agency industry will reach $13.6 billion in 2026, while the number of firms declined at a 3.5% compound annual rate between 2020 and 2025 according to IBISWorld's debt collection agency industry profile. That combination tells you two things. The market is still large, and firms are competing inside a more consolidated environment.

Good reasons to escalate

A nationwide collector starts to make sense when the account has moved beyond normal AR discipline and into specialized recovery.

- The debtor is out of state. Your team may be able to call and email anywhere, but effective recovery across state lines requires more than outreach.

- The balance is material to working capital. If the account can distort cash planning, payroll timing, partner draws, or tax reserves, waiting for “one more internal touch” often costs more than it saves.

- Internal collection has stalled. If your PM, partner, and finance team have all contacted the client and nothing changes, the account likely needs a different workflow.

- You need a defined escalation path. Some firms jump from reminder emails straight to legal threats. That usually creates more noise than results. A collector can sit between internal dunning and litigation.

Practical rule: Use a nationwide debt collection company for severe delinquencies that your internal team can no longer move with normal commercial pressure.

There's also a strategic distinction between outsourcing collections and selling the receivable. If you're weighing both, it helps to understand the economics and control trade-offs in this breakdown of selling debt to collection agencies.

What doesn't justify a national collector is simple frustration. If your issue is inconsistent invoicing, weak follow-up cadence, poor payment options, or no ownership inside AR, sending accounts out won't fix the process that created the delinquency.

National vs Local Collectors A Strategic Analysis

A national collector and a local collector can both recover money. They do it under different operating models, and those differences matter more for a professional services firm than most agencies admit.

Where national collectors win

The core advantage is infrastructure. A true nationwide debt collection company maintains licensing and bonding to operate in all 50 states, and that capability depends on a distributed compliance system rather than a single call center, as described by Kaplan's overview of nationwide collection agencies.

That matters when your clients are spread across multiple jurisdictions. A national firm can route accounts based on debtor location, claim type, and the state rules that govern enforcement. For a CFO, that reduces one specific risk. You don't want to hand off an account only to learn the collector isn't positioned to work it properly where the debtor sits.

National firms also tend to fit better when your client base looks like this:

Situation | Better fit |

|---|---|

Clients concentrated in one metro or state | Local collector |

Clients distributed across many states | National collector |

Need for state-by-state escalation options | National collector |

Relationship-heavy account with local context | Local collector |

A national collector can also be easier to govern if you want one vendor, one reporting structure, and one set of review meetings instead of several local relationships.

Where local collectors still matter

Local firms can have an edge when the debt is tied to regional relationships, local business norms, or a narrow industry community. In professional services, that matters more than many finance teams expect.

A local collector may understand the debtor's reputation, payment habits, and market context in a way a large national shop won't. That can be useful when the goal is recovery without burning a referral source or an adjacent relationship.

The best collector for a commercial account isn't always the biggest one. It's the one whose operating model matches the geography and sensitivity of the claim.

There's also a practical trade-off around client experience. Large agencies often run more standardized workflows. That can improve consistency, but it can also feel blunt if the account is disputed, nuanced, or tied to unfinished scope.

The decision criteria that matter most

If you're choosing between national and local, evaluate against these questions:

- Jurisdictional fit: Can the agency legally and operationally work the account where the debtor is located?

- Commercial fit: Do they understand professional services disputes, milestones, retainers, and change-order style billing issues?

- Escalation style: Will they preserve room for negotiated resolution, or do they move too quickly into a hard-edged collections posture?

- Reporting discipline: Can your team see placements, status changes, disputes, promises to pay, and remittance timing clearly?

- Portfolio logic: Are you placing a handful of large balances, or a broad pool of smaller delinquent invoices?

If you're comparing external help broadly, not just geography, this guide on choosing an AR collection agency is worth reviewing before you issue an RFP.

For most firms, the answer is straightforward. Use a local collector when local knowledge is the asset. Use a nationwide debt collection company when interstate compliance and enforcement readiness are the asset.

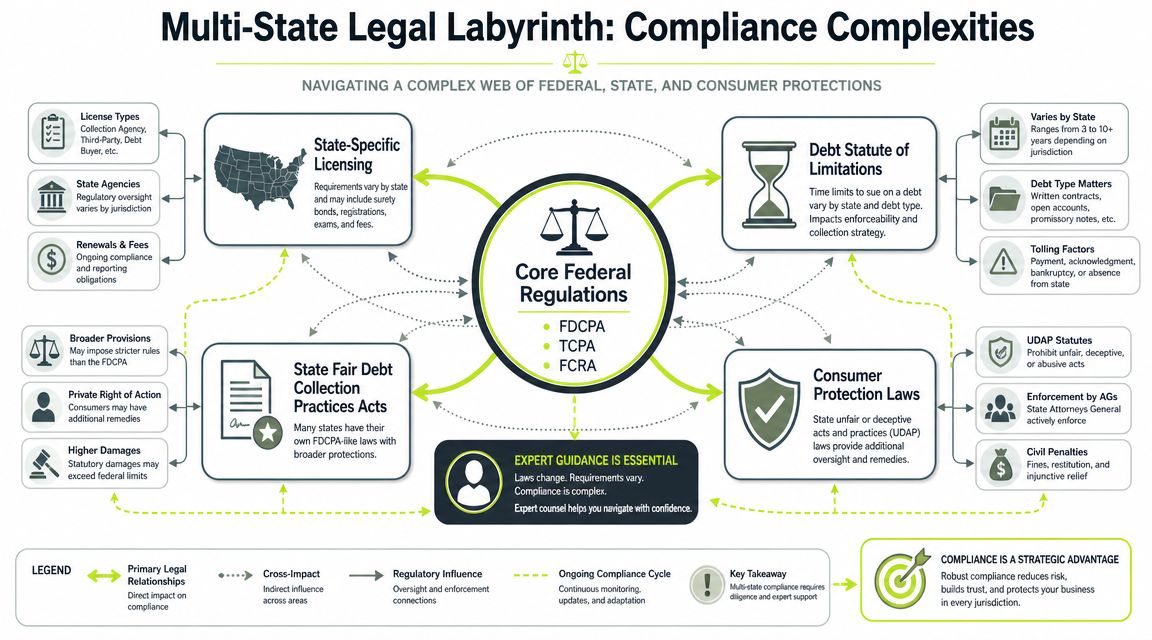

Navigating the Multi-State Legal Labyrinth

The legal risk in collections usually isn't the obvious one. It's not just whether the collector gets paid. It's whether they operate correctly in the states where your debtors sit.

Why multi-state compliance changes the economics

Finance leaders often evaluate agencies on fee percentages first. That's understandable, but incomplete. With a nationwide debt collection company, compliance architecture is part of the product.

State rules can differ on licensing, bonding, revenue treatment, and reporting obligations. A collector that works cleanly in one state may need a materially different workflow in another. If they don't have that infrastructure, your recovery process can slow down, become more expensive, or create exposure you didn't price into the decision.

California is a good example. The state requires debt collection activity to be reported through the Nationwide Multistate Licensing System, and it applies a net-proceeds methodology that differs depending on whether the entity is a debt buyer, debt owner, or third-party collector, according to the California DFPI debt collection licensee guidance. For third-party collectors, the treatment of net proceeds can materially change the economics compared with contingency arrangements used elsewhere.

That tells you something important. “National coverage” is not a marketing label. It's an accounting, licensing, and workflow problem that has to be solved state by state.

Questions to ask before placement

When I review a collector for a client, I want specific operational answers, not generic assurances.

Ask questions like these:

- License management: Which states are you licensed in for the accounts we may place?

- Bonding status: How do you track renewals, lapses, and jurisdiction changes?

- Workflow controls: How do you prevent an account from being worked in a state where your permissions differ?

- Revenue treatment: How do you handle state-specific rules that affect fee reporting or net proceeds?

- Legal handoff: If the file moves toward legal escalation, who reviews state-specific requirements first?

A collector's compliance weakness usually shows up in process answers. If they speak only in generalities, assume the back office is thinner than the sales deck.

What CFOs should protect

Your firm doesn't need to become a specialist in every state. It does need to avoid blind delegation.

A simple way to protect yourself is to require the agency to document three things in writing:

- Jurisdictions covered for your portfolio

- The workflow for disputed accounts and escalations

- The reporting you'll receive on account status and remittances

If you're moving toward a more formal escalation step before placement, a structured legal demand letter for payment can help determine whether the debtor is merely slow or unwilling to resolve the balance.

The firms that manage this well treat compliance as an operating control, not a legal footnote. That's the standard you want.

Deconstructing Performance Metrics and Pricing Models

Most collection proposals lead with a recovery rate. That number is rarely enough to make a finance decision.

A collection agency can post an attractive gross recovery rate and still produce a mediocre financial outcome for your firm if the accounts take too long to resolve, if fees apply to settlements you would have achieved internally, or if the agency performs well only on fresher placements.

The collections environment has also changed. The Consumer Financial Protection Bureau reported that collections tradelines on consumer credit reports fell 33% from about 261 million in Q1 2018 to about 175 million in Q1 2022 in its market snapshot on third-party debt collections tradelines reporting. Even if your firm is focused on commercial receivables, the broader lesson is useful. Agencies have to operate with more precision, not just more volume.

What to measure instead of headline recovery

Start with net economics.

Net recovery

This is the amount your firm keeps after fees, legal costs if applicable, and any other deductions. Gross recovery can make a weak arrangement look strong.

Time to cash

Cash received late still has value, but less value than cash recovered quickly. For a CFO managing payroll, tax deposits, and partner distributions, timing matters almost as much as amount.

Recovery by invoice age

An agency should be able to explain how it performs on newer placements versus very aged accounts. If it can't segment performance by age bucket, assume the reporting isn't strong enough for forecasting.

Recovery by claim type

Professional services debt isn't all the same. A clean unpaid invoice behaves differently from a scope dispute, a holdback, or a matter where the client claims deliverables were incomplete.

How pricing models affect control

The common structures are contingency, flat fee, and hybrid arrangements.

- Contingency fee: Simple to understand and often aligned with recovery, but it can become expensive if the agency collects money your internal team still had a realistic chance to recover.

- Flat fee: Better when you want predictable cost on early-stage accounts, but it can encourage lower-touch handling if the vendor's economics are too thin.

- Hybrid model: Sometimes useful when you place mixed account types, though it requires tighter contract language.

Review the service agreement carefully for these points:

- Fee trigger language: Does the agency earn a fee on all payments after placement, even if your relationship team resolves the account?

- Recall rights: Can you pull back an account cleanly if the client re-engages?

- Settlement authority: Who approves discounted resolution?

- Dispute handling: What happens if the debtor contests the invoice after placement?

Key takeaway: The right metric is not “How much do they collect?” It's “How much do we keep, how fast do we get it, and how much control do we lose in the process?”

The Definitive Vendor Evaluation Checklist

A collection agency review should look more like vendor diligence and less like emergency outsourcing. If the balance is material enough to place, it's material enough to vet properly.

Six checks that matter

1. Compliance and licensing

Verify that the agency is authorized for the states where your debtors are located. Don't accept “nationwide” as sufficient proof by itself. Ask for current licensing and bonding support where relevant to your portfolio.

2. Technology and security

You are sending client data, invoice history, and contact records outside your organization. Review how files are transmitted, who has access, how disputes are logged, and how reporting is shared back to your team.

3. Recovery visibility

You need more than monthly remittance totals. Require reporting that shows placements, status changes, debtor responses, disputes, payment arrangements, and closed-account reasons.

Questions worth asking in the meeting

Use the diligence call to test how the agency operates.

- “Show me a sample client report.” If reporting is opaque during the sales process, it won't improve after contract.

- “How do you handle professional services disputes?” Listen for familiarity with engagement letters, approvals, scope changes, and milestone billing.

- “Who owns escalations?” You want a named point of contact, not a shared queue.

- “What happens when our client pays us directly?” This reveals whether the fee policy is fair and whether reconciliation will be painful.

The collector you hire becomes part of your receivables process. Treat the review the same way you'd treat a banking, payroll, or ERP decision.

A practical checklist for final approval

Before legal review, I'd want these items completed:

- Reference calls done: Speak with firms that resemble yours in client profile and invoice structure.

- Contract exceptions marked: Fee triggers, settlement rights, recall terms, and dispute procedures should be redlined before signature.

- Escalation map documented: Your internal owner, the vendor contact, and the legal backup path should be clear.

- Pilot scope defined: Start with a controlled batch of accounts rather than the entire backlog.

- Success criteria agreed: Decide in advance what “working” means for your firm. Usually that includes net cash, speed, transparency, and minimal relationship damage.

A rushed placement often creates a second problem after the first one. Careful diligence prevents that.

The Modern Alternative AR Automation

Most firms wait too long to modernize receivables. They tolerate slow collections as an operating annoyance, then react with outside agencies when the backlog becomes painful.

That sequence is expensive because it attacks bad debt late.

Why first-party process usually has the better economics

For a professional services firm, many overdue invoices don't start as hard collections problems. They start as workflow failures.

The invoice goes out late. The billing contact is wrong. A partner assumes finance is following up. Finance assumes the account lead is handling it. The client wants a revised invoice or a portal link. Nobody owns the sequence tightly enough, so the balance ages into a collections issue that might have been avoided.

That's where accounts receivable automation changes the equation. Instead of outsourcing pain after delinquency, you build a first-party system that applies pressure early, consistently, and professionally.

A good AR software for professional services platform handles the basic discipline your team often struggles to maintain manually:

- Invoice delivery with proof

- Scheduled reminders tied to due dates

- Segmented follow-up by client type or risk

- Escalation paths for ignored invoices

- Clear payment options and reconciliation support

What modern automation looks like in practice

This isn't just reminder emails. The better systems behave like an in-house collections operation before the account ever needs third-party placement.

For firms using QuickBooks AR automation, the benefit is usually operational before it's analytical. Billing data, open balances, payment status, and follow-up activity stay closer to the accounting record. That reduces handoffs and lowers the odds that a delinquent account is missed because someone exported an aging report too late.

For teams evaluating AI AR automation, value lies in prioritization. Not every late invoice needs the same message, cadence, or escalation path. Some clients respond to a simple payment link. Others need a nudge from the account owner. A few need formal escalation quickly because silence is their pattern.

This video offers a useful look at how modern receivables workflows are evolving in practice.

Control is the real return

The biggest gain from automation is not cosmetic efficiency. It's control over cash flow.

When reminders fire on time, when payment options are easy, when disputes are surfaced early, and when account managers can see what finance has already sent, you reduce DSO and improve cash flow through discipline instead of heroics.

That also protects client relationships better than late-stage collections. A structured first-party process feels like competent finance operations. A third-party handoff feels like failure, even when it's justified.

I'd frame the choice this way:

If your main problem is... | The better first move is... |

|---|---|

A few severe, stale, out-of-state delinquencies | Nationwide debt collection company |

Broad inconsistency in reminders, follow-up, and payment handling | Accounts receivable automation |

Weak visibility into who owes what and what was sent | AR automation |

Lack of internal leverage after repeated non-response | External collections |

If you're building a broader operational approach to customer communication, this guide to transforming customer service is useful because it shows how automated, human-aware workflows can improve consistency without making interactions feel robotic.

For most firms between $3 million and $50 million, the smarter long-term move is to reserve agencies for edge cases and improve first-party execution everywhere else.

Your Next Move Control Your Cash Flow

A nationwide debt collection company is a valid tool. It can be the right move when a balance is material, the debtor is out of state, and your internal team has exhausted normal recovery paths.

It's still a late-stage intervention. You're paying to recover cash after the process has already broken down.

Most professional services firms have a bigger opportunity upstream. If you tighten invoice timing, standardize follow-up, improve payment accessibility, and use accounts receivable automation to manage cadence and escalation, you prevent more accounts from reaching collections at all. That gives you better economics, stronger client preservation, and more predictable working capital.

The finance question isn't “collections or software?” It's sequence.

Use external collectors for the accounts that require interstate recovery infrastructure. Use AI AR automation, QuickBooks AR automation, and disciplined first-party workflows to reduce DSO, improve cash flow, and keep control inside your firm.

That's how you stop treating receivables as a recurring cleanup project and start managing them as an operating system.

Resolut helps professional services firms automate AR with the kind of consistency finance teams usually have to build manually. If you want a more controlled way to reduce DSO, improve cash flow, and handle follow-up without sacrificing client experience, Resolut is built for that. Consistent, accurate, and human.