What Is Invoice Reconciliation: A CFO's Guide to 2026 Cash

Discover what is invoice reconciliation & its critical role for CFOs in 2026. Explore manual vs. automated processes to boost cash flow & reduce DSO.

A client payment lands in your bank account before 9 a.m. The reference line is vague. The amount doesn't match any single open invoice. Your AR lead opens QuickBooks, your controller checks the remittance inbox, and someone emails the account partner to ask whether the client mentioned a deduction.

By noon, three people have touched one payment, and you still don't know whether cash is applied correctly, whether a dispute exists, or whether collections should keep following up. That isn't a small process flaw. It's a control gap.

In a professional services firm, invoice reconciliation sits right in the middle of cash flow, client communication, and reporting accuracy. If you want to reduce DSO, improve cash flow, or make accounts receivable automation perform as expected, this is one of the first operational disciplines to tighten.

The Reconciliation Problem You Already Have

Most firms don't notice reconciliation as a problem until it creates noise.

A payment comes in without usable remittance. A client bundles several invoices into one wire. Another client short-pays because they believe part of the work is still under review. Your team can't apply the cash cleanly, so the ledger shows invoices as overdue even though money is in the bank.

That's when finance starts running a manual investigation process disguised as routine AR work.

What the fire drill looks like

In practice, the pattern is familiar:

- Bank first, context later: Treasury or accounting sees the deposit before AR knows what it covers.

- Multiple systems, no single answer: The team checks the bank feed, inbox, PSA, billing records, and accounting ledger.

- Client communication gets messy: Collections may follow up on invoices that were already partially paid.

- Month-end gets distorted: Open AR, unapplied cash, and short-pay balances all blur together.

This is why a lot of firms think they have a collections problem when they instead have a reconciliation problem.

Weak reconciliation doesn't just slow the close. It changes what your team believes is collectible, overdue, or resolved.

In a services business, that matters because your invoices often reflect milestones, retainers, change requests, pass-through costs, and negotiated adjustments. The payment rarely arrives in the neat one-invoice, one-payment format that basic accounting workflows assume.

Why this becomes a control issue

A weak process creates three risks at once.

First, cash visibility gets worse. You may have money received but not properly applied, which makes AR aging less trustworthy.

Second, team time gets consumed by exception handling. Skilled finance people spend their day tracing email threads instead of reviewing trends, billing quality, or client behavior.

Third, client trust takes avoidable hits. Nobody wants a payment reminder on an invoice they already paid.

If you need a more grounded look at how these mismatches show up in day-to-day accounting, this walkthrough on reconciliation in accounting examples is a useful companion.

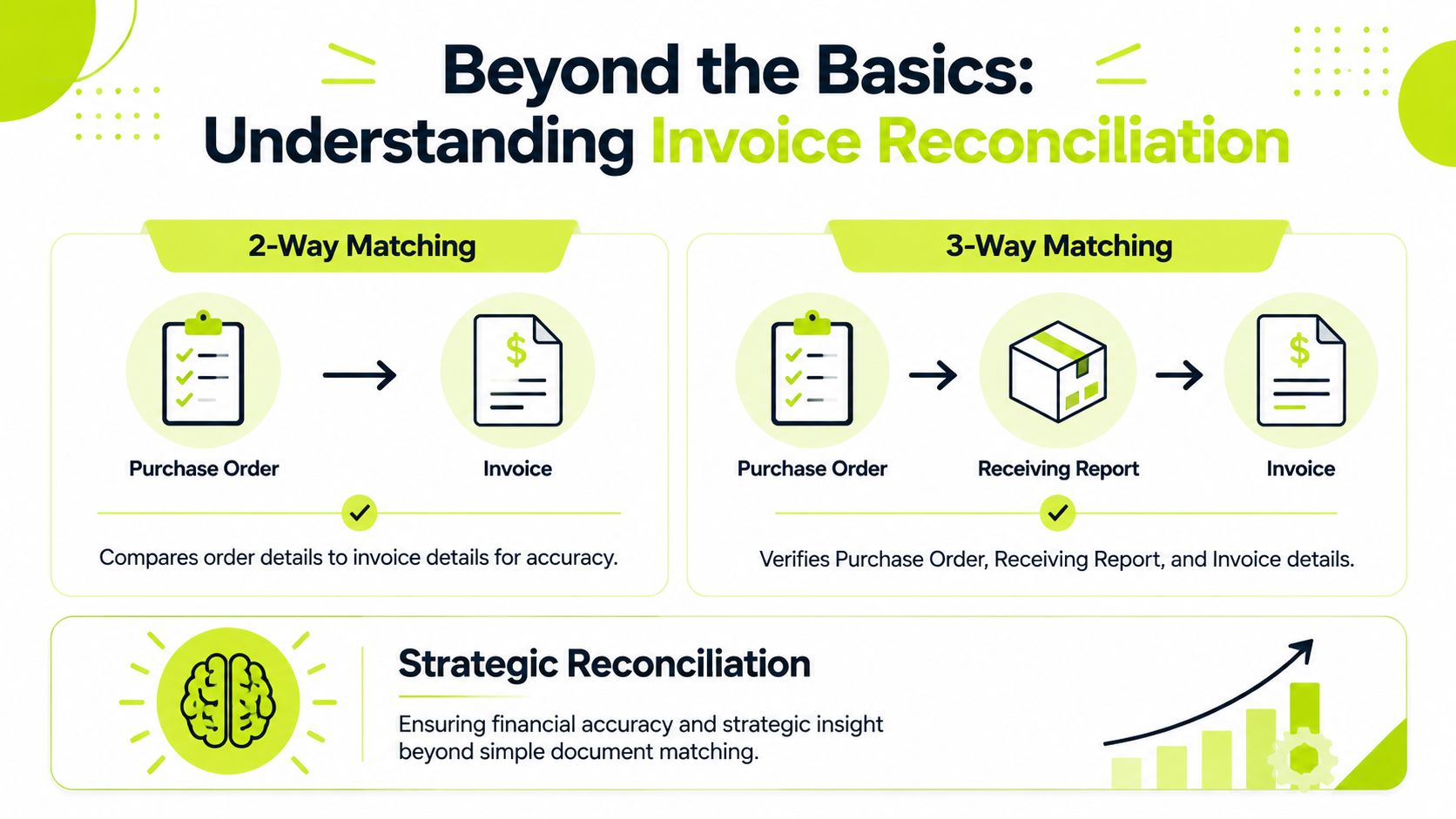

Reconciliation Is More Than Matching Purchase Orders

When finance teams ask, what is invoice reconciliation, most definitions start in accounts payable. That's accurate, but incomplete for a professional services firm.

The classic definition is straightforward. Invoice reconciliation is the control process that compares an invoice with supporting records such as purchase orders, receiving documents, contracts, and payment records. Teams commonly use 2-way matching and 3-way matching to catch mismatches, duplicate charges, unauthorized billing, and fraud while preserving an audit trail, as described by Precoro's explanation of invoice reconciliation.

The AP definition is correct, but it's only half the story

In AP, reconciliation asks a simple control question. Does the invoice match what the company ordered and received?

That usually means:

Matching type | What gets compared | Main purpose |

|---|---|---|

2-way match | Invoice against purchase order | Confirm billed terms align with approved order |

3-way match | Invoice, purchase order, and receipt | Confirm the company was billed for what was actually received |

For a product business, that logic is central. For a professional services firm, it often isn't the daily bottleneck.

In AR, the job is cash application under uncertainty

On the receivables side, reconciliation means something more operational. You're trying to match incoming client payments to the right invoices, amounts, and timing, then decide what to do with anything that doesn't fit cleanly.

That's harder than it sounds.

A law firm may receive a retainer top-up that should sit unapplied until future work is billed. An agency may get one ACH payment covering several invoices across brands or business units. A consulting client may deduct an amount tied to a disputed line item and send no explanation at all.

AP reconciliation validates spend before money goes out. AR reconciliation validates cash after money comes in. Same word. Different pressure.

Think of AP reconciliation as procurement control. Think of AR reconciliation as cash intelligence.

That distinction matters if you're evaluating AR software for professional services, QuickBooks AR automation, or broader AI AR automation. A system that's strong at PO matching doesn't automatically solve payment matching, deductions, or split remittances.

Why professional services firms feel this more acutely

Service firms don't usually have clean receiving documents the way inventory businesses do. Instead, they have statements of work, time entries, milestone approvals, matter-level billing, and client-side payment behavior that doesn't always follow invoice structure.

That's why the strategic version of invoice reconciliation in a firm like yours isn't just “did the invoice exist.” It's “can we convert bank activity into an accurate AR position fast enough to manage cash, collections, and client communication with confidence.”

The Hidden Costs of Manual Reconciliation

Manual reconciliation doesn't fail all at once. It leaks time, clarity, and cash in small increments until finance starts operating from a foggy AR position.

A controller may not see the damage in a single afternoon. They see it over a month of unapplied cash, disputed balances, and follow-ups that should never have gone out.

Where the real cost shows up

The obvious cost is labor. Someone has to review the bank feed, search email for remittance detail, compare amounts, split receipts across invoices, and decide whether a short-pay is a deduction, timing issue, or client error.

The less obvious cost is decision quality.

If cash is in the bank but not correctly applied, your aging report can overstate collections risk. If deductions sit unresolved, your forecast can understate uncertainty. If a payment is posted to the wrong invoice, your team may chase the wrong balance.

Here's how the drag usually appears:

- Collections noise: AR follows up on balances that are already paid, partially paid, or under dispute.

- Forecast distortion: Finance can't cleanly separate true delinquency from unapplied cash.

- Write-off creep: Small unexplained balances stay open longer than they should.

- Partner frustration: Revenue leaders question the aging because exceptions aren't visible in one place.

Why this hurts professional services firms more than they expect

Service firms often have fewer invoices than high-volume product businesses, but each invoice carries more context. One payment may involve milestone billing, negotiated discounts, expense reimbursements, or client-specific approval chains.

That makes “just have someone review it manually” a weak answer. Manual review tends to rely on tribal knowledge. It works until a key team member is out, volume rises, or month-end pressure shortens the review.

If your reconciliation process depends on one person who “just knows” how a client pays, you don't have a process. You have a memory problem.

This is also why cash application deserves more attention than it often gets in smaller and mid-sized firms. If you want a practical bridge between incoming payments and AR accuracy, this guide to cash application in accounting is worth keeping close.

The quiet relationship cost

Clients notice when finance asks unnecessary questions.

Repeated “friendly reminders” on already-paid work make the firm look disorganized. So do emails asking a client to resend remittance that should have been captured the first time. For a professional services firm, that matters because AR communication is never only operational. It reflects directly on the brand.

A Modern Reconciliation Workflow Manual vs Automated

The strongest reason to modernize reconciliation isn't speed alone. It's control.

Manual invoice reconciliation is widely described as slow, error-prone, and difficult to scale, while modern systems are built to capture invoice data, perform matching, flag anomalies, and track operational measures like cycle time, exception rate, and straight-through processing, according to Scry AI's overview of invoice reconciliation automation.

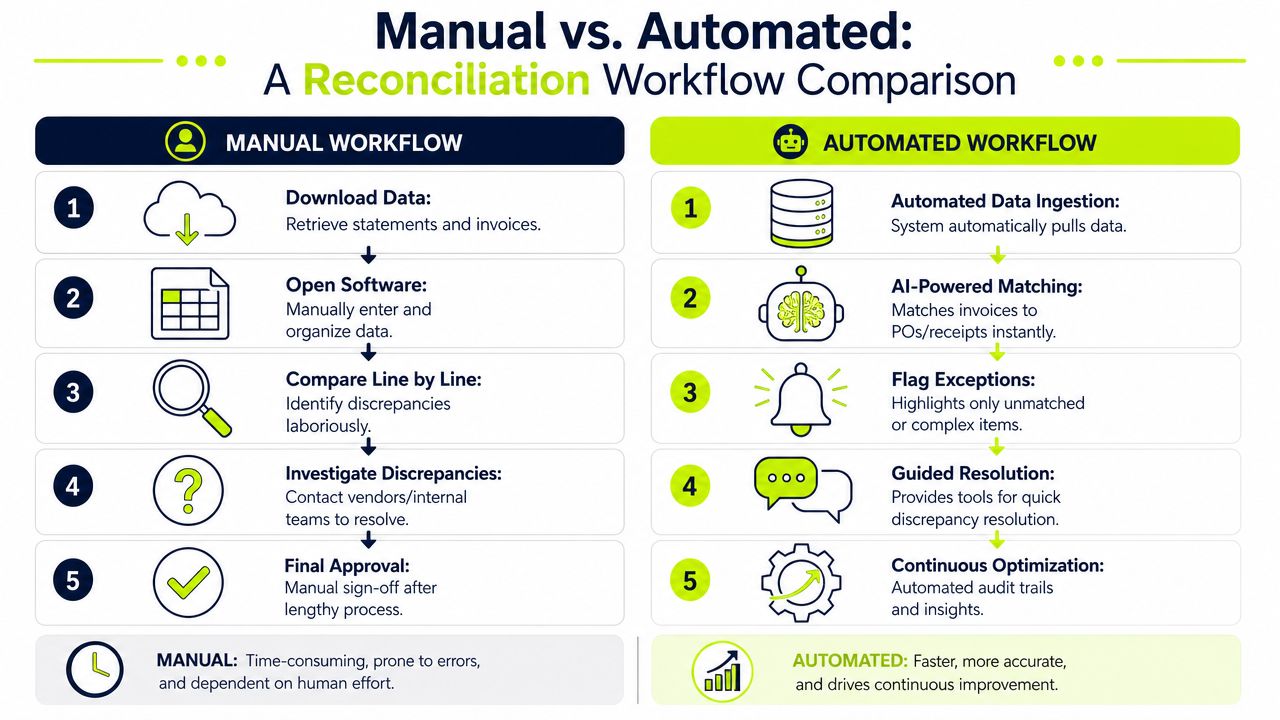

What the manual workflow actually looks like

Most firms know the steps because they're already living them.

Manual workflow | What usually goes wrong |

|---|---|

Download bank activity and payment reports | Timing gaps between systems create confusion |

Open QuickBooks or ERP and review open invoices | Staff work from stale or incomplete context |

Match amounts visually | Similar values create false matches |

Split one payment across several invoices by hand | Allocation errors are easy to introduce |

Create notes or journal entries for discrepancies | Explanations end up scattered across email and spreadsheets |

Contact client for remittance or deduction details | Resolution depends on who responds, and when |

That process is fragile because every step invites delay or inconsistency. It also leaves little audit structure unless someone is disciplined enough to document every decision.

For smaller firms and independent operators, adjacent resources can still be useful. For example, this guide on invoice matching for UK freelancers offers a practical perspective on matching workflows from a leaner operating environment.

What a modern automated workflow changes

Automation doesn't eliminate judgment. It reserves judgment for the items that actually need it.

A stronger workflow typically does the following:

- Ingests payment data automatically: Bank feeds, lockbox files, portal exports, or processor data enter the workflow without manual copying.

- Suggests likely matches: The system compares payer name, amount, invoice references, dates, and remittance signals.

- Captures support detail: Remittance emails, portal notices, or payment references are pulled into the same case.

- Routes only exceptions: Partial payments, deductions, unknown receipts, and ambiguous matches go to a review queue.

- Posts clean outcomes: Once confirmed, transactions move into the ledger with a traceable record.

A useful walkthrough of this model appears in this piece on automated payment reconciliation.

Later in the workflow, a short visual explanation can help align the team on what “good” looks like:

What works and what doesn't

What works is a system that treats reconciliation as a controlled exception process. Clean matches should pass quickly. Ambiguous items should be isolated, documented, and assigned.

What doesn't work is partial automation layered on top of spreadsheet habits. If your team still exports data to manipulate allocations offline, you've only moved the bottleneck.

There are several categories of tools in this space. QuickBooks can support the ledger side. Some firms add treasury tools, bank-feed apps, or practice management systems. Others use purpose-built accounts receivable automation platforms. Resolut, for example, includes automated cash application and payment reconciliation as part of a broader AR workflow. The right choice depends on whether your main problem is posting payments, managing exceptions, or coordinating collections and billing around the same client record.

Troubleshooting Common AR Reconciliation Roadblocks

The hardest reconciliation issues aren't theoretical. They're the exceptions that hit your team every week and refuse to fit a clean rule.

This is also the part many invoice reconciliation explainers skip. The receivables side often comes down to reconciling incoming payments that are partial, short-paid, deducted for disputes, or split across multiple invoices, which directly affects DSO and collections visibility, as highlighted by Ivalua's glossary entry on invoice reconciliation.

When a payment arrives with no usable remittance

Treat unidentified cash as a controlled exception, not a casual inbox search.

Start with the payment source, legal entity, amount pattern, and recent open balances. Check whether the client usually pays exact invoice amounts, statement totals, or rounded figures. Then hold the item in an unapplied cash queue until there's enough evidence to post confidently.

A good rule is simple:

Don't force a match just to clear the bank feed. A wrong application creates more downstream work than a short delay with documented unapplied cash.

When one payment covers many invoices

Bundled payments are common in professional services, especially with larger clients.

The wrong response is to post the full amount against the oldest invoice and plan to fix it later. The right response is to create an allocation record tied to the remittance logic, even if that means a temporary hold while the team confirms line-level intent.

Use this order of operations:

- Match explicit invoice references first.

- Apply any exact amount matches next.

- Flag the residual balance for review, not assumption.

- Document who approved the final split and why.

That approach preserves your audit trail and keeps disputes visible instead of burying them in manual adjustments.

When the client short-pays

Short-pays are where reconciliation merges with collections.

Sometimes the deduction is legitimate. Sometimes it reflects a pricing dispute, unapproved expense, service issue, or internal client process. Sometimes it's just an unsupported reduction that nobody communicated.

Your team needs a standard classification model. At minimum, separate:

- Active dispute: The client has stated a reason tied to scope, quality, timing, or contract terms.

- Administrative deduction: The payment is reduced due to client-side process issues or unsupported offsets.

- Unexplained short-pay: No defensible reason exists yet.

That classification tells collections how to respond and tells finance whether the issue belongs in AR, project management, or leadership escalation. If your payment issues also spill into card failures or retry workflows, Revcover's payment recovery insights can add useful context around recovery behavior and failed payment follow-up.

When retainers or prepayments are involved

Retainers complicate reconciliation because the cash receipt and the invoice event don't always happen at the same time.

Don't apply prepayments opportunistically to make aging look cleaner. Hold them in a clearly defined customer credit or retainer balance until the billing event supports application. Otherwise, your AR may look improved while your underlying client liability position gets messier.

From Reconciliation to Financial Control

The mature view of invoice reconciliation is simple. It is not a bookkeeping chore. It is a financial control that determines whether your AR data is believable enough to run the business.

When reconciliation is tight, finance can trust what sits in aging, what belongs in dispute, what has already been collected, and what still needs action. That improves the quality of weekly cash calls, partner reporting, and forecast conversations.

What better control looks like

A firm with strong reconciliation discipline usually has a few visible traits:

- Clean exception queues: Unapplied cash, deductions, and disputes are separated instead of blended into one AR balance.

- Reliable outreach: Collections messages go to the right client, for the right invoice, at the right time.

- Stronger forecast inputs: Finance can distinguish delayed payment from unresolved application.

- Better use of staff time: Controllers review exception patterns instead of investigating one-off mysteries all day.

The image above makes the strategic case visually, but one note matters. Those percentages appear in the graphic design brief only. If you're making an internal business case, use your own operational data rather than generic benchmark claims.

Why this matters for DSO and cash flow

If you want to reduce DSO, start by asking a blunt question. How much of your “late AR” is late, and how much is just poorly reconciled cash, unresolved deductions, or delayed application?

That distinction changes the playbook.

A collections problem needs outreach strategy, escalation paths, and payment options. A reconciliation problem needs cleaner matching, faster exception handling, and better visibility between bank activity and invoice status. Many firms need both, but they shouldn't treat them as the same issue.

Operator's view: The finance team can't improve cash flow consistently if the ledger can't tell the difference between unpaid, underpaid, disputed, and unapplied.

The practical next step

For most firms in the $3M to $50M range, the move isn't toward a giant transformation project. It's toward a cleaner operating model.

Connect the bank feed and ledger reliably. Standardize exception codes. Capture remittance in one place. Set approval rules for write-offs, deductions, and split applications. Then let accounts receivable automation handle the repetitive matching work so people can focus on exceptions and client judgment.

That's the point where AI AR automation becomes useful instead of ornamental. It helps finance move faster without sacrificing control, and it gives leadership a more credible view of cash.

Resolut automates AR for professional services with workflows for collections, payment reconciliation, and cash application that help firms keep client communication consistent and records accurate. If your team is trying to reduce DSO, improve cash flow, or make QuickBooks AR automation more dependable, Resolut is built to support that operating model. Resolut automates AR for professional services, consistent, accurate, and human.